|

市場調查報告書

商品編碼

1934906

測試與測量:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Test And Measurement - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

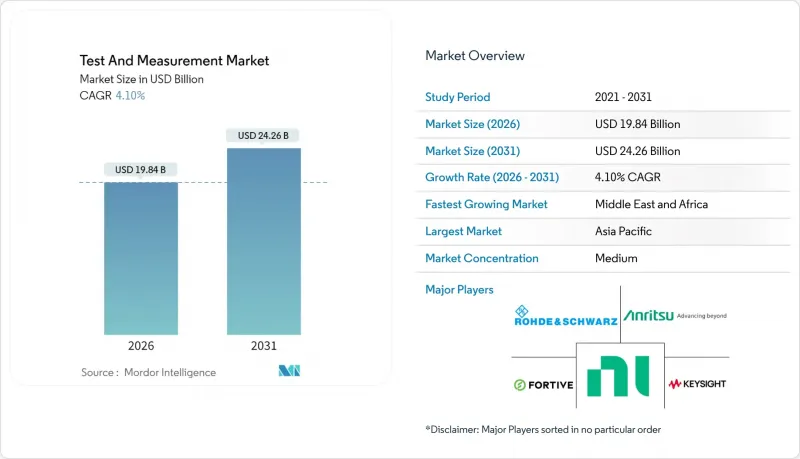

預計到 2026 年,測試和測量市場價值將達到 198.4 億美元,高於 2025 年的 190.6 億美元。

預計到 2031 年將達到 242.6 億美元,2026 年至 2031 年的複合年成長率為 4.1%。

工程師正從以硬體為中心的系統轉向軟體定義、基於訂閱的平台,這些平台在提高利潤率的同時降低了資本投入。模組化測試設備正是這種轉變的典型代表,預計到2030年,其複合年成長率將達到4.7%,因為設計團隊正在尋求用於複雜設備的可重構架構。亞太地區的需求正在成長,這得益於5G/6G基礎設施的建設和先進的電子製造能力;同時,汽車行業的電氣化進程以及醫療保健領域日益嚴格的法令遵循也在推動該細分市場的擴張。諸如艾默生以82億美元收購美國國家儀器公司等策略整合,凸顯了軟體連接的自動化測試生態系統日益成長的價值。

全球測試與測量市場趨勢及洞察

汽車電動車領域對高壓、高頻寬測試解決方案的需求

電動車平台的工作電壓範圍在 400V 至 800V 之間,必須符合嚴格的安全性和效率標準。一級製造商的研發中心已安裝了 200 多台專用測試台,用於電池、逆變器和馬達的檢驗,從而能夠在動態負載和溫度變化範圍內進行微秒測量。整合式功率分析儀的取樣率高達 1MS/s,能夠捕捉傳統設備無法捕捉的瞬態尖峰,確保動力傳動系統在再生煞車環境下的可靠性。

亞洲5G/6G快速部署推動Sub-6GHz與毫米波測試能力發展

中國於2024年初發射的6G測試衛星為天地一體化網路樹立了標竿。工作頻率高於50GHz的毫米波鏈路存在較高的路徑損耗,對頻譜分析儀的動態範圍性能提出了更高的要求。隨著亞洲通訊業者加速部署新一代通訊技術,對無線測試室、相位陣列分析設備和即時訊號記錄器的需求正在激增。

新興市場租賃需求成長拉低了新測試設備的平均售價

預算有限的用戶更傾向於選擇無需前期資本投入的租賃協議。如今,租賃公司將校準和物流服務打包提供,擠壓了原始設備製造商(OEM)的利潤空間,迫使供應商設計堅固耐用、便於現場維修的設備。結合訂閱軟體和低成本硬體升級的混合模式正日益普及。

細分市場分析

到2025年,通用測試設備的市場規模仍將佔據主導地位,收入佔有率將達到65.35%,為廣泛的研發和製造活動提供支援。然而,成長趨勢正在轉向模組化儀器,預計到2031年,模組化儀器的複合年成長率將達到4.55%,因為工程師優先考慮擴充性和快速重配置。在混合訊號整合方面,設計團隊正在將基於FPGA的卡與PXI底盤整合,以在保持通道密度的同時減少機架面積。

