|

市場調查報告書

商品編碼

1937283

資料中心液冷:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Data Center Liquid Cooling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

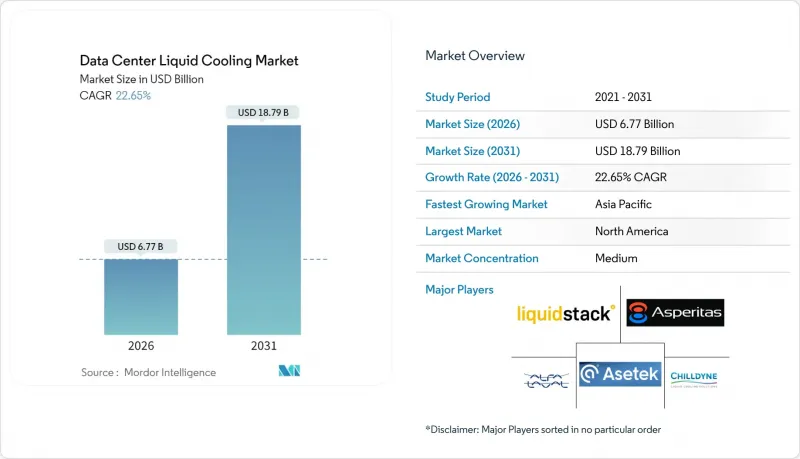

2025年資料中心液冷市場價值為55.2億美元,預計到2031年將達到187.9億美元,高於2026年的67.7億美元。

預測期(2026-2031 年)的複合年成長率預計為 22.65%。

機架密度超過 30kW、GPU 在人工智慧模型中的加速應用以及日益嚴格的永續性法規,共同促使液冷成為現代設施的核心架構要求。雖然可改造現有機架的晶片級直接冷卻解決方案仍佔據主導地位,但隨著營運商尋求更高的散熱效率,兩相浸沒式冷卻系統正以最快的速度成長。超大規模雲端服務供應商正將初始試點專案過渡到全機群部署,而集中的需求正在降低企業和託管用戶的單價。同時,促進熱能再利用和低碳化的政策獎勵正在推動北美、歐洲和部分亞太地區採用液冷技術。

全球資料中心液冷市場趨勢與洞察

快速提高機架密度會增加對液冷的需求

當資料中心營運商部署 NVIDIA H200 GPU 時,每台設備將面臨 700W 的熱負荷,而風冷無法以經濟高效的方式將其排出。雖然處理器效能比上一代提升高達 1.9 倍,業者可以減少所需的伺服器數量,但他們必須有效地散發集中的熱量。因此,液冷從一種可選的節能措施轉變為必不可少的基礎設施,它能夠在不超出設施電源使用效率 (PUE)閾值下實現更高的密度。隨著每機架每千瓦功耗超過 20kW,營運商將轉向液冷解決方案,資料中心液冷市場也將從中直接受益。

超大規模企業的淨零排放承諾加速了這一趨勢的實現。

大型雲端服務公司已承諾在所有資料中心實現淨零排放,並指出液冷系統相比傳統風冷系統可節能 20%。歐洲法規進一步強制要求 1MW 以上的資料中心進行熱回收,加速了簡化熱回收的液冷架構的普及。這些自願性和監管性舉措的結合,使得液冷既成為一種合規性基礎設施,又成為一種提升營運效率的策略,從而擴大了資料中心液冷市場的覆蓋範圍,使其不再局限於早期採用者。

缺乏現場專業知識限制了實施速度。

液冷系統需要管道安裝、洩漏檢測和水泵選型等方面的技能,而許多傳統資料中心人員恰恰缺乏這些技能。雖然培訓計畫正在不斷擴展,但在人才儲備進一步充足之前,液冷系統的實施週期可能比風冷計劃更長。

細分市場分析

2025年,直接晶片冷卻解決方案將佔據資料中心液冷市場42.85%的佔有率,預計近期仍將維持成長動能。營運商青睞這些解決方案對CPU和中功率GPU的即插即用特性。身臨其境型解決方案的市場規模將以26.62%的複合年成長率快速成長,這主要得益於對需要極強散熱能力的AI訓練叢集的需求。資料中心正朝著混合型方向發展,中階機架採用後門式熱交換器、GPU島採用浸沒式冷卻槽的趨勢日益明顯。包括Invented在內的台灣公司提交的專利申請也印證了該技術發展的持續動能。

