|

市場調查報告書

商品編碼

1934846

網路安全軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Cybersecurity Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

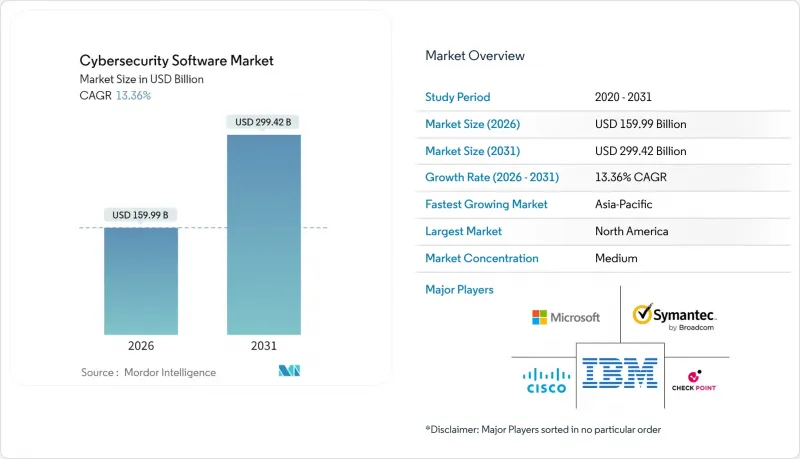

預計到 2026 年,網路安全軟體市場規模將達到 1,599.9 億美元,高於 2025 年的 1,411.3 億美元。

預計到 2031 年將達到 2,994.2 億美元,2026 年至 2031 年的複合年成長率為 13.36%。

雲端優先策略、零信任框架的日益普及以及人工智慧攻擊的興起,正在推動對整合安全平台的需求。雲端部署模式已佔總支出的三分之二,而隨著企業尋求減少工具冗餘並實現可衡量的風險降低,平台整合正在推動市場成長。監管罰款和日益嚴格的事件揭露規則正在加速採購決策,投資範圍也從大型企業擴展到中小企業。能夠將身分、雲端和分析功能整合到單一架構中的供應商,在網路安全軟體市場擁有巨大的發展機會。

全球網路安全軟體市場趨勢與洞察

雲端優先採用和零信任指令

零信任框架已從策略願景變為現實,81% 的組織計劃在 2026 年前採用該框架。領先的供應商正在將安全設計融入其雲端服務中,微軟的網路安全收入預計將在 2024 年超過 200 億美元,這印證了供應商的發展勢頭。分析師估計,近期 68% 的工業安全事件始於 IT 系統漏洞,進一步凸顯了零信任計劃對營運彈性的重要性。多重雲端環境日益複雜,促使企業優先考慮跨環境統一策略執行,從而推動了對整合平台的需求。能夠在單一技術堆疊中整合身分管理、存取控制和網路分段的供應商獲得了採購優先權。因此,平台訂閱長期合約的鎖定效應也在穩定增強。

人工智慧驅動的多向量網路攻擊激增

2024年,資訊竊取惡意軟體案件將激增500%,而勒索軟體即服務(RaaS)供應商降低了攻擊者的進入門檻。由於攻擊者實現了偵察和利用的自動化,API漏洞增加了1205%,傳統防禦措施不堪重負。 Change Healthcare的資料外洩事件影響了1億用戶,並導致2,200萬美元的贖金支付,凸顯了人工智慧驅動的攻擊宣傳活動對企業的影響。 CrowdAstrike目前每天處理84兆個威脅訊號以支援其預測分析,這反映出一場日益激烈的「軍備競賽」。董事會越來越將人工智慧驅動的風險視為策略性威脅,這促使他們在更廣泛的IT支出審查中尋求預算保護。

