|

市場調查報告書

商品編碼

1934830

新加坡電信行動網路業者:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Singapore Telecom MNO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

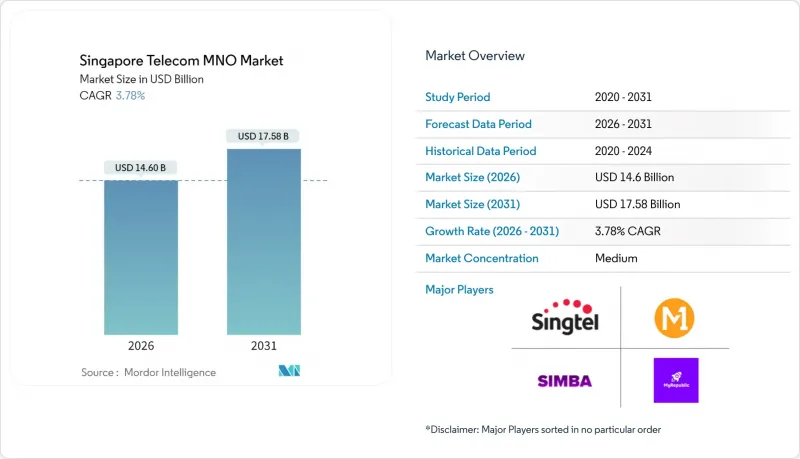

預計新加坡電信行動網路營運商 (MNO) 市場將從 2025 年的 140.7 億美元成長到 2026 年的 146 億美元,到 2031 年將達到 175.8 億美元,2026 年至 2031 年的複合年成長率為 3.78%。

就用戶數量而言,預計市場將從2025年的1009萬成長到2030年的1169萬,在預測期(2025-2030年)內複合年成長率低於2.98%。這一穩步成長的趨勢得益於強力的基礎設施投資、覆蓋全國的5G獨立組網以及積極的雲端優先公共舉措,這些因素共同推動了企業需求,同時保持了高階消費者的升級需求。住宅光纖普及率已達100%,使業者能夠將Gigabit級寬頻與5G行動套餐捆綁銷售,支援平均每月超過50GB的行動數據流量。政府和工業領域的數位化加速,推動了對安全、高容量連接的需求,通訊業者正透過網路切片產品來滿足關鍵任務工作負載的需求,並提供人工智慧驅動的網路安全套餐來應對這一需求。來自Simba和其他十多家行動虛擬網路營運商(MVNO)日益激烈的競爭,已將新加坡的資料通訊速率推至東南亞最低水平之列,但謹慎的資本支出週期和新的企業收入來源幫助維持了利潤率。透過針對海事和港口用途的專用網路試驗以及對雲端邊緣部署的積極投資,新加坡電信行動網路營運商(MNO)市場正將自身打造成為工業5G應用案例的區域典範。

新加坡電信行動網路營運商市場趨勢與洞察

全國範圍內的5G獨立組網部署和網路切片

2025年,新加坡成為全球首個在所有人口密集區域實現5G獨立組網覆蓋的國家,賦予通訊業者架構上的自由度,可為對延遲敏感的流量分配專用網路切片。新加坡電信的700MHz頻寬將室內覆蓋率提升40%,同時以遠低於一般行動套餐的成本實現超低頻寬的物聯網網路切片,從而拓展了目標企業應用場景。網路切片技術也為高階消費者「5G+」套餐提供了支撐,確保尖峰時段的頻寬,預計到2025年,早期採用者的平均每用戶收入(ARPU)將提升23%。

數位化優先的公共部門措施和雲端遷移

2024年底,超過80%的政府系統將運作在商業雲端平台。這一里程碑事件立即提升了政府機構及其供應商對安全連接的需求。 2024年12月推出的「共享責任架構」鼓勵金融機構與通訊業者在網路釣魚防範方面開展進一步的合作創新,並在合規主導的通訊和API安全領域創造新的收入來源。

來自虛擬營運商和Simba的激烈競爭

Simba 的「50GB 10 新元套餐」重塑了消費者對價格的預期,幫助這家第四大通訊業者在 2024 年實現超過 10% 的用戶佔有率。由於有超過 10 家 MVNO 瞄準微型用戶群體,解約率每月超過 1.7%,這限制了任何營運商在無線存取能源成本不斷上漲的情況下提高標價的空間。

