|

市場調查報告書

商品編碼

1934858

垂直產業軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Vertical Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

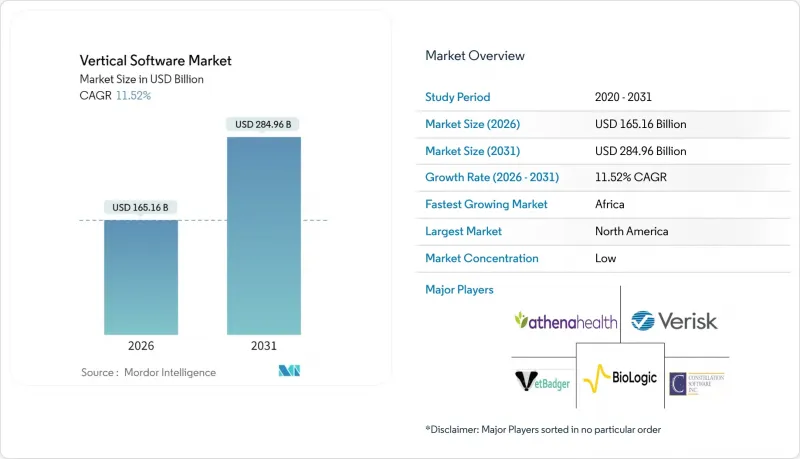

2025年垂直軟體市場價值1,481億美元,預計到2031年將達到2,849.6億美元,高於2026年的1,651.6億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 11.52%。

雲端優先交付模式、嵌入式監管框架和人工智慧工具包正在加速受監管產業、中型製造業和農業領域的採用。現有橫向供應商和純粹的專業供應商之間日益激烈的競爭,正透過領域級工作流程和嵌入式支付推動產品差異化。在北美保持主導地位的同時,非洲正經歷著最快的擴張,這得益於政府對數位化現代化的支持以及透過訂閱定價降低中小企業准入門檻。然而,不斷上漲的網路責任險和公共部門持續存在的遺留資料孤島正在限制技術的普及速度。

全球垂直產業軟體市場趨勢與洞察

產業專用的雲端平台的興起正在加速美國和歐洲的普及應用。

專為產業專用的打造的雲端平台透過整合合規資料模型和預先配置工作流程,顯著縮短了引進週期。歐洲雲端市場預計將從2023年的1,970億美元成長到2024年的2,320億美元,展現出快速的普及速度。醫院、工廠、銀行和零售商等行業擴大選擇承包平台,以最大限度地減少客製化編碼和審核風險。基於這些雲端平台所建構的金融服務能夠提升經常性收入和客戶鎖定率,從而推動整個垂直行業軟體市場以3.5%的複合年成長率成長。即時資料處理歷程、參考架構和持續合規性監控等功能進一步降低了轉換成本,並建構了可抵禦的競爭優勢。

隨著銀行、金融服務和保險 (BFSI) 以及醫療保健行業的監管合規壓力日益增大,專業解決方案也不斷擴展。

將於2025年10月生效的《公平貸款規則》修正案將強制實施自動化估值模型,迫使銀行採用內建審核追蹤和模型風險管治的軟體。同樣,對人工智慧醫療設備的審查力度加大,也迫使供應商依賴具有可追溯資料管道和受控更新的平台。這些壓力推動了尋求避免罰款和聲譽風險的買家的需求,從而促進了產業專用的SaaS的成長,增幅達2.8%。

傳統資料孤島阻礙公共部門向垂直雲端遷移

正如美國國防部創新委員會的評估所示,分散的本地環境由於資料發現和存取困難而阻礙了互通性。複雜的遷移項目會增加預算、延長工期,並對垂直軟體市場造成1.2%的負面影響。政府機構通常要求分階段實施雙運行架構,這使得雲端優勢的實現被推遲,直到舊有系統完全淘汰。

細分市場分析

至2025年,雲端服務將佔垂直產業軟體市場規模的69.92% 。付費使用制、自動擴充和託管合規服務可將整體擁有成本 (TCO) 降低高達30%。企業也重視與公共雲端人工智慧服務的嵌入式,以增強決策支援。同時,本地部署解決方案的支出佔比將僅為30.08%,但隨著資料主權要求和空氣間隙安全需求重新提上規劃議程,其複合年成長率將達到13.97%。

