|

市場調查報告書

商品編碼

1937286

木漿:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Wood Pulp - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

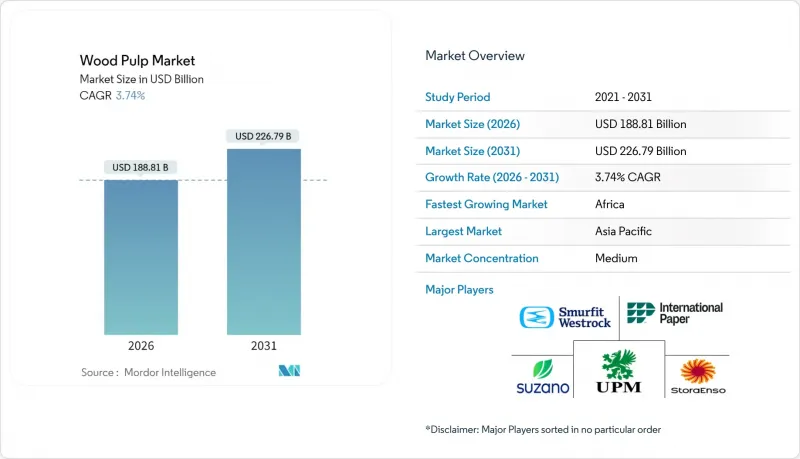

預計木漿市場規模將從 2025 年的 1,820 億美元成長到 2026 年的 1,888.1 億美元,到 2031 年將達到 2,267.9 億美元,2026 年至 2031 年的複合年成長率為 3.74%。

這一穩定成長主要得益於需求從印刷用紙轉向瓦楞紙包裝和吸水性衛生紙。生產商正日益關注電商主導的箱板紙、高檔衛生紙和特種紙漿,這些產品的利潤率高於傳統印刷用紙。儘管原料價格波動,但造紙廠的持續升級、生物精煉廠的整合以及人工智慧驅動的流程管理進一步穩定了收入。區域需求模式差異顯著,亞太地區引領銷售成長,非洲持續以小規模擴張,而北美和歐洲則轉向高價值的細分市場。跨境關稅,特別是美國對加拿大紙漿進口徵收的關稅,正在擾亂現有的貿易格局,迫使生產商要么承受利潤壓縮,要么在亞太地區開發替代市場。

全球木漿市場趨勢與洞察

電子商務推動瓦楞紙包裝需求激增

線上零售的成長正在加速瓦楞紙箱的消費,而瓦楞紙箱需要大量使用牛皮紙襯裡和由商品紙漿製成的瓦楞芯材。國際紙業指出,隨著電商客戶補充庫存,箱板紙的需求將在2024年復甦。新成立的斯莫菲特-韋斯特洛克公司預計,其專注於包裝業務的投資組合在2024年將實現47億美元的調整後EBITDA。與傳統零售相比,面向消費者的直接配送的保護性運輸方式提高了每個包裹的纖維用量。這一趨勢在中國、印度和美國最為顯著,這些國家的大批量小包裹配送與優先使用紙張而非塑膠的永續性理念相契合。造紙廠正在透過將印刷紙機改造為箱板紙生產線來應對這一趨勢,從而透過增加原料供應來刺激木漿市場。數位貿易的結構性發展勢頭為紙漿的長期消費奠定了基礎,即使在宏觀經濟週期波動的情況下也是如此。

新興經濟體紙巾和衛生用品消費成長

亞太和非洲的人均紙巾消費量仍遠低於歐洲和北美。國際紙業公司約90%的吸水紙漿出口銷往這些高成長地區,凸顯了市場需求缺口。可支配收入的成長、都市化的加快以及衛生意識的提高,正在推動對高純度紙漿製成的高檔紙巾和尿布產品的需求。由於家庭用紙的需求不受景氣衰退的影響,這項需求因素正在推動木漿市場銷售穩定成長,並與週期性更強的包裝市場形成平衡。在新興市場,供應量超過消費量,使得擁有絨毛漿產能的生產商能夠獲得可觀的利潤。長期人口趨勢表明,這種成長勢頭將持續到預測期之後。

