|

市場調查報告書

商品編碼

1934905

資料中心線纜:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Data Center Wire And Cable - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

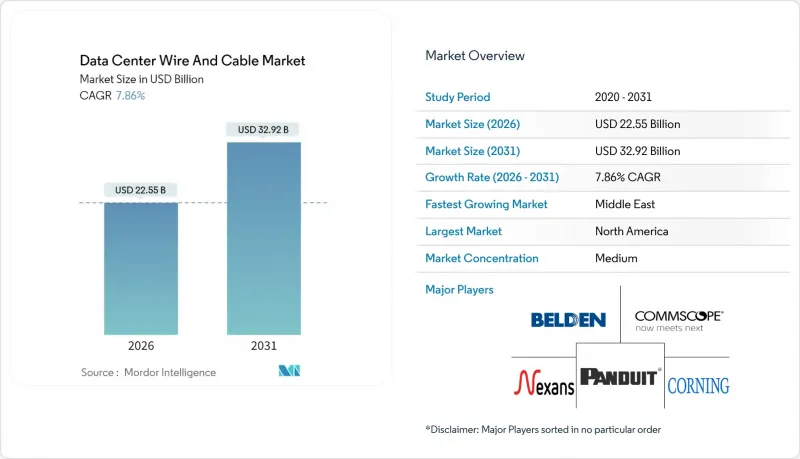

資料中心線纜市場預計將從 2025 年的 209.1 億美元成長到 2026 年的 225.5 億美元,預計到 2031 年將達到 329.2 億美元,2026 年至 2031 年的複合年成長率為 7.86%。

超大規模資料中心的持續建置、向400G和800G光連接模組的快速轉型,以及人工智慧和高效能運算(HPC)工作負載的激增需求,是推動成長的核心動力。新建設採用的結構化佈線佈局密度是傳統以CPU為中心的機房的五倍,光纖在機架內和機架間鏈路中的消耗量已超過銅纜。受5G和對延遲敏感的應用推動,邊緣資料中心和微型資料中心的部署,為環境友善和耐熱線設計創造了新的應用場景。諸如「建造美國,購買美國貨」法案等政策獎勵正在推動國內光纖投資,而歐洲的永續性法規則推動了低損耗和可回收材料的採購。商品價格波動仍是關注的焦點,預計到2024年銅價將達到每磅5.20美元,將使線纜成本上漲高達35%。

全球資料中心線市場趨勢與洞察

全球資料中心穩步擴張

超大規模雲端營運商宣布將於2025年在美國、印度和印尼建造一系列千兆瓦級園區,每個園區都需要數百萬個光纖終端。平均機架功率密度將從2022年的15千瓦提升至新建人工智慧機房的40千瓦,每個機架的水平電纜長度也隨之翻倍。這促使安裝商透過增加電纜配線架容量和採用預端接主幹線束來縮短安裝週期。儘管新加坡和馬來西亞的地方政府對新建資料中心許可證的數量設定了上限,但柔佛新山和鳳凰城等區域性城市的新計畫正在抵消這一影響。能夠保證快速交付多模光纖組件的供應商正在贏得與超大規模資料中心業者簽訂的多年期供貨合約。

人工智慧/高效能運算工作負載的快速成長需要超低延遲鏈路

基於數萬個GPU的訓練叢集,每台伺服器所需的跳線數量是CPU機架的四到五倍,這使得材料清單清單轉向高密度MPO-MPO主幹網路。乙太網路正在大規模AI架構中取代InfiniBand,推動了400G和800G短距離光學模組的廣泛應用,這些模組符合葉脊式架構模型。康寧的Contour Flow光纜在與傳統144芯光纖束相同的外徑下可容納288根光纖,從而將佈線擁塞減少了一半。 GPU節點間5微秒的低延遲需求迫使營運商盡可能減少連接點,從而推動了工廠端接解決方案的需求,並刺激了對精密拋光MT連接器的需求。

高密度束的溫度控管挑戰

電纜橋架內部的氣流限制會提高進氣溫度,每升高1°C,DWDM鏈路裕量就會降低0.08 dB。液冷歧管會佔用電纜配線架的空間,迫使設計人員重新佈線,採用更小的彎曲半徑,增加微彎損耗的風險。供應商正在推出耐溫85°C的無凝膠電纜,並引入扁平包裝的主幹線纜,其面積比圓形設計減少了30%。營運商正在嘗試使用耐熱拉片,以便在溫度高達55°C的通道中方便連接,但頻繁重新端接帶來的高昂營運成本仍需要納入預算。

