|

市場調查報告書

商品編碼

1934845

雲端運算:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Cloud Computing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

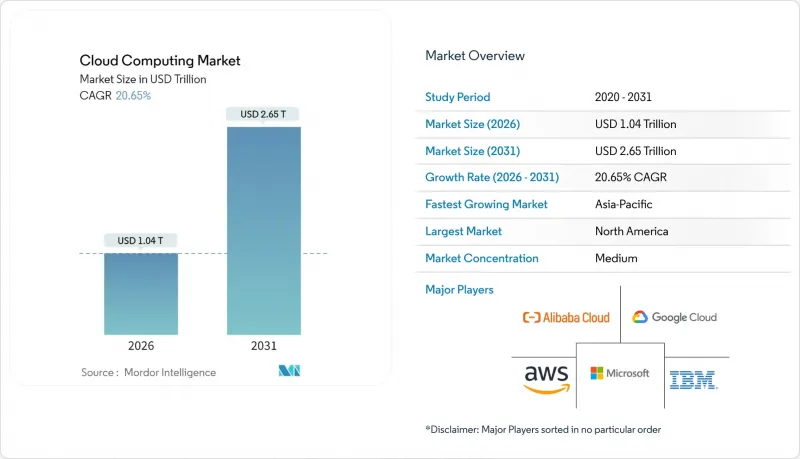

預計雲端運算市場將從 2025 年的 8,600 億美元成長到 2026 年的 1.04 兆美元,到 2031 年達到 2.65 兆美元,2026 年至 2031 年的複合年成長率為 20.65%。

這種快速成長與以人工智慧為先導的數位轉型計畫、核心應用程式向SaaS平台的遷移、歐洲和沿岸地區主權雲端法規的擴展,以及支援擴增實境(XR)和自動駕駛用例的10毫秒以下邊緣雲端區域的部署密切相關。因此,超大規模雲端服務供應商正在迅速擴展其GPU密集型資料中心的面積,而產業專用的雲端藍圖正在簡化醫療保健、金融和公共部門的合規性。同時,隨著企業尋求工作負載可攜性和成本控制,混合雲端策略的重要性日益凸顯。提供者之間日益激烈的競爭使得多重雲端互通性成為重中之重,而開放的生態系統(而非鎖定)正在成為創造新價值的關鍵驅動力。

全球雲端運算市場趨勢與洞察

SaaS在關鍵業務線軟體領域的爆炸性成長

雲端遷移的應用範圍已從生產力工作負載擴展到業務線的企業資源規劃 (ERP)、客戶關係管理 (CRM) 和財務系統,這一轉變正日益重塑整個雲端運算市場。Delta航空在 2024 年投資 5 億美元用於數位化基礎架構的現代化改造,利用 SaaS 實現人工智慧驅動的個人化服務並提升航班準點率。這一轉變實現了持續的功能更新和嵌入式分析,從而支援即時決策,而這些是本地部署軟體無法實現的。受監管行業由於 SaaS 堆疊中內建的標準化合規控制,審核速度更快,營運成本更低。與優先採用 SaaS 的競爭對手相比,延遲遷移的企業將面臨功能缺失和產品週期延長的風險。

需要彈性運算的生成式人工智慧工作負載激增

訓練大型語言模式需要數千個高頻寬GPU並行運作,遠超過傳統企業工作負載的規模。 OracleOracle為其位於德克薩斯的OpenAI資料中心預訂了價值400億美元的NVIDIA處理器,用於2025年。這種規模將從根本上改變資料中心的供電、冷卻和網路架構設計。供應商正在圍繞AI最佳化晶片、直接液冷和高速互連進行重新設計,以滿足不斷成長的需求。客戶越來越傾向於選擇能夠為突發性AI實驗和生產推理提供容量保證和經濟效益的供應商。

