|

市場調查報告書

商品編碼

1934872

數控工具機:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)CNC Machines - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

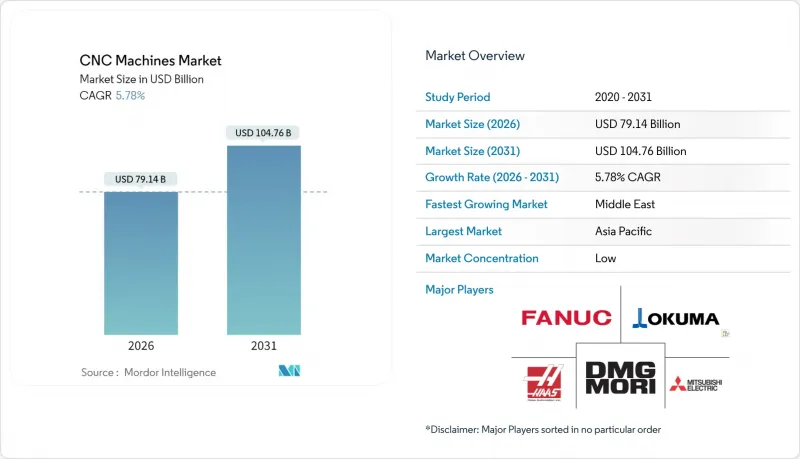

預計到 2026 年,CNC工具機市場價值將達到 791.4 億美元,高於 2025 年的 748.2 億美元,預計到 2031 年將達到 1,047.6 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 5.78%。

對數位化生產日益成長的需求、電動車和航太專案對公差要求的提高,以及工廠現代化改造的財政激勵措施,共同推動了這一擴張。供應商正不斷整合硬體、軟體和預測服務,使客戶能夠在擴大產能的同時提高資產利用率並推遲新設備的採購。籌資策略目前優先考慮與工業5G和邊緣運算平台的互通性,這可以將廢品率降低高達30%,並將備件前置作業時間縮短10%。地緣政治供應鏈問題也促使原始設備製造商(OEM)將關鍵加工業務遷回國內,增強了對北美和歐盟本土設備的需求。

全球CNC工具機市場趨勢與洞察

工業4.0主導的自動化升級

製造商正從孤立的工具機轉向完全連網的單元式加工中心。物聯網感測器將即時運作狀態傳輸到邊緣伺服器,從而減少30%的廢品率和10%的備件庫存。第五代無線技術消除了傳統的延遲問題,為操作人員提供可靠的連接,防止程式中斷。數位雙胞胎技術能夠在切削開始前模擬熱漂移和主軸動態特性,從而將推出40%。人工智慧輔助的刀具路徑代理將程式設計工作量減少50%,同時提高了表面光潔度的重複性。這些升級正在將CNC工具機從獨立設備轉變為自主生產循環中的節點。

汽車和航太產業對高精度產品的需求日益成長

電動汽車電池外殼、逆變器極板和電機定子如今對精度的要求已達到以往航太結構的水平,這推動了汽車工廠對五軸加工技術的應用。航太航太的加工週期縮短35%,同時維持尺寸精度。監管追溯要求進一步要求建立數位化加工日誌,以證明微米級精度。這兩個行業日益成長的需求正使高精度數控加工能力成為一項基本要求,而非高級選項。

高昂的資本成本和生命週期成本

五軸加工中心整合了高精度旋轉軸、線性馬達和熱補償系統,使其購置成本超過50萬美元,對小規模工廠來說構成了一道障礙。 Okuma估計,生命週期成本中只有15%是在購買時產生的,而85%則與維護、能源和非計畫性停機有關。數位雙胞胎授權和人工智慧模組也會增加企業資源規劃的成本。研究表明,混合積層和減材加工單元在實現合理的投資回收期之前,需要進行全面的批量分析,尤其是在粉末成本較高的情況下。因此,高昂的擁有成本限制了它們在小批量製造商中的應用。

細分市場分析

到2025年,CNC車床將佔總收入的26.95%,這印證了其在多個價值鏈中製造旋轉零件(例如軸和襯套)的關鍵作用。簡單的編程和剛性刀具使其能夠快速換刀,從而成為一級汽車和油壓設備供應商的主力設備。銑床位居第二,因為它們用於加工需要多方面精度的矩形形狀。同時,雷射切割機是成長最快的細分市場,年複合成長率達8.55%,這主要得益於光纖雷射光源能夠以最小的變形切割鋼、鋁和複合材料層壓板。