細分市場分析

到2025年,數據產品將佔新加坡電信行動網路營運商(MNO)市場佔有率的52.64%,這反映了行動寬頻的廣泛普及和100%的住宅光纖接入。物聯網(IoT)和機器對機器(M2M)通訊將以3.94%的複合年成長率(CAGR)領跑,這主要得益於智慧工廠試點專案和城市級感測器網路對超可靠、低延遲連接的需求。語音服務將佔19.74%,但隨著OTT服務持續萎縮,其成長速度將會放緩。 OTT和付費電視將佔10.08%,其中串流媒體套餐將帶來溫和成長。其他附加價值服務,包括託管安全和GPU即服務,將成長3.88%,因為營運商正在實現收入來源多元化。這種多元化表明,新加坡電信行動網路營運商市場的規模越來越與企業數位轉型預算掛鉤,而非傳統的消費者語音服務趨勢。

競爭格局正在推動服務融合。通訊業者將無限流量的純SIM卡套餐與2Gbps家庭寬頻和雲端儲存捆綁銷售,價格與2019年單獨購買這些產品的價格相同,推動了多產品組合的普及率超過65%。從大士港的自動導引運輸車到樟宜機場的AR引導飛機檢查,預計到2031年,工業5G應用案例將帶來3.4億美元的新增業務收益,進一步鞏固了向高收益平台服務的結構性轉變。

新加坡電信行動網路營運商 (MNO) 市場按服務類型(語音服務、數據及網際網路服務、通訊服務、物聯網及機器對機器 (IoT & M2M) 服務、OTT 及付費電視服務、其他服務)及最終用戶(企業、消費者)進行細分。市場預測以價值(美元)和用戶數量(用戶數)為單位。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 監理與政策框架

- 當前競爭格局中的頻寬狀況和擁有情形

- 通訊業生態系統

- 宏觀經濟與外在因素

- 波特五力模型

- 競爭對手之間的競爭

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 領先行動網路營運商的關鍵績效指標(2020-2025)

- 獨立行動用戶和滲透率

- 行動網路使用者數量和普及率

- 按接入技術分類的SIM卡連線數和滲透率

- 蜂巢式物聯網/M2M連接

- 寬頻連線(移動和固定)

- ARPU(每位用戶平均收入)

- 每用戶平均數據使用量(GB/月)

- 市場促進因素

- 全國獨立的組網 5G 部署將支援高階消費者和企業應用場景

- 加強公共部門的數位化優先措施將推動安全、高容量連接的需求。

- 光纖到府 (FTTH) 部署的快速普及使得提供Gigabit級配套服務成為可能。

- 行動數據人均消耗量的快速成長(每月超過50GB)推動了ARPU值的成長。

- 私營海事和港口網路試點計畫推動工業界採用 5G 技術(低調進行)

- 針對遊戲玩家和金融科技用戶的 5G 網路切片(優先通道)將創造新的 B2C 獲利機會(但關注度較低)。

- 市場限制

- 來自虛擬營運商和第四家行動網路營運商(Simba)的過度競爭導致消費者價格彈性居高不下。

- OTT服務的興起正在蠶食傳統語音/簡訊和付費電視的收入。

- 高昂的頻譜續費和能源成本對EBITDA獲利率帶來壓力。

- 國內市場規模有限,限制了5G獨立組網的規模經濟效益,而5G獨立組網則需要大量的資本投資(低利率)。

- 技術展望

- 電信業主要經營模式分析

- 定價模型和定價分析

第5章 市場規模與成長預測

- 通訊總收入和每位用戶平均收入

- 服務類型

- 語音服務

- 數據和網際網路服務

- 通訊服務

- 物聯網和機器對機器服務

- OTT和付費電視服務

- 其他服務(附加價值服務、漫遊/國際服務、企業/批發服務等)

- 最終用戶

- 公司

- 一般消費者

第6章 競爭情勢

- 市場集中度

- 主要供應商的策略與投資動向(2023-2025)

- 2024年行動網路營運商市場佔有率分析

- MNO snapshot(subscribers, churn rate, ARPU, etc.)

- 行動網路營運商公司簡介*

- Singtel

- M1(Keppel)

- Simba Telecom

- MyRepublic

第7章 市場機會與未來展望

The Singapore Telecom MNO Market is expected to grow from USD 14.07 billion in 2025 to USD 14.6 billion in 2026 and is forecast to reach USD 17.58 billion by 2031 at 3.78% CAGR over 2026-2031.

In terms of subscriber volume, the market is expected to grow from 10.09 million units in 2025 to 11.69 million units by 2030, at a CAGR of less than 2.98% during the forecast period (2025-2030). This steady trajectory reflects resilient infrastructure investment, nationwide 5G standalone coverage, and aggressive cloud-first public initiatives that jointly lift enterprise demand while sustaining premium consumer upgrades. Household fiber penetration sits at 100%, enabling operators to bundle gigabit-class broadband with 5G mobile tiers, which in turn supports average monthly mobile data consumption above 50 GB. Intensifying digitalization across government and industry pushes demand for secure, high-capacity connectivity, and operators are responding with network-slicing products for mission-critical workloads and AI-enabled cybersecurity bundles. Competitive tension, sparked by the entry of Simba and more than ten MVNOs, has driven data prices to the lowest level in Southeast Asia, yet prudent capex cycles and new enterprise revenue streams help sustain margins. Maritime and port private-network pilots, plus aggressively funded cloud-edge rollouts, position the Singapore MNO telecom market as a regional showcase for industrial 5G use cases.

