|

市場調查報告書

商品編碼

1934880

數位線程:市佔率分析、產業趨勢與統計、成長預測(2026-2031)Digital Thread - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

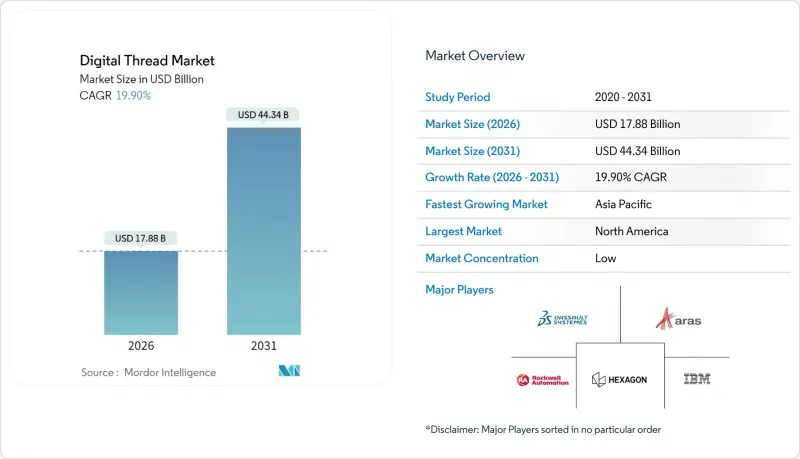

預計到 2026 年,數位線程市場價值將達到 178.8 億美元,高於 2025 年的 149.1 億美元。

預計到 2031 年將達到 443.4 億美元,2026 年至 2031 年的複合年成長率為 19.9%。

隨著製造商透過貫穿設計、生產和服務的單一、持久的數據流,將設計意圖與即時營運相結合,市場需求日益成長。雲端原生產品生命週期管理平台創造了一個全天候運作環境,同時降低了IT成本。低成本的工業物聯網感測器將詳細的現場資料傳輸到模擬模型中,使工程師能夠更好地連接虛擬資產和實體資產。生成式人工智慧透過自動標註CAD模型進一步縮短了設計週期,而永續性法規則推動了對生命週期碳排放追蹤的需求。網路攻擊風險是推動建構安全架構以保護互聯生產線的另一個重要因素。

全球數位線程市場趨勢與洞察

雲端原生PLM採用率激增

雲端平台透過 API 優先的環境消除了本地資料孤島,整合了設計、執行和服務資料。 Aras 展示了區域託管如何為全球團隊提供安全的共用工作空間,同時滿足資料主權法規的要求。 PTC 的雲端部署將醫療設備的上市時間縮短了 40%,帶來了實際的經濟效益。降低的升級成本使得預算可以分配給模擬和分析模組,從而擴展數位線程的價值。然而,歐洲企業面臨嚴格的 GDPR 要求,對供應商鎖定的擔憂正在推遲最終的採購決策。

工業物聯網感測器成本下降

感測器的平均價格已降至0.38美元,大規模生產正迅速接近0.30美元的關鍵價位,屆時工廠即可為其所有資產配備智慧感測器。亞太地區44%的工廠計劃在未來12個月內採用智慧製造,比美國計畫高出10個百分點。低成本的感測器和邊緣閘道器可將即時指標傳輸到數位雙胞胎模型中,從而縮短品質干預的反應時間並降低廢品率。隨著硬體成本的下降,軟體訂閱和網路安全工具在計劃總預算中所佔的比例越來越大。

中小企業在基於模型的工程領域面臨技能短缺問題

到2030年,製造業將有200萬個職缺,而目前三分之一的勞動力缺乏數位化技能。中小企業無法與大型企業相比提高薪資水平,並且在採用先進的產品生命週期管理(PLM)模組方面進展緩慢。社區大學正在增設基於模型的系統工程(MBSE)課程,但畢業生需要四年才能找到相關工作。人工智慧驅動的設計助理可以簡化技術應用,但文化變革仍然是企業主經營工廠面臨的一大障礙。

