|

市場調查報告書

商品編碼

1934908

自動識別與資料擷取(AIDC):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Automatic Identification And Data Capture (AIDC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

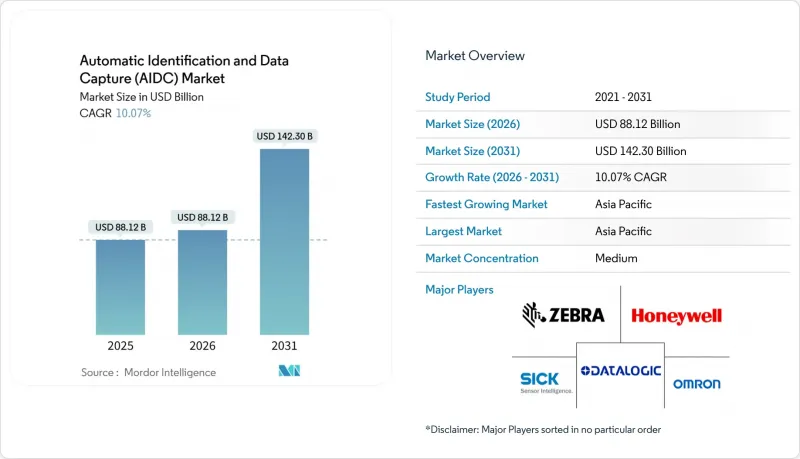

自動識別和資料擷取(AIDC) 市場預計到 2026 年將達到 881.2 億美元,高於 2025 年的 800.5 億美元。

預計到 2031 年將達到 1,423 億美元,2026 年至 2031 年的複合年成長率為 10.07%。

預計累積成長率將達到 62.7%,這反映了製造業、零售業和醫療保健行業的結構性數位化,使得自動識別成為提高吞吐量、合規性和消除錯誤的關鍵組成部分。勞動力短缺、日益複雜的監管以及即時可視性帶來的顯著投資回報率共同造就了市場需求,使得自動識別和資料擷取(AIDC) 市場被視為基礎設施而非可自由支配的支出 (biometricupdate.com)。2D條碼、被動式超高頻射頻識別 (UHF-RFID) 和國家電子識別計劃的日益普及,為能夠構建整合設備、中間件和雲端分析的統一生態系統的解決方案供應商創造了機會。

全球自動識別與資料擷取(AIDC) 市場趨勢與洞察

加速全通路零售向2D/QR碼轉型

為了迎接GS1 Sunrise 2027的實施,全球零售商正積極遷移至2D碼/QR碼。此標準允許將有效期限、批號和行銷連結嵌入到單一高密度符號中。早期採用者報告稱,2D碼/2D碼的使用減少了食物廢棄物,並帶來了更流暢的全通路體驗,豐富的數據支援自動折扣和動態客戶參與。投資回報體現在減少人工操作、提高銷售點掃描準確率、利用消費者智慧型手機開展新型互動行銷方式等。硬體供應商預計,隨著零售商用能夠解碼多種符號的成像器取代傳統的1D掃描器,銷售額將會增加;而軟體供應商則將從POS韌體更新帶來的升級成本中獲益。

UHF-RFID在物品級庫存管理中的應用迅速成長

沃爾瑪強制要求在2024年部署物品等級RFID標籤,這正在推動零售業全面採用該技術。供應商鼓勵零售連鎖店在收貨點、倉庫和貨架上嵌入可掃描的嵌體。每個被動式標籤的成本已降至0.04美元以下,這使得在服裝和家居用品等關鍵品類中採用即時庫存可見性成為可能。部署RFID技術已將庫存準確率提高了25%,顯著減少了缺貨情況的發生。持續掃描的數據還可用於安全分析,使RFID技術兼具提高利潤率和防止庫存損耗的雙重優勢。