Singapore Telecom MNO Market Trends and Insights

Nationwide 5G standalone roll-out with network slicing

Singapore became the first country to blanket all populated areas with 5G standalone in 2025, giving operators the architectural freedom to allocate dedicated slices for latency-sensitive traffic. Singtel's 700 MHz layer lifted indoor coverage by 40% while permitting ultra-low-bandwidth IoT slices that cost only a fraction of regular mobile plans, expanding addressable enterprise use cases. Network slicing also underpins premium consumer "5G +" bundles that guarantee bandwidth during peak hours, generating a 23% ARPU uplift among early adopters in 2025

Digital-first public-sector initiatives and cloud migration

More than 80% of eligible government systems ran on the commercial cloud by late-2024, a milestone that immediately multiplied secure connectivity demand from agencies and their vendors. The Shared Responsibility Framework launched in December 2024 further compels financial institutions to co-innovate with telecom operators on anti-phishing defenses, spawning new compliance-driven messaging and API-security revenues.

Hyper-competition from MVNOs and Simba

Simba's SGD 10-for-50 GB plan re-anchored consumer price expectations and helped the fourth operator exceed 10% subscriber share by 2024. With more than ten MVNOs targeting micro-segments, churn has risen above 1.7% monthly, curbing the ability of any provider to push list prices upward despite rising radio-access energy costs.

Other drivers and restraints analyzed in the detailed report include:

- Full fiber-to-the-home saturation enabling 10 Gbps upgrades

- Surging per-capita mobile data use (>50 GB monthly)

- OTT substitution of voice/SMS and Pay-TV

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Data products commanded 52.64% of Singapore telecom MNO market share in 2025, reflecting ubiquitous mobile broadband adoption and 100% household fiber access. IoT and M2M posted the highest 3.94% CAGR, fueled by smart-factory pilots and city-wide sensor grids that demand ultrareliable low-latency connectivity. Voice held 19.74% yet lagged in growth as OTT erosion persisted. OTT and PayTV represented 10.08%, bolstered modestly by streaming bundles. Other value-added services including managed security and GPU-as-a-Service grew at 3.88% as operators diversified revenue. This breadth underscores how the Singapore MNO telecom market size increasingly tracks enterprise digital-transformation budgets rather than legacy consumer voice trends.

The competitive configuration encourages convergence. Operators package unlimited-data SIM-only plans with 2 Gbps home broadband and cloud storage at price points equal to 2019 single surfaces, driving multi-product take-rates above 65%. Industrial 5G use cases from automated guided vehicles at Tuas Port to AR-guided aircraft checks at Changi are projected to inject USD 340 million incremental service revenue by 2031, reinforcing the structural pivot toward high-margin platform services.

The Singapore Telecom MNO Market is Segmented by Service Type (Voice Services, Data and Internet Services, Messaging Services, Iot and M2M Services, OTT and PayTV Services, and Other Services), and End User (Enterprises, Consumer). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Subscribers).

List of Companies Covered in this Report:

- Singtel

- M1 (Keppel)

- Simba Telecom

- MyRepublic

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 Market Landscape

- 4.1 Market Overview

- 4.2 Regulatory And Policy Framework

- 4.3 Spectrum Landscape And Competitive Holdings

- 4.4 Telecom Industry Ecosystem

- 4.5 Macroeconomic And External Drivers

- 4.6 Porter's Five Forces

- 4.6.1 Competitive Rivalry

- 4.6.2 Threat of New Entrants

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Bargaining Power of Buyers

- 4.6.5 Threat of Substitutes

- 4.7 Key MNO KPIs (2020-2025)

- 4.7.1 Unique Mobile Subscribers And Penetration Rate

- 4.7.2 Mobile Internet Users And Penetration Rate

- 4.7.3 SIM Connections by Access Technology And Penetration

- 4.7.4 Cellular IoT / M2M Connections

- 4.7.5 Broadband Connections (Mobile And Fixed)

- 4.7.6 ARPU (Average Revenue Per User)

- 4.7.7 Average Data Usage per Subscription (GB/month)

- 4.8 Market Drivers

- 4.8.1 Nationwide Stand-alone 5G roll-out unlocks premium consumer and enterprise use-cases

- 4.8.2 Intensifying digital-first public-sector initiatives driving secure high-capacity connectivity demand