細分市場分析

預計到2025年,光纖將佔資料中心線纜市場59.30%的佔有率,到2031年將以8.12%的複合年成長率成長,並在幾乎所有指標上超越銅纜。到2031年,光纖電纜的資料中心市場規模預計將達到198億美元,這表明光纖電纜對於升級到400G、800G以及即將到來的1.6T技術至關重要。銅纜數據線在10G以下和低延遲旁路區域仍然有用,但不斷增加的熱負載和電磁干擾(EMI)問題限制了其傳輸距離。電力電纜雖然尺寸較小,但隨著機架功率超過90kW以及設施採用415V配電,仍至關重要。

技術創新正致力於提高光纖密度。康寧的SMF-28 Contour光纖連接器可將288根光纖裝入傳統的144芯光纖外殼中,使設計人員的彎曲半徑放寬40%。在短距離、低電流應用中,銅包鋁光纖逐漸成為替代方案,以抵銷金屬價格波動的影響。供應商也正在推出採用生物基護套的光纖組件,以符合歐洲環境法規。將電纜、連接器和收發器整合到一起進行協同設計,推動了供應商之間的差異化競爭,並促成了長期主服務協議的建立。

超大規模資料中心將佔據資料中心線材市場最大佔有率,到2025年將佔總營收的48.60%。然而,邊緣和微節點部署將以8.78%的複合年成長率推動市場成長,預計到2031年,這些部署的資料中心線線市場規模將達到65.5億美元。位於俄亥俄州、維吉尼亞和北方邦的千兆級資料中心需要數千公里的單模光纖來互連GPU模組。另一方面,預製微型EDC(µEDC)雖然可以縮短佈線距離,但需要堅固的護套和IP防護等級的連接器,因此價格更高。

法蘭克福和阿什本的託管服務供應商正持續升級其結構化佈線系統,以吸引人工智慧租戶,而許多傳統企業設施則選擇雲端卸載而非昂貴的維修。供應商正在最佳化產品規格,在超大規模資料中心內部佈線時採用抗彎多模光纖,在走道機櫃中使用鎧裝鬆套管。隨著5G獨立組網核心網路的普及,微型站點也開始部署乙太網路供電(PoE)技術用於無線終端,這略微增加了對銅纜的需求。集中式和分散式投資的平衡將決定供應商如何分配研發資金。

區域分析

2025年,北美引領資料中心線纜市場,這主要得益於超過340億美元的超大規模投資以及聯邦政府強制要求公共資助的寬頻計畫使用國產光纖的政策。康寧、康普和AFL三家公司已承諾總合超過5億美元用於新增產能,從而降低對進口的依賴並縮短計劃前置作業時間。加拿大魁北克省的寒冷氣候和可再生能源優勢正吸引許多託管設施落腳於此。在墨西哥,近岸外包正在振興克雷塔羅的Tier III級資料中心,這些資料中心現在需要熟悉美國標準的雙語安裝人員。

亞太地區將在2031年前實現最高的區域複合年成長率,這主要得益於印度的資料主權法規和中國雲端運算服務的擴張。新加坡的建設禁令鼓勵業者向柔佛州和巴淡島擴張,重振了跨境光纖走廊。澳洲在其西海岸完成了一條新的海底光纜登陸,連接珀斯、Muscat和蒙巴薩。同時,日本和韓國在1.6T乙太網路的研發方面主導,刺激了國內對原型幹線光纜的需求。

歐洲市場保持穩定,但監管嚴格,EN 50575 和 CPR 法規要求永久安裝在建築物內的電纜必須帶有 CE 標誌和防火等級認證。德國、荷蘭和北歐國家正在競相開發可再生能源和建造穩定的電網,並積極推廣永續性的電纜規格。中東和非洲地區雖然規模較小,但正經歷兩位數的成長,阿拉伯聯合大公國、沙烏地阿拉伯和肯亞等國吸引了許多國際雲端營運商。儘管政治風險溢價依然存在,但環繞非洲大陸的海底光纜計劃確保了對超長距離光纖的長期需求。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 全球資料中心穩步擴張