紙漿木材價格波動與氣候變遷和物流中斷有關

2024年,風暴、乾旱和運輸瓶頸導致北歐紙漿材價格飆升至歷史新高,迫使比勒魯德公司提高產品價格以維持利潤。北美也遭遇了類似的供應衝擊,暴露出對易受極端天氣影響的卡車和鐵路運輸路線的依賴。價格飆升壓縮了紙漿銷售價格與原料成本之間的邊際收益,導致造紙廠推遲自願升級改造計畫。中小企業缺乏避險工具和合約談判能力,增加了破產風險。雖然長期植樹造林計劃可能緩解供應緊張,但短期價格波動仍是限制木漿市場成長的主要因素。

細分市場分析

木漿市場規模正受到纖維偏好變化和永續性趨勢的影響。到2025年,硬木纖維將佔木漿市場佔有率的47.25%,這主要得益於桉樹和樺樹人工林,它們提供的短纖維特性使其在衛生紙、印刷和輕質包裝等領域備受青睞。亞太地區,特別是中國和印尼的人工林,透過向國內加工商和出口工廠提供價格具競爭力的硬木原料,進一步鞏固了這一優勢。來自北歐和北美森林的軟木纖維對於箱板紙和麻袋紙等對長纖維強度要求極高的應用仍然至關重要。然而,生產商正日益精細地調整硬木與軟木的混合比例,以在控制原料成本的同時達到性能目標。隨著工廠不斷最佳化配比,即使整個木漿市場的籌資策略不斷演變,硬木仍將繼續保持其作為產量基礎的地位。

預計非木材替代品將以最快的速度成長,在2026年至2031年間以5.07%的複合年成長率成長,因為永續性的迫切需求推動了資源多樣化。在集約化耕作地區,小麥秸稈、稻殼和甘蔗渣等農業殘餘物提供了豐富的纖維來源,而竹子具有快速的再生週期,對注重環保的品牌和監管機構極具吸引力。 UPM與Sodra在木質素萃取方面的合作表明,生產商正在探索新的增值途徑,以補充非木材纖維的利用。

區域分析

亞太地區佔全球木漿市場的48.05%,支撐著全球需求。中國消耗了全球整體超過三分之一的箱板紙,印度的衛生紙市場正經歷兩位數的成長。巴西、印尼和越南的人工林為中國加工商提供低成本纖維,增強了該地區的規模優勢。日本和韓國依賴進口高純度紙漿用於特殊用途,而澳洲則向本國造紙廠出口人工林桉木片。投資改造現有造紙廠,消除產能瓶頸,並建造新的大型單一製程造紙廠,將確保亞太地區的供應安全,並使其在全球價格中保持影響力。

儘管非洲木漿市場規模相對小規模,但南非的綜合林業和造紙資產為其在非洲大陸提供了戰略基礎。 Sappi公司108億蘭特(約6億美元)的投資正在加速現代化進程,提升區域互聯互通,改善原料供應鏈,並提高社會認可度。加強德班港和馬布多的物流能力旨在縮短出口到歐洲和亞洲的前置作業時間。新興的北非生產商正利用接近性歐洲終端用戶中心的優勢,助力非洲大陸實現2031年5.55%的複合年成長率。

北美和歐洲的需求結構已趨於成熟。美國纖維原料供應充足,但面臨關稅爭端帶來的挑戰,導致分銷管道轉向亞洲。加拿大西部生產商正將業務拓展至美國以外的市場,以降低關稅風險。歐洲優先發展生物精煉煉製和塑膠替代,儘管印刷用紙消費量下降,但特種紙仍保持成長。日益嚴格的環境法規增加了合規成本,但也刺激了創新,推動了木漿市場高級產品的差異化。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 電子商務推動紙板包裝需求激增