舊版ERP系統之間資料格式不相容

仍在使用90年代ERP系統的公司往往難以原生整合RFID和影像數據,必須部署中間件層,導致計劃成本增加高達40%。因此,自動識別和資料擷取(AIDC)市場面臨著銷售週期延長的挑戰,因為整合、測試和遷移成本必須納入預算。在多站點網路中,不同的資料模式會增加複雜性,並造成資料孤島,從而削弱預期的投資報酬率。儘管供應商透過提供預先建置連接器和諮詢服務來降低風險,但將新系統整合到現有系統中仍然是一大障礙。

細分市場分析

到2025年,硬體收入將佔總收入的62.50%,這主要得益於零售和醫療保健產業的基礎設施更新換代。然而,價格壓縮、標準化和供應鏈波動正在擠壓利潤空間,並加速向利潤率更高的諮詢和支援合約模式轉變。提供硬體即服務(HaaS)的供應商在調整產品組合的同時,也維持了銷售量。因此,自動識別和資料擷取(AIDC)市場的競爭優勢正向那些掌握混合收入模式(將資本設備與持續服務結合)的供應商傾斜。

服務領域的成長速度超過硬體領域,複合年成長率高達 11.64%,這主要得益於企業擴大採用基於結果的合約模式,涵蓋整合、維護和雲端分析等服務。許多大型零售商正從資本支出購買轉向託管服務,以確保掃描器、印表機和 RFID 入口網站的運作。服務供應商正憑藉其在邊緣到雲端編配、增強型網路安全和多站點部署方面的專業知識脫穎而出,而硬體 OEM 廠商則透過收購系統整合商來保障全生命週期收入。

條碼作為一種通用的支付和合規標識符,在全通路營運中佔據了 46.20% 的收入佔有率。隨著零售店面面積的擴大,與條碼列印機、成像器和標籤相關的自動識別和資料擷取(AIDC) 市場規模持續溫和成長。然而,被動式超高頻射頻識別 (UHF-RFID) 的複合年成長率 (CAGR) 高達 12.05%,反映出強制性的單品級部署,該技術能夠同時掃描多個商品並進行即時庫存確認。投資報酬率源自於商品流失率的降低和交付準確率的提高,從而推動了時尚、運動用品和消費性產品類型的廣泛應用。

被動式RFID成本的下降和中間件的日趨成熟將支援混合部署,其中RFID連接上游價值鏈運營,而條碼則在商店保持面向消費者的展示。主動式RFID將在高價值資產監控領域,尤其是在航太和醫療設備,繼續發揮其獨特作用。嵌入式人工智慧OCR系統將實現物流和製造領域的字母數位資料擷取,從而拓展缺失或損壞標籤的應用場景。

區域分析

北美地區預計到2025年將佔全球收入的34.00%,這主要得益於該地區作為早期採用者,已將產品級RFID和數位化患者安全管理制度化。沃爾瑪的政策推動了嵌體轉換器、印表機編碼器和中介軟體整合商等供應商生態系統的蓬勃發展。同時,美國正優先發展生物識別邊境管制,促進了多種技術的普及應用。自動識別和資料擷取(AIDC)市場參與企業正利用更新周期和先進的倉庫自動化技術,連接加拿大和墨西哥的跨境供應鏈。

亞太地區以11.44%的複合年成長率領先全球,主要得益於製造業自動化和國家識別計劃的推進。中國作為全球最大的RFID標籤生產國,正透過出口規模經濟來控制全球標籤價格。韓國、日本和印度正在實施融合生物識別識別項目,推動了對智慧卡和感測器的需求。電商巨頭加速推動倉庫機器人化,進一步促進了自動識別和資料擷取(AIDC)市場的應用。

監管合規性持續推動歐洲市場的穩定成長。醫療設備法規強制要求使用標準化的UDI標籤,而數位身分框架法規則為公民電子錢包奠定了基礎。在法國和瑞士,整合身分和醫療保健解決方案的開發正在推動對生物識別和智慧卡的需求。 AIDC市場參與者正在調整其產品以符合嚴格的資料保護標準,從而在確保合規性的同時實現創新應用。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 加速全通路零售向2D/QR碼轉型