- 人工智慧/高效能運算工作負載的快速成長需要超低延遲鏈路

- 400G/800G光連接模組的快速普及

- 邊緣和微型資料中心的興起

- 低損耗可回收電纜的永續性要求

- 政府對國內光纖和電力電纜生產的激勵措施

- 市場限制

- 高密度束的溫度控管挑戰

- 現有設施的高速電纜維修

- 銅鋁原料價格波動;

- 先進光纖端接工藝技術純熟勞工短缺

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 定價分析

- 投資分析

5. 全球資料中心建設活動分析

- 未來資料中心建設熱點地區(計畫中的IT負載成長)

- 超大規模資料中心的成長

- 區域資料中心建置趨勢 - 供應商概況

第6章 市場規模與成長預測

- 按電纜類型

- 光纖電纜

- 銅質數據線(雙絞線)

- 電源線

- 電壓類型

- 高壓(HV)

- 中壓(MV)

- 低壓(LV)

- 材料類型

- 銅

- 鋁

- 應用

- PDU 和 UPS 系統

- 暖通空調系統

- 網路及IT設備

- 其他

- 電壓類型

- 其他電纜(接地線、感測器線、控制線)

- 依資料中心類型

- 企業/邊緣/微型

- 搭配

- 超大規模

- 透過使用

- 結構化佈線

- 配電

- 暖通空調和建築系統

- 監控與控制

- 高速互連(100G以上)

- 透過索結構

- 盾

- 無防護

- 盔甲

- 普倫姆評級

- 按部署環境

- 室內(閒置頻段)

- 戶外植物

- 海底與設施之間

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 北歐地區

- 俄羅斯

- 其他歐洲

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞

- 亞太其他地區

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 北美洲

第7章 競爭情勢

- 市佔率分析

- 公司簡介

- Nexans SA

- Belden Inc.

- Panduit Corp.

- CommScope Holding Co. Inc.

- Corning Inc.

- TE Connectivity plc

- Yangtze Optical Fibre and Cable(YOFC)

- Legrand Group

- Southwire Company LLC

- Furukawa Electric Co. Ltd.

- Prysmian Group

- Sumitomo Electric Industries Ltd.

- LS Cable and System

- Superior Essex Inc.

- AFL Global

- Rosenberger Hochfrequenztechnik GmbH

- Hexatronic Group AB

- HUBER+SUHNER AG

- Fujikura Ltd.

- Datwyler IT Infra

- Ciena Corporation

- Tratos Cavi SpA

第8章:市場機會與未來展望

- 評估差距和未滿足的需求

The Data Center Wire and Cable market is expected to grow from USD 20.91 billion in 2025 to USD 22.55 billion in 2026 and is forecast to reach USD 32.92 billion by 2031 at 7.86% CAGR over 2026-2031.

Continued hyperscale construction, rapid migration to 400 G and 800 G optical interconnects, and surging demand from AI and high-performance computing (HPC) workloads are the core growth engines. New-build facilities now specify structured cabling footprints up to five times denser than legacy CPU-centric halls, pushing optical-fiber consumption ahead of copper for intra-rack and inter-rack links. Edge and micro-data-center roll-outs, accelerated by 5G and latency-sensitive applications, are creating fresh use cases for ruggedized, temperature-hardened cable designs. Policy incentives such as the Build America Buy America Act are spurring domestic fiber investments, while sustainability mandates in Europe are steering purchasing toward low-loss and recyclable formulations. Commodity volatility remains a watch item; copper briefly touched USD 5.20 per pound in 2024 and lifted cable bills by as much as 35%.

Global Data Center Wire And Cable Market Trends and Insights

Robust Data-Center Expansion Worldwide

Hyperscale cloud operators announced multi-gigawatt campuses across the United States, India, and Indonesia in 2025, each demanding several million fiber terminations. Average rack densities rose from 15 kW in 2022 to 40 kW in new AI halls, doubling the horizontal cable runs per rack. Contractors, therefore, specify higher cable-tray capacities and pre-terminated trunk bundles to compress installation schedules. Regional governments in Singapore and Malaysia capped new data-center permits, yet green-field projects in secondary metros such as Johor Bahru and Phoenix offset the slowdown. Suppliers able to guarantee short lead times on multimodal assemblies are winning multi-year supply agreements with hyperscalers.

