|

市場調查報告書

商品編碼

1934902

汽車零件:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Automotive Parts - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

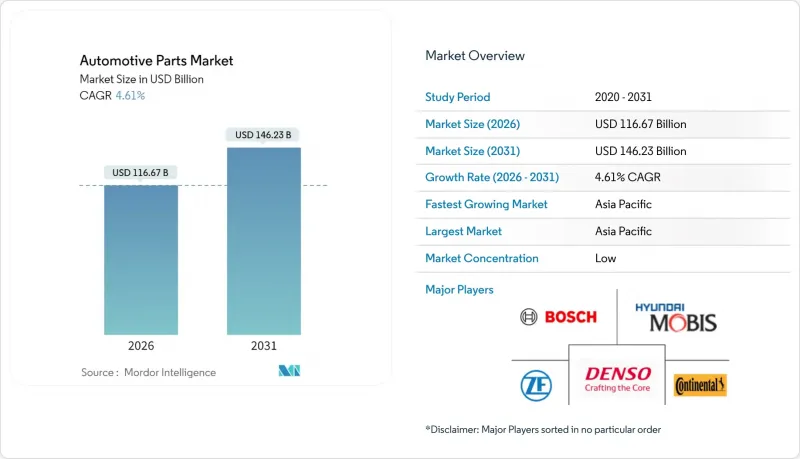

2025年汽車零件市場價值為1,115.3億美元,預計到2031年將達到1,462.3億美元,而2026年為1,166.7億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 4.61%。

汽車產量不斷成長、全球車齡化帶來的穩定售後市場需求以及加速推進的電氣化進程,共同支撐著這條溫和的成長軌跡。電動動力傳動系統正在降低對某些內燃機零件的需求,同時將收入來源轉向更高價值的電氣和電子元件。數位商務正在重塑全球零件通路,將成千上萬的小規模供應商納入正規的價值鏈。亞太地區擁有結構性的成本優勢、大規模的製造業基礎和深厚的本地需求,使其在採購新車方面佔據了不成比例的優勢。同時,半導體短缺、原料成本波動以及日益嚴格的數據存取法規仍然是可能影響季度產量和盈利的關鍵不利因素。

全球汽車零件市場趨勢與洞察

全球汽車產量增加

預計2023年全球汽車產量將達到9,050萬輛,恢復新冠疫情前的水平,但2024年將放緩至8,850萬輛,之後再次回升。產量的成長與原廠配套和售後市場零件需求的增加直接相關,尤其是在汽車保有量持續成長的新興市場。中國正轉型為主要出口低成本內燃機汽車和電動車的淨出口國,這正在重塑全球供應鏈,並為零零件供應商創造新的需求模式。向「多能源」生產線的轉型使製造商能夠在應對市場不確定性的同時,保持不同動力傳動系統技術零件需求的穩定性。

軟體定義車輛需要可升級的硬體

預計未來幾年汽車軟體市場將迎來強勁成長,業內高階主管預測,到2035年,汽車將實現軟體定義和人工智慧驅動。這項轉型需要一種截然不同的硬體架構,以支援空中下載(OTA)更新和持續的功能增強。與傳統的固定功能汽車零件不同,軟體定義汽車需要一個模組化、可升級的硬體平台,以適應車輛生命週期內不斷變化的軟體需求。這種轉變正在推動對高效能運算單元、先進感測器和可遠端重新編程的靈活電控系統(ECU)的需求,從而為這些先進零件的供應商創造新的商機。

半導體持續短缺

儘管採取了復甦措施,汽車半導體市場仍面臨供應緊張的局面,在短缺高峰期,該產業的產量下降幅度高達40%。汽車產業向軟體定義汽車的轉型預計將使每輛車的半導體成本從2023年的800美元增加到2030年的1,350美元。由於生產區域集中以及汽車級零件採購前置作業時間長,供應鏈的脆弱性仍然存在。此次短缺對高級駕駛輔助系統(ADAS)和資訊娛樂系統組件的影響尤其嚴重,迫使原始設備製造商(OEM)優先分配晶片,並在某些情況下,為了維持生產進度,不得不從車輛中移除某些功能。