持續的勞動力短缺和不斷上漲的工資

光是日本就面臨超過20萬名網路安全專業人員的缺口,當地專業人員的平均時薪約為135.50美元(高於歷史水準)。儘管到2024年操作技術(OT)攻擊預計將成長73%,但OT安全技能人才卻更加稀缺。為了應對這一短缺,企業正轉向資安管理服務和基於人工智慧的自動化,但這兩者都需要文化變革和實施投資。這種短缺推高了高級安全程序的整體擁有成本,並減緩了大規模部署的步伐。持續的工資上漲壓力可能會隨著時間的推移影響供應商的定價模式,從而限制網路安全軟體市場的成長速度。

細分市場分析

到2025年,身分和存取管理 (IAM) 將佔據網路安全軟體市場25.10%的佔有率,這表明身分已成為企業防禦的關鍵控制基礎。隨著企業對多重雲端和混合工作負載的安全保護,雲端安全解決方案預計到2031年將以14.60%的複合年成長率成長,成為所有產品領域中成長最快的細分市場。 CyberArk以15.4億美元收購Venafi凸顯了機器身分管治日益成長的重要性。此外,DevSecOps的日益普及和日益嚴格的隱私法規正在推動與應用和資料安全相關的網路安全軟體市場擴張。

市場對涵蓋身分、雲端、資料和基礎設施層的整合平台的需求日益成長。基礎設施和網路保護仍然是混合環境的核心,而新興的後量子密碼解決方案在NIST於2024年最終確定三種抗量子演算法後,正從實驗室走向試點。客戶越來越傾向於選擇能夠將多種功能整合到單一控制架構中的供應商,以降低營運成本。

預計到2025年,雲端採用率將達到66.85%,並在2031年之前以13.62%的複合年成長率持續成長,這將鞏固網路安全軟體市場不可逆轉的趨勢。微軟已透過人工智慧威脅分析和後量子加密技術增強了Azure的功能,這表明超大規模資料中心業者正在將先進功能直接整合到其技術堆疊中。本地部署的使用率將穩定下降,但在受監管資料居住規則約束的領域仍將持續存在。

混合策略將雲端的敏捷性與本地控制相結合,用於保護患者資料等敏感工作負載。自 2015 年以來,醫療機構遭受的攻擊激增 300%,因此,醫療機構已果斷轉向雲端安全。邊緣運算已成為第三個支柱,需要基於位置的策略執行。能夠跨雲端、本地和邊緣提供一致工作負載保護的供應商在採購過程中更具優勢。

網路安全軟體市場按產品類型(應用安全、雲端安全、資料安全等)、部署模式(本地部署、雲端部署)、終端用戶產業(銀行、金融服務和保險、醫療保健、製造業等)、企業規模(大型企業、中小企業)和地區進行細分。市場預測以美元計價。

區域分析

北美地區佔據最大的區域市場佔有率,達到 24.35%,這主要得益於成熟的供應商生態系統、強勁的創業融資以及諸如美國證券交易委員會 (SEC) 事件披露規則等監管要求。微軟的安全收入超過 200 億美元,CrowdStrike 預計 2025 年的年度經常性收入將達到 46 億美元,這充分體現了該地區的市場規模。跨境供應鏈的需求正在推動加拿大和墨西哥對網路安全解決方案的採用。網路保險保費趨於穩定,顯示企業正在加強基礎防禦體系。

亞太地區是成長最快的地區,預計到2031年將以13.42%的複合年成長率成長,這主要得益於快速的數位化進程和日益成長的威脅數量(佔全球整體網路安全事件的31%)。在政府指南下,中國的網路安全支出預計到2023年將超過386億美元。日本預計2029年將達到132.5億美元,但面臨嚴重的人才短缺問題。韓國正在扶持像AI SPERA這樣的創新Start-Ups,該公司已籌集850萬美元用於擴展其犯罪智慧財產權平台。該地區的網路保險保費正以每年約50%的速度成長,顯示風險轉移機制日趨成熟。