5G設備和早期6G原型機的推出也推動了對射頻和微波測試系統的需求。頻譜分析靈敏度先前受限於熱噪聲基底,如今得益於ADC解析度的提升和低相位雜訊合成器的應用,靈敏度已顯著提高。機械測試設備對於材料和結構檢驗至關重要,但其重型框架的使用壽命長達數十年,導致更新周期較長。自動化測試設備為半導體大規模生產線提供支持,它將參數測量與人工智慧驅動的異常值檢測相結合,從而將產量比率維持在99.5%以上。

營運支出策略正在重塑企業採購測量能力的方式。資產管理和租賃服務是成長最快的服務領域,複合年成長率達 6.05%,使製造商能夠在確保獲得最新平台的同時節省現金。訂閱套餐現在包含遠端校準、預測性維護和合規性文件。然而,到 2025 年,校準服務仍將佔據測試和測量市場 71.20% 的主導地位,這反映了半導體光刻、航太航太電子和醫療診斷領域對可追溯精度的法律要求。

數位化工作流程簡化了校準週期,QR碼資產追蹤將每台設備與其服務記錄關聯起來,自動化夾具可將週轉時間縮短高達 25%,遠端韌體更新則消除了兩次定期巡檢之間的測量空白期。培訓和諮詢服務完善了產品組合,提供現場研討會,以彌補電力完整性、電磁相容性和安全關鍵型軟體檢驗的技能缺口。

區域分析

到2025年,亞太地區將佔全球營收的37.62%,反映出該地區擁有深厚的電子製造生態系統以及對5G/6G基礎設施的大力投資。中國的現場測試網路效能提升了10倍,帶動了多端口向量網路分析儀和OTA測試腔的訂單。台灣和韓國的晶圓代工廠推出了高密度探針台,用於檢驗人工智慧加速器的2.5D封裝。

北美位居第二,受益於航太、國防和醫療產業的強勁發展,以及美國食品藥物管理局 (FDA) 嚴格的監管,強制要求基於 IEC 60601 標準的電磁相容性 (EMC)檢驗。 2024 年基礎設施獎勵策略後,人工智慧和雲端測試平台的投資加速成長。光纖、鐵塔和資料中心資產的私募股權交易也推高了對攜帶式光時域反射儀 (OTDR) 和高速誤碼率測試儀 (BERT) 的需求。

到2031年,中東和非洲地區將以5.15%的複合年成長率實現最快成長,這主要得益於通訊業者升級回程傳輸線路以及工業運營商採用ISO認證的品質框架。該地區的能源計劃,特別是氫能和太陽能計劃,也需要精確的電氣測量。歐洲在電動車動力傳動系統和電池測試技術領域保持領先地位,這得益於要求進行回收檢驗的永續性法規。南美洲智慧電網和寬頻容量的擴張也帶動了功率分析儀和射頻干擾分析儀的訂單成長。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 汽車電動交通領域對高壓、高頻寬測試解決方案的需求

- 亞洲5G/6G快速部署推動Sub-6GHz與毫米波測試能力發展

- 人工智慧驅動的設計檢驗工具可加快半導體產品上市速度。

- 歐洲整合式電動車電池週期計的應用日益普及。

- 加強北美醫療用電子設備的電磁相容性/電磁干擾標準

- 從資本投資轉向測試即服務 (TaaS) 訂閱模式

- 市場限制

- 租賃模式的轉變降低了新興市場新計量設備的平均售價(ASP)

- 射頻人才短缺阻礙毫米波測試的普及

- 全球校準標準片段化加劇了合規成本。

- 精密半導體貿易壁壘擾亂供應鏈

- 產業生態系分析

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 依產品

- 通用測試設備(GPTE)

- 機械測試設備(MTE)

- 模組化儀器(PXI、VXI、AXIe)

- 射頻/微波測試設備

- 自動測試設備(ATE)

- 特殊設備(電池、環境、訊號品質)

- 按服務類型

- 校對服務

- 維修和售後服務

- 資產管理及租賃服務

- 培訓和諮詢

- 按最終用戶行業分類

- 汽車與運輸

- 航太/國防

- 電訊和資訊技術

- 半導體和電子設備製造

- 醫療保健和醫療設備

- 教育和研究機構

- 工業自動化與能源

- 按外形規格

- 桌上型/機架式儀器

- 可攜式/手持設備

- 模組化/插件卡(USB、PCIe)

- 嵌入式/系統內測試模組

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家(丹麥、瑞典、挪威、芬蘭)

- 其他歐洲

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 東南亞

- 澳洲

- 亞太其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東

- GCC

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Keysight Technologies Inc.