細分市場分析

到2025年,電氣和電子元件將佔據最大的市場佔有率,達到29.56%,預計到2031年將以9.12%的複合年成長率實現最快成長。這兩個細分市場的主導地位反映了汽車產業向聯網汽車、自動駕駛和電動車的根本性轉變,而這些轉變需要先進的電子系統。一輛現代汽車平均包含80個感測器和100個電子單元,預計到2030年,電子元件將佔新車成本的50%。此細分市場包括ADAS(高級駕駛輔助系統)、資訊娛樂平台、電池管理系統和V2X(車聯網)模組等關鍵系統。

傳動系統和動力傳動系統總成部件正面臨複雜的變革時期,傳統內燃機部件的需求不斷下降,而電動動力傳動系統部件的需求卻在快速成長。內裝和外觀設計受益於優質化趨勢和對使用者體驗日益重視,座艙技術正成為關鍵的差異化因素,尤其是在軟體定義車輛中。車身和底盤部件也在不斷發展,以適應新型材料和輕量化要求。同時,車輪和輪胎市場保持相對穩定,其成長主要得益於老舊車輛的更換需求以及全球汽車保有量的成長。

到2025年,內燃機汽車仍將維持75.88%的最大市場佔有率,這反映出現有車輛的普及以及許多全球市場持續的生產。然而,在監管要求、電池技術進步和充電基礎設施擴展的推動下,電池式電動車(BEV)將成為成長最快的細分市場,年複合成長率高達34.1%。到2024年,全球電動車產量將達到1,730萬輛,其中中國產量將達到1,240萬輛,佔全球總產量的70%以上。

混合動力汽車和插電式混合動力汽車屬於過渡性技術,需要同時具備電動動力傳動系統和內燃機的零件,這增加了供應商的複雜性,也使需求模式多樣化。燃料電池電動車目前仍屬於小眾市場,但在商用車領域前景廣闊,因為氫的能量密度優勢在那裡更為顯著。動力系統配置因地區而異,中國和歐洲在電氣化方面處於領先地位。同時,北美和新興市場仍保持著較高的內燃機汽車佔有率,這就要求供應商保持靈活的生產能力,以適應多種動力傳動系統技術。

區域分析

亞太地區將保持主導地位,到2025年市場佔有率將達到45.31%,並在2031年之前以6.19%的複合年成長率引領區域成長,這主要得益於中國汽車製造業的優勢和不斷擴大的國內市場。預計2024年,中國將生產1,240萬輛電動車,佔全球電動車產量的70%以上,並轉型為汽車淨出口國。這種生產國和出口國的雙重角色,使得國內外汽車零件的需求都大幅成長。預計到2028年,印度汽車售後市場規模將達到140億美元,主要得益於汽車保有量的成長和售後服務需求的增加。日本將繼續發揮其在先進零件領域的技術優勢,包括混合動力傳動系統和精密製造技術。同時,韓國則專注於電動車技術和用於汽車應用的半導體解決方案。

北美和歐洲是擁有成熟汽車生態系統的成熟市場,但在適應產業轉型方面面臨獨特的挑戰。規模達640億歐元的歐洲汽車售後市場正面臨經濟波動、監管變化以及向電動車轉型帶來的壓力,因為電動車無需傳統的維護服務。該地區的獨立售後市場佔市場佔有率的60%,這主要得益於老齡化車隊和注重預算的消費者,但預計在2026年後,由於電動車普及的影響,其成長速度將會放緩。北美受益於近岸外包趨勢和支持本土電動車生產的抗通膨立法,但貿易政策和來自中國汽車製造商的競爭可能會對其市場造成衝擊。

南美、中東和非洲等新興市場雖然目前市佔率較小,但展現出巨大的成長潛力。受美國電動車產量擴張和對電子元件需求成長的推動,墨西哥汽車零件產業預計在2024年將吸引超過25億美元的外國直接投資,較去年同期成長23.5%。在中東和北非地區,2024年第一季宣布了11個新的汽車計劃,總投資額超過29億美元,其中沙烏地阿拉伯投資13億美元的電動車製造綜合體項目主導。這些地區政府主導的旨在發展汽車產業和降低進口依賴的舉措,正在為國內外零件供應商創造商機。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 全球汽車產量增加

- 適用於軟體定義車輛 (SDV) 的可升級硬體

- 老舊車隊推動售後市場支出增加

- 電子商務零件平台快速成長

- 「維修權」立法提高了獨立服務提供者的佔有率

- 促進尖端材料零件的輕量化

- 市場限制

- 半導體持續短缺

- 由於向電動車的轉型,對內燃機零件的需求下降

- 原物料價格波動正在擾亂我們的成本結構。

- 主要製造地勞動力短缺

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 主要供應商資訊(按類型)