在GDPR、NIS2以及要求可驗證控制的新人工智慧法規的推動下,歐洲正在穩步擴張。德國、英國和法國在相關支出方面處於領先地位,而東歐國家則在歐盟一體化進程中加速採用這些技術。中東和非洲地區正經歷高速成長,這主要得益於波灣合作理事會(GCC)的智慧城市計劃以及阿拉伯聯合大公國和沙烏地阿拉伯的國家網路安全戰略。南非、奈及利亞和埃及是非洲大陸的先驅者,但勞動力發展仍是限制因素。能夠根據資料主權規則和語言偏好進行產品本地化的供應商,將在這些新興次區域中受益。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 雲端優先採用和零信任指令

- 人工智慧驅動的多向量網路攻擊激增

- 監管罰款不斷增加(例如,美國證券交易委員會的事件揭露)

- 轉向以 API 為中心的架構(新的攻擊面)

- 關鍵基礎設施中的OT/IT融合

- 網路保險保費上漲將促使人們採取積極主動的安全措施。

- 市場限制

- 持續的人才短缺和薪資上漲

- 工具氾濫導致經營團隊對投資報酬率感到疲勞

- 公共部門和中小企業遺留的技術債務

- 主權雲端與資料居住

- 供應鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 評估市場中的宏觀經濟因素

第5章 市場規模與成長預測

- 報價

- 應用程式安全

- 雲端安全

- 資料安全

- 身分和存取管理

- 基礎設施/網路保護

- 其他

- 按部署模式

- 本地部署

- 雲

- 終端用戶產業

- BFSI

- 衛生保健

- 製造業

- 政府/國防

- 資訊科技/通訊

- 其他

- 按組織規模

- 主要企業

- 中小企業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 東南亞

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- IBM

- Microsoft

- Cisco

- Check Point

- Broadcom(Symantec)

- Fortinet

- F5

- Palo Alto Networks

- Proofpoint

- CyberArk

- Zscaler

- Mandiant(Google)

- Sophos

- CrowdStrike

- Okta

- Cloudflare

- Trend Micro

- Rapid7

- SentinelOne

- Qualys

第7章 市場機會與未來展望

The cybersecurity software market size in 2026 is estimated at USD 159.99 billion, growing from 2025 value of USD 141.13 billion with 2031 projections showing USD 299.42 billion, growing at 13.36% CAGR over 2026-2031.

Cloud-first mandates, rising adoption of zero-trust frameworks, and the growing volume of AI-enabled attacks are reinforcing demand for unified security platforms. Cloud deployment models already command two-thirds of total spending, while platform consolidation continues as enterprises reduce tool sprawl and seek measurable risk reduction. Escalating regulatory fines and incident-disclosure rules are accelerating procurement decisions, and proactive investment is spreading from large enterprises to small and medium businesses. Vendors that integrate identity, cloud, and analytics functions into a single architecture are capturing outsized opportunity within the cybersecurity software market.

Global Cybersecurity Software Market Trends and Insights

Cloud-first Adoption and Zero-trust Mandates

Zero-trust frameworks are moving from strategic vision to operational reality, with 81% of organizations planning deployments by 2026. Major providers now embed security-by-design into cloud services, and Microsoft's cybersecurity revenue surpassed USD 20 billion in 2024, underscoring vendor momentum. Analysts confirm that 68% of recent industrial incidents started with IT system compromise, tightening the link between zero-trust projects and operational resilience. Multicloud complexity is prompting enterprises to favor unified policy enforcement across environments, which is driving up demand for integrated platforms. Providers that combine identity, access, and network segmentation within a single stack are gaining procurement preference. The result is a steady uptick in long-term contracts that lock in platform subscriptions.

Surge in AI-driven, Multi-vector Cyber-attacks

Information-stealing malware cases spiked 500% in 2024, while ransomware-as-a-service shops lowered entry barriers for attackers. API vulnerabilities rose 1,205% as adversaries automated reconnaissance and exploitation, overwhelming traditional defenses. The high-profile Change Healthcare breach affected 100 million people and involved a USD 22 million ransom payment, demonstrating the business impact of AI-enabled campaigns. CrowdStrike now processes 84 trillion daily threat signals to sharpen predictive analytics, reflecting escalating arms-race dynamics. Boards increasingly treat AI-driven risk as a strategic threat, translating into budget protection even amid broader IT spending reviews.

