|

市場調查報告書

商品編碼

1934917

跨領域解決方案:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Cross-Domain Solution - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

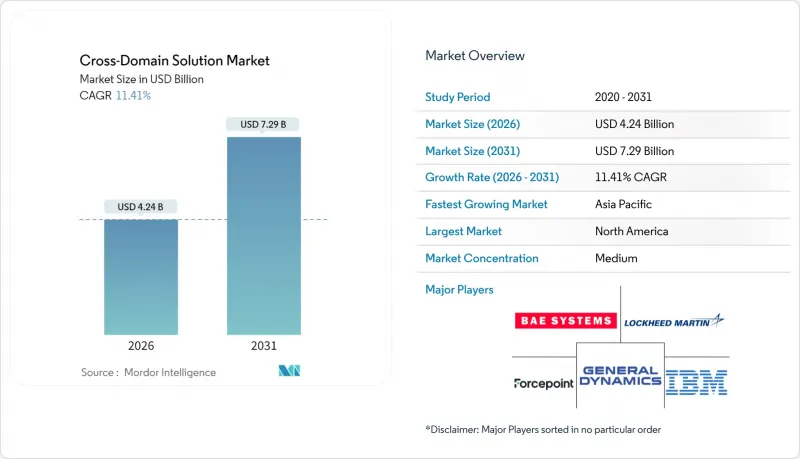

跨域解決方案市場預計將從 2025 年的 38.1 億美元成長到 2026 年的 42.4 億美元,預計到 2031 年將達到 72.9 億美元,2026 年至 2031 年的複合年成長率為 11.41%。

這一成長的驅動力來自日益成長的敏感資料量、強制性的零信任計劃以及旨在替換老舊、空氣間隙基礎設施的現代化項目。國防、情報和關鍵基礎設施機構的需求最為旺盛,這些機構必須在多個安全域之間傳輸數據,同時避免資料外洩的風險。儘管資料二極體等硬體設備仍佔據部署主導地位,但政府雲端環境的成熟正在推動雲端託管閘道器和託管服務的普及。地緣政治緊張局勢進一步加速了相關支出,各國政府,特別是印太地區的政府,正在從零開始建立網路防禦體系。同時,認證週期延長和人才短缺阻礙了短期內技術的普及,從而形成了一個由成熟的國防巨頭和專業領域專家並存的市場格局。

全球跨域解決方案市場趨勢與洞察

分類多域資料流的快速成長

機密感測器、衛星和情報、監視與偵察(ISR)平台如今每天產生Terabyte的數據,這些數據必須在機密、絕密和聯盟網路之間交換。人工透過「人肉網路」傳輸已不再可行,美國國防部的「提高標準」(Raise-the-Bar)計畫明確要求建立自動化的跨域傳輸管道,以應對自2020年以來機密資料流量成長300%的情況。北約聯合行動進一步凸顯了無縫且隔離的資料共用需求,迫使各機構部署經過認證的跨域閘道器,以實現即時協作並確保資料機密性。

美國國防部和北約嚴格執行零信任要求

美國國防部2025年零信任戰略要求對每筆交易進行持續檢驗,這就要求跨域解決方案必須整合細粒度的身份驗證和行為分析。北約成員國也採取了類似的策略,累計1500億美元用於網路安全現代化。能夠證明符合NIST SP 800-207標準並透過通用準則評估的供應商現在可以獲得更高的價格,而傳統的基於邊界防禦的產品正在迅速被取代。

複雜的多機構認證週期

產品必須通過通用準則EAL4+測試,以及NIAP、NSA和NCDSMO的審核,這可能會使交貨時間延長18至24個月。北約成員國各自運作不同的認證體系,要求供應商接受重複評估,並增加了進入門檻。

細分市場分析

到2025年,硬體設備將佔據跨域解決方案市場52.55%的佔有率,這主要得益於市場對符合嚴格軍用測試標準的高可靠性數據二極體的需求不斷成長。同時,隨著各機構轉向營運管理服務以彌補技能短缺,服務市場預計將以14.23%的複合年成長率成長。預計跨域解決方案的管理服務市場規模成長速度將超過資本採購,這反映出在預算受限的專案中優先考慮營運支出的趨勢。提供全天候監控、修補程式管理和持續身分驗證支援的供應商正在吸引那些尋求可預測成本和合規性保證的客戶。

硬體領域也並非一成不變。供應商現在提供整合了基於FPGA的策略引擎並與雲端閘道器整合的虛擬化二極體功能。然而,對於最高層級的安全需求,採購團隊仍然傾向於物理隔離的、僅用於傳輸的通道。在預測期內,能夠將硬體可靠性與軟體定義編配結合,在保持防篡改路徑的同時,促進與零信任架構整合的供應商,將成為成功的供應商。

