|

市場調查報告書

商品編碼

1934859

美國工業木器塗料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)United States Industrial Wood Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

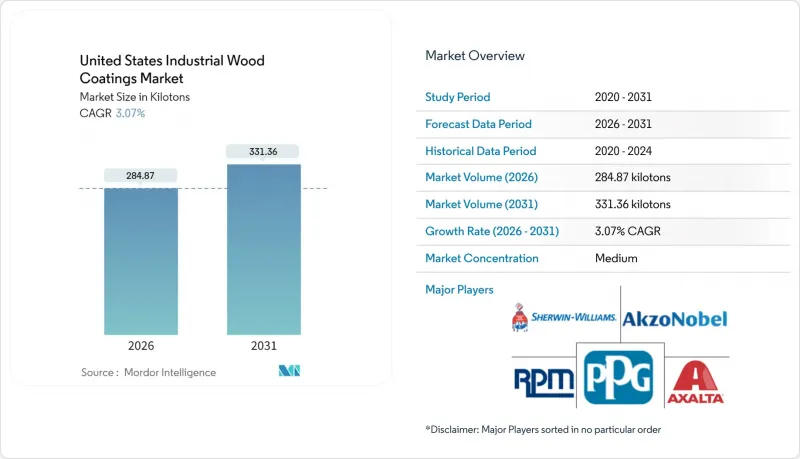

美國工業木器塗料市場預計將從 2025 年的 276.39 千噸成長到 2026 年的 284.87 千噸,預計到 2031 年將達到 331.36 千噸,2026 年至 2031 年的複合年成長率為 3.07%。

這一穩步成長歸功於住宅的復甦、租賃住房建設熱潮的加速以及製造業向工廠預塗裝工藝的轉變,從而減少了現場施工。儘管聚氨酯塗料因其卓越的耐化學性而佔據主導地位,但儘管水性塗料面臨監管壓力,溶劑型塗料的銷售仍領先。木工零件供應商優先研發能夠與機器人塗裝生產線無縫整合的配方,以緩解技術純熟勞工短缺並保持塗裝效果的一致性。將樹脂創新與端到端自動化指導相結合的製造商,透過確保客戶同時滿足性能和環保標準,正在贏得市場佔有率。聚酯多元醇和二氧化鈦等原料的供應挑戰持續考驗籌資策略,促使企業採取策略性儲備和長期供應協議談判等措施。

美國工業木器塗料市場趨勢與洞察

美國家具和櫥櫃產量增加

家具和櫥櫃銷售的成長帶動了面漆、密封劑和UV填料的強勁需求。受疫情導致的運輸中斷影響,國內製造商的市佔率正不斷擴大。大型機殼和嵌入式家電收納的興起,推動了對耐刮聚氨酯塗層的需求。廚房改造傾向於深色、低光澤飾面,這需要兼具深邃色彩和低VOC含量的塗料。水性聚氨酯混合產品供應商正在競標競標於2026年推出的新產品線。

新冠疫情後住宅翻新熱潮

2024年,住宅維修支出達到頂峰,屋主們將節省的錢用於廚房維修、客製化木工和實木地板翻新。櫥櫃更換週期加快,縮短了塗料的使用壽命,導致工廠預塗塗料的訂單穩定成長。承包商在居住的住宅施工中,傾向於選擇低氣味、快速固化的塗料系統,這進一步推動了對丙烯酸和紫外線固化塗料的需求,因為這些塗料無需延長通風時間即可滿足緊迫的計劃要求。

嚴格的聯邦和州VOC/HAP法規

美國環保署(EPA)的有害空氣污染物法規將甲醛含量限制在0.20 ppm以內,並限制在擦拭巾劑中使用二氯甲烷,這會影響滲透深度和顯色效果。加州對芳香族化合物含量的額外規定要求進行廣泛的第三方測試,這增加了配方成本。規模較小、合規能力有限的區域性公司正被迫退出市場,增加了2027年後供應商格局進一步整合的可能性。

細分市場分析

到2025年,聚氨酯塗料將佔據美國工業木器塗料市場59.42%的佔有率,並在2031年之前以3.60%的複合年成長率持續成長。聚氨酯塗料的耐用性能夠滿足家具檯面、門窗和樓梯部件對耐磨性和耐化學腐蝕性的需求。水性聚氨酯塗料在透明度和流動性方面已與溶劑型塗料不相上下,這加速了其在VOC(揮發性有機化合物)法規嚴格的州的普及。