- 新興國家紙巾和衛生用品消費成長

- 由於永續性要求,用纖維取代塑膠

- 亞太地區硬木牛皮紙漿廠擴建計劃

- 透過生物精煉一體化開發木質素和半纖維素的收入來源

- 人工智慧驅動的預測性維護可提高工廠使用率和生產效率

- 市場限制

- 氣候變遷和物流中斷導致紙漿木材價格波動

- 加強廢水和化學品排放的監管

- 由於技術純熟勞工短缺,新建設和維修計劃延誤。

- 跨境關稅重塑紙漿貿易流向

- 監管環境

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按原料

- 針葉樹

- 硬木

- 非木質纖維

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 英國

- 法國

- 芬蘭

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東地區

- 非洲

- 南非

- 埃及

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Suzano SA

- International Paper Company

- Stora Enso Oyj

- UPM-Kymmene Oyj

- Smurfit WestRock plc

- Metsaliitto Cooperative

- Sappi Limited

- Celulosa Arauco y Constitucion SA(Empresas Copec SA)

- Asia Pulp & Paper Co. Ltd.(Sinar Mas Group)

- Mercer International Inc.

- Canfor Pulp Products Inc.(Canfor Corporation)

- Paper Excellence BV

- Klabin SA

第7章 市場機會與未來展望

The wood pulp market is expected to grow from USD 182.00 billion in 2025 to USD 188.81 billion in 2026 and is forecast to reach USD 226.79 billion by 2031 at 3.74% CAGR over 2026-2031.

A shift away from graphic paper and toward corrugated packaging and absorbent hygiene grades underpins this steady advance. Producers deepen their focus on e-commerce-driven containerboard, premium tissue, and specialty pulps that carry higher margins than legacy printing grades. Continual mill upgrades, bio-refinery integration, and AI-enabled process control further stabilize earnings despite raw-material volatility. Geographic demand patterns diverge sharply as Asia-Pacific drives volume, Africa expands from a small base, and North America and Europe pivot to value-added niches. Cross-border tariffs, particularly duties imposed on Canadian pulp imports to the United States, disrupt established trade patterns and force producers to absorb margin compression or seek alternative markets in Asia-Pacific regions.

Global Wood Pulp Market Trends and Insights

E-commerce-driven Corrugated-packaging Demand Surge

Online retail growth intensifies the consumption of corrugated boxes that use high volumes of kraft liner and medium produced from market pulp. International Paper noted containerboard volume recovery in 2024 as e-commerce clients replenished stocks, and the newly formed Smurfit WestRock projects USD 4.7 billion in adjusted EBITDA for 2024 from its packaging-heavy portfolio. Protective shipping formats for direct-to-consumer deliveries raise fiber intensity per package versus traditional retail. The trend is most pronounced in China, India, and the United States, where high parcel volumes intersect with sustainability mandates that favor paper over plastic. Mill operators respond by converting graphic-paper machines to containerboard, boosting the wood pulp market through incremental furnish demand. Digital trade's structural momentum supports long-run pulp consumption even as macro cycles fluctuate.

Growth in Tissue and Hygiene Consumption in Emerging Economies

Per-capita tissue use in Asia-Pacific and Africa remains well below levels observed in Europe and North America. International Paper directs roughly 90% of absorbent pulp exports to these high-growth regions, underscoring the demand gap. Rising disposable incomes, urbanization, and heightened hygiene awareness lift uptake of premium tissue and diaper products that rely on high-purity pulps. Because household paper demand is relatively recession-resilient, this driver provides consistent volume growth for the wood pulp market, balancing more cyclical packaging segments. Producers with fluff-pulp capacity enjoy favorable margins as supply lags consumption in emerging markets. Long-term demographic trends point to sustained expansion well beyond the forecast horizon.

Volatile Pulpwood Prices Tied to Climate and Logistics Shocks

Storm damage, drought, and transport bottlenecks lifted Nordic pulpwood prices to record levels in 2024, forcing Billerud to raise product prices to preserve margins. Similar supply shocks in North America exposed dependence on truck and rail corridors vulnerable to extreme weather. Price spikes compress spreads between pulp realizations and fiber costs, delaying discretionary mill upgrades. Smaller firms lack hedging tools and contractual leverage, heightening bankruptcy risk. While long-term plantation projects may ease tightness, near-term volatility remains a key brake on wood pulp market growth.