Persistent Talent Deficit and Wage Inflation

Japan alone needs over 200,000 additional cybersecurity professionals, and specialists there earn about USD 135.50 per hour, up from prior levels. Operational-technology security skills are scarcer still, even as OT attacks rose 73% in 2024. Companies are shifting to managed security services and to AI-based automation to fill gaps, but both require cultural change and onboarding investments. The shortfall increases the total cost of ownership for advanced security programs and slows large-scale rollouts. Over time, persistent wage pressure will influence vendor pricing models and could moderate the cybersecurity software market growth rate.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Regulatory Fines and SEC Incident-disclosure

- Tool Sprawl Causing ROI Fatigue in C-suites

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Identity and Access Management commanded 25.10% of the cybersecurity software market share in 2025, illustrating that identity is now the primary control plane for enterprise defense. Cloud security solutions are forecast to register a 14.60% CAGR through 2031, the fastest of all offerings, as businesses secure multicloud and hybrid workloads. CyberArk's USD 1.54 billion acquisition of Venafi spotlights the growing importance of machine-identity governance. The cybersecurity software market size tied to application and data security is also rising as DevSecOps gains ground and privacy regulations tighten.

Demand is coalescing around integrated platforms that span identity, cloud, data, and infrastructure layers. Infrastructure and network protection remains core for hybrid environments, while emerging post-quantum cryptography solutions move from labs to pilots after NIST finalized three quantum-resistant algorithms in 2024. Customers increasingly prefer vendors that can knit multiple functions into a single control fabric to lower operational overhead.

Cloud deployments captured 66.85% share in 2025 and are expected to grow at 13.62% CAGR through 2031, cementing irreversible migration trends in the cybersecurity software market. Microsoft enhanced Azure with AI threat analytics and post-quantum encryption, showing how hyperscalers embed advanced capabilities directly into their stacks. On-premises implementations decline steadily yet persist where regulatory data-residency rules apply.

Hybrid strategies combine cloud agility with on-site controls for sensitive workloads such as patient data. Healthcare organizations moved decisively to cloud security after seeing a 300% jump in attacks since 2015. Edge computing is emerging as a third pillar requiring location-aware policy enforcement. Vendors able to protect workloads consistently across cloud, on-premises, and edge win favor in procurement cycles.

Cybersecurity Software Market is Segmented by Offering (Application Security, Cloud Security, Data Security and More), Deployment Model (On-Premises, Cloud), End-User Vertical (BFSI, Healthcare, Manufacturing and More), Organization Size (Large Enterprises, Small and Medium Enterprises (SMEs)), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounts of 24.35% the largest regional share through a mature vendor ecosystem, strong venture funding, and regulatory mandates such as SEC incident-disclosure rules. Microsoft's security revenue surpassed USD 20 billion, and CrowdStrike reported USD 4.6 billion annual recurring revenue in 2025, showcasing regional scale. Cross-border supply-chain requirements are boosting adoption in Canada and Mexico. Cyber-insurance premiums have stabilized, suggesting improving baseline defenses across enterprises.

Asia-Pacific is the fastest-growing region with a 13.42% CAGR through 2031, driven by rapid digitization and elevated threat volume that accounts for 31% of global incidents. China's cybersecurity outlays are projected to top USD 38.6 billion by 2023, propelled by government directives. Japan expects a USD 13.25 billion market by 2029 but faces significant talent shortages. South Korea nurtures innovative startups like AI SPERA, which raised USD 8.5 million to scale its Criminal IP platform. The region's cyber-insurance premiums are growing near 50% annually, signaling maturation of risk-transfer mechanism.