作為次要影響,零件供應商正在重新設計泵浦、閥門和快速接頭,以適應更高的流量和對非導電流體的耐受性。產品標準化程度的提高縮短了採購週期,降低了總安裝成本,並加速了技術更新換代。

由於供應鏈成熟,單相碳氫化合物將在2025年佔據資料中心液冷市場最大佔有率。然而,具有更高傳熱係數的雙相氟化碳氫化合物預計將以25.64%的複合年成長率成長。 3M公司計劃逐步淘汰含PFAS的冷卻液,這正在重組其採購結構,而中國特種化學品製造商正在填補半導體和伺服器冷卻液需求的替代供應。英國等政府正在資助下一代低全球暖化潛勢冷卻液的研究,加速向更環保化學品的更廣泛轉型。將節水作為首要任務的設施也考慮採用乙二醇混合物。含有金屬氧化物和奈米碳管的奈米流體仍處於測試階段,但測試結果顯示其導熱係數提高了10-15%,預計在未來十年內將實現更薄的冷板。

區域分析

北美在超大規模資本投資和稅收優惠方面繼續保持主導。堪薩斯州對超過2.5億美元的資料中心投資提供20年的銷售稅豁免,而馬薩諸塞州則對超過5000萬美元的計劃提供類似的豁免。通膨控制法使得清潔能源補貼更具盈利,並推動許多新建設採用更流動性的設計。

歐洲是第二大成長引擎。能源效率指令要求對超過1兆瓦的資料中心進行熱回收評估,而斯堪地那維亞半島的區域供熱網路則為回收的熱能提供經濟的購買價格。法國為在電力效率方面具有優勢的設施提供能源稅減免。這些法規將液冷系統從一種節能選項提升為一項合規要求,尤其是在已經存在水側節熱器的環境中。

亞太地區是資料中心液冷市場成長最快的區域市場。中國正在填補3M公司因PFAS產品停產而造成的冷卻液供應缺口;在日本,公用事業公司正在鼓勵使用節能型運算節點。印度特倫甘納邦和北方邦的資料中心扶持政策推動了快速的數位化,使得新建資料中心能夠直接過渡到液冷架構。台灣製造商,尤其是ING大學,在全球專利申請和整合冷板組件出口方面主導。

非洲、拉丁美洲和中東雖然面積不大,但具有重要的戰略意義。在這些地區,炎熱的氣候和高成本的電力成本使得風冷系統吸引力下降,從而開闢了一個利基市場,緊湊型浸入式水槽可以用最少的機械設備處理電信和金融科技的工作負載。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 人工智慧和高效能運算設施中機架密度不斷提高(超過 30kW)

- 超大規模業者的淨零排放藍圖加速了流動性的採用

- OEM保固現在涵蓋直接連接到尖端的線圈

- NVIDIA 和 AMD 液冷參考設計引領生態系統

- 政府對綠色資料中心的激勵措施(例如歐盟分類法)將支持資本支出(CAPEX)。

- 利用餘熱再利用的區域供熱能夠實現獲利性的營運成本節約。

- 市場限制

- 設施工程師的現場專業知識有限。

- 現有設施維修的初始成本很高

- 流體材質相容性問題(長期密封件、PCB)

- 特殊介電液供應風險

- 產業價值鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅(先進空氣、兩相二氧化碳)

- 競爭程度

第5章 市場規模與成長預測

- 依冷卻技術進行分段

- 浸沒式冷卻

- 晶片級液冷

- 後門熱交換器(RDHx)

- 冷板/姻親液冷系統

- 依冷卻液類型細分

- 單相烴流體

- 兩相氟化液

- 水/乙二醇溶液

- 奈米流體和其他特殊液體

- 依資料中心類型細分

- 超大規模

- 搭配

- 企業/本地部署

- 邊緣微資料中心

- 按應用程式/工作負載進行細分

- 高效能運算(HPC)

- 人工智慧/機器學習

- 加密貨幣挖礦

- 雲端運算和虛擬化

- 區域細分

- 北美洲

- 美國

- 加拿大

- 南美洲

- 巴西

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 荷蘭

- 俄羅斯

- 其他歐洲

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 其他亞太地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 非洲

- 南非

- 其他中東和非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Alfa Laval Corporate AB

- Asetek A/S

- Asperitas BV

- Chilldyne Inc.

- CoolIT Systems Inc.

- Fujitsu Ltd.

- Kaori Heat Treatment Co., Ltd.

- Lenovo Group Ltd.