細分市場分析

到2025年,PLM將佔據數位線程市場27.80%的佔有率,並繼續成為企業數位化策略的支柱。隨著企業將設計和執行數據連接起來,以PLM為中心的技術堆疊中的數位線程市場規模預計將穩定成長。然而,ALM 21.7%的複合年成長率表明,市場正向軟體定義產品轉變,這需要程式碼和硬體之間的緊密同步。據Triebwerk稱,生成式人工智慧透過將文字提示轉換為參數化模型,減少了70%的初始設計工作,從而推動了這一趨勢。 CAD和CAM領域正呈現緩慢但穩定的成長,因為人工智慧外掛能夠及早發現設計錯誤,而SLM在航太和醫療領域正獲得發展動力,這些領域售後服務合規性要求嚴格。 ERP和MRP套件現在正在開放API,將營運交易與工程變更單連接起來,從而促進數位線程市場向傳統PLM以外的領域擴展。其他模擬和分析工具也加入了這波整合浪潮,為工程師提供了一個統一的介面,可以查看從有限元素模型到現場感測器回饋的所有資訊。

企業越來越傾向於選擇整合多個模組的平台供應商,而不是購買單一解決方案。西門子、PTC 和達梭系統在嵌入式模擬引擎和更靠近受監管用戶的雲端區域方面擁有優勢,但它們正面臨部署純雲端架構並付費使用制的新競爭對手。隨著客戶抵制專有技術鎖定,開放標準資料格式預計將在藍圖中佔據更有利的地位。競爭趨勢表明,PLM(產品生命週期管理)收入趨於穩定,而能夠自動化執行勞動密集型任務的人工智慧增強模組的擴展正在加速,這正在逐步改變數位線程市場的支出模式。

經過多年的SaaS普及,隨著眾多中小企業開始在完全託管的環境中部署數位線程,雲端技術將在2025年佔據53.85%的市場佔有率。大型企業則尋求折衷方案,將敏感的智慧財產權保留在內部,推動了20.6%的複合年成長率。預計到2031年,混合部署相關的數位線程市場規模將成長近三倍,因為企業需要兼顧傳統設備、延遲要求和出口管制法規。國防相關企業正在利用FedRAMP高支援位置進行協作,同時在防火牆後鏡像核心儲存庫以符合ITAR法規。在歐洲,由於GDPR中嚴格的居住要求,雙棧部署正成為營運標準。

隨著製造商從簡單的文件複製轉向微服務編配,混合部署模式日益成熟。雲層負責處理模擬突發任務和人工智慧推理,而生產歷史系統則駐留在本地資料中心,以實現毫秒級的回饋。供應商提供在兩種環境中運行完全相同的容器化服務,從而簡化了更新周期。對於核能、製藥和關鍵基礎設施營運商而言,本地部署仍然至關重要,因為軟體變更認證是這些行業的必備條件。儘管本地部署的成長速度有所放緩,但它仍然影響著產品功能藍圖,並確保空氣間隙功能仍然是主流產品的一部分。

區域分析

北美目前的優勢源於其成熟的航太主承包商、國防預算以及與矽谷的軟體夥伴關係。數位化工程的迫切需求正在推動對端到端資料連續性計劃的投資,而雲端超大規模資料中心業者營運符合FedRAMP標準、滿足嚴格安全要求的區域。類似的實踐正透過與美國飛機製造商的通用供應鏈在加拿大向北擴展,而墨西哥新興的航太園區也在採用數位線程來贏得新契約。勞動力短缺是一個真正的限制因素,而人工智慧增強的設計工具正在緩解生產力下降的問題。

亞太地區的發展速度遠超過其他地區。中國政府正在資助一條融合工業物聯網、人工智慧和先進機器人技術的試點生產線,為本土原始設備製造商(OEM)帶來成本和速度優勢。日本電子製造商也正在運用類似的理念來維持其全球品質領先地位。韓國造船廠正在利用數位雙胞胎技術預測船體應力並制定維護計畫。印度正在將低成本感測器與雲端資料中心結合,使中小企業能夠跨越傳統的製造執行系統(MES)架構。在東協內部,電子和醫療設備出口商正在採用數位線程平台,以透過西方客戶的供應商審核。

在歐洲,數位線程正被用來滿足碳排放報告義務。德國機械製造商正將能耗指標納入所有資產記錄。法國航太供應商正在將複合材料資料和零件護照互聯互通,以實現合規性。義大利汽車零件產業叢集正專注於可追溯性,以維持其一級供應商的地位。 《一般資料保護規則》(GDPR) 正在推動多實例雲端架構的發展,並增加對混合部署的需求。同時,歐盟的碳邊境調節措施即將對缺乏檢驗的生命週期資料的進口產品處以附加稅,迫使全球合作夥伴遷移到相容的平台。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 雲端原生PLM採用率激增