- Rohde and Schwarz GmbH and Co. KG

- National Instruments Corporation

- Fortive Corp.(Tektronix, Fluke)

- Anritsu Corporation

- Yokogawa Electric Corporation

- Advantest Corporation

- Teradyne Inc.

- VIAVI Solutions Inc.

- Teledyne Technologies Inc.(Teledyne LeCroy)

- EXFO Inc.

- Pico Technology Ltd.

- Chroma ATE Inc.

- Hioki EE Corporation

- BandK Precision Corporation

- GW Instek(Good Will Instrument Co.)

- Rigol Technologies Co. Ltd.

- Boonton Electronics(Wireless Telecom Group)

- AMETEK Inc.(VTI Instruments)

- Spectrum Instrumentation GmbH

- Astro-Nova Inc.

第7章 市場機會與未來展望

Test and measurement market size in 2026 is estimated at USD 19.84 billion, growing from 2025 value of USD 19.06 billion with 2031 projections showing USD 24.26 billion, growing at 4.1% CAGR over 2026-2031.

Engineers are shifting from hardware-centric systems toward software-defined, subscription-based platforms that lighten capital requirements while lifting margins. Modular instrumentation, growing 4.7% annually through 2030, illustrates this transition as design teams seek reconfigurable architecture for complex devices. Asia Pacific leads demand, supported by 5G/6G build-outs and deep electronics manufacturing capacity, while the automotive push for e-mobility and healthcare's stricter compliance rules fuel segment expansion. Strategic consolidation- exemplified by Emerson's USD 8.2 billion acquisition of National Instruments - highlights the rising value of software-connected automated test ecosystems.

Global Test And Measurement Market Trends and Insights

Automotive e-mobility's demand for high-voltage, high-bandwidth testing solutions

Electric vehicle platforms operate between 400 V and 800 V and must meet strict safety and efficiency criteria. Tier-one laboratories have installed more than 200 dedicated stands for battery, inverter, and motor validation, enabling microsecond-level measurements across dynamic load and temperature profiles. Integrated power analyzers now sample at 1 MS/s to capture transient spikes that legacy equipment missed, ensuring drivetrain reliability under regenerative-braking regimes.

Rapid 5G/6G roll-outs driving sub-6 GHz and mmWave test capacity in Asia

China's early-2024 launch of a 6G test satellite set a benchmark for integrated space-ground networks. Operating above 50 GHz, mmWave links suffer high path loss, raising the bar for dynamic-range performance in spectrum analyzers. Demand for over-the-air chambers, phased-array characterization rigs and real-time signal recorders has accelerated as Asian carriers accelerate next-gen deployments.

Rental-shift depressing new instrument ASPs in emerging markets

Budget-constrained users favor rental contracts that eliminate up-front capex. Rental firms now bundle calibration and logistics, squeezing OEM margins and prompting vendors to design robust, field-serviceable gear. Hybrid models that mix subscription software with low-cost hardware updates are gaining traction.

Other drivers and restraints analyzed in the detailed report include:

- AI-enabled design-for-test tools shortening semiconductor time-to-market

- Increasing adoption of integrated EV battery cyclers in Europe

- Scarcity of RF talent hindering mmWave test adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The test and measurement market size for general-purpose test equipment remained dominant at 65.35% revenue share in 2025, underpinning a wide spectrum of R&D and manufacturing tasks. Growth, however, is pivoting toward modular instrumentation, which is expanding at a 4.55% CAGR through 2031 as engineers prioritize scalability and rapid reconfiguration. Design teams integrate PXI chassis with FPGA-based cards for mixed-signal consolidation, reducing rack footprints while preserving channel density.

Demand for RF and microwave test systems is also accelerating on the back of 5G handset launches and early 6G prototypes. Spectrum-analysis sensitivity, previously capped by thermal noise floors, now benefits from upgraded ADC resolution and low-phase-noise synthesizers. Mechanical test equipment, though essential for materials and structural validation, experiences slower replacement cycles because heavy frameworks remain serviceable for decades. Automated test equipment bridges high-volume semiconductor lines, combining parametric measurements with AI-driven outlier detection to keep yields above 99.5%.

Operational expenditure strategies are reshaping how firms procure measurement capability. Asset management and rental services, the fastest-growing service subset at a 6.05% CAGR, let manufacturers preserve cash while ensuring access to the latest platforms. Subscription bundles now include remote calibration, predictive maintenance, and compliance documentation. Nonetheless, calibration services kept a commanding 71.20% share of the test and measurement market size in 2025, reflecting the statutory need for traceable accuracy in semiconductor lithography, aerospace avionic,s and medical diagnostics.