第5章 市場規模及成長預測(價值(美元))

- 按類型

- 傳動系統和動力傳動系統

- 內部和外部

- 電氣和電子設備

- 車身和底盤

- 車輪和輪胎

- 其他類型

- 透過推進力

- 內燃機

- 電池式電動車

- 油電混合車

- 插電式混合動力電動車

- 燃料電池電動車

- 按車輛類型

- 搭乘用車

- 商用車輛

- 按銷售管道

- OEM

- 售後市場

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 亞太其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 埃及

- 土耳其

- 南非

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- ZF Friedrichshafen AG

- Magna International Inc.

- Valeo SA

- Hyundai Mobis Co. Ltd

- Faurecia SE

- Lear Corporation

- Aisin Corporation

- Aptiv Plc

- BorgWarner Inc.

- Schaeffler AG

- Cummins Inc.

- CATL

- Tenneco Inc.

- Brembo SpA

- Mando Corporation

- ACDelco(GM Genuine Parts)

- Nidec Corporation

第7章 市場機會與未來展望

The automotive parts market was valued at USD 111.53 billion in 2025 and estimated to grow from USD 116.67 billion in 2026 to reach USD 146.23 billion by 2031, at a CAGR of 4.61% during the forecast period (2026-2031).

Higher vehicle production volumes, steady aftermarket demand from an aging global fleet, and accelerating electrification together sustain this moderate growth path. Electrified powertrains shift revenue pools toward high-value electrical and electronic content, even as they reduce demand for some internal-combustion components. Digital commerce is redrawing global distribution routes for spare parts, bringing thousands of smaller suppliers into the formal supply chain. Asia-Pacific holds structural cost advantages, extensive manufacturing scale, and deep local demand, allowing the region to capture disproportionate gains in new-model sourcing. Meanwhile, semiconductor constraints, volatile raw-material input costs, and stricter data-access rules remain primary headwinds that can distort quarterly output and profitability.

Global Automotive Parts Market Trends and Insights

Rise in Global Vehicle Production

Global automotive production reached 90.5 million units in 2023, returning to pre-COVID levels, though production is expected to moderate to 88.5 million units in 2024 before recovering. This production expansion directly correlates with increased demand for both original equipment and aftermarket parts, particularly in emerging markets where vehicle ownership rates continue to climb. China's transformation into a net vehicle exporter, primarily of low-cost internal combustion engine and electric vehicles, reshapes global supply chains and creates new demand patterns for component suppliers. The shift toward "multi-energy" production lines allows manufacturers to adapt quickly to market uncertainties while maintaining consistent parts demand across different powertrain technologies.

Software-Defined Vehicles Requiring Upgradeable Hardware

The automotive software market is projected to demonstrate strong growth over the next few years, with industry executives believing vehicles will be software-defined and AI-powered by 2035. This transformation requires fundamentally different hardware architectures supporting over-the-air updates and continuous feature enhancements. Unlike traditional automotive components with fixed functionality, software-defined vehicles demand modular, upgradeable hardware platforms to accommodate evolving software requirements throughout the vehicle's lifecycle. This shift drives demand for high-performance computing units, advanced sensors, and flexible electronic control units that can be reprogrammed remotely, creating new revenue opportunities for suppliers capable of delivering these sophisticated components.

Persistent Semiconductor Shortages

The automotive semiconductor market faces continued supply constraints despite recovery efforts, with the industry experiencing production reductions of up to 40% during peak shortage periods. The automotive sector's transition to software-defined vehicles is increasing semiconductor content per vehicle from USD 800 in 2023 to an expected USD 1,350 by 2030. Supply chain vulnerabilities persist due to concentrated production in specific geographic regions and the long lead times required for automotive-grade components. The shortage particularly impacts advanced driver assistance systems and infotainment components, forcing OEMs to prioritize chip allocation and sometimes remove features from vehicles to maintain production schedules.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Growth of E-commerce Parts Platforms

- "Right-to-Repair" Legislation Widening Independent Service Share

- EV Shift Eroding Demand for ICE-Specific Parts

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electrical and electronics components command the largest market share at 29.56% in 2025 while achieving the fastest growth rate of 9.12% CAGR through 2031. This dual leadership reflects the automotive industry's fundamental shift to ward connected, autonomous, and electrified vehicles that require sophisticated electronic systems. Modern vehicles average 80 sensors and 100 electronic units, with electronic components expected to comprise 50% of a new car's cost by 2030. The segment encompasses critical systems including advanced driver assistance systems (ADAS), infotainment platforms, battery management systems, and vehicle-to-everything communication modules.