- LiquidStack Inc.

- LiquidCool Solutions Inc.

- Iceotope Technologies Ltd.

- Rittal GmbH and Co. KG

- Schneider Electric SE

- Submer Technologies SL and Submer Inc.

- Vertiv Group Corp.

- Wiwynn Corporation

- 3M Company

- Engineered Fluids Inc.

- Green Revolution Cooling Inc.

- Solvay SA

- Mikros Technologies

- Midas Green Technologies LLC

- USystems Ltd.(Legrand Group)

第7章 市場機會與未來展望

The data center liquid cooling market was valued at USD 5.52 billion in 2025 and estimated to grow from USD 6.77 billion in 2026 to reach USD 18.79 billion by 2031, at a CAGR of 22.65% during the forecast period (2026-2031).

Rising rack densities above 30 kW, the accelerating use of graphics processing units for AI models, and tighter sustainability mandates are converging to make liquid cooling a core architectural requirement for modern facilities. Direct-to-chip solutions continue to dominate because they retrofit into existing racks, while two-phase immersion systems are advancing fastest as operators pursue still higher thermal efficiencies. Hyperscale cloud providers are translating early pilots into fleet-wide rollouts, and their aggregated demand is lowering unit costs for enterprise and colocation buyers. Meanwhile, policy incentives that favour heat re-use and lower carbon intensity are reinforcing liquid adoption across North America, Europe, and selected Asia-Pacific (APAC) hubs.

Global Data Center Liquid Cooling Market Trends and Insights

Surging rack densities drive liquid cooling necessity

Data center operators deploying NVIDIA H200 GPUs face 700 W thermal loads per device, and air cooling cannot cost-effectively remove that heat at volume. With processors delivering up to 1.9 times prior-generation performance, operators can shrink server counts but must dissipate concentrated heat. Liquid cooling, therefore, shifts from an optional efficiency measure to indispensable infrastructure, enabling higher density without blowing past facility power-usage-effectiveness thresholds. The data center liquid cooling market benefits directly because every incremental kilowatt above 20 kW per rack pushes operators toward liquid solutions.

Hyperscale net-zero commitments accelerate adoption

Cloud giants have pledged fleet-wide net-zero emissions and see liquid cooling as a 20% energy-reduction lever compared with legacy air systems. European regulations further require heat recovery from data centers above 1 MW, intensifying uptake of liquid architectures that simplify thermal capture. These combined voluntary and regulatory forces turn liquid cooling into a compliance infrastructure as well as an operational efficiency strategy, expanding the data center liquid cooling market beyond early adopters.

Limited field expertise constrains deployment velocity

Liquid systems demand skills in pipe fitting, leak detection, and pump sizing that many legacy data center staff lack. Training programs are expanding, but until the talent pool deepens, roll-out schedules will remain lengthier than air-based projects.

Other drivers and restraints analyzed in the detailed report include:

- OEM warranty coverage reduces deployment risk

- Semiconductor reference designs standardize implementation

- Retrofit costs challenge brown-field adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Direct-to-chip captured 42.85% of the 2025 data center liquid cooling market share and will continue to anchor short-term growth. Operators favour its drop-in nature for CPUs and moderate-power GPUs. The data center liquid cooling market size for immersion solutions will climb fastest at a 26.62% CAGR, helped by AI training clusters that need extreme heat flux removal. Facilities are increasingly hybrid, using rear-door heat exchangers for moderate racks and immersion baths for GPU islands. Patent filings by Invented and other Taiwanese firms underscore sustained engineering momentum.

A second-order effect is that component suppliers are redesigning pumps, valves, and quick-disconnects to tolerate higher flow rates and non-conductive fluids. As products standardize, procurement cycles shorten and total installed cost falls, reinforcing the technology shift.

Single-phase hydrocarbons accounted for the largest slice of the data center liquid cooling market size in 2025 due to mature supply chains. However, two-phase fluorocarbons deliver stronger heat-transfer coefficients and will post a 25.64% CAGR. 3M's scheduled phase-out of PFAS fluids is reshaping sourcing; Chinese specialty chemical makers are stepping in to backfill demand for semiconductor and server coolant buyers. Governments such as the United Kingdom are funding research into next-generation, low-global-warming-potential fluids, accelerating a broader shift to environmentally aligned chemistries. Operators are also exploring glycol mixes for facilities where water conservation is paramount. Nanofluids, infused with metal oxides or carbon nanotubes, remain at pilot stage, but test results suggest 10-15% conductivity gains that could unlock thinner cold plates in the coming decade.