Digital workflows are streamlining the calibration cycle. QR-coded asset tracking links each instrument to its service record, while automated fixtures reduce turnaround times by up to 25%. Remote firmware updates close metrological gaps between scheduled visits. Training and consulting services round out the portfolio, offering on-premises workshops that bridge skills gaps in power integrity, EMC, and safety-critical software validation.

The Test and Measurement Market Report is Segmented by Product (General-Purpose Test Equipment, Mechanical Test Equipment, and More), Service Type (Calibration, Repair/After-Sales, and More), End-User Industry (Automotive and Transportation, Aerospace and Defense, and More), Form Factor (Benchtop/Rack-Mounted Instruments, Portable Instruments, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific accounted for 37.62% of global revenue in 2025, reflecting deep electronics manufacturing ecosystems and aggressive 5G/6G infrastructure spend. China's field test network demonstrated a 10-fold performance gain, driving orders for multi-port vector network analyzers and OTA chambers. Taiwan and South Korea's foundries imported high-density probe stations to validate 2.5D packages for AI accelerators.

North America, the second-largest region, leveraged strong aerospace, defense, and medical sectors and strict FDA oversight requiring IEC 60601-based EMC verification. Investment in AI and cloud testing platforms accelerated after the 2024 infrastructure stimulus. Private-equity transactions in fiber, tower, and data-center assets lifted demand for field-portable optical-time-domain reflectometers and high-speed BERTs.

The Middle East and Africa displayed the fastest CAGR at 5.15% to 2031 as telecom carriers upgraded backhaul links and industrial operators adopted ISO-certified quality frameworks. Regional energy initiatives around hydrogen and solar projects also required precision electrical metering. Europe preserved its lead in EV powertrain and battery-testing competence, supported by sustainability regulations mandating recycling validation. South America's build-out of smart-grid and broadband capacity stimulated incremental orders for power analyzers and RF interference analyzers.

- Keysight Technologies Inc.

- Rohde and Schwarz GmbH and Co. KG

- National Instruments Corporation

- Fortive Corp. (Tektronix, Fluke)

- Anritsu Corporation

- Yokogawa Electric Corporation

- Advantest Corporation

- Teradyne Inc.

- VIAVI Solutions Inc.

- Teledyne Technologies Inc. (Teledyne LeCroy)

- EXFO Inc.

- Pico Technology Ltd.

- Chroma ATE Inc.

- Hioki E.E. Corporation

- BandK Precision Corporation

- GW Instek (Good Will Instrument Co.)

- Rigol Technologies Co. Ltd.

- Boonton Electronics (Wireless Telecom Group)

- AMETEK Inc. (VTI Instruments)

- Spectrum Instrumentation GmbH

- Astro-Nova Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Automotive E-Mobility's Demand for High-Voltage, High-Bandwidth Testing Solutions

- 4.2.2 Rapid 5G/6G Roll-outs Driving Sub-6 GHz and mmWave Test capacity in Asia

- 4.2.3 AI-Enabled Design-for-Test Tools Shortening Semiconductor Time-to-Market

- 4.2.4 Increasing Adoption of Integrated EV Battery Cyclers in Europe

- 4.2.5 Tightening EMC/EMI Norms for Medical Electronics in North America

- 4.2.6 Transition from CapEx to Test-as-a-Service Subscription Models

- 4.3 Market Restraints

- 4.3.1 Rental-Shift Depressing New Instrument ASPs in Emerging Markets

- 4.3.2 Scarcity of RF Talent Hindering mmWave Test Adoption

- 4.3.3 Fragmented Global Calibration Standards Raising Compliance Costs

- 4.3.4 Trade Barriers on Precision Semiconductors Disrupting Supply Chain

- 4.4 Industry Ecosystem Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product

- 5.1.1 General Purpose Test Equipment (GPTE)

- 5.1.2 Mechanical Test Equipment (MTE)

- 5.1.3 Modular Instrumentation (PXI, VXI, AXIe)

- 5.1.4 RF/Microwave Test Equipment

- 5.1.5 Automated Test Equipment (ATE)

- 5.1.6 Specialized Instruments (Battery, Environmental, Signal Integrity)