Driveline and powertrain components face a complex transition as traditional internal combustion engine parts experience declining demand while electric powertrain components surge. Interior and exterior segments benefit from premiumization trends and increased focus on user experience, particularly in software-defined vehicles where cabin technology becomes a key differentiator. Body and chassis components are evolving to accommodate new materials and lightweighting requirements. At the same time, wheel and tire segments remain relatively stable, with growth driven by replacement demand from aging vehicle fleets and expanding global vehicle populations.

Internal combustion engine vehicles maintain the largest market share at 75.88% in 2025, reflecting the installed base of existing vehicles and continued production in many global markets. However, battery-electric vehicles represent the fastest-growing segment with an extraordinary 34.1% CAGR, driven by regulatory mandates, improving battery technology, and expanding charging infrastructure. Global electric car production reached 17.3 million units in 2024, with China producing 12.4 million vehicles and dominating over 70% of global output.

Hybrid and plug-in hybrid electric vehicles serve as transitional technologies, requiring components for electric and combustion powertrains, creating complexity for suppliers and diversifying demand patterns. Fuel-cell electric vehicles remain a niche segment but show promise in commercial vehicle applications where hydrogen's energy density advantages become more pronounced. The propulsion mix varies significantly by region, with China and Europe leading electrification. At the same time, North America and emerging markets maintain higher ICE shares, requiring suppliers to maintain flexible production capabilities across multiple powertrain technologies.

The Automotive Parts Market Report is Segmented by Type (Driveline and Powertrain, Electrical and Electronics, and More), Propulsion (Internal Combustion Engine, Battery-Electric Vehicle, and More), Vehicle Type (Passenger Car and Commercial Vehicle), Sales Channel (OEM and Aftermarket), and Geography (North America, South America, Europe, Asia-Pacific and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific maintains its dominant position with 45.31% market share in 2025 and leads regional growth at 6.19% CAGR through 2031, driven by China's automotive manufacturing supremacy and expanding domestic markets. China produced 12.4 million electric vehicles in 2024, representing over 70% of global electric car output, while transforming into a net vehicle exporter. This dual role as producer and exporter creates substantial demand for automotive parts both domestically and for export vehicles. India's automotive aftermarket is projected to reach USD 14 billion by 2028, supported by increasing vehicle ownership and growing demand for aftermarket services. Japan continues to leverage its technological expertise in advanced components, particularly in hybrid powertrains and precision manufacturing. At the same time, South Korea focuses on electric vehicle technologies and semiconductor solutions for automotive applications.

North America and Europe represent mature markets with established automotive ecosystems but face distinct challenges in adapting to industry transformation. Europe's automotive aftermarket, valued at EUR 64 billion, confronts pressure from economic volatility, regulatory changes, and the transition to electric vehicles that require fewer traditional maintenance services. The region's independent aftermarket holds a 60% market share, driven by aging vehicles and budget-conscious consumers, but growth is expected to slow post-2026 due to EV adoption. North America benefits from nearshoring trends and the Inflation Reduction Act's support for domestic EV production, though the market faces potential disruption from trade policies and Chinese automotive competition.

Emerging markets in South America, the Middle East, and Africa demonstrate significant growth potential despite smaller current market shares. Mexico's auto parts sector attracted over USD 2.5 billion in foreign direct investment in 2024, representing a 23.5% increase driven by electric vehicle production growth in the U.S. and rising demand for electric components. The Middle East and North Africa region saw 11 new automotive projects with investments exceeding USD 2.9 billion in Q1 2024, led by Saudi Arabia's USD 1.3 billion electric vehicle manufacturing complex. These regions benefit from government initiatives to develop local automotive capabilities and reduce dependence on imports, creating opportunities for domestic and international parts suppliers.

- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- ZF Friedrichshafen AG

- Magna International Inc.

- Valeo SA

- Hyundai Mobis Co. Ltd

- Faurecia SE

- Lear Corporation

- Aisin Corporation

- Aptiv Plc

- BorgWarner Inc.

- Schaeffler AG

- Cummins Inc.

- CATL

- Tenneco Inc.