The Data Center Liquid Cooling Market Report is Segmented by Cooling Technology (Immersion Cooling, Direct-To-Chip Liquid Cooling, and More), Coolant Type (Single-Phase Hydrocarbon Fluids, Two-Phase Fluorocarbon Fluids, and More), Data Center Type (Hyperscale, Colocation, Enterprise, and More), Application (HPC, AI/ML, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America preserves its lead position thanks to hyperscale capex and pro-investment tax regimes. Kansas grants 20-year sales-tax holidays on data center spending above USD 250 million, and Massachusetts offers similar exemptions for projects over USD 50 million. The Inflation Reduction Act further augments returns with clean-energy credits, tipping many new builds toward liquid-ready designs.

Europe is the second growth engine. The Energy Efficiency Directive obliges data centers above 1 MW to evaluate heat recovery, and Scandinavian district-heating grids provide an economic off-take route for captured thermal energy. France rewards facilities that prove superior power-usage effectiveness with reduced energy taxes. Collectively, these rules elevate liquid systems from an efficiency choice to a compliance requirement, especially where water-side economizers already exist.

APAC represents the fastest-growing regional slice of the data center liquid cooling market. China is bridging the coolant gap created by 3M's PFAS exit, while Japan's utilities incentivize energy-efficient compute nodes. India's rapid digitalization, supported by dedicated data-center-friendly policies in Telangana and Uttar Pradesh, provides greenfield opportunities to leapfrog directly into liquid architectures. Taiwanese manufacturers, headlined by Inventec, dominate global patent filings and are exporting integrated cold-plate assemblies worldwide.

Africa, Latin America, and the Middle East remain smaller but strategic. Their hot climates and costly power make air systems less attractive, opening niches where compact immersion baths can serve telecom and fintech workloads with minimal mechanical plant.

- Alfa Laval Corporate AB

- Asetek A/S

- Asperitas BV

- Chilldyne Inc.

- CoolIT Systems Inc.

- Fujitsu Ltd.

- Kaori Heat Treatment Co., Ltd.

- Lenovo Group Ltd.

- LiquidStack Inc.

- LiquidCool Solutions Inc.

- Iceotope Technologies Ltd.

- Rittal GmbH and Co. KG

- Schneider Electric SE

- Submer Technologies SL and Submer Inc.

- Vertiv Group Corp.

- Wiwynn Corporation

- 3M Company

- Engineered Fluids Inc.

- Green Revolution Cooling Inc.

- Solvay SA

- Mikros Technologies

- Midas Green Technologies LLC

- USystems Ltd. (Legrand Group)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging rack densities (>30 kW) in AI and HPC facilities

- 4.2.2 Hyperscale operators' net-zero roadmaps accelerating liquid adoption

- 4.2.3 OEM warranties now covering direct-to-chip loops

- 4.2.4 Nvidia and AMD liquid-ready reference designs driving ecosystem

- 4.2.5 Government incentives for green DCs (e.g., EU Taxonomy) underwrite CAPEX

- 4.2.6 Re-use of waste-heat for district heating monetises OPEX savings

- 4.3 Market Restraints

- 4.3.1 Limited field expertise among facility engineers

- 4.3.2 High upfront retrofit costs for brown-field sites

- 4.3.3 Fluid material-compatibility concerns (long-term seals, PCB)

- 4.3.4 Supply risk of specialty dielectric fluids

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes (advanced air, two-phase CO?)

- 4.7.5 Degree of Competition

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 Segmentation by Cooling Technology

- 5.1.1 Immersion Cooling

- 5.1.2 Direct-to-Chip Liquid Cooling

- 5.1.3 Rear-Door Heat Exchangers (RDHx)

- 5.1.4 Cold-Plate / In-row Liquid Systems

- 5.2 Segmentation by Coolant Type

- 5.2.1 Single-Phase Hydrocarbon Fluids

- 5.2.2 Two-Phase Fluorocarbon Fluids

- 5.2.3 Water / Glycol Solutions

- 5.2.4 Nanofluids and Other Specialty Liquids

- 5.3 Segmentation by Data Center Type

- 5.3.1 Hyperscale

- 5.3.2 Colocation

- 5.3.3 Enterprise / On-Premise

- 5.3.4 Edge and Micro DCs

- 5.4 Segmentation by Application / Workload

- 5.4.1 High-Performance Computing (HPC)

- 5.4.2 Artificial Intelligence / Machine Learning

- 5.4.3 Cryptocurrency Mining

- 5.4.4 Cloud and Virtualisation

- 5.5 Segmentation by Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Netherlands

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 APAC

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 Australia

- 5.5.4.5 Rest of APAC

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of MEA

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)

- 6.4.1 Alfa Laval Corporate AB

- 6.4.2 Asetek A/S

- 6.4.3 Asperitas BV

- 6.4.4 Chilldyne Inc.