Prima Power 的 Laser Next 2130 雷射切割機與西門子的 SINUMERIK ONE控制設備結合,使汽車車體線的動態響應速度提升了 20%,生產效率提高了 13%。這表明雷射加工正在取代沖壓工藝,成為複雜面板加工的主流選擇。電火花加工和研磨在模具和軸承製造商中仍然佔據著重要的地位。積層製造和減材製造相結合的混合型工具機能夠實現鎳基高溫合金的近淨成形沉積,並在同一工作台上完成精加工,從而顯著簡化了一家領先的航太製造商的物流流程。這使得CNC工具機市場能夠在車床需求趨於穩定的同時,實現雷射技術的快速創新。

區域分析

到2025年,亞太地區將佔全球收入的46.10%,這主要得益於中國、日本和印度擴大國內產能以降低進口風險並滿足國內需求。中國第一瑞沃自動化公司融資1億元人民幣(約1,390萬美元)用於研發國產高階控制設備,反映了中國政府推動策略性工具機技術國產化的決心。日本則透過持續升級控制設備來鞏固其高階市場地位。大隈研吾的OSP-P500將自適應加工與網路安全雲端連接結合,展現了傳統技術向資料驅動型服務的轉型。

北美維持了第二的位置,這得益於回流補貼、航太整合以及國防需求。橡樹嶺國家實驗室和MSC工業供應公司合作開發了攻絲測試軟體,旨在透過公私合營提高允許切削速度並提升生產效率。加拿大充分利用了安大略省的汽車產業叢集,而墨西哥的巴希奧走廊則吸收了電子產品和白色家電的加工業務,以滿足美國的需求。

歐洲憑藉德國、義大利和斯堪的納維亞等國的專業企業向全球出口高精度加工單元,保持技術優勢。然而,隨著產油國實現多元化發展,預計到2031年,中東地區的複合年成長率將達到8.85%,成為該地區成長最快的地區。艾默生在薩勒曼國王能源園區新建的13,000平方公尺工廠以及先進精密工業服務公司在達曼擴建的54,000平方公尺工廠,將為該地區的能源、航太和石化產業提供重型機械加工服務。這些投資將降低進口依賴性,並為當地的零件維修創造下游機會。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 工業4.0主導的自動化升級

- 汽車和航太領域對高精度產品的需求日益成長

- 政府對工廠現代化改造的激勵措施

- 五軸加工技術在電動車和植入的快速應用

- 混合積層製造及切削數控整合

- 利用數位雙胞胎進行預測編程

- 市場限制

- 高昂的資本成本和生命週期成本

- 熟練的CNC編程人員短缺

- 聯網控制設備的網路安全風險

- 零件供應鏈不穩定(滾珠螺桿、導軌)

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 產業吸引力—五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模及成長預測(價值,單位:十億美元)

- 按模型

- CNC車床

- CNC銑床

- 數控雷射切割機

- 數控等離子切割機

- CNC電火花加工(電火花成型和線切割)

- CNC研磨

- 數控鑽孔/攻牙中心

- 其他專用CNC工具工具機

- 軸類型

- 三軸加工工具機

- 四軸加工工具機

- 五軸加工工具機

- 6 個或更多軸

- 按最終用戶行業分類

- 車

- 航太/國防

- 電子裝置和半導體

- 醫療設備

- 建築和重型設備

- 電力和能源

- 造船

- 一般製造和合約工廠

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 秘魯

- 其他南美洲

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 比荷盧經濟聯盟(比利時、荷蘭、盧森堡)

- 北歐國家(丹麥、芬蘭、冰島、挪威、瑞典)

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東協(印尼、泰國、菲律賓、馬來西亞、越南)

- 亞太其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 科威特

- 土耳其

- 埃及

- 南非

- 奈及利亞

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- FANUC Corporation

- DMG Mori Co. Ltd

- Haas Automation Inc.

- Okuma Corporation

- Mitsubishi Electric Corporation

- Siemens AG

- Yamazaki Mazak Corporation

- Bosch Rexroth AG

- GSK CNC Equipment Co. Ltd

- Hurco Companies Inc.