- UHF頻段 RFID在物品級庫存管理中的應用迅速成長

- 推出政府核發的電子身分證和數位健康卡

- 勞動力短缺背景下的倉庫自動化

- 強制性即時低溫運輸追蹤

- 旅行安檢通道上的非接觸式生物識別閘機

- 市場限制

- 舊版ERP系統之間資料格式不相容

- 將基於視覺的AIDC引入現有工廠需要較高的初始資本投入。

- 來自灰色市場的假冒低價條碼掃描器

- 生物識別資料儲存引發隱私反彈

- 價值/供應鏈分析

- 監理展望

- 擴展 ISO/IEC 19762;歐盟醫療設備法規 (MDR) UDI 截止日期 2027 年

- 技術展望

- 投資趨勢分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 報價

- 硬體

- 固定式閱讀器/掃描儀

- 行動電腦和手持終端機

- 印表機/編碼器

- 軟體

- 服務

- 整合與諮詢

- 維護和支援

- 硬體

- 依產品

- 條碼

- 1D

- 2D/QR

- RFID

- 被動式(低頻、高頻、超高頻)

- 積極的

- 智慧卡

- 聯繫類型

- 非接觸式

- 生物識別系統

- 指紋

- 臉部認證/虹膜辨識

- 光學字元辨識(OCR)

- 其他產品

- 磁條、NFC、BLE標籤

- 條碼

- 按媒體類型

- 標籤

- 標籤

- 卡片

- 按最終用戶行業分類

- 製造業

- 零售與電子商務

- 運輸/物流

- 醫療/製藥

- BFSI

- 飯店業

- 政府/公共部門

- 能源與公共產業

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 其他歐洲

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- ASEAN

- 澳洲

- 紐西蘭

- 亞太其他地區

- 中東和非洲

- 中東

- GCC

- 土耳其

- 以色列

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Zebra Technologies Corporation

- Honeywell International Inc.

- Datalogic SpA

- SICK AG

- Cognex Corporation

- Omron Corporation

- Toshiba Tec Corporation

- SATO Holdings Corporation

- Newland AIDC

- Bluebird Inc.

- Impinj Inc.

- Alien Technology LLC

- Avery Dennison Corporation

- Axicon Auto ID Ltd.

- Opticon Sensors Europe BV

- Zebex Industries Inc.

- Brady Corporation

- Thales Group(Gemalto)

- NEC Corporation

- HID Global Corporation

第7章 市場機會與未來展望

Automatic Identification And Data Capture (AIDC) market size in 2026 is estimated at USD 88.12 billion, growing from 2025 value of USD 80.05 billion with 2031 projections showing USD 142.3 billion, growing at 10.07% CAGR over 2026-2031.

The projected 62.7% cumulative expansion reflects structural digitization across manufacturing, retail, and healthcare, where automated identification has become mission-critical to throughput, compliance, and error elimination. Labor-scarcity, increasing regulatory specificity, and proven ROI for real-time visibility collectively shape a demand environment in which the Automatic Identification And Data Capture (AIDC) market is viewed as infrastructure rather than discretionary spend biometricupdate.com. Heightened adoption of 2D codes, passive UHF-RFID, and national e-ID programs widens the opportunity set for solution providers able to integrate devices, middleware, and cloud analytics within cohesive ecosystems.

Global Automatic Identification And Data Capture (AIDC) Market Trends and Insights

Accelerated Migration to 2D/QR Codes in Omnichannel Retail

Global retailers are transitioning to 2D/QR codes in preparation for the GS1 Sunrise 2027 deadline, embedding expiry dates, lot numbers, and marketing links inside a single dense symbol. Early adopters report lower food waste and smoother omnichannel experiences because richer data supports automated markdowns and dynamic customer engagement. Investment returns manifest through fewer manual interventions, higher scan accuracy at point-of-sale, and emerging interactive marketing formats that leverage consumer smartphones. Hardware vendors gain incremental unit sales as retailers replace legacy 1D scanners with imagers capable of decoding stacked symbologies, while software providers capture upgrade fees tied to POS firmware refreshes.