- 5.2 By Service Type

- 5.2.1 Calibration Services

- 5.2.2 Repair/After-Sales Services

- 5.2.3 Asset Management and Rental Services

- 5.2.4 Training and Consulting

- 5.3 By End-user Industry

- 5.3.1 Automotive and Transportation

- 5.3.2 Aerospace and Defense

- 5.3.3 Telecommunications and IT

- 5.3.4 Semiconductor and Electronics Manufacturing

- 5.3.5 Healthcare and Medical Devices

- 5.3.6 Education and Research Laboratories

- 5.3.7 Industrial Automation and Energy

- 5.4 By Form Factor

- 5.4.1 Benchtop/Rack-Mounted Instruments

- 5.4.2 Portable/Handheld Instruments

- 5.4.3 Modular/Plug-in Cards (USB, PCIe)

- 5.4.4 Embedded/In-System Test Modules

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Nordics (Denmark, Sweden, Norway, Finland)

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 South Korea

- 5.5.3.4 India

- 5.5.3.5 Southeast Asia

- 5.5.3.6 Australia

- 5.5.3.7 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East

- 5.5.5.1 Gulf Cooperation Council Countries

- 5.5.5.2 Turkey

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)}

- 6.4.1 Keysight Technologies Inc.

- 6.4.2 Rohde and Schwarz GmbH and Co. KG

- 6.4.3 National Instruments Corporation

- 6.4.4 Fortive Corp. (Tektronix, Fluke)

- 6.4.5 Anritsu Corporation

- 6.4.6 Yokogawa Electric Corporation

- 6.4.7 Advantest Corporation

- 6.4.8 Teradyne Inc.

- 6.4.9 VIAVI Solutions Inc.

- 6.4.10 Teledyne Technologies Inc. (Teledyne LeCroy)

- 6.4.11 EXFO Inc.

- 6.4.12 Pico Technology Ltd.

- 6.4.13 Chroma ATE Inc.

- 6.4.14 Hioki E.E. Corporation

- 6.4.15 BandK Precision Corporation

- 6.4.16 GW Instek (Good Will Instrument Co.)

- 6.4.17 Rigol Technologies Co. Ltd.

- 6.4.18 Boonton Electronics (Wireless Telecom Group)

- 6.4.19 AMETEK Inc. (VTI Instruments)

- 6.4.20 Spectrum Instrumentation GmbH

- 6.4.21 Astro-Nova Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

測試和測量設備市場:2026-2032年全球市場預測(按產品類型、測試類型、服務、應用和最終用戶產業分類)電氣測量儀器市場:2026-2032年全球市場預測(依儀器類型、設備類型、應用及最終用戶產業分類)視覺測量設備市場:按組件、技術、產品類型、價格範圍和應用分類-2026-2032年全球預測水基火炬流量計市場:按技術、部署類型、測量範圍和終端用戶產業分類的全球預測,2026-2032年AC/DC高壓分壓器市場:按類型、應用、最終用戶、分銷管道分類,全球預測(2026-2032年)高壓突波突波產生器市場:按發生器類型、電壓範圍、波形、技術、額定功率、安裝方式、終端用戶產業和應用分類-全球預測,2026-2032年按產品類型、技術、終端用戶產業和銷售管道分類的形狀和輪廓測量儀器市場,全球預測,2026-2032年

測試和測量設備市場:2026-2032年全球市場預測(按產品類型、測試類型、服務、應用和最終用戶產業分類)電氣測量儀器市場:2026-2032年全球市場預測(依儀器類型、設備類型、應用及最終用戶產業分類)視覺測量設備市場:按組件、技術、產品類型、價格範圍和應用分類-2026-2032年全球預測水基火炬流量計市場:按技術、部署類型、測量範圍和終端用戶產業分類的全球預測,2026-2032年AC/DC高壓分壓器市場:按類型、應用、最終用戶、分銷管道分類,全球預測(2026-2032年)高壓突波突波產生器市場:按發生器類型、電壓範圍、波形、技術、額定功率、安裝方式、終端用戶產業和應用分類-全球預測,2026-2032年按產品類型、技術、終端用戶產業和銷售管道分類的形狀和輪廓測量儀器市場,全球預測,2026-2032年 2026-2030年全球測試與測量市場

2026-2030年全球測試與測量市場 測試測量設備市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區的洞察,2026-2034年預測

測試測量設備市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區的洞察,2026-2034年預測 測試和測量設備市場規模、佔有率和趨勢分析報告:按產品、服務、最終用途、地區和細分市場預測(2026-2033 年)

測試和測量設備市場規模、佔有率和趨勢分析報告:按產品、服務、最終用途、地區和細分市場預測(2026-2033 年)