儘管傳輸閘道器在2025年仍將保持48.23%的收入佔有率,但以訪問為中心的產品預計將以15.54%的複合年成長率成長,這一速度預計將在2031年重塑跨域解決方案的市場格局。基於身分的存取控制與零信任理念完美契合,它允許管理員授予對特定資料集的限時、情境感知進入許可權權限,從而無需跨域批量移動文件。存取閘道器的跨域解決方案市場佔有率得益於其能夠直接與企業級身分識別管理 (IAM) 和安全資訊與事件管理 (SIEM) 平台整合。

僅提供傳輸的供應商現在也開始整合基於屬性的存取控制元素,而存取控制專家則在增加檔案傳輸和通訊協定分離功能,這預示著統一平台未來。因此,買家越來越傾向於選擇提供統一策略引擎的供應商,因為維護獨立的技術堆疊會增加審核的複雜性和生命週期成本。

區域分析

北美地區佔2025年總收入的41.45%,這得益於美國國防部8,410億美元的預算和完善的認證流程。洛克希德馬丁公司等主要承包商(2024年收入達710.7億美元)確保了跨領域部署和升級的持續進行。 AWS Secret Region和Azure Government Secret等聯邦雲端平台透過為影響等級6的機密工作負載提供承包託管服務,正在加速其應用。

亞太地區是成長最快的市場,複合年成長率達17.02%。日本2025年國防預算高達7,340億美元,創歷史新高;澳洲的REDSPICE網路安全舉措;以及印度正在進行的三軍現代化建設,都為國內外閘道器供應商創造了有利條件。 「四方安全對話」(QUAD)夥伴關係正在製定通用的互通性標準,使符合標準的供應商在多國指揮控制計劃中搶佔先機。

歐洲正藉助北約的數位轉型計劃和歐盟網路安全認證框架(該框架簡化了多國核准程序)加速發展。德國、法國和英國正在投資建立跨領域平台,以支援聯合資料共用,同時滿足國內資料主權法規的要求。

除此之外,中東和非洲市場正在發展,但具有重要的戰略意義,沙烏地阿拉伯國家網路安全局強制要求能源設施採用基於二極體的分段技術,而南非國防軍計畫將跨域保護納入未來的衛星地面站。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 多領域敏感資料流的快速成長

- 美國國防部和北約嚴格執行零信任要求

- 快速採用人工智慧/機器學習決策支援系統需要空氣間隙連接

- 擴大商業雲端安全區在敏感工作負載的應用

- 新型衛星星系中的空地遙測安全漏洞

- 關鍵基礎設施領域OT-IT整合的激增

- 市場限制

- 複雜的多機構認證週期

- 跨領域DevSecOps人才短缺

- 數據二極體通訊協定缺乏互通性標準

- 小規模部署的總擁有成本 (TCO) 較高

- 供應鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 宏觀經濟影響評估

第5章 市場規模與成長預測

- 按組件

- 硬體

- 軟體

- 服務

- 按解決方案類型

- 接取解決方案

- 傳輸解決方案

- 其他類型

- 透過部署

- 雲

- 本地部署

- 最終用戶

- 航太/國防

- 執法機關和安全機構

- 關鍵基礎設施營運商

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 肯亞

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- BAE Systems plc

- Lockheed Martin Corporation

- General Dynamics Corporation

- Forcepoint LLC

- IBM Corporation

- Advenica AB

- Cisco Systems Inc.

- Everfox Inc.

- Owl Cyber Defense Solutions LLC

- 4Secure Ltd.

- Raytheon Technologies Corp.

- Northrop Grumman Corp.

- Airbus Defence and Space

- Thales Group

- Leonardo SpA

- Rohde and Schwarz GmbH and Co. KG

- Ultra Intelligence and Communications

- Seceon Inc.

- Waterfall Security Solutions Ltd.

- Belden Inc.

第7章 市場機會與未來展望

The cross-domain solution market is expected to grow from USD 3.81 billion in 2025 to USD 4.24 billion in 2026 and is forecast to reach USD 7.29 billion by 2031 at 11.41% CAGR over 2026-2031.

This growth is driven by rising classified data volumes, mandatory zero-trust initiatives, and modernization programs that replace aging air-gapped infrastructure. Demand is strongest among defense agencies, intelligence services, and critical-infrastructure operators that must move data between multiple security domains without risking leakage. Hardware appliances such as data diodes still dominate deployments, yet cloud-hosted gateways and managed services are gaining traction as government cloud enclaves mature. Geopolitical tensions further accelerate spending, especially in the Indo-Pacific region where governments are building cyber defenses from the ground up. Meanwhile, prolonged certification cycles and talent shortages temper near-term adoption, creating a market where established defense primes and niche specialists coexist.