混合架構正逐漸成為主流。企業在本地維護客戶個人識別資訊 (PII) 和基因組數據,同時將匿名化的遙測數據串流傳輸到雲端分析引擎。這種方法既滿足了監管要求,也確保了敏捷性。物聯網部署進一步強化了這種混合架構,營運感測器將資料傳輸到本地邊緣伺服器和雲端模型,從而實現即時洞察和長期最佳化。目前,能夠提供跨這些環境整合編配的供應商正獲得很高的訂單率。

到2025年,企業將佔總收入的51.67%,這反映了多站點部署和複雜的合規性要求。企業通常會採用分層架構模板,該模板由供應商藍圖驅動,並透過內建的支付和資料交換模組來促進帳戶擴展。然而,中小企業(SME)的採用率也在加速成長,其複合年成長率(CAGR)高達14.38%,高於整體軟體市場。按月收費、引導式實施精靈和市場附加元件降低了財務和技術門檻。

巨量資料分析正在為中小企業帶來可觀的利潤成長,而能夠洞察供應商和客戶行為的專有儀表板已被證明可以提高收入和效率。供應商提供的模組化軟體包支援逐步採用,確保用戶在提升銷售前即可獲得即時價值。遍遠地區寬頻的普及和行動優先介面的興起進一步釋放了潛在需求,尤其是在非洲和東南亞地區,從而擴大了垂直軟體產業的長期潛在市場規模。

本垂直產業軟體市場報告按部署模式(雲端/本地部署)、組織規模(中小企業/大型企業)、最終用戶產業(銀行、金融服務和保險 (BFSI)/教育等)、應用(客戶關係管理/企業資源規劃等)和地區進行細分。市場預測以美元計價。

區域分析

2025年,北美將佔全球收入的51.76%,這得益於先進的雲端基礎設施、充裕的創業投資資金以及重視領域豐富型平台的嚴格合規體系。聯邦政府對電子健康記錄現代化和開放銀行API的獎勵進一步提振了市場需求。受監管領域的大規模標竿客戶案例,其影響力延伸至中端市場,從而增強了網路效應,並推動了整個垂直行業軟體市場的發展。

亞太地區正以14.02%的複合年成長率成長。中國、日本和韓國等製造業驅動型經濟體正在採用人工智慧工具包進行預測性維護並建構智慧工廠。同時,印度的中小企業正透過訂閱模式採用人工智慧,並跨越式舊有系統。預計到2027年,該地區的人工智慧支出將達到907億美元。儘管人才短缺問題依然存在,但頂尖大學和跨國培訓夥伴關係正在幫助彌合技能差距。

歐洲市場格局複雜。嚴格的資料保護框架推動了對具備認證控制的行業雲的需求,而跨境監管差異則增加了複雜性和成本。能夠實現本地化託管、證明符合主權雲端標準並整合ESG報告工具的供應商在採購競爭中佔據優勢,從而增強了垂直軟體市場的成長勢頭。非洲正以15.97%的複合年成長率快速擴張。在中小企業快速數位化以及農業、金融科技和醫療保健領域強勁需求的推動下,非洲正在崛起為垂直軟體市場的重要參與者。南非、奈及利亞和埃及處於領先地位,這得益於政府主導轉型舉措計劃正在推動垂直SaaS解決方案的普及,這些解決方案能夠滿足本地合規性要求、語言差異化需求,並採用行動優先策略。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 產業專用的雲端平台的興起正在加速美國和歐洲的普及應用。

- 銀行、金融服務和保險 (BFSI) 以及醫療保健行業日益成長的監管合規壓力,推動了對專業解決方案的需求。

- 人工智慧/機器學習工具包推動亞太地區中小企業製造業現代化

- 南美洲農業食品供應鏈數位化推動農業技術SaaS發展

- 政府資助的智慧醫院計劃推動醫療技術軟體發展

- 訂閱定價模式加速了中小企業在非洲的滲透。

- 市場限制

- 傳統資料孤島正在減緩公共部門的垂直雲端遷移進程。

- 缺乏領域知識會限制客製化速度。

- 網路責任責任險成本不斷上漲,推高了整體擁有成本。

- 歐盟和東協的多司法管轄區法規阻礙了跨境擴張

- 價值鏈分析

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 對宏觀經濟趨勢的市場評估

第5章 市場規模與成長預測

- 按部署模式

- 雲

- 本地部署

- 按組織規模

- 中小企業

- 主要企業

- 按最終用戶行業分類

- BFSI

- 醫療保健和生命科學

- 教育

- 政府和法律

- 媒體、娛樂和飯店

- 服飾和服飾

- 農業和農場管理

- 其他終端用戶產業

- 透過使用

- 客戶關係管理

- 企業資源規劃

- 供應鏈管理

- 人力資源管理

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Constellation Software Inc.