資料本地化法律使全球足跡支離破碎

司法管轄區居住規則迫使服務提供者複製基礎設施並創建獨立的邏輯環境,從而增加成本和營運複雜性。跨國公司在儲存、處理和人員存取方面面臨重疊的義務,這通常迫使它們重新設計架構並提高服務價格。

細分市場分析

平台即服務 (PaaS) 預計將在 2026 年至 2031 年間以 22.85% 的年複合成長率(CAGR)成長,成為所有服務模式中成長最快的。軟體即服務 (SaaS) 將在 2025 年保持其 52.87% 的主導收入佔有率,而基礎設施即服務 (IaaS) 將繼續作為其靈活的底層支撐。 PaaS 浪潮的驅動力來自容器編排管理、無伺服器運行時和低程式碼工具,這些技術將發布週期從數月縮短至數週。亞馬遜已投資 1500 億美元用於以人工智慧為中心的資料中心,以支援這些 PaaS 工作負載。隨著服務供應商透過內建安全和人工智慧服務增強其平台,開發人員可以騰出精力專注於使用者價值,而不是底層架構的維護。

在雲端運算市場,PaaS 供應商正日益透過產業框架和整合的 MLOps 功能來凸顯自身差異化優勢。這些功能能夠加速進階分析的部署,提升程式碼質量,並降低開發人員的工作量。這種組合使 PaaS 成為數位化產品的策略推動者,支援快速實驗和持續交付。

到2025年,私有雲端將佔總營收的46.62%,而混合雲端正以22.24%的複合年成長率快速成長。這種模式既能確保敏感工作負載的資料接近性,又能利用公共雲端的容量進行測試、分析和災害復原。隨著企業在本地基礎設施和外包容量中採用Kubernetes控制平面,混合雲部署的市場規模預計將呈指數級成長。

Oracle和 AWS 的跨雲端協定免除了資料傳輸費用,並使Oracle資料庫能夠在兩個雲端服務供應商之間無縫運作。互通性降低了供應商鎖定風險,並幫助客戶最佳化效能和價格。因此,混合雲策略既是合規性的保障,也是實現現代化的跳板,避免了風險極高的「即拆即遷移」。

雲端運算市場依服務模式(IaaS、PaaS、SaaS)、部署模式(公共雲端、私有雲端、混合雲端)、最終用戶產業(IT與電信、銀行、金融服務和保險、製造業等)、組織規模(大型企業、中小企業)和地區進行細分。市場預測以美元計價。

區域分析

北美地區憑藉其領先雲端運算應用優勢和眾多數位化原生企業的集中度,在2025年貢獻了24.18%的收入。投資仍在繼續:亞馬遜正斥資300億美元在賓州和北卡羅萊納州興建園區,微軟計畫在2025會計年度投入800億美元的資本支出。該地區目前的成長主要圍繞著人工智慧工作負載展開,這需要接近性人才和研究中心。隨著企業為了實現冗餘和成本最佳化而分散工作負載,加拿大和墨西哥也湧現出新的機會。

在歐洲,積極的數位轉型目標與嚴格的資料主權法規之間的平衡正在塑造該地區雲端運算市場的發展軌跡。企業傾向於採用混合架構,將敏感資料保留在本地,同時利用全球雲端進行開發和分析。 OVHcloud 等供應商將歐洲數據居住作為其獨特的賣點。英國脫歐後的地緣政治變化迫使英國企業應對不斷變化的跨境資料協議,這進一步推動了混合架構的普及。

亞太地區是未來的成長引擎,預計複合年成長率將達到21.65%。基礎建設計劃正在快速擴張,Sify計劃在印度投資50億美元建造一座專注於人工智慧的資料中心。阿里雲和騰訊雲等國內巨頭主導中國市場,而國際供應商則將目光投向了日本、韓國、印度以及快速成長的東南亞國協。各國政府都在支持「雲端優先」政策和智慧城市計劃,這加速了對可擴展平台的需求。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- SaaS在關鍵業務線軟體領域的爆炸性成長

- 需要彈性運算的生成式人工智慧工作負載激增

- 產業專用的雲端平台(合規藍圖)