Global Cross-Domain Solution Market Trends and Insights

Escalating Volume of Multi-Domain Classified Data Flows

Classified sensors, satellites, and ISR platforms now generate terabytes of data daily that must cross between SECRET, TOP SECRET, and coalition networks. Manual sneaker-net transfers are no longer feasible, and the U.S. DoD's Raise-the-Bar program explicitly demands automated cross-domain pipelines to cope with a 300% jump in classified traffic since 2020. NATO's joint operations further amplify requirements for seamless yet compartmented data sharing, pushing agencies toward certified cross-domain gateways that assure confidentiality while enabling real-time collaboration.

Stringent Zero-Trust Mandates in U.S. DoD and NATO

The 2025 DoD Zero Trust Strategy stipulates continuous verification for every transaction, forcing cross-domain solutions to embed granular identity checks and behavioral analytics. NATO allies mirror the approach, having earmarked USD 150 billion for cybersecurity modernization in 2024. Vendors able to prove alignment with NIST SP 800-207 and to pass Common Criteria evaluations now command premium pricing, while legacy perimeter-based products face rapid displacement.

Complex Multi-Authority Certification Cycles

Products must clear NIAP, NSA, and NCDSMO reviews on top of Common Criteria EAL4+ testing, adding 18-24 months to delivery schedules. Each NATO nation also runs its own scheme, prompting vendors to pursue duplicate evaluations and increasing barriers for new entrants.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Proliferation of AI/ML Decision-Support Systems

- Growing Use of Commercial Cloud Enclaves for Secret Workloads

- Scarcity of Cross-Domain-Aware DevSecOps Talent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware appliances captured 52.55% of the cross-domain solution market in 2025, propelled by high-assurance data diodes that satisfy rigorous military test criteria. At the same time, services are forecast to grow at a 14.23% CAGR as agencies pivot toward managed operations to offset skills shortages. The cross-domain solution market size for managed services is therefore expected to expand faster than capital purchases, reflecting an operating-expense preference among budget-constrained programs. Vendors that bundle 24/7 monitoring, patch management, and continuous accreditation support increasingly appeal to customers seeking predictable costs and compliance guarantees.

The hardware segment is not static; suppliers now embed FPGA-based policy engines and offer virtualized diode functions that integrate with cloud gateways. Nevertheless, procurement teams still favor physically isolated transmit-only channels for the highest classification tiers. Over the forecast period, successful vendors will be those fusing hardware reliability with software-defined orchestration, thereby easing integration into zero-trust stacks while preserving tamper-resistant pathways.

Transfer gateways maintained a 48.23% share of 2025 revenues, yet access-centric products are slated for a 15.54% CAGR, a pace that could redraw the cross-domain solution market landscape by 2031. Identity-driven access controls align neatly with zero-trust doctrine, letting administrators grant time-bounded, context-aware entry to specific datasets instead of bulk-moving files across domains. The cross-domain solution market share for access gateways is boosted by their ability to hook directly into enterprise IAM and SIEM platforms.

Transfer-focused vendors now embed attribute-based access elements, while access specialists add file-transfer and protocol break functions, hinting at a converged platform future. As a result, buyers increasingly shortlist suppliers that deliver unified policy engines, since maintaining separate stacks inflates audit complexity and lifecycle costs.

Cross-Domain Solution Market Report is Segmented by Component (Hardware, Software, Services), Solution Type (Access Solutions, Transfer Solutions, Other Types), Deployment (Cloud, On-Premises), End-User (Aerospace and Defense, Law-Enforcement and Security Agencies, Critical Infrastructure Operators, Others), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 41.45% of 2025 revenues, undergirded by the U.S. DoD's USD 841 billion appropriation and well-established certification pathways. Prime contractors such as Lockheed Martin logged USD 71.07 billion in 2024 sales, guaranteeing a sustained pipeline of cross-domain deployments and upgrades. Federal cloud enclaves, including AWS Secret Region and Azure Government Secret, accelerate adoption by offering turnkey hosting for classified workloads at Impact Level 6.

Asia-Pacific is the fastest-growing theatre at 17.02% CAGR. Japan's record USD 734 billion 2025 defense budget, Australia's REDSPICE cyber initiative, and India's ongoing tri-service modernization create fertile ground for indigenous and Western gateway suppliers. The QUAD partnership sets common interoperability benchmarks, giving compliant vendors a head start in multi-nation command-and-control projects.

Europe maintains steady momentum through NATO's Digital Transformation vision and the EU Cybersecurity Certification Framework, which simplifies multi-state approvals. Germany, France, and the United Kingdom invest in cross-domain platforms that support coalition data sharing while satisfying domestic data-sovereignty statutes.