Other drivers and restraints analyzed in the detailed report include:

- Plastic-to-fiber Substitution Prompted by Sustainability Mandates

- Capacity Additions of Hardwood Kraft Mills in Asia-Pacific

- Tightening Wastewater and Chemical-emissions Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Wood pulp market size is being shaped by shifting fiber preferences and sustainability trends. Hardwood fibers captured 47.25% of the wood pulp market share in 2025, supported by eucalyptus and birch plantations that deliver short-fiber characteristics prized in tissue, printing, and lightweight packaging applications. Asia-Pacific plantations in China and Indonesia reinforce this advantage by supplying domestic converters and export mills with competitively priced hardwood furnish. Softwood fibers from Nordic and North American forests retain relevance where long-fiber strength is critical, such as containerboard and sack paper, yet producers increasingly fine-tune hardwood-softwood blends to hit performance targets while curbing raw-material costs. As mills optimize recipes, hardwood continues to anchor volume even as procurement strategies evolve across the wood pulp market.

Non-wood alternatives are set to grow fastest, advancing at a 5.07% CAGR from 2026 to 2031 as sustainability mandates push the industry toward resource diversification. Agricultural residues such as wheat straw, rice husks, and sugarcane bagasse supply abundant fiber streams in intensive farming regions, while bamboo offers rapid regrowth cycles attractive to environmentally conscious brands and regulators. UPM's collaboration with Sodra on lignin extraction underlines how producers explore new valorization pathways that complement non-wood fiber utilization.

The Wood Pulp Market Report is Segmented by Fiber Source (Hardwood, Softwood, Non-Wood Fibers) and Geography (North America, Europe, Asia-Pacific, South America, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific's 48.05% wood pulp market share anchors global demand, with China consuming more than one-third of worldwide corrugated liner shipments and India recording double-digit tissue growth. Plantation forestry across Brazil, Indonesia, and Vietnam channels low-cost fiber into Chinese converters, reinforcing the region's scale advantage. Japan and South Korea rely on high-purity imports for specialty applications, while Australia exports plantation eucalyptus chips to regional mills. Investments in brownfield debottlenecking and new single-phase mega-mills safeguard Asia-Pacific's supply security and global price influence.

Africa's wood pulp market size remains comparatively modest, yet South Africa's integrated forestry and mill assets give the continent a strategic foothold. Sappi's R10.8 billion (USD 600 million) commitment accelerates modernization and community engagement, improving raw-material flows and social license to operate. Logistical upgrades at Durban and Maputo ports aim to cut export lead times to Europe and Asia. Emerging North African producers leverage proximity to European end-users, supporting the continent's 5.55% CAGR through 2031.

North America and Europe exhibit mature demand profiles. The United States maintains surplus fiber availability but wrestles with tariff disputes that redirect flows toward Asia. Canada's Western producers diversify beyond U.S. markets to offset duty exposure. Europe prioritizes bio-refinery projects and plastic substitution, sustaining specialty-grade growth despite shrinking graphic-paper consumption. Stricter environmental regulations raise compliance costs but also encourage innovation that differentiates premium offerings within the wood pulp market.

- Suzano S.A.

- International Paper Company

- Stora Enso Oyj

- UPM-Kymmene Oyj

- Smurfit WestRock plc

- Metsaliitto Cooperative

- Sappi Limited

- Celulosa Arauco y Constitucion S.A. (Empresas Copec S.A.)

- Asia Pulp & Paper Co. Ltd. (Sinar Mas Group)

- Mercer International Inc.

- Canfor Pulp Products Inc. (Canfor Corporation)

- Paper Excellence B.V.