丙烯酸類化學品在低磨損的室內裝飾部件領域佔據著經濟實惠的一席之地。同時,醇酸樹脂在傳統木工車間仍佔據主導地位,但其市場佔有率正被低氣味產品蠶食。聚酯樹脂是紫外線固化生產線的核心,這些生產線在櫥櫃和地板生產車間中佔據主導地位。環氧樹脂為需要強耐化學性的實驗室和醫療設備提供材料。硝化纖維素漆的應用範圍有限,但其快速的維修週期使其保持了價值,而這正是製琴師所重視的。

美國工業木器塗料市場報告按樹脂類型(環氧樹脂、丙烯酸樹脂、醇酸樹脂、聚氨酯、聚酯樹脂等)、技術(水性、溶劑型、UV固化、粉末塗料)和終端用戶行業(木製家具、細木工、地板/甲板等)進行細分。市場預測以公噸為單位。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 美國家具和櫥櫃產量增加

- 新冠疫情後住宅翻新熱潮

- 促進低揮發性有機化合物配方的相關法規

- 引進機器人和輸送機式噴塗生產線

- 「租賃住宅」正在推動對預製木製品的需求

- 市場限制

- 嚴格的聯邦和州VOC/HAP法規

- 石油樹脂和二氧化鈦的價格波動

- 聚酯多元醇間歇性供不應求

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 依樹脂類型

- 環氧樹脂

- 丙烯酸纖維

- 醇酸樹脂

- 聚氨酯

- 聚酯纖維

- 其他(硝化纖維素等)

- 透過技術

- 水溶液

- 溶劑型

- 紫外線固化型

- 粉末塗裝

- 按最終用戶行業分類

- 木製家具

- 配件(窗戶、門、裝飾線條)

- 地板和露台

- 其他(樂器、體育器材)

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Akzo Nobel NV

- Axalta Coating Systems

- Benjamin Moore & Co.

- CERAMIC INDUSTRIAL COATINGS

- Diamond Vogel

- Hempel A/S

- ICP Industrial Solutions Group

- Jotun A/S

- PPG Industries Inc.

- RPM International Inc.

- Stiles Industrial Coatings

- Teknos Group

- The Sherwin William Company

第7章 市場機會與未來展望

The United States Industrial Wood Coatings Market is expected to grow from 276.39 kilotons in 2025 to 284.87 kilotons in 2026 and is forecast to reach 331.36 kilotons by 2031 at 3.07% CAGR over 2026-2031.

This steady expansion follows the recovery of residential construction, the accelerating build-to-rent boom, and a shift in manufacturing toward factory-applied finishes that reduce job-site labor requirements. Polyurethane systems dominate due to their superior chemical resistance, while solvent-borne chemistries still lead in volume, despite regulatory pressure favoring water-borne alternatives. Millwork suppliers are prioritizing formulations that integrate smoothly with robotic spray lines to curb skilled-labor shortfalls and maintain finish consistency. Manufacturers that pair resin innovations with end-to-end automation guidance are carving out share by ensuring customers meet both performance and environmental benchmarks. Challenges with raw materials, such as polyester polyols and titanium dioxide, continue to test procurement strategies, prompting strategic stockpiling and the negotiation of long-term supplier contracts.

United States Industrial Wood Coatings Market Trends and Insights

Rising U.S. Furniture and Cabinetry Production

Furniture and cabinetry increased sales, underpinning robust volume pull for topcoats, sealers, and UV fillers. Domestic makers gained ground after the pandemic's shipping snarls, and their shift toward larger cabinet carcasses and integrated appliance housing heightens the requirements for scratch-resistant polyurethane layers. Kitchen remodel projects now favor dark, low-gloss looks, demanding stains that balance deep color with low-VOC compliance. Suppliers responding with water-borne polyurethane hybrids are winning bids for new lines set to launch in 2026.

Residential Remodeling Boom Post-COVID

Home-improvement outlays peaked in 2024 as owners funneled savings into kitchen refits, custom millwork, and hardwood refinishing. Faster cabinet replacement cycles shorten finish lifespans, keeping orders for factory-applied coatings on a steady climb. Contractors working in occupied homes specify low-odor, rapid-cure systems, steering more volume to acrylic and UV-curable options that meet tight project schedules without extended ventilation times.