- Verisk Analytics, Inc.

- athenahealth, Inc.

- Bio-Logic Science Instruments SA

- VetBadger LLC

- FastBound LLC

- Mail Technologies Inc.

- Granular, Inc.(Corteva)

- Farmbrite, LLC

- Renderforest LLC

- Veeva Systems Inc.

- Guidewire Software, Inc.

- Epic Systems Corporation

- Procore Technologies, Inc.

- Toast, Inc.

- Shopify Inc.

- Oracle Health(Cerner Corp.)

- Teladoc Health, Inc.

- IFS AB

- Infor, Inc.

- ServiceTitan, Inc.

- Blackbaud, Inc.

- MINDBODY, Inc.

- Intelerad Medical Systems Incorporated

第7章 市場機會與未來展望

The vertical software market was valued at USD 148.10 billion in 2025 and estimated to grow from USD 165.16 billion in 2026 to reach USD 284.96 billion by 2031, at a CAGR of 11.52% during the forecast period (2026-2031).

Cloud-first delivery models, embedded regulatory frameworks, and artificial-intelligence toolkits are accelerating adoption across regulated industries, mid-sized manufacturing, and agriculture. Intensifying competition between incumbent horizontal vendors and pure-play specialists is sharpening product differentiation through domain-level workflows and embedded payments. North America retains a leadership position, but Africa is expanding fastest as governments support digital modernization and as subscription pricing lowers barriers for small and medium enterprises. Simultaneously, rising cyber-liability premiums and persistent legacy data silos in the public sector temper deployment velocity.

Global Vertical Software Market Trends and Insights

Emergence of Industry-specific Cloud Platforms Accelerating Adoption in US & Europe

Purpose-built industry clouds radically shorten implementation cycles by bundling compliant data models and pre-configured workflows. Rapid uptake is evident in the European cloud market, which rose from USD 197 billion in 2023 to USD 232 billion in 2024. Hospitals, factories, banks, and retailers increasingly choose turnkey platforms to minimise custom coding and audit risk. Embedded financial services within these clouds augment recurring revenue and lock-in, driving the +3.5% lift to the overall vertical software market CAGR. Capabilities such as real-time data lineage, reference architectures, and continuous compliance monitoring further strengthen switching costs and create defensible moats.

Regulatory Compliance Pressures in BFSI & Healthcare Boosting Specialized Solutions

Evolving fair-lending rules effective October 2025 require automated valuation models, pushing banks toward software that embeds audit trails and model-risk governance. Parallel scrutiny surrounds AI-enabled medical devices, compelling providers to rely on platforms with traceable data pipelines and managed updates. These pressures escalate demand for sector-specific SaaS, producing a +2.8% contribution to growth as buyers seek to avoid fines and reputational risk.

Legacy Data Silos Slowing Vertical Cloud Migration in the Public Sector

Fragmented on-premise estates hinder interoperability, as documented by the US Defense Innovation Board's assessment of poor data discoverability and access. Complex migration programs inflate budgets and extend timelines, causing a -1.2% drag on the vertical software market. Agencies often require phased dual-run architectures that slow realisation of cloud benefits until legacy retirement is complete.

Other drivers and restraints analyzed in the detailed report include:

- AI/ML Toolkits Driving Mid-sized Manufacturing Modernization in Asia-Pacific

- Digitalization of Ag-food Supply Chains Fueling AgTech SaaS in South America

- Rising Cyber-Liability Insurance Costs Inflating TCO

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-based offerings account for 69.92% of the vertical software market size in 2025. Pay-as-you-go pricing, auto-scaling, and managed compliance services lower total ownership costs by up to 30%. Enterprises also value built-in integration to public cloud AI services that sharpen decision support. Conversely, on-premise solutions, while only 30.08% of spending, register a 13.97% CAGR as data-sovereignty mandates and air-gapped security requirements re-enter the planning agenda.