- 工業物聯網感測器成本低於 0.30 美元

- 促進航太領域遵守脫碳法規

- 快速循環積層製造迴路

- 國防數位線程指令(美國國防部模型驅動系統工程)

- 基於生成式人工智慧的自動模型標註引擎

- 市場限制

- 中小企業缺乏以模型為基礎的工程人才

- 主權雲端和資料居住障礙

- 對PLM/SaaS供應商鎖定問題的擔憂

- 網路攻擊保險費飆升

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 對宏觀經濟趨勢的市場評估

第5章 市場規模與成長預測

- 透過技術

- 產品生命週期管理 (PLM)

- 電腦輔助設計 (CAD)

- 電腦輔助製造 (CAM)

- 服務生命週期管理 (SLM)

- ALM(應用程式生命週期管理)

- 物料需求計劃 (MRP)

- ERP(企業資源計畫)

- 其他技術

- 透過部署模式

- 雲

- 本地部署

- 混合

- 按公司規模

- 主要企業

- 中小企業

- 按行業

- 航太與國防

- 汽車與運輸

- 工業機械

- 能源與公共產業

- 醫療和醫療設備

- 電子和半導體

- 其他行業部門

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- ASEAN

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Dassault Systemes SE

- Aras Corporation

- Rockwell Automation, Inc.

- Hexagon AB

- International Business Machines Corporation

- Autodesk, Inc.

- Ansys, Inc.

- Siemens AG

- PTC Inc.

- Oracle Corporation

- SAP SE

- General Electric Company

- Honeywell International Inc.

- Microsoft Corporation

- Accenture plc

- Capgemini SE

- DXC Technology Company

- Tata Consultancy Services Limited

- ABB Ltd.

- Altair Engineering Inc.

第7章 市場機會與未來展望

digital thread market size in 2026 is estimated at USD 17.88 billion, growing from 2025 value of USD 14.91 billion with 2031 projections showing USD 44.34 billion, growing at 19.9% CAGR over 2026-2031.

Demand rises as manufacturers link engineering intent with real-time operations through a single, persistent data flow that spans design, production, and service. Cloud-native product lifecycle management platforms cut IT overhead while creating always-on collaboration environments. Cheaper IIoT sensors feed granular shop-floor data into simulation models, letting engineers close the loop between virtual and physical assets. Generative AI further trims design cycles by auto-annotating computer-aided models, and sustainability regulations intensify the need for lifecycle carbon tracking. Cyber-attack risks add a parallel push toward secure architectures that guard connected production lines.

Global Digital Thread Market Trends and Insights

Cloud-Native PLM Adoption Surge

Cloud platforms replace on-premises silos with API-first environments that unite design, execution, and service data. Aras shows how regional hosting satisfies data-sovereignty rules while giving global teams a secure shared workspace. PTC's cloud deployment cuts medical-device time to market by 40%, proving tangible financial benefit. Lower upgrade costs free budgets for simulation and analytics modules that extend digital thread value. Yet European firms face tougher GDPR hurdles, and the fear of vendor lock-in slows final purchase decisions.

IIoT Sensor Cost Decline

Average sensor pricing has dropped to USD 0.38, with volume production racing toward the pivotal USD 0.30 mark that lets factories instrument every asset. Forty-four percent of Asia-Pacific plants plan smart-manufacturing rollouts within 12 months, eclipsing U.S. intent by 10 percentage points. Cheap sensors plus edge gateways feed real-time metrics into digital twins, cutting response times for quality interventions and shrinking scrap rates. As hardware costs fall, software subscriptions and cybersecurity tools become the larger share of total project budgets.

SME Talent Gap in Model-Based Engineering

Two million manufacturing positions may stay vacant by 2030, and one-third of today's workforce lacks digital skills. Small firms cannot match enterprise salaries, so they lag in adopting advanced PLM modules. Community colleges add MBSE courses, but four years must pass before graduates fill shop floors. AI-guided design assistants ease onboarding, yet culture change remains a stumbling block for many owner-managed plants.