- Dr. Johannes Heidenhain GmbH

- Trumpf Group

- Doosan Machine Tools

- Hyundai Wia Corp.

- Biesse Group

- Brother Industries Ltd

- FFG Europe & Americas

- Makino Milling Machine Co. Ltd

- Chiron Group SE

- JTEKT Corporation(Toyoda)

第7章 市場機會與未來展望

CNC Machines Market size in 2026 is estimated at USD 79.14 billion, growing from 2025 value of USD 74.82 billion with 2031 projections showing USD 104.76 billion, growing at 5.78% CAGR over 2026-2031.

Rising demand for digitally enabled production, tighter tolerance requirements in electric-vehicle and aerospace programs, and fiscal incentives for factory modernization collectively underpin this expansion. Vendors increasingly bundle hardware, software, and predictive services, allowing customers to raise asset utilization and defer new-equipment purchases while still expanding productive capacity. Procurement strategies now prioritize interoperability with industrial 5G and edge-computing platforms that reduce scrap rates by up to 30% and shorten spare-parts lead times by 10%. Geopolitical supply-chain concerns are also encouraging OEMs to reshore critical machining work, strengthening demand for domestic installations in North America and the European Union.

Global CNC Machines Market Trends and Insights

Industry 4.0-driven Automation Upgrades

Manufacturers are migrating from isolated machine tools to fully networked cells where IoT sensors stream real-time conditions to edge servers, cutting scrap by 30% and trimming spare-parts inventories by 10%. Fifth-generation wireless closes previous latency gaps, giving operators steady connectivity that prevents program interruptions. Digital twins now model thermal drift and spindle dynamics before a single chip is cut, trimming ramp-up times by 40%. AI-assisted toolpath agents lower programming workloads by 50% while improving surface finish repeatability. Collectively, these upgrades reposition CNC equipment as nodes within autonomous production loops rather than stand-alone capital assets.

Rising Precision Demand in Automotive & Aerospace

Electric-vehicle battery housings, inverter plates, and motor stators impose tolerance bands once limited to aerospace structures, prompting wider 5-axis adoption in automotive shops. Aerospace recovery adds a second precision stream, with titanium and carbon-fiber components requiring stable tool engagement beyond conventional parameters. Hybrid additive-subtractive processes can shave 35% off cycle times for intricate aerospace brackets while preserving dimensional integrity. Regulatory traceability rules further compel digital machining logs that prove micron-level accuracy. This dual-sector pull cements high-precision CNC capability as a baseline requirement rather than a premium option.

High Capital & Lifecycle Costs

Five-axis centers integrate high-precision rotary axes, linear motors, and thermal-compensation systems, lifting purchase tickets well above USD 500,000, a hurdle for small shops. Okuma estimates only 15% of lifetime spending happens at acquisition, with 85% tied to maintenance, energy, and unplanned outages. Digital twin licenses and AI modules pile extra costs onto enterprise resource plans. Studies show hybrid additive-subtractive cells demand thorough batch-size analyses before payback is viable, especially when powders carry premium prices. High ownership burden, therefore, limits penetration among low-volume manufacturers.

Other drivers and restraints analyzed in the detailed report include:

- Government Incentives for Factory Modernization

- Rapid Adoption of 5-Axis Machining for EV & Implants

- Skilled CNC Programmer Shortage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

CNC lathes captured 26.95% of 2025 revenue, underscoring their indispensable role in shafts, bushings, and other rotational parts across multiple value chains. Their straightforward programming and rigid tooling allow quick changeovers, making them staples for Tier 1 automotive and hydraulic suppliers. Milling machines follow, serving prismatic geometries where multi-surface accuracy matters. Laser cutters, however, are climbing fastest at an 8.55% CAGR thanks to fiber-laser sources that pierce steel, aluminum, and composite stacks with minimal distortion.

Prima Power's Laser Next 2130, paired with Siemens' SINUMERIK ONE control, boosted dynamic response by 20% and productivity by 13% in automotive body-in-white lines, illustrating why lasers are displacing stamping on complex panels. Electro-discharge machining and grinding sustain niche dominance in die-makers and bearing producers. Hybrid additive-subtractive units enable near-net deposition of nickel superalloys, then finishing on the same table, saving aerospace primes multiple logistics steps. The CNC machines market thus balances mature turning demand with rapid laser innovation.