- 6.4.5 CoolIT Systems Inc.

- 6.4.6 Fujitsu Ltd.

- 6.4.7 Kaori Heat Treatment Co., Ltd.

- 6.4.8 Lenovo Group Ltd.

- 6.4.9 LiquidStack Inc.

- 6.4.10 LiquidCool Solutions Inc.

- 6.4.11 Iceotope Technologies Ltd.

- 6.4.12 Rittal GmbH and Co. KG

- 6.4.13 Schneider Electric SE

- 6.4.14 Submer Technologies SL and Submer Inc.

- 6.4.15 Vertiv Group Corp.

- 6.4.16 Wiwynn Corporation

- 6.4.17 3M Company

- 6.4.18 Engineered Fluids Inc.

- 6.4.19 Green Revolution Cooling Inc.

- 6.4.20 Solvay SA

- 6.4.21 Mikros Technologies

- 6.4.22 Midas Green Technologies LLC

- 6.4.23 USystems Ltd. (Legrand Group)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026-2030年全球人工智慧資料中心液冷市場

2026-2030年全球人工智慧資料中心液冷市場 人工智慧資料中心液冷市場:2034 年預測-按冷卻方式、組件、冷卻劑類型、技術、最終用戶和地區分類的全球分析

人工智慧資料中心液冷市場:2034 年預測-按冷卻方式、組件、冷卻劑類型、技術、最終用戶和地區分類的全球分析 資料中心液冷市場:依冷卻技術、組件、液體類型、基礎架構層、資料中心類型、最終用戶產業和資料中心規模分類-2026年至2032年全球市場預測

資料中心液冷市場:依冷卻技術、組件、液體類型、基礎架構層、資料中心類型、最終用戶產業和資料中心規模分類-2026年至2032年全球市場預測 資料中心液冷市場報告:按組件、資料中心類型、最終用途、應用和地區分類(2026-2034 年)

資料中心液冷市場報告:按組件、資料中心類型、最終用途、應用和地區分類(2026-2034 年) 全球資料中心液冷市場:按組件、最終用戶、冷卻介質、資料中心類型、冷卻類型、企業和地區分類 - 預測(至 2033 年)

全球資料中心液冷市場:按組件、最終用戶、冷卻介質、資料中心類型、冷卻類型、企業和地區分類 - 預測(至 2033 年) 全球資料中心液冷閥市場:按閥門類型、冷卻類型、資料中心類型和地區分類 - 預測(至 2032 年)

全球資料中心液冷閥市場:按閥門類型、冷卻類型、資料中心類型和地區分類 - 預測(至 2032 年) 資料中心液冷市場分析及預測(至2035年):類型、產品、服務、技術、組件、應用、材料類型、部署模式、最終用戶、解決方案資料中心自主液冷系統市場:依產品、類型、資料中心類型、最終用途及部署方式分類,全球預測(2026-2032年)

資料中心液冷市場分析及預測(至2035年):類型、產品、服務、技術、組件、應用、材料類型、部署模式、最終用戶、解決方案資料中心自主液冷系統市場:依產品、類型、資料中心類型、最終用途及部署方式分類,全球預測(2026-2032年) 全球資料中心冷卻液市場(至2032年):依液體類型(水-乙二醇混合物、合成烴、氟基冷卻液)、冷卻方式(單相冷卻、兩相冷卻)、資料中心類型、冷卻技術與區域分類

全球資料中心冷卻液市場(至2032年):依液體類型(水-乙二醇混合物、合成烴、氟基冷卻液)、冷卻方式(單相冷卻、兩相冷卻)、資料中心類型、冷卻技術與區域分類 資料中心液冷市場規模、佔有率和趨勢分析:按組件、冷卻方式、資料中心、最終用途、地區和細分市場預測(2026-2033 年)

資料中心液冷市場規模、佔有率和趨勢分析:按組件、冷卻方式、資料中心、最終用途、地區和細分市場預測(2026-2033 年)