Other drivers and restraints analyzed in the detailed report include:

- Aerospace Decarbonization Compliance Push

- Rapid-Cycle Additive Manufacturing Loops

- Sovereign-Cloud and Data-Residency Barriers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

PLM commanded 27.80% of the digital thread market in 2025 and remains the backbone of enterprise digital strategies. The digital thread market size for PLM-centric stacks is projected to climb steadily as companies connect design vaults with execution data. However, ALM's 21.7% CAGR signals a pivot toward software-defined products that demand tighter code-hardware synchronization. Generative AI adds fuel by turning text prompts into parametric models, slashing initial design work by 70% according to Triebwerk. CAD and CAM segments show modest but consistent growth as AI plug-ins surface design errors early, while SLM picks up momentum in aerospace and healthcare, where after-sales compliance is strict. ERP and MRP suites now publish open APIs that join operational transactions with engineering change orders, expanding the addressable digital thread market beyond traditional PLM boundaries. Other simulation and analytics tools ride this integration wave, giving engineers a single pane of glass that stretches from finite-element models to field sensor feedback.

Enterprises increasingly choose platform vendors that fuse multiple modules rather than buying point solutions. Siemens, PTC, and Dassault lean on embedded simulation engines and cloud regions near regulated users, yet face new rivals who launch cloud-only stacks with consumption billing. Open-standard data formats appear on more roadmaps as customers push back against proprietary lock-ins. The competitive narrative suggests steady PLM revenue but faster expansion for AI-augmented modules that automate labor-intensive tasks, indicating a gradual redistribution of spending within the digital thread market.

Cloud held a 53.85% share in 2025 after years of software-as-a-service evangelism, and many SMEs began their digital thread journey in fully hosted environments. Large primes keep sensitive IP on site, driving hybrid's 20.6% CAGR as the preferred compromise. The digital thread market size associated with hybrid rollouts will nearly triple by 2031 as firms juggle legacy gear, latency demands, and export-control rules. Defense contractors rely on FedRAMP high-assurance regions for collaboration, yet mirror core repositories behind firewalls to meet U.S. International Traffic in Arms Regulations. In Europe, GDPR's strict residency clauses make dual-stack deployments an operational norm.

Hybrid adoption patterns mature as manufacturers shift from simple file replication to microservice orchestration. Cloud tiers now handle simulation bursts and AI inference, while production historians reside in local data centers for millisecond feedback. Vendors have responded with containerized services that run identically in both locations, simplifying update cycles. On-premises deployments remain relevant for nuclear, pharmaceutical, and critical-infrastructure operators who must certify every software change. Although their growth lags, they continue to influence feature roadmaps, ensuring that air-gapped functionality remains part of mainstream offerings.

The Digital Thread Market Report is Segmented by Technology (PLM, CAD, CAM, SLM, ALM, and More), Deployment Mode (Cloud, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium-Sized Enterprises), Industry Vertical (Aerospace and Defense, Automotive and Transportation, Industrial Machinery, Healthcare and Medical Devices, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America's current dominance stems from entrenched aerospace primes, defense budgets, and Silicon Valley software partnerships. Digital engineering mandates funnel investment into end-to-end data continuity projects, and cloud hyperscalers operate FedRAMP regions that satisfy strict security needs. Canada's shared supply chain with U.S. airframe builders spreads similar practices northward, while Mexico's rising aerospace parks embrace digital threads to win new contracts. Labor shortages pose a real constraint, yet AI-augmented design tools moderate the productivity hit.

Asia-Pacific advances faster than any other bloc. China's government funds pilot lines that integrate IIoT, AI, and advanced robotics, giving local OEMs cost and speed advantages. Japanese electronics makers apply the same principles to keep global quality leadership. South Korea's shipyards use digital twins to predict hull stress and schedule maintenance. India combines low sensor costs with cloud datacenters to let SMEs leapfrog older MES architectures. Across ASEAN, electronics and medical-device exporters adopt digital thread platforms to pass supplier audits from Western customers.

Europe relies on digital threads to meet carbon-reporting duties. German machine builders embed energy-consumption metrics in every asset record. French aerospace suppliers interlink composite material data with component passports for regulatory compliance. Italy's automotive parts clusters focus on traceability to maintain Tier-1 status. GDPR forces multi-instance cloud designs, boosting demand for hybrid deployments. In parallel, EU carbon border adjustments will soon penalize imports lacking verified lifecycle data, nudging global partners onto compatible platforms.

- Dassault Systemes SE

- Aras Corporation

- Rockwell Automation, Inc.

- Hexagon AB

- International Business Machines Corporation

- Autodesk, Inc.

- Ansys, Inc.