The CNC Machines Market Report is Segmented by Machine Type (CNC Lathes, CNC Milling Machines, and More), by Axis Type (3-Axis, 4-Axis, and More), by End-User Industry (Automotive, Aerospace & Defense, Electronics & Semiconductor, and More), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific secured 46.10% of global revenue in 2025 as China, Japan, and India expanded domestic capacity to mitigate import risk and satisfy internal demand. China's First Automation raised RMB 100 million (USD 13.9 million) to develop native high-end controllers, signaling official intent to localize strategic machine-tool technology. Japan protects its premium segment through continual control upgrades; Okuma's OSP-P500 pairs adaptive machining with cyber-secure cloud links, demonstrating how legacy expertise evolves into data-driven services.

North America ranks second, combining reshoring subsidies, aerospace consolidation, and defense imperatives. Oak Ridge National Laboratory and MSC Industrial Supply co-developed tap-testing software that raises permissible material-removal rates, showing public-private collaboration on productivity. Canada leverages automotive clusters in Ontario, whereas Mexico's Bajio corridor absorbs electronics and white-goods machining to serve the United States' demand.

Europe retains technical leadership through German, Italian, and Nordic specialists who export high-tolerance cells worldwide. The Middle East, though, will post the strongest 8.85% CAGR to 2031 as oil-rich nations diversify. Emerson's 13,000 m2 plant at King Salman Energy Park and Advanced Precision Industrial Services' 54,000 m2 expansion in Dammam equip the region with heavy-duty machining for energy, aerospace, and petrochemical needs. These investments reduce import reliance and open downstream opportunities for localized component repair.

- FANUC Corporation

- DMG Mori Co. Ltd

- Haas Automation Inc.

- Okuma Corporation

- Mitsubishi Electric Corporation

- Siemens AG

- Yamazaki Mazak Corporation

- Bosch Rexroth AG

- GSK CNC Equipment Co. Ltd

- Hurco Companies Inc.

- Dr. Johannes Heidenhain GmbH

- Trumpf Group

- Doosan Machine Tools

- Hyundai Wia Corp.

- Biesse Group

- Brother Industries Ltd

- FFG Europe & Americas

- Makino Milling Machine Co. Ltd

- Chiron Group SE

- JTEKT Corporation (Toyoda)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Industry 4.0-driven automation upgrades

- 4.2.2 Rising precision demand in automotive & aerospace

- 4.2.3 Government incentives for factory modernization

- 4.2.4 Rapid adoption of 5-axis machining for EV & implants

- 4.2.5 Hybrid additive-subtractive CNC integration

- 4.2.6 Digital-twin-enabled predictive programming

- 4.3 Market Restraints

- 4.3.1 High capital & lifecycle costs

- 4.3.2 Skilled CNC programmer shortage

- 4.3.3 Cyber-security risks to connected CNC controls

- 4.3.4 Component supply-chain instability (ball screws, guides)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts(Value, In USD Billion)

- 5.1 By Machine Type

- 5.1.1 CNC Lathes

- 5.1.2 CNC Milling Machines

- 5.1.3 CNC Laser Cutting Machines

- 5.1.4 CNC Plasma Cutters

- 5.1.5 CNC EDM (Die-sink & Wire)

- 5.1.6 CNC Grinding Machines

- 5.1.7 CNC Drilling/Tapping Centers

- 5.1.8 Other Specialty CNC Machines

- 5.2 By Axis Type

- 5.2.1 3-Axis Machines

- 5.2.2 4-Axis Machines

- 5.2.3 5-Axis Machines

- 5.2.4 6-Axis & Above

- 5.3 By End-user Industry

- 5.3.1 Automotive

- 5.3.2 Aerospace & Defense

- 5.3.3 Electronics & Semiconductor

- 5.3.4 Medical Devices

- 5.3.5 Construction & Heavy Machinery

- 5.3.6 Power & Energy

- 5.3.7 Shipbuilding

- 5.3.8 General Manufacturing & Job Shops

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Peru

- 5.4.2.4 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.4.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.4.3.8 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 Australia

- 5.4.4.5 South Korea

- 5.4.4.6 ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam)

- 5.4.4.7 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Qatar

- 5.4.5.4 Kuwait

- 5.4.5.5 Turkey

- 5.4.5.6 Egypt

- 5.4.5.7 South Africa

- 5.4.5.8 Nigeria

- 5.4.5.9 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 FANUC Corporation

- 6.4.2 DMG Mori Co. Ltd

- 6.4.3 Haas Automation Inc.