- 歐盟和海灣合作理事會的主權雲授權

- 面向 XR 和自主運作的 10 毫秒以下邊緣雲端區域的興起

- 與範圍 3 目標相關的綠色雲採購標準

- 市場限制

- 數據本地化法律導致全球營運碎片化

- 運作成本高於本地部署的總擁有成本。

- 高等級的半導體出口限制限制了GPU的供應。

- 超大規模資料中心低碳電力短缺

- 供應鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 對影響市場的宏觀經濟因素進行評估

第5章 市場規模與成長預測

- 按服務模式

- IaaS

- PaaS

- SaaS

- 按部署模式

- 公共雲端

- 私有雲端

- 混合雲端

- 按最終用戶行業分類

- 資訊科技和電信

- BFSI

- 製造業

- 零售和消費品

- 醫療保健和生命科學

- 其他

- 按公司規模

- 主要企業

- 中小企業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Amazon(AWS)

- Microsoft

- Google Cloud

- Alibaba Cloud

- IBM

- Oracle

- Salesforce

- SAP SE

- Adobe

- Tencent Cloud

- Huawei Cloud

- Rackspace

- VMware

- Snowflake

- Workday

- ServiceNow

- DigitalOcean

- OVHcloud

- Linode

- Nutanix

第7章 市場機會與未來展望

The Cloud Computing market is expected to grow from USD 0.86 trillion in 2025 to USD 1.04 trillion in 2026 and is forecast to reach USD 2.65 trillion by 2031 at 20.65% CAGR over 2026-2031.

The surge is tied to AI-first digital-transformation agendas, enterprise migration of core applications to Software-as-a-Service (SaaS) platforms, expanding sovereign-cloud rules in Europe and the Gulf, and the rollout of sub-10 millisecond edge-cloud zones that underpin extended-reality (XR) and autonomous-operations use cases. Hyperscale providers are therefore racing to enlarge GPU-rich data-center footprints, while industry-specific cloud blueprints simplify compliance for health, finance, and the public sector. At the same time, hybrid-cloud strategies gain prominence as enterprises seek workload portability and cost discipline. Intensifying competition among providers is pushing multi-cloud interoperability to the forefront, positioning open ecosystems over lock-in as a new source of value creation.

Global Cloud Computing Market Trends and Insights

Explosive SaaS adoption in core enterprise software

Cloud migrations now encompass mission-critical enterprise-resource-planning, customer-relationship-management, and finance systems rather than only productivity workloads, a shift that is increasingly shaping the broader Cloud Computing Market. Delta Air Lines finalized a USD 500 million overhaul of its digital core in 2024, using SaaS to enable AI-driven personalization and punctuality improvements. The pivot delivers continuous feature updates and embedded analytics, unlocking real-time decision-making that on-premises software cannot match. Regulated sectors benefit from standardized compliance controls baked into SaaS stacks, accelerating audits and lowering operational overhead. Organizations delaying migration risk capability gaps and slower product cycles compared with SaaS-first peers

Proliferation of Gen-AI workloads demanding elastic compute

Large-language-model training requires thousands of high-bandwidth GPUs operating in parallel, dwarfing previous enterprise-workload footprints. Oracle reserved USD 40 billion worth of Nvidia processors for a Texas site supporting OpenAI in 2025. Such scale drives radical shifts in data-center power, cooling, and network fabric design. Providers are re-architecting around AI-optimized silicon, direct-liquid cooling, and high-speed interconnects to satisfy growing demand. Customers gravitate toward vendors able to guarantee capacity and favorable economics for bursty AI experiments and production inference.

Data-localization laws fragmenting global footprints

Jurisdiction-specific residency rules compel providers to duplicate infrastructure and create discrete logical environments, adding cost and operational complexity. Multinationals face overlapping obligations on storage, processing, and personnel access, often forcing architectural redesigns and higher service prices.