Surge in UHF-RFID Adoption for Item-Level Inventory

Walmart's 2024 mandate for item-level RFID tags catalyzed broad retail adoption, pushing suppliers to embed inlays that retail chains read at dock, stockroom, and shelf. Cost per passive tag has fallen below USD 0.04, enabling mainstream categories such as apparel and home goods to justify real-time inventory visibility. Deployments deliver up to 25% accuracy improvement and materially reduce out-of-stock events . Continuous reads also power loss-prevention analytics, making RFID a dual lever for margin expansion and shrink mitigation.

Inter-System Data-Format Incompatibility Across Legacy ERPs

Enterprises with 1990s-era ERP stacks struggle to ingest RFID and image data natively, often funding middleware layers that inflate project cost by up to 40%. The Automatic Identification And Data Capture (AIDC) market therefore faces elongated sales cycles because budgets must include integration, testing, and migration. In multi-site networks, disparate schema multiply complexity, generating data silos that erode promised ROI. Vendors mitigate risk by offering pre-built connectors and consulting engagements, yet the barrier remains meaningful for brown-field rollouts.

Other drivers and restraints analyzed in the detailed report include:

- Government E-ID & Digital Health-Card Roll-outs

- Labor-Scarcity-Led Warehouse Automation

- High Initial CAPEX for Vision-Based AIDC in Brown-Field Plants

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware dominated 62.50% of 2025 turnover due to foundational equipment refresh across retail and healthcare. Yet pricing compression, standardization, and supply-chain contingencies squeeze margins, accelerating the pivot toward higher-margin consulting and support contracts. Vendors bundling hardware-as-a-service maintain volume while shifting mix. Consequently, Automatic Identification And Data Capture (AIDC) market competitive advantage tilts toward providers mastering hybrid revenue models that unite capital equipment with recurring service matrices.

The services layer contributed 11.64% CAGR, outpacing hardware because enterprises increasingly award outcome-based contracts covering integration, maintenance, and cloud analytics. Many tier-1 retailers migrate from capex procurement to managed services that ensure uptime for scanners, printers, and RFID portals. Services players differentiate through domain expertise in edge-to-cloud orchestration, cybersecurity hardening, and multi-site rollouts, while hardware OEMs acquire systems integrators to secure lifecycle revenue.

Barcodes retained 46.20% revenue share as ubiquitous checkout and compliance identifiers underpin omnichannel operations. The Automatic Identification And Data Capture (AIDC) market size tied to barcode printers, imagers, and labels continues to expand modestly alongside retail floor space growth. However, passive UHF-RFID expands at 12.05% CAGR, reflecting item-level mandates that unlock simultaneous multi-item scans and real-time inventory verification. ROI stems from shrink reduction and fulfillment accuracy, prompting fashion, sports equipment, and consumer electronics categories to convert.

Passive RFID's cost curve decline and middleware maturity support hybrid deployments where RFID bridges upstream supply-chain workflows while barcodes remain consumer-facing on the shelf. Active RFID preserves niche roles in high-value asset monitoring, particularly aerospace and healthcare equipment. OCR systems incorporating AI extract alphanumeric data in logistics and manufacturing, widening addressable scenarios where labels are absent or damaged.

The Automatic Identification and Data Capture (AIDC) Market Report is Segmented by Offering (Hardware, Software, Services), Product (Barcodes, RFID, Smart Cards, and More), Media Type (Labels, Tags, Cards), End-User Industry (Manufacturing, Retail and E-Commerce, and More), and by Geography (North America, South America, Europe, Asia Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 34.00% of revenue in 2025 as early adopters institutionalized item-level RFID and digital patient safety. Walmart's mandate created a robust supplier ecosystem of inlay converters, printer-encoders, and middleware integrators. Meanwhile, the United States prioritizes biometric border control, reinforcing multi-technology adoption. Automatic Identification And Data Capture (AIDC) market participants capitalize on replacement cycles and advanced warehouse automation in Canada and Mexico that link cross-border supply chains.