- Klabin S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce driven corrugated-packaging demand surge

- 4.2.2 Growth in tissue and hygiene consumption in emerging economies

- 4.2.3 Plastic-to-fiber substitution prompted by sustainability mandates

- 4.2.4 Capacity additions of hardwood kraft mills in Asia-Pacific

- 4.2.5 Bio-refinery integration unlocking lignin and hemicellulose revenue streams

- 4.2.6 AI-enabled predictive maintenance boosting mill uptime and yield

- 4.3 Market Restraints

- 4.3.1 Volatile pulpwood prices tied to climate and logistics shocks

- 4.3.2 Tightening wastewater and chemical-emissions regulations

- 4.3.3 Skilled-labor shortages delaying greenfield and retrofit projects

- 4.3.4 Cross-border tariffs reshaping pulp trade flows

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Fiber Source

- 5.1.1 Softwood

- 5.1.2 Hardwood

- 5.1.3 Non-wood Fibers

- 5.2 By Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Finland

- 5.2.2.5 Russia

- 5.2.2.6 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 Australia

- 5.2.3.5 South Korea

- 5.2.3.6 Rest of Asia-Pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle East

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 Rest of Middle East

- 5.2.6 Africa

- 5.2.6.1 South Africa

- 5.2.6.2 Egypt

- 5.2.6.3 Rest of Africa

- 5.2.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Suzano S.A.

- 6.4.2 International Paper Company

- 6.4.3 Stora Enso Oyj

- 6.4.4 UPM-Kymmene Oyj

- 6.4.5 Smurfit WestRock plc

- 6.4.6 Metsaliitto Cooperative

- 6.4.7 Sappi Limited

- 6.4.8 Celulosa Arauco y Constitucion S.A. (Empresas Copec S.A.)

- 6.4.9 Asia Pulp & Paper Co. Ltd. (Sinar Mas Group)

- 6.4.10 Mercer International Inc.

- 6.4.11 Canfor Pulp Products Inc. (Canfor Corporation)

- 6.4.12 Paper Excellence B.V.

- 6.4.13 Klabin S.A.

7 Market Opportunities and Future Outlook

漂白桉樹牛皮紙漿市場:依等級、產品形式、應用、通路,全球預測(2026-2032年)全球漂白硬木牛皮紙漿市場(按漂白技術、等級、紙漿形態、應用和分銷管道分類)預測(2026-2032年)北方漂白軟木牛皮紙市場按產品等級、認證、應用、最終用途和分銷管道分類 - 全球預測(2026-2032 年)漂白軟木牛皮紙市場按等級、應用、終端用戶產業和銷售管道,全球預測(2026-2032年)

漂白桉樹牛皮紙漿市場:依等級、產品形式、應用、通路,全球預測(2026-2032年)全球漂白硬木牛皮紙漿市場(按漂白技術、等級、紙漿形態、應用和分銷管道分類)預測(2026-2032年)北方漂白軟木牛皮紙市場按產品等級、認證、應用、最終用途和分銷管道分類 - 全球預測(2026-2032 年)漂白軟木牛皮紙市場按等級、應用、終端用戶產業和銷售管道,全球預測(2026-2032年) 日本木漿市場規模、佔有率、趨勢及預測(按類型、等級、最終用途行業和地區分類),2026-2034年

日本木漿市場規模、佔有率、趨勢及預測(按類型、等級、最終用途行業和地區分類),2026-2034年 木漿市場規模、佔有率和成長分析(按類型、製造流程、最終用途產業和地區分類)-2026-2033年產業預測

木漿市場規模、佔有率和成長分析(按類型、製造流程、最終用途產業和地區分類)-2026-2033年產業預測 漂白尤加利牛皮紙漿市場:全球2025-2029年

漂白尤加利牛皮紙漿市場:全球2025-2029年 全球木漿市場規模按產品類型、應用、最終用戶產業、地區、範圍和預測劃分

全球木漿市場規模按產品類型、應用、最終用戶產業、地區、範圍和預測劃分 越南硫酸鹽紙漿進口:2024-2033

越南硫酸鹽紙漿進口:2024-2033