Other drivers and restraints analyzed in the detailed report include:

- Industry-specific cloud platforms (compliance-ready blueprints)

- Sovereign-cloud mandates in EU and GCC

- Run-rate cost overruns vs on-prem TCO

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Platform-as-a-Service is forecast to compound at 22.85% from 2026-2031, the quickest pace among service models. SaaS retained a commanding 52.87% of 2025 revenue, while Infrastructure-as-a-Service remains the elastic foundation underneath. The PaaS wave is fueled by container orchestration, serverless runtimes, and low-code tools that compress release cycles from months to weeks. Amazon earmarked USD 150 billion for AI-centric data centers catering to those PaaS workloads. As providers enrich platforms with built-in security and AI services, developers gain more freedom to focus on user value rather than plumbing.

In the cloud computing market, PaaS vendors increasingly differentiate through industry frameworks and integrated MLOps. These capabilities shorten deployment of advanced analytics, raise code quality, and reduce developer toil. The combination positions PaaS as a strategic lever for digital products, underpinning rapid experimentation and continuous delivery.

Although private clouds captured 46.62% revenue in 2025, hybrid clouds are expanding at 22.24% CAGR. The model preserves data closeness for sensitive workloads while bursting to public capacity for testing, analytics, and disaster recovery. The cloud computing market size for hybrid deployments is set to rise sharply as firms standardize Kubernetes control planes across on-premises cores and outsourced capacity.

Oracle's cross-cloud pact with AWS eliminates data-egress fees and permits Oracle Database to run seamlessly on either provider. Interoperability curbs vendor-lock fears and lets customers optimize on performance or price. Consequently, the hybrid strategy is viewed as a safety valve for compliance and a springboard for modernization without risky forklift migrations.

Cloud Computing Market is Segmented by Service Model (IaaS, Paas, Saas). Deployment Model (Public Cloud, Private Cloud, Hybrid Cloud), End User Vertical (IT and Telecom, BFSI, Manufacturing, and More), Organization Size (Large Enterprises, Small and Mid-Sized Enterprises (SMEs)) and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 24.18% of 2025 revenue thanks to an early lead in cloud adoption and dense clusters of digital-native enterprises. Investment continues: Amazon is channeling USD 30 billion into Pennsylvania and North Carolina campuses, while Microsoft plans USD 80 billion in fiscal-year 2025 capacity. Growth in the region now pivots around AI workloads that demand proximity to talent and research hubs. Canada and Mexico open incremental opportunities as firms spread workloads for redundancy and cost optimization.

Europe balances aggressive digital-transformation targets with stringent data-sovereignty rules, shaping the region's trajectory within the Cloud Computing Market. Organizations favor hybrid architectures that keep sensitive data local yet leverage global clouds for development and analytics. Providers such as OVHcloud emphasize European data residency as a unique selling point. Geopolitical shifts post-Brexit compel UK businesses to navigate evolving cross-border data agreements, further reinforcing hybrid adoption.

Asia-Pacific is the engine of future expansion, with a projected 21.65% CAGR. Infrastructure projects scale rapidly: Sify will invest USD 5 billion in Indian AI-focused data centers. Domestic champions such as Alibaba Cloud and Tencent Cloud dominate China, while international providers target Japan, South Korea, India, and fast-growing ASEAN states. Governments back cloud-first policies and smart-city programs, accelerating demand for scalable platforms.

- Amazon (AWS)

- Microsoft

- Google Cloud

- Alibaba Cloud

- IBM

- Oracle

- Salesforce

- SAP SE

- Adobe

- Tencent Cloud

- Huawei Cloud

- Rackspace

- VMware

- Snowflake

- Workday

- ServiceNow

- DigitalOcean

- OVHcloud

- Linode

- Nutanix

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosive SaaS adoption in core enterprise software

- 4.2.2 Proliferation of Gen-AI workloads demanding elastic compute

- 4.2.3 Industry-specific cloud platforms (compliance-ready blueprints)