Elsewhere, Middle East and Africa markets are nascent yet strategic: Saudi Arabia's National Cybersecurity Authority mandates diode-based segmentation for energy facilities, and South Africa's defense forces plan to embed cross-domain guards in forthcoming satellite-ground stations.

- BAE Systems plc

- Lockheed Martin Corporation

- General Dynamics Corporation

- Forcepoint LLC

- IBM Corporation

- Advenica AB

- Cisco Systems Inc.

- Everfox Inc.

- Owl Cyber Defense Solutions LLC

- 4Secure Ltd.

- Raytheon Technologies Corp.

- Northrop Grumman Corp.

- Airbus Defence and Space

- Thales Group

- Leonardo S.p.A.

- Rohde and Schwarz GmbH and Co. KG

- Ultra Intelligence and Communications

- Seceon Inc.

- Waterfall Security Solutions Ltd.

- Belden Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating volume of multi-domain classified data flows

- 4.2.2 Stringent zero-trust mandates in U.S. DoD and NATO

- 4.2.3 Rapid proliferation of AI/ML decision-support systems requiring air-gapped feeds

- 4.2.4 Growing use of commercial cloud enclaves for secret workloads

- 4.2.5 Space-to-ground telemetry security gaps in new satellite constellations

- 4.2.6 Surge in OT-IT convergence across critical infrastructure

- 4.3 Market Restraints

- 4.3.1 Complex multi-authority certification cycles

- 4.3.2 Scarcity of cross-domain aware DevSecOps talent

- 4.3.3 Lack of interoperability standards for data-diode protocols

- 4.3.4 High TCO for small-footprint deployments

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Macroeconomic Impact Assessment

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Solution Type

- 5.2.1 Access Solutions

- 5.2.2 Transfer Solutions

- 5.2.3 Other Types

- 5.3 By Deployment

- 5.3.1 Cloud

- 5.3.2 On-Premises

- 5.4 By End-user

- 5.4.1 Aerospace and Defense

- 5.4.2 Law-Enforcement and Security Agencies

- 5.4.3 Critical Infrastructure Operators

- 5.4.4 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 UAE

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Kenya

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 BAE Systems plc

- 6.4.2 Lockheed Martin Corporation

- 6.4.3 General Dynamics Corporation

- 6.4.4 Forcepoint LLC

- 6.4.5 IBM Corporation

- 6.4.6 Advenica AB

- 6.4.7 Cisco Systems Inc.

- 6.4.8 Everfox Inc.

- 6.4.9 Owl Cyber Defense Solutions LLC

- 6.4.10 4Secure Ltd.

- 6.4.11 Raytheon Technologies Corp.

- 6.4.12 Northrop Grumman Corp.

- 6.4.13 Airbus Defence and Space

- 6.4.14 Thales Group

- 6.4.15 Leonardo S.p.A.

- 6.4.16 Rohde and Schwarz GmbH and Co. KG

- 6.4.17 Ultra Intelligence and Communications

- 6.4.18 Seceon Inc.

- 6.4.19 Waterfall Security Solutions Ltd.

- 6.4.20 Belden Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

網域名稱系統 (DNS) 工具市場:按組件、組織規模、部署類型和產業分類-2026-2032 年全球市場預測託管 DNS 服務市場:按組件、部署類型、組織規模和產業分類-2026-2032 年全球市場預測

網域名稱系統 (DNS) 工具市場:按組件、組織規模、部署類型和產業分類-2026-2032 年全球市場預測託管 DNS 服務市場:按組件、部署類型、組織規模和產業分類-2026-2032 年全球市場預測 全球跨域解決方案 (CDS) 市場規模、佔有率、趨勢和成長分析報告(2026-2034 年)全球跨域解決方案市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034)DNS 安全市場 - 2026-2031 年預測

全球跨域解決方案 (CDS) 市場規模、佔有率、趨勢和成長分析報告(2026-2034 年)全球跨域解決方案市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034)DNS 安全市場 - 2026-2031 年預測 2026-2030年全球域名系統工具市場

2026-2030年全球域名系統工具市場 DNS 服務市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、部署方式、最終用戶產業、企業規模、地區和競爭格局分類,2021-2031 年預測

DNS 服務市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、部署方式、最終用戶產業、企業規模、地區和競爭格局分類,2021-2031 年預測 全球託管網域名稱系統 (DNS) 市場跨領域解決方案的全球市場

全球託管網域名稱系統 (DNS) 市場跨領域解決方案的全球市場 託管域名系統市場規模、佔有率、趨勢分析報告:按服務、部署、公司規模、最終用途、地區和細分市場進行預測,2025 年至 2030 年

託管域名系統市場規模、佔有率、趨勢分析報告:按服務、部署、公司規模、最終用途、地區和細分市場進行預測,2025 年至 2030 年