Hybrid architectures are becoming standard; organisations retain customer PII or genomic data on-site while streaming anonymised telemetry into cloud analytics engines. The approach satisfies regulators yet still captures agility. IoT adoption amplifies this mix, as operational sensors feed both local edge servers and cloud models, yielding real-time insights and long-term optimisation. Suppliers that offer unified orchestration across these environments now enjoy premium win rates.

Enterprises accounted for 51.67% of 2025 revenue, reflecting multi-site rollouts and complex compliance demands. They typically execute phased global templates that anchor vendor roadmaps and feed account expansion via embedded payments or data-exchange modules. However, SME uptake is accelerating, delivering a 14.38% CAGR that outpaces the overall vertical software market. Pay-monthly pricing, guided implementation wizards, and marketplace add-ons lower both financial and skills barriers.

Big-data analytics drive measurable gains for smaller firms, with studies showing revenue and efficiency improvements once proprietary dashboards reveal supplier and customer behavior. Vendors respond with modular packaging that allows incremental adoption, ensuring immediate value before upsell. Rural broadband expansion and mobile-first interfaces further open latent demand, particularly in Africa and Southeast Asia, reinforcing the long-run addressable pool for the vertical software industry.

The Vertical Software Market Report Segmented by Deployment Model (Cloud, and On-Premises), Organization Size (Small and Medium Enterprise, and Large Enterprise), End-User Industry (Banking, Financial Services, and Insurance (BFSI), Educational Institution, and More), Application (Customer Relationship Management, Enterprise Resource Planning, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 51.76% of 2025 revenue, supported by sophisticated cloud infrastructure, deep venture funding, and strict compliance regimes that reward domain-rich platforms. Federal incentives for electronic health-record modernisation and open banking APIs further cement demand. Large-scale reference customers in regulated arenas provide proof points that ripple through mid-market segments, reinforcing network effects and the overall vertical software market.

Asia-Pacific is advancing at a 14.02% CAGR. Manufacture-heavy economies, such as China, Japan, and South Korea, deploy AI toolkits for predictive maintenance and smart-factory orchestration, while India's SME population leverages subscription models to leapfrog legacy systems. Regional AI spending is expected to hit USD 90.7 billion by 2027. Although talent constraints persist, tier-one universities and cross-border training partnerships are helping to narrow the skills gap.

Europe presents mixed dynamics with a stringent data-protection framework spurs demand for industry clouds with certified controls, yet cross-border regulatory divergence introduces complexity and cost. Providers able to localise hosting, attest to sovereign-cloud standards, and integrate ESG reporting tools are winning procurement contests and reinforcing momentum in the vertical software market. Africa is expanding at fastest CAGR of 15.97%. Driven by swift SME digitization and robust demand in agriculture, fintech, and healthcare, Africa is carving out a pivotal role in the vertical software market. South Africa, Nigeria, and Egypt are at the forefront, championing the adoption of vertical SaaS solutions that cater to local compliance, language nuances, and a mobile-first approach, all bolstered by government-led digital transformation initiatives.

- Constellation Software Inc.

- Verisk Analytics, Inc.

- athenahealth, Inc.

- Bio-Logic Science Instruments SA

- VetBadger LLC

- FastBound LLC

- Mail Technologies Inc.

- Granular, Inc. (Corteva)

- Farmbrite, LLC

- Renderforest LLC

- Veeva Systems Inc.

- Guidewire Software, Inc.

- Epic Systems Corporation

- Procore Technologies, Inc.

- Toast, Inc.

- Shopify Inc.

- Oracle Health (Cerner Corp.)

- Teladoc Health, Inc.

- IFS AB

- Infor, Inc.

- ServiceTitan, Inc.

- Blackbaud, Inc.

- MINDBODY, Inc.