- Brembo SpA

- Mando Corporation

- ACDelco (GM Genuine Parts)

- Nidec Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise in global vehicle production

- 4.2.2 Software-defined vehicles requiring upgradeable hardware

- 4.2.3 Aging vehicle fleet boosting aftermarket spend

- 4.2.4 Rapid growth of e-commerce parts platforms

- 4.2.5 Right-to-repair" legislation widening independent service share"

- 4.2.6 Light-weighting push for advanced material components

- 4.3 Market Restraints

- 4.3.1 Persistent semiconductor shortages

- 4.3.2 EV shift eroding demand for ICE-specific parts

- 4.3.3 Volatile raw material prices disrupting cost structures

- 4.3.4 Labor shortages in key manufacturing hubs

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Key Supplier Information By Type

5 Market Size and Growth Forecasts (Value (USD))

- 5.1 By Type

- 5.1.1 Driveline and Powertrain

- 5.1.2 Interior and Exterior

- 5.1.3 Electrical and Electronics

- 5.1.4 Body and Chassis

- 5.1.5 Wheel and Tires

- 5.1.6 Other Types

- 5.2 By Propulsion

- 5.2.1 Internal Combustion Engine

- 5.2.2 Battery-Electric Vehicle

- 5.2.3 Hybrid Electric Vehicle

- 5.2.4 Plug-in Hybrid Electric Vehicle

- 5.2.5 Fuel-Cell Electric Vehicle

- 5.3 By Vehicle Type

- 5.3.1 Passenger Car

- 5.3.2 Commercial Vehicle

- 5.4 By Sales Channel

- 5.4.1 Original Equipment Manufacturer (OEM)

- 5.4.2 Aftermarket

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of APAC

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Egypt

- 5.5.5.4 Turkey

- 5.5.5.5 South Africa

- 5.5.5.6 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Robert Bosch GmbH

- 6.4.2 Continental AG

- 6.4.3 Denso Corporation

- 6.4.4 ZF Friedrichshafen AG

- 6.4.5 Magna International Inc.

- 6.4.6 Valeo SA

- 6.4.7 Hyundai Mobis Co. Ltd

- 6.4.8 Faurecia SE

- 6.4.9 Lear Corporation

- 6.4.10 Aisin Corporation

- 6.4.11 Aptiv Plc

- 6.4.12 BorgWarner Inc.

- 6.4.13 Schaeffler AG

- 6.4.14 Cummins Inc.

- 6.4.15 CATL

- 6.4.16 Tenneco Inc.

- 6.4.17 Brembo SpA

- 6.4.18 Mando Corporation

- 6.4.19 ACDelco (GM Genuine Parts)

- 6.4.20 Nidec Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

2026-2030年全球汽車零件市場

2026-2030年全球汽車零件市場 引擎罩鎖板和鎖扣市場預測至2034年-全球汽車引擎罩、材料、技術、銷售管道、應用與區域分析汽車零件市場預測至2034年-按產品類型、車輛類型、通路和地區分類的全球分析

引擎罩鎖板和鎖扣市場預測至2034年-全球汽車引擎罩、材料、技術、銷售管道、應用與區域分析汽車零件市場預測至2034年-按產品類型、車輛類型、通路和地區分類的全球分析 汽車零件市場:2026-2032年全球市場預測(依產品類型、材料、車輛類型、銷售形式及銷售管道)

汽車零件市場:2026-2032年全球市場預測(依產品類型、材料、車輛類型、銷售形式及銷售管道) 2026年全球拖車穩定設備市場報告2026年全球汽車零件市場報告2026年全球汽車零件循環包裝市場報告汽車零件製造市場:2026-2032年全球市場預測(按產品類型、燃料類型、車輛類型、應用和分銷管道分類)汽車零件及配件市場:依產品類型、車輛類型、替換類型、通路分類,全球預測(2026-2032年)汽車座椅核心零件市場:依產品類型、車輛類型、動力系統、座椅類型、材質和銷售管道,全球預測,2026-2032年

2026年全球拖車穩定設備市場報告2026年全球汽車零件市場報告2026年全球汽車零件循環包裝市場報告汽車零件製造市場:2026-2032年全球市場預測(按產品類型、燃料類型、車輛類型、應用和分銷管道分類)汽車零件及配件市場:依產品類型、車輛類型、替換類型、通路分類,全球預測(2026-2032年)汽車座椅核心零件市場:依產品類型、車輛類型、動力系統、座椅類型、材質和銷售管道,全球預測,2026-2032年