Europe shows steady expansion under GDPR, NIS2, and emerging AI regulations requiring demonstrable controls. Germany, the United Kingdom, and France lead spending, while Eastern European states accelerate adoption amid EU integration. The Middle East and Africa exhibit high-growth pockets, led by Gulf Cooperation Council smart-city projects and national cyber strategies in the UAE and Saudi Arabia. South Africa, Nigeria, and Egypt are early continental leaders, though workforce development remains a constraint. Vendors that localize offerings to data-sovereignty rules and language preferences stand to gain within these emerging sub-regions.

- IBM

- Microsoft

- Cisco

- Check Point

- Broadcom (Symantec)

- Fortinet

- F5

- Palo Alto Networks

- Proofpoint

- CyberArk

- Zscaler

- Mandiant (Google)

- Sophos

- CrowdStrike

- Okta

- Cloudflare

- Trend Micro

- Rapid7

- SentinelOne

- Qualys

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-first adoption and zero-trust mandates

- 4.2.2 Surge in AI-driven, multi-vector cyber-attacks

- 4.2.3 Expanding regulatory fines (e.g., SEC incident-disclosure)

- 4.2.4 Shift to API-centric architectures (new attack surface)

- 4.2.5 OT/IT convergence in critical infrastructure

- 4.2.6 Rising cyber-insurance premiums drive proactive security

- 4.3 Market Restraints

- 4.3.1 Persistent talent deficit and wage inflation

- 4.3.2 Tool sprawl causing ROI fatigue in C-suites

- 4.3.3 Legacy technical debt in public sector and SMBs

- 4.3.4 Sovereign-cloud and data-residency conflicts

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assesment of Macroeconomic Factors on the market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Application Security

- 5.1.2 Cloud Security

- 5.1.3 Data Security

- 5.1.4 Identity and Access Management

- 5.1.5 Infrastructure / Network Protection

- 5.1.6 Others

- 5.2 By Deployment Model

- 5.2.1 On-premises

- 5.2.2 Cloud

- 5.3 By End-User Vertical

- 5.3.1 BFSI

- 5.3.2 Healthcare

- 5.3.3 Manufacturing

- 5.3.4 Government and Defense

- 5.3.5 IT and Telecommunications

- 5.3.6 Others

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises (SMEs)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Southeast Asia

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 IBM

- 6.4.2 Microsoft

- 6.4.3 Cisco

- 6.4.4 Check Point

- 6.4.5 Broadcom (Symantec)

- 6.4.6 Fortinet

- 6.4.7 F5

- 6.4.8 Palo Alto Networks

- 6.4.9 Proofpoint

- 6.4.10 CyberArk

- 6.4.11 Zscaler

- 6.4.12 Mandiant (Google)

- 6.4.13 Sophos

- 6.4.14 CrowdStrike

- 6.4.15 Okta

- 6.4.16 Cloudflare

- 6.4.17 Trend Micro

- 6.4.18 Rapid7

- 6.4.19 SentinelOne

- 6.4.20 Qualys

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

2026年全球旅遊安全市場報告

2026年全球旅遊安全市場報告 全球數位攻防靶場市場報告:實際結果與預測(2021-2032)2026年全球Web3安全市場報告2026年全球電信網路安全解決方案市場報告2026年全球漏洞預測評分平台市場報告2026年通訊業全球資料保存市場報告

全球數位攻防靶場市場報告:實際結果與預測(2021-2032)2026年全球Web3安全市場報告2026年全球電信網路安全解決方案市場報告2026年全球漏洞預測評分平台市場報告2026年通訊業全球資料保存市場報告 企業網路安全解決方案市場:按解決方案類型、應用、產業、部署模式和客戶類型分類 - 2026-2032 年全球預測2026年全球資訊科技(IT)與通訊網路安全市場報告2026年全球網路安全市場報告

企業網路安全解決方案市場:按解決方案類型、應用、產業、部署模式和客戶類型分類 - 2026-2032 年全球預測2026年全球資訊科技(IT)與通訊網路安全市場報告2026年全球網路安全市場報告 網路安全軟體和服務市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶和解決方案分類

網路安全軟體和服務市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶和解決方案分類