Stringent Federal and State VOC/HAP Limits

EPA caps on hazardous air pollutants restrict formaldehyde to 0.20 ppm and curb the use of methylene chloride in wipe stains, forcing compromises in penetration depth and color build. California's additional aromatic content rules require exhaustive third-party testing, which inflates formulation costs. Smaller regional companies with limited compliance teams face exit decisions, raising the likelihood of a more consolidated supplier landscape after 2027.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Push Toward Low-VOC Formulations

- Adoption of Robotics and Conveyorized Spray Lines

- Volatile Petro-Resin and TiO2 Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyurethane systems accounted for 59.42% of the United States industrial wood coatings market share in 2025, expanding at a 3.60% CAGR toward 2031. The robustness of polyurethane meets the demands of abrasion and chemical exposure on furniture tops, doors, and stair parts. Waterborne grades now match solvent analogs in clarity and flow, accelerating adoption in states with stringent VOC caps.

Acrylic chemistries retain a cost-efficient niche for interior components with lighter wear, while alkyds continue to dominate traditional millwork shops but are losing market share to lower-odor options. Polyester resins form the backbone of UV-curable lines that dominate high-throughput cabinet and flooring plants. Epoxies supply laboratory and healthcare fixtures needing aggressive chemical resistance. Nitrocellulose lacquers, though relegated to musical instruments, preserve value through fast repair cycles valued by luthiers.

The United States Industrial Wood Coatings Market Report is Segmented by Resin Type (Epoxy, Acrylic, Alkyd, Polyurethane, Polyester, and Others), Technology (Water-Borne, Solvent-Borne, UV-Curable, and Powder), and End-User Industry (Wooden Furniture, Joinery, Flooring and Decking, and Others). The Market Forecasts are Provided in Terms of Volume (Tons).

List of Companies Covered in this Report:

- Akzo Nobel N.V.

- Axalta Coating Systems

- Benjamin Moore & Co.

- CERAMIC INDUSTRIAL COATINGS

- Diamond Vogel

- Hempel A/S

- ICP Industrial Solutions Group

- Jotun A/S

- PPG Industries Inc.

- RPM International Inc.

- Stiles Industrial Coatings

- Teknos Group

- The Sherwin William Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising U.S. furniture and cabinetry production

- 4.2.2 Residential remodeling boom post-COVID

- 4.2.3 Regulatory push toward low-VOC formulations

- 4.2.4 Adoption of robotics and conveyorized spray lines

- 4.2.5 "Build-to-Rent" housing fueling pre-finished millwork demand

- 4.3 Market Restraints

- 4.3.1 Stringent federal and state VOC/HAP limits

- 4.3.2 Volatile petro-resin and TiO2 prices

- 4.3.3 Intermittent polyester polyol shortages

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Resin Type

- 5.1.1 Epoxy

- 5.1.2 Acrylic

- 5.1.3 Alkyd

- 5.1.4 Polyurethane

- 5.1.5 Polyester

- 5.1.6 Others (Nitro-cellulose, etc.)

- 5.2 By Technology

- 5.2.1 Water-Borne

- 5.2.2 Solvent-Borne

- 5.2.3 UV-Curable

- 5.2.4 Powder

- 5.3 By End-User Industry

- 5.3.1 Wooden Furniture

- 5.3.2 Joinery (Windows, Doors, Molding)

- 5.3.3 Flooring and Decking

- 5.3.4 Others (Musical instruments, Sports goods)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Akzo Nobel N.V.

- 6.4.2 Axalta Coating Systems

- 6.4.3 Benjamin Moore & Co.

- 6.4.4 CERAMIC INDUSTRIAL COATINGS

- 6.4.5 Diamond Vogel

- 6.4.6 Hempel A/S

- 6.4.7 ICP Industrial Solutions Group

- 6.4.8 Jotun A/S

- 6.4.9 PPG Industries Inc.

- 6.4.10 RPM International Inc.

- 6.4.11 Stiles Industrial Coatings

- 6.4.12 Teknos Group

- 6.4.13 The Sherwin William Company

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

中東·非洲的產業用木材塗料市場:2025年亞洲的產業用木材塗料市場:2025年南北美洲的產業用木材塗料市場:2025年歐洲的產業用木材塗料市場:2025年產業用木材塗料的全球市場:2025年(報告套組)中東·非洲的工業用木材塗料市場 (2024年)

中東·非洲的產業用木材塗料市場:2025年亞洲的產業用木材塗料市場:2025年南北美洲的產業用木材塗料市場:2025年歐洲的產業用木材塗料市場:2025年產業用木材塗料的全球市場:2025年(報告套組)中東·非洲的工業用木材塗料市場 (2024年)