- Intelerad Medical Systems Incorporated

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Emergence of Industry-specific Cloud Platforms Accelerating Adoption in US and Europe

- 4.2.2 Regulatory Compliance Pressures in BFSI and Healthcare Boosting Specialized Solutions

- 4.2.3 AI/ML Toolkits Driving Mid-sized Manufacturing Modernization in Asia-Pacific

- 4.2.4 Digitalization of Ag-food Supply Chains Fueling AgTech SaaS in South America

- 4.2.5 Government-funded Smart-Hospital Programs Propelling Health-tech Software

- 4.2.6 Subscription Pricing Unlocking SME Penetration in Africa

- 4.3 Market Restraints

- 4.3.1 Legacy Data Silos Slowing Vertical Cloud Migration in Public Sector

- 4.3.2 Shortage of Domain-savvy Talent Limiting Customization Speed

- 4.3.3 Rising Cyber-Liability Insurance Costs Inflating TCO

- 4.3.4 Multi-jurisdiction Regulations Hindering Cross-border Rollouts in EU and ASEAN

- 4.4 Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 Assessment of Macro Economic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Deployment Model

- 5.1.1 Cloud

- 5.1.2 On-Premise

- 5.2 By Organization Size

- 5.2.1 Small and Medium Enterprises (SMEs)

- 5.2.2 Large Enterprises

- 5.3 By End-User Industry

- 5.3.1 BFSI

- 5.3.2 Healthcare and Life Sciences

- 5.3.3 Education

- 5.3.4 Government and Legal

- 5.3.5 Media, Entertainment and Hospitality

- 5.3.6 Clothing and Apparel

- 5.3.7 Agriculture and Farming

- 5.3.8 Other End-user Industries

- 5.4 By Application

- 5.4.1 Customer Relationship Management

- 5.4.2 Enterprise Resource Planning

- 5.4.3 Supply Chain Management

- 5.4.4 Human Resource Management

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Spain

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emiartes

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global and Market Overviews, Segments, Financials, Strategy, Rank/Share, Products, Developments)

- 6.4.1 Constellation Software Inc.

- 6.4.2 Verisk Analytics, Inc.

- 6.4.3 athenahealth, Inc.

- 6.4.4 Bio-Logic Science Instruments SA

- 6.4.5 VetBadger LLC

- 6.4.6 FastBound LLC

- 6.4.7 Mail Technologies Inc.

- 6.4.8 Granular, Inc. (Corteva)

- 6.4.9 Farmbrite, LLC

- 6.4.10 Renderforest LLC

- 6.4.11 Veeva Systems Inc.

- 6.4.12 Guidewire Software, Inc.

- 6.4.13 Epic Systems Corporation

- 6.4.14 Procore Technologies, Inc.

- 6.4.15 Toast, Inc.

- 6.4.16 Shopify Inc.

- 6.4.17 Oracle Health (Cerner Corp.)

- 6.4.18 Teladoc Health, Inc.

- 6.4.19 IFS AB

- 6.4.20 Infor, Inc.

- 6.4.21 ServiceTitan, Inc.

- 6.4.22 Blackbaud, Inc.

- 6.4.23 MINDBODY, Inc.

- 6.4.24 Intelerad Medical Systems Incorporated

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

2026年全球綜合發展環境(永續發展目標)市場報告2026年全球軟體開發工具市場報告2026年全球獨立軟體供應商市場報告2026年全球垂直整合軟體市場報告

2026年全球綜合發展環境(永續發展目標)市場報告2026年全球軟體開發工具市場報告2026年全球獨立軟體供應商市場報告2026年全球垂直整合軟體市場報告 獨立軟體供應商市場規模、佔有率和成長分析(按軟體類型、部署類型、公司規模、最終用戶產業和地區分類)—產業預測(2026-2033 年)

獨立軟體供應商市場規模、佔有率和成長分析(按軟體類型、部署類型、公司規模、最終用戶產業和地區分類)—產業預測(2026-2033 年) 垂直軟體市場規模、佔有率和趨勢分析報告:按組織規模、應用、部署、最終用途、地區和細分市場預測,2025 年至 2033 年

垂直軟體市場規模、佔有率和趨勢分析報告:按組織規模、應用、部署、最終用途、地區和細分市場預測,2025 年至 2033 年 按應用程式類型和地區分類的軟體開發市場獨立軟體供應商 (ISV) 市場按部署模式、最終用戶產業垂直、公司規模和地區分類

按應用程式類型和地區分類的軟體開發市場獨立軟體供應商 (ISV) 市場按部署模式、最終用戶產業垂直、公司規模和地區分類 全球獨立軟體供應商 (ISVS) 市場,2025-2029

全球獨立軟體供應商 (ISVS) 市場,2025-2029 產業專用軟體的全球市場,2025-2029

產業專用軟體的全球市場,2025-2029