- 4.2.4 Sovereign-cloud mandates in EU and GCC

- 4.2.5 Rise of less than 10 ms edge-cloud zones for XR and autonomous ops

- 4.2.6 Green-cloud buying criteria tied to Scope-3 targets

- 4.3 Market Restraints

- 4.3.1 Data-localisation laws fragmenting global footprints

- 4.3.2 Run-rate cost overruns vs on-prem TCO

- 4.3.3 Advanced chip export controls limiting GPU supply

- 4.3.4 Scarcity of low-carbon power for hyperscale DCs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Assesment of Macroeconomic Factors on the market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Model

- 5.1.1 IaaS

- 5.1.2 PaaS

- 5.1.3 SaaS

- 5.2 By Deployment Model

- 5.2.1 Public Cloud

- 5.2.2 Private Cloud

- 5.2.3 Hybrid Cloud

- 5.3 By End-user Vertical

- 5.3.1 IT and Telecom

- 5.3.2 BFSI

- 5.3.3 Manufacturing

- 5.3.4 Retail and Consumer Goods

- 5.3.5 Healthcare and Life Sciences

- 5.3.6 Others

- 5.4 By Organisation Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Mid-Sized Enterprises (SMEs)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Southeast Asia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.5.2.5 Egypt

- 5.5.5.2.6 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amazon (AWS)

- 6.4.2 Microsoft

- 6.4.3 Google Cloud

- 6.4.4 Alibaba Cloud

- 6.4.5 IBM

- 6.4.6 Oracle

- 6.4.7 Salesforce

- 6.4.8 SAP SE

- 6.4.9 Adobe

- 6.4.10 Tencent Cloud

- 6.4.11 Huawei Cloud

- 6.4.12 Rackspace

- 6.4.13 VMware

- 6.4.14 Snowflake

- 6.4.15 Workday

- 6.4.16 ServiceNow

- 6.4.17 DigitalOcean

- 6.4.18 OVHcloud

- 6.4.19 Linode

- 6.4.20 Nutanix

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

2026-2030年全球政府部門雲端運算市場

2026-2030年全球政府部門雲端運算市場 2026-2031年全球雲端運算市場預測

2026-2031年全球雲端運算市場預測 日本雲端運算市場,2026-2030年

日本雲端運算市場,2026-2030年 雲端運算在臨床試驗市場的應用:按服務模式、試驗階段、部署模式、應用程式和最終用戶分類的全球預測(2026-2032 年)

雲端運算在臨床試驗市場的應用:按服務模式、試驗階段、部署模式、應用程式和最終用戶分類的全球預測(2026-2032 年) Cerebras Systems公司:全球WSE/CS部署分析主權雲端市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察與預測(2026-2034)

Cerebras Systems公司:全球WSE/CS部署分析主權雲端市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察與預測(2026-2034) 2025年全球自託管雲端平台市場報告

2025年全球自託管雲端平台市場報告 雲端運算市場規模、佔有率和趨勢分析:按服務、部署類型、工作負載、企業規模、最終用途、地區和細分市場預測(2026-2033 年)

雲端運算市場規模、佔有率和趨勢分析:按服務、部署類型、工作負載、企業規模、最終用途、地區和細分市場預測(2026-2033 年) 雲端運算市場-全球產業規模、佔有率、趨勢、機會和預測,按服務、部署方式、應用程式類型、最終用戶、地區和競爭格局分類,2020-2030 年預測

雲端運算市場-全球產業規模、佔有率、趨勢、機會和預測,按服務、部署方式、應用程式類型、最終用戶、地區和競爭格局分類,2020-2030 年預測 雲端運算市場:按服務、部署方式、企業規模、工作負載、最終用途、技術類型、國家分類 - 全球產業分析、市場規模、市場佔有率及2025-2032年預測

雲端運算市場:按服務、部署方式、企業規模、工作負載、最終用途、技術類型、國家分類 - 全球產業分析、市場規模、市場佔有率及2025-2032年預測