- 6.4.4 Okuma Corporation

- 6.4.5 Mitsubishi Electric Corporation

- 6.4.6 Siemens AG

- 6.4.7 Yamazaki Mazak Corporation

- 6.4.8 Bosch Rexroth AG

- 6.4.9 GSK CNC Equipment Co. Ltd

- 6.4.10 Hurco Companies Inc.

- 6.4.11 Dr. Johannes Heidenhain GmbH

- 6.4.12 Trumpf Group

- 6.4.13 Doosan Machine Tools

- 6.4.14 Hyundai Wia Corp.

- 6.4.15 Biesse Group

- 6.4.16 Brother Industries Ltd

- 6.4.17 FFG Europe & Americas

- 6.4.18 Makino Milling Machine Co. Ltd

- 6.4.19 Chiron Group SE

- 6.4.20 JTEKT Corporation (Toyoda)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

自動多軸攻牙機市場:依驅動類型、機器方向、軸類型、通路、最終用途產業分類,全球預測(2026-2032年)工業分板銑床市場(按銑床類型、切割技術、軸配置、自動化程度和最終用途行業分類)-全球預測,2026-2032年按玻璃材料、介面類型、測量範圍、解析度和終端用戶產業分類的CNC玻璃尺市場,全球預測,2026-2032年金屬板材矯直機市場(按機器類型、最終用途行業、材料類型、板材厚度、自動化程度、配置、驅動類型和配銷通路分類),全球預測,2026-2032年電動捲材矯直機市場按材料、最終用戶、機器類型、自動化程度、厚度範圍、驅動類型和部署方式分類-全球預測,2026-2032年

自動多軸攻牙機市場:依驅動類型、機器方向、軸類型、通路、最終用途產業分類,全球預測(2026-2032年)工業分板銑床市場(按銑床類型、切割技術、軸配置、自動化程度和最終用途行業分類)-全球預測,2026-2032年按玻璃材料、介面類型、測量範圍、解析度和終端用戶產業分類的CNC玻璃尺市場,全球預測,2026-2032年金屬板材矯直機市場(按機器類型、最終用途行業、材料類型、板材厚度、自動化程度、配置、驅動類型和配銷通路分類),全球預測,2026-2032年電動捲材矯直機市場按材料、最終用戶、機器類型、自動化程度、厚度範圍、驅動類型和部署方式分類-全球預測,2026-2032年 數控切割機市場規模、佔有率及成長分析(按機器類型、技術類型、應用產業、最終用戶和地區分類)-2026-2033年產業預測CNC等離子切割台市場按檯面類型、功率、操作模式、驅動類型、材質、切割厚度、應用和最終用戶分類-2026-2032年全球預測按冷卻類型、工具機類型、冷卻液配方、終端用戶產業和分銷管道分類的CNC工具機冷卻市場,全球預測,2026-2032年按技術、自動化程度、機器尺寸、最終用戶和分銷管道分類的數控熔融機市場—2026-2032年全球預測按自動化程度、驅動類型、控制系統、材料類型和最終用戶分類的數控等離子切割機市場,全球預測,2026-2032年

數控切割機市場規模、佔有率及成長分析(按機器類型、技術類型、應用產業、最終用戶和地區分類)-2026-2033年產業預測CNC等離子切割台市場按檯面類型、功率、操作模式、驅動類型、材質、切割厚度、應用和最終用戶分類-2026-2032年全球預測按冷卻類型、工具機類型、冷卻液配方、終端用戶產業和分銷管道分類的CNC工具機冷卻市場,全球預測,2026-2032年按技術、自動化程度、機器尺寸、最終用戶和分銷管道分類的數控熔融機市場—2026-2032年全球預測按自動化程度、驅動類型、控制系統、材料類型和最終用戶分類的數控等離子切割機市場,全球預測,2026-2032年