Asia Pacific posts 11.44% CAGR, the fastest globally, fueled by manufacturing automation and national identity projects. China, the world's largest RFID tag producer, exports scale efficiencies that compress global tag pricing. South Korea, Japan, and India implement e-ID programs integrating biometrics, driving smart-card and sensor demand. E-commerce giants accelerate warehouse robotization, further expanding Automatic Identification And Data Capture (AIDC) market deployments.

Europe sustains steady growth through regulatory compliance. EU Medical Device Regulation mandates standardized UDI labeling, while the Digital Identity Framework Regulation sets a foundation for citizen wallets. France and Switzerland progress toward integrated identity-health solutions, reinforcing biometrics and smart-card volume. Automatic Identification And Data Capture (AIDC) market players align offerings with stringent data-protection norms, ensuring adoption remains compliant yet innovative.

- Zebra Technologies Corporation

- Honeywell International Inc.

- Datalogic S.p.A.

- SICK AG

- Cognex Corporation

- Omron Corporation

- Toshiba Tec Corporation

- SATO Holdings Corporation

- Newland AIDC

- Bluebird Inc.

- Impinj Inc.

- Alien Technology LLC

- Avery Dennison Corporation

- Axicon Auto ID Ltd.

- Opticon Sensors Europe B.V.

- Zebex Industries Inc.

- Brady Corporation

- Thales Group (Gemalto)

- NEC Corporation

- HID Global Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated migration to 2D/QR codes in omnichannel retail

- 4.2.2 Surge in UHF-RFID adoption for item-level inventory

- 4.2.3 Government e-ID and digital health-card roll-outs

- 4.2.4 Labor-scarcity-led warehouse automation

- 4.2.5 Real-time cold-chain tracking mandates

- 4.2.6 Contactless biometric gates in travel-security corridors

- 4.3 Market Restraints

- 4.3.1 Inter-system data-format incompatibility across legacy ERPs

- 4.3.2 High initial CAPEX for vision-based AIDC in brown-field plants

- 4.3.3 Counterfeit low-cost barcode scanners from grey markets

- 4.3.4 Privacy pushback on biometric data storage

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.5.1 ISO/IEC 19762 expansion; EU MDR UDI deadline 2027

- 4.6 Technological Outlook

- 4.7 Investment Trend Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Hardware

- 5.1.1.1 Fixed Readers/Scanners

- 5.1.1.2 Mobile Computers and Handhelds

- 5.1.1.3 Printers/Encoders

- 5.1.2 Software

- 5.1.3 Services

- 5.1.3.1 Integration and Consulting

- 5.1.3.2 Maintenance and Support

- 5.1.1 Hardware

- 5.2 By Product

- 5.2.1 Barcodes

- 5.2.1.1 1D

- 5.2.1.2 2D/QR

- 5.2.2 RFID

- 5.2.2.1 Passive (LF, HF, UHF)

- 5.2.2.2 Active

- 5.2.3 Smart Cards

- 5.2.3.1 Contact

- 5.2.3.2 Contactless

- 5.2.4 Biometric Systems

- 5.2.4.1 Fingerprint

- 5.2.4.2 Facial/Iris

- 5.2.5 Optical Character Recognition (OCR)