Surge in AI/HPC Workloads Requiring Ultra-Low-Latency Links

Training clusters built around tens of thousands of GPUs need four to five times more fiber jumpers per server than CPU racks, shifting bill-of-materials weighting toward high-density MPO-to-MPO trunks. Ethernet is overtaking InfiniBand for large-scale AI fabrics, prompting broad adoption of 400 G and 800 G short-reach optics that still fit the leaf-and-spine model. Corning's Contour Flow cable now ships with 288 fibers in the same outer diameter as earlier 144-fiber bundles, halving pathway congestion. Latency budgets of 5 µs between GPU nodes force operators to minimize splice points, favoring factory-terminated solutions and driving demand for precision-polished MT-based connectors.

Thermal-Management Challenges in High-Density Bundles

Airflow constriction inside cable ladders raises inlet temperatures, and each 1 °C rise cuts DWDM link margin by 0.08 dB. Liquid-cooling manifolds occupy space once used for cable trays, forcing designers to reroute bundles in tighter radii that risk micro-bending losses. Vendors counter with gel-free cables rated to 85 °C and introduce flat-pack trunk formats that occupy 30% less cross-section than round designs. Operators trial heat-resistant pull-tabs to ease port access inside 55 °C aisles but still budget higher OpEx for frequent re-termination.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of 400 G/800 G Optical Interconnects

- Proliferation of Edge and Micro Data Centers

- Retrofitting Legacy Facilities with High-Speed Cabling

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Optical fiber captured 59.30% of the Data Center Wire and Cable market in 2025 and is forecast to grow at an 8.12% CAGR to 2031, outpacing copper on nearly every metric. The Data Center Wire and Cable market size for fiber cables is projected to reach USD 19.8 billion by 2031, reflecting its indispensability for 400 G, 800 G, and forthcoming 1.6 T upgrades. Copper data cables retain relevance below 10 G and in low-latency bypass zones, yet rising thermal loads and EMI concerns cap their lane length. Power cables, while volumetrically smaller, remain mission-critical as rack power climbs past 90 kW and facilities adopt 415 V distribution.

Innovation centers on density: Corning's SMF-28 Contour enables 288 fibers within earlier 144-fiber envelopes, giving designers 40% bend-radius relief. Copper-clad aluminum substitutes appear in short, low-ampacity applications to offset metal volatility. Vendors also release fiber-optic assemblies with bio-based jackets to meet European environmental regulations. The race to co-design cable, connector, and transceiver as a holistic channel differentiates suppliers and cements long-term master-service agreements.

Hyperscale facilities held 48.60% of 2025 revenue, equal to the largest share in the Data Center Wire and Cable market. Edge and micro nodes, however, lead growth at 8.78% CAGR, lifting the Data Center Wire and Cable market size for these deployments to USD 6.55 billion by 2031. Gigawatt-scale campuses in Ohio, Virginia, and Uttar Pradesh require thousands of kilometers of single-mode fiber to interconnect GPU pods. Conversely, prefabricated µEDCs consume shorter runs but demand ruggedized sheathing and IP-rated connectors that command premium pricing.

Colocation operators in Frankfurt and Ashburn keep refreshing structured cabling to court AI tenants, yet many legacy enterprise halls opt for cloud offload rather than expensive overhauls. Suppliers tailor SKUs: bend-insensitive multimode for hyperscale intra-build runs and armored loose-tube for sidewalk cabinets. As 5G standalone cores proliferate, micro sites also install power-over-ethernet for radio heads, subtly raising copper volumes. The balance between centralized and distributed spends will dictate the allocation of R&D funds across vendors.

The Data Center Wire and Cable Market is Segmented by Cable Type (Optical Fiber, Copper Data and More), Data Center Type (Enterprise, Colocation and More), Application (Structured Cabling, Power Distribution and More), Cable Construction(Shielded, Unshielded and More), Deployment Environment (Indoor White Space, Outdoor Plant and More), and Geography(North America, and More). Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led the Data Center Wire and Cable market in 2025, driven by hyperscale investments exceeding USD 34 billion and reinforced by federal policies mandating domestic fiber for publicly funded broadband projects. Corning, CommScope, and AFL collectively pledged more than USD 500 million in new capacity, reducing import reliance and shortening project lead times. Canada benefits from colder climates and renewable energy, luring colocation builds in Quebec. Mexico's near-shoring wave fuels Tier III halls in Queretaro, which now require bilingual installation crews versed in U.S. standards.