- Siemens AG

- PTC Inc.

- Oracle Corporation

- SAP SE

- General Electric Company

- Honeywell International Inc.

- Microsoft Corporation

- Accenture plc

- Capgemini SE

- DXC Technology Company

- Tata Consultancy Services Limited

- ABB Ltd.

- Altair Engineering Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-Native PLM Adoption Surge

- 4.2.2 IIoT Sensor Cost Declines Below USD 0.30

- 4.2.3 Aerospace Decarbonization Compliance Push

- 4.2.4 Rapid-Cycle Additive Manufacturing Loops

- 4.2.5 Defense Digital Thread Mandates (U.S. DoD MBSE)

- 4.2.6 Gen-AI Automated Model Annotation Engines

- 4.3 Market Restraints

- 4.3.1 SME Talent Gap in Model-Based Engineering

- 4.3.2 Sovereign-Cloud and Data-Residency Barriers

- 4.3.3 PLM/SaaS Vendor Lock-In Concerns

- 4.3.4 Cyber-Attack Insurance Premium Spikes

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Assessment of Macro-economic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 PLM (Product Lifecycle Management)

- 5.1.2 CAD (Computer-Aided Design)

- 5.1.3 CAM (Computer-Aided Manufacturing)

- 5.1.4 SLM (Service Lifecycle Management)

- 5.1.5 ALM (Application Lifecycle Management)

- 5.1.6 MRP (Material Requirements Planning)

- 5.1.7 ERP (Enterprise Resource Planning)

- 5.1.8 Other Technologies

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises (SMEs)

- 5.4 By Industry Vertical

- 5.4.1 Aerospace and Defense

- 5.4.2 Automotive and Transportation

- 5.4.3 Industrial Machinery

- 5.4.4 Energy and Utilities

- 5.4.5 Healthcare and Medical Devices

- 5.4.6 Electronics and Semiconductors

- 5.4.7 Other Industry Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 ASEAN

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Dassault Systemes SE

- 6.4.2 Aras Corporation

- 6.4.3 Rockwell Automation, Inc.

- 6.4.4 Hexagon AB

- 6.4.5 International Business Machines Corporation

- 6.4.6 Autodesk, Inc.

- 6.4.7 Ansys, Inc.

- 6.4.8 Siemens AG

- 6.4.9 PTC Inc.

- 6.4.10 Oracle Corporation

- 6.4.11 SAP SE

- 6.4.12 General Electric Company

- 6.4.13 Honeywell International Inc.

- 6.4.14 Microsoft Corporation

- 6.4.15 Accenture plc

- 6.4.16 Capgemini SE

- 6.4.17 DXC Technology Company

- 6.4.18 Tata Consultancy Services Limited

- 6.4.19 ABB Ltd.

- 6.4.20 Altair Engineering Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

2026-2030年全球數位線程市場

2026-2030年全球數位線程市場 2026-2030年全球製造業數位產品護照平台市場

2026-2030年全球製造業數位產品護照平台市場 2026年全球數位線程市場報告

2026年全球數位線程市場報告 數位線程市場:按解決方案和區域分類

數位線程市場:按解決方案和區域分類 數位線程市場:按產品類型、業務功能、應用、部署模式和最終用戶產業分類-2026-2032年全球預測

數位線程市場:按產品類型、業務功能、應用、部署模式和最終用戶產業分類-2026-2032年全球預測 數位線程市場分析及預測(至2035年):按類型、產品類型、技術、元件、應用、流程、部署類型、最終用戶、功能和解決方案分類

數位線程市場分析及預測(至2035年):按類型、產品類型、技術、元件、應用、流程、部署類型、最終用戶、功能和解決方案分類 數位線程市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2026-2034)

數位線程市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2026-2034) 數位線程-全球市場佔有率和排名、總收入和需求預測(2025-2031 年)

數位線程-全球市場佔有率和排名、總收入和需求預測(2025-2031 年) 全球數位線程市場:未來預測(至2032年)-按模組、部署模式、技術、應用、最終用戶和地區進行分析

全球數位線程市場:未來預測(至2032年)-按模組、部署模式、技術、應用、最終用戶和地區進行分析 全球數位線程市場:依技術、部署類型、模組類型、應用、最終用戶、地區、機會及預測,2018-2032

全球數位線程市場:依技術、部署類型、模組類型、應用、最終用戶、地區、機會及預測,2018-2032