- 4.8.3 Rapid fibre-to-the-home (FTTH) saturation enabling gigabit-class bundled offers

- 4.8.4 Surging mobile data consumption per-capita (>50 GB/mo) supports ARPU uplift

- 4.8.5 Maritime And port private-network pilots catalyse Industrial 5G adoption (UNDER-RADAR)

- 4.8.6 5G network-slicing -priority lanes- for gamers And fintech users creates new B2C monetisation (UNDER-RADAR)

- 4.9 Market Restraints

- 4.9.1 Hyper-competition from MVNOs And fourth MNO (Simba) keeps consumer price elasticity high

- 4.9.2 OTT substitution erodes legacy voice/SMS and Pay-TV revenues

- 4.9.3 High spectrum-renewal And energy costs compress EBITDA margins

- 4.9.4 Limited domestic market size caps scale economics for heavy-capex 5G standalone (UNDER-RADAR)

- 4.10 Technological Outlook

- 4.11 Analysis of key business models in Telecom

- 4.12 Analysis of Pricing Models and Pricing

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 Overall Telecom Revenue and ARPU

- 5.2 Service Type

- 5.2.1 Voice Services

- 5.2.2 Data and Internet Services

- 5.2.3 Messaging Services

- 5.2.4 IoT and M2M Services

- 5.2.5 OTT and PayTV Services

- 5.2.6 Other Services (VAS, Roaming & International Services, Enterprise And Wholesale Services, etc.)

- 5.3 End-user

- 5.3.1 Enterprises

- 5.3.2 Consumer

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Investments by key vendors, 2023-2025

- 6.3 Market share analysis for MNOs, 2024

- 6.4 MNO snapshot (subscribers, churn rate, ARPU, etc.)

- 6.5 Company Profiles* of MNOs (Includes Business Overview | Service Portfolio | Financials | Business Strategy and Recent Developments | SWOT Analysis)

- 6.5.1 Singtel

- 6.5.2 M1 (Keppel)

- 6.5.3 Simba Telecom

- 6.5.4 MyRepublic

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space And Unmet-Need Assessment

行動虛擬網路啟用器市場規模、佔有率和趨勢分析報告:按服務類型、部署模式、最終用戶產業、地區和細分市場預測(2026-2033 年)行動虛擬網路聚合器市場規模、佔有率和趨勢分析報告:按服務、最終用途、地區和細分市場分類(2026-2033 年)

行動虛擬網路啟用器市場規模、佔有率和趨勢分析報告:按服務類型、部署模式、最終用戶產業、地區和細分市場預測(2026-2033 年)行動虛擬網路聚合器市場規模、佔有率和趨勢分析報告:按服務、最終用途、地區和細分市場分類(2026-2033 年) 全球行動虛擬網路營運商(MVNO)市場規模、佔有率、趨勢和成長分析報告(2026-2034年)虛擬行動服務業者(MVNO) 市場:市場規模、佔有率和趨勢分析(按類型、商業模式、服務類型、合約類型、最終用途和地區分類),細分市場預測(2026-2033 年)

全球行動虛擬網路營運商(MVNO)市場規模、佔有率、趨勢和成長分析報告(2026-2034年)虛擬行動服務業者(MVNO) 市場:市場規模、佔有率和趨勢分析(按類型、商業模式、服務類型、合約類型、最終用途和地區分類),細分市場預測(2026-2033 年) 行動虛擬網路營運商 (MVNO) 市場:2026-2032 年全球市場預測(按服務類型、費率方案、銷售管道、最終用戶產業和應用程式分類)5G MVNO市場:按套餐類型、最終用戶、設備類型、銷售管道、產業和網路類型分類-2026-2032年全球市場預測

行動虛擬網路營運商 (MVNO) 市場:2026-2032 年全球市場預測(按服務類型、費率方案、銷售管道、最終用戶產業和應用程式分類)5G MVNO市場:按套餐類型、最終用戶、設備類型、銷售管道、產業和網路類型分類-2026-2032年全球市場預測 2026年全球行動虛擬網路營運商(MVNO)市場報告

2026年全球行動虛擬網路營運商(MVNO)市場報告 行動虛擬網路營運商 (MVNO) 市場規模、佔有率、趨勢和預測:按類型、商業模式、服務類型、用戶數量和地區分類,2026-2034 年

行動虛擬網路營運商 (MVNO) 市場規模、佔有率、趨勢和預測:按類型、商業模式、服務類型、用戶數量和地區分類,2026-2034 年 行動虛擬網路營運商 (MVNO) 市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、解決方案和功能分類

行動虛擬網路營運商 (MVNO) 市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、解決方案和功能分類 亞太地區行動虛擬網路營運商(MVNO):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

亞太地區行動虛擬網路營運商(MVNO):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)