Asia-Pacific delivers the highest regional CAGR through 2031, propelled by India's data-sovereignty rules and China's cloud service scale-up. Singapore's construction moratorium pushed operators to Johor and Batam, stimulating cross-border fiber corridors. Australia records new submarine landings on its western coast, linking Perth to Muscat and Mombasa. Meanwhile, Japan and South Korea spearhead 1.6 T Ethernet R&D, accelerating domestic demand for prototype trunk cables.

Europe remains steady but highly regulated; EN 50575 and CPR rules require CE marking and fire-class certification for any cable permanently installed in buildings. Germany, the Netherlands, and the Nordics compete on renewable energy availability and stable grids, fostering sustainability-driven cable specifications. Middle East and Africa, though smaller, post double-digit growth as UAE, Saudi Arabia, and Kenya entice international cloud incumbents. Subsea projects circling the African continent guarantee long-term pull for ultra-long-haul fiber, even as political risk premiums linger.

- Nexans S.A.

- Belden Inc.

- Panduit Corp.

- CommScope Holding Co. Inc.

- Corning Inc.

- TE Connectivity plc

- Yangtze Optical Fibre and Cable (YOFC)

- Legrand Group

- Southwire Company LLC

- Furukawa Electric Co. Ltd.

- Prysmian Group

- Sumitomo Electric Industries Ltd.

- LS Cable and System

- Superior Essex Inc.

- AFL Global

- Rosenberger Hochfrequenztechnik GmbH

- Hexatronic Group AB

- HUBER+SUHNER AG

- Fujikura Ltd.

- Datwyler IT Infra

- Ciena Corporation

- Tratos Cavi S.p.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Robust data-center expansion worldwide

- 4.2.2 Surge in AI/HPC workloads requiring ultra-low-latency links

- 4.2.3 Rapid adoption of 400G/800G optical inter-connects

- 4.2.4 Proliferation of edge and micro data centers

- 4.2.5 Sustainability mandates for low-loss recyclable cabling

- 4.2.6 Government incentives for domestic fiber and power-cable production

- 4.3 Market Restraints

- 4.3.1 Thermal-management challenges in high-density bundles

- 4.3.2 Retrofitting legacy facilities with high-speed cabling

- 4.3.3 Volatility in copper and aluminum commodity prices

- 4.3.4 Skilled-labor shortage for advanced fiber termination

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Pricing Analysis

- 4.9 Investment Analysis

5 ANALYSIS OF DATA CENTER CONSTRUCTION ACTIVITY WORLDWIDE

- 5.1 Upcoming Data Center Construction Hotspots (planned IT-load additions)

- 5.2 Growth of Hyperscale Data Centers

- 5.3 Regional DC Construction - Vendor Landscape

6 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 6.1 By Cable Type

- 6.1.1 Optical Fiber Cables

- 6.1.2 Copper Data Cables (Twisted Pair)

- 6.1.3 Power Cables

- 6.1.3.1 Voltage Type

- 6.1.3.1.1 High Voltage (HV)

- 6.1.3.1.2 Medium Voltage (MV)

- 6.1.3.1.3 Low Voltage (LV)

- 6.1.3.2 Material Type

- 6.1.3.2.1 Copper

- 6.1.3.2.2 Aluminum

- 6.1.3.3 Application

- 6.1.3.3.1 PDUs and UPS Systems

- 6.1.3.3.2 HVAC System

- 6.1.3.3.3 Networking and IT Equipment

- 6.1.3.3.4 Others

- 6.1.3.1 Voltage Type

- 6.1.4 Other Cables (Grounding, Sensor, Control)

- 6.2 By Data Center Type

- 6.2.1 Enterprise/ Edge / Micro

- 6.2.2 Colocation

- 6.2.3 Hyperscale

- 6.3 By Application

- 6.3.1 Structured Cabling

- 6.3.2 Power Distribution

- 6.3.3 HVAC and Building Systems

- 6.3.4 Monitoring and Control

- 6.3.5 High-Speed Interconnects (>100 G)

- 6.4 By Cable Construction

- 6.4.1 Shielded

- 6.4.2 Unshielded

- 6.4.3 Armored

- 6.4.4 Plenum-Rated

- 6.5 By Deployment Environment

- 6.5.1 Indoor (White Space)