- 5.2.6 Other Products

- 5.2.6.1 Magnetic Stripe, NFC, BLE Tags

- 5.2.1 Barcodes

- 5.3 By Media Type

- 5.3.1 Labels

- 5.3.2 Tags

- 5.3.3 Cards

- 5.4 By End-user Industry

- 5.4.1 Manufacturing

- 5.4.2 Retail and E-commerce

- 5.4.3 Transportation and Logistics

- 5.4.4 Healthcare and Pharma

- 5.4.5 BFSI

- 5.4.6 Hospitality

- 5.4.7 Government and Public Sector

- 5.4.8 Energy and Utilities

- 5.4.9 Others

- 5.5 By Region

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Nordics

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 ASEAN

- 5.5.4.6 Australia

- 5.5.4.7 New Zealand

- 5.5.4.8 Rest of Asia Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 GCC

- 5.5.5.1.2 Turkey

- 5.5.5.1.3 Israel

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Zebra Technologies Corporation

- 6.4.2 Honeywell International Inc.

- 6.4.3 Datalogic S.p.A.

- 6.4.4 SICK AG

- 6.4.5 Cognex Corporation

- 6.4.6 Omron Corporation

- 6.4.7 Toshiba Tec Corporation

- 6.4.8 SATO Holdings Corporation

- 6.4.9 Newland AIDC

- 6.4.10 Bluebird Inc.

- 6.4.11 Impinj Inc.

- 6.4.12 Alien Technology LLC

- 6.4.13 Avery Dennison Corporation

- 6.4.14 Axicon Auto ID Ltd.

- 6.4.15 Opticon Sensors Europe B.V.

- 6.4.16 Zebex Industries Inc.

- 6.4.17 Brady Corporation

- 6.4.18 Thales Group (Gemalto)

- 6.4.19 NEC Corporation

- 6.4.20 HID Global Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment

自動識別系統 (AIS) 市場:按組件、平台類型、通訊類型、技術類型、船舶類型、應用和最終用戶分類—2026-2032 年全球市場預測

自動識別系統 (AIS) 市場:按組件、平台類型、通訊類型、技術類型、船舶類型、應用和最終用戶分類—2026-2032 年全球市場預測 自動識別和資料擷取(AIDC) 市場規模、佔有率、趨勢和預測:按產品、產品類型、產業和地區分類,2026-2034 年船舶自動識別系統市場報告:按船型、組件、平台、應用和地區分類,2026-2034年

自動識別和資料擷取(AIDC) 市場規模、佔有率、趨勢和預測:按產品、產品類型、產業和地區分類,2026-2034 年船舶自動識別系統市場報告:按船型、組件、平台、應用和地區分類,2026-2034年 自動識別系統(AIS)市場:規模、佔有率、成長率、全球產業分析、按類型、應用和地區分類以及未來預測(2026-2034 年)ID卡證件閱讀器市場:按閱讀器類型、最終用戶、應用、分銷管道分類,全球預測(2026-2032年)

自動識別系統(AIS)市場:規模、佔有率、成長率、全球產業分析、按類型、應用和地區分類以及未來預測(2026-2034 年)ID卡證件閱讀器市場:按閱讀器類型、最終用戶、應用、分銷管道分類,全球預測(2026-2032年) 醫療保健自動識別和資料收集市場:依產品、技術、應用和地區,至2036年全球預測全球堅固型工業手持閱讀器市場(按類型、連接方式、作業系統、操作模式、價格範圍、應用和最終用戶產業分類)預測(2026-2032年)

醫療保健自動識別和資料收集市場:依產品、技術、應用和地區,至2036年全球預測全球堅固型工業手持閱讀器市場(按類型、連接方式、作業系統、操作模式、價格範圍、應用和最終用戶產業分類)預測(2026-2032年) 自動識別系統 (AIS) 市場規模、佔有率和成長分析(按類別、平台、應用、最終用戶和地區分類)—2026-2033 年行業預測

自動識別系統 (AIS) 市場規模、佔有率和成長分析(按類別、平台、應用、最終用戶和地區分類)—2026-2033 年行業預測 AIS(自動識別系統):市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

AIS(自動識別系統):市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) AIT防止的全球市場:2024-2029年

AIT防止的全球市場:2024-2029年