- 6.5.2 Outdoor Plant

- 6.5.3 Sub-sea / Inter-facility

- 6.6 By Geography

- 6.6.1 North America

- 6.6.1.1 United States

- 6.6.1.2 Canada

- 6.6.1.3 Mexico

- 6.6.2 South America

- 6.6.2.1 Brazil

- 6.6.2.2 Argentina

- 6.6.2.3 Rest of South America

- 6.6.3 Europe

- 6.6.3.1 Germany

- 6.6.3.2 United Kingdom

- 6.6.3.3 France

- 6.6.3.4 Nordic Region

- 6.6.3.5 Russia

- 6.6.3.6 Rest of Europe

- 6.6.4 Asia-Pacific

- 6.6.4.1 China

- 6.6.4.2 India

- 6.6.4.3 Japan

- 6.6.4.4 South Korea

- 6.6.4.5 Southeast Asia

- 6.6.4.6 Rest of Asia-Pacific

- 6.6.5 Middle East

- 6.6.5.1 UAE

- 6.6.5.2 Saudi Arabia

- 6.6.5.3 Turkey

- 6.6.5.4 Rest of Middle East

- 6.6.6 Africa

- 6.6.6.1 South Africa

- 6.6.6.2 Nigeria

- 6.6.6.3 Rest of Africa

- 6.6.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Market Share Analysis

- 7.2 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 7.2.1 Nexans S.A.

- 7.2.2 Belden Inc.

- 7.2.3 Panduit Corp.

- 7.2.4 CommScope Holding Co. Inc.

- 7.2.5 Corning Inc.

- 7.2.6 TE Connectivity plc

- 7.2.7 Yangtze Optical Fibre and Cable (YOFC)

- 7.2.8 Legrand Group

- 7.2.9 Southwire Company LLC

- 7.2.10 Furukawa Electric Co. Ltd.

- 7.2.11 Prysmian Group

- 7.2.12 Sumitomo Electric Industries Ltd.

- 7.2.13 LS Cable and System

- 7.2.14 Superior Essex Inc.

- 7.2.15 AFL Global

- 7.2.16 Rosenberger Hochfrequenztechnik GmbH

- 7.2.17 Hexatronic Group AB

- 7.2.18 HUBER+SUHNER AG

- 7.2.19 Fujikura Ltd.

- 7.2.20 Datwyler IT Infra

- 7.2.21 Ciena Corporation

- 7.2.22 Tratos Cavi S.p.A.

8 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 8.1 White-Space and Unmet-Need Assessment

NeoCloud 資料中心NeoCloud 資料中心:市場資料概覽(2026 年第二季)

NeoCloud 資料中心NeoCloud 資料中心:市場資料概覽(2026 年第二季) 2026年全球人工智慧(AI)資料中心網路市場報告

2026年全球人工智慧(AI)資料中心網路市場報告 資料中心網路市場:2026-2032年全球市場預測(依產品類型、部署模式、連接埠速度、應用程式和最終用戶分類)自癒網路市場:按組件、部署類型、組織規模、應用程式和最終用戶分類-2026年至2032年全球市場預測2026年全球自癒網路市場報告2026年全球雲端資料中心市場報告

資料中心網路市場:2026-2032年全球市場預測(依產品類型、部署模式、連接埠速度、應用程式和最終用戶分類)自癒網路市場:按組件、部署類型、組織規模、應用程式和最終用戶分類-2026年至2032年全球市場預測2026年全球自癒網路市場報告2026年全球雲端資料中心市場報告 資料中心網路市場分析及預測(至2035年):依類型、產品類型、服務、技術、元件、應用、部署模式、最終使用者及解決方案分類

資料中心網路市場分析及預測(至2035年):依類型、產品類型、服務、技術、元件、應用、部署模式、最終使用者及解決方案分類 全球資料中心線市場:市場規模、佔有率和趨勢分析(按線纜類型、資料中心類型、應用、部署方式和地區分類),細分市場預測(2026-2033 年)

全球資料中心線市場:市場規模、佔有率和趨勢分析(按線纜類型、資料中心類型、應用、部署方式和地區分類),細分市場預測(2026-2033 年) 全球資料中心網路市場:按產品、網路基礎設施、軟體、服務、工作負載類型、資料中心規模和容量、最終用戶和地區分類-預測至2031年

全球資料中心網路市場:按產品、網路基礎設施、軟體、服務、工作負載類型、資料中心規模和容量、最終用戶和地區分類-預測至2031年