|

市場調查報告書

商品編碼

1934775

智慧追蹤器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Smart Tracker - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

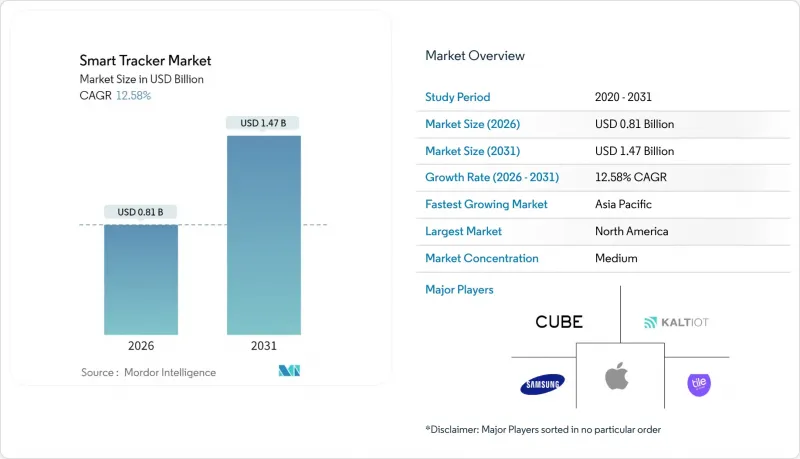

智慧追蹤器市場預計將從 2025 年的 7.2 億美元成長到 2026 年的 8.1 億美元,預計到 2031 年將達到 14.7 億美元,2026 年至 2031 年的複合年成長率為 12.58%。

智慧型手機的快速普及、超寬頻 (UWB) 高精度測距技術以及與智慧家庭生態系統的整合,正在拓展追蹤器的應用場景,使其從失物找回擴展到醫療保健和企業資產管理。消費者越來越將追蹤器視為避免時間損失、壓力和生產力下降的低成本保障,而企業則認為即時可見性和降低合規成本是採用追蹤器的理由。供應商之間的差異不僅體現在硬體上,也體現在其生態系統的廣度上。例如,蘋果的「查找我的」和三星的「SmartThings」利用網路效應來提高定位精度和覆蓋範圍。同時,監管機構強制執行的隱私保護措施推高了開發成本,並有助於建立人們對資料密集型服務的信任。

全球智慧追蹤器市場趨勢與洞察

超寬頻 (UWB) 和低功耗藍牙 (Bluetooth LE) 技術的快速發展

超寬頻 (UWB) 技術使追蹤器從近距離通知發展到公分級精度,從而實現了室內導航和高價值資產的監控。蘋果已在其 AirTag 更新中整合了第二代 UWB 晶片,三星公司也已將其整合到 Galaxy 裝置的 SmartTag 2 中,進一步推動了 UWB 技術的普及。 FiRa 聯盟的互通性規範正在消除傳統的碎片化問題,使工廠和醫院等企業先導計畫更具可行性。同時,藍牙低功耗 (Bluetooth LE) 技術的進步使電池壽命延長了兩年以上,在理想條件下傳輸距離超過 100 公尺。這些通訊協定共同實現了多重通訊協定協定設備,這些設備可以無縫切換到最高效的無線電,從而降低了設備擁有成本,並擴大了智慧追蹤器市場的潛在基本客群。

智慧型手機日益普及,使其能夠進行追蹤和監控

每部新智慧型手機實際上都成為了全球群眾外包定位網路中的一個節點。蘋果的「尋找我的設備」功能覆蓋超過10億台設備,三星的SmartThings網路也不斷擴展,覆蓋安卓設備。售價低於100美元的安卓設備正在幫助印度、奈及利亞和印尼的用戶初步連接到網際網路,從而顯著提高了追蹤器訊號的接收機率。網路外部性提升了追蹤器的效用。智慧型手機的普及縮短了尋找遺失物品所需的時間,吸引了更多用戶加入這個生態系統。行動網路業者意識到流量商機的商機,正將追蹤服務捆綁到5G物聯網套餐中。 Verizon的車隊追蹤服務就是一個典型的例子。

資料隱私和網路追蹤問題

諸如GDPR之類的法規要求用戶明確同意並盡可能縮短資料保存,這使得全球範圍內的群眾外包定位技術變得複雜。針對AirTags可能被濫用的追蹤行為,蘋果和谷歌推出了定期發出蜂鳴聲、輪換識別碼以及自動通知附近用戶等措施。雖然這些措施有助於建立信任,但也縮短了電池續航時間並降低了位置更新的準確性,從而略微降低了使用者體驗。網際網路工程任務小組(IETF)正在進行關於惡意追蹤偵測通訊協定的工作,旨在統一各廠商的因應措施,但合規性工作會增加開發成本,並減緩智慧追蹤器市場的功能部署速度。

細分市場分析

截至2025年,藍牙在智慧追蹤器市場保持了54.10%的佔有率,並與幾乎所有現代智慧型手機和智慧型手錶相容。超寬頻(UWB)作為一項新興技術,正以13.02%的複合年成長率快速成長,因為消費者願意為10厘米以下的定位精度買單,以便在家具底下或擁擠的倉庫中定位物品。 GPS和蜂窩網路技術則主要針對行動電話覆蓋不佳的戶外資產追蹤,以更高的電力消耗為代價換取全球覆蓋。整合藍牙、UWB和GPS的多重通訊協定晶片組如今已成為高級產品設計的主流,使裝置能夠根據實際情況切換無線連接方式,從而節省電池電量。

隨著UWB晶片實現規模經濟,平均售價呈下降趨勢,這促使中端廠商更多地採用通訊協定。然而,藍牙仍然是大規模生產的基礎技術,尤其是在新興經濟體,而價格親民的行動電話正在推動UWB技術的初期普及。企業先導計畫擴大將UWB和藍牙技術結合使用,以實現面向未來的部署,從而推動了該技術在智慧追蹤器市場的成長。

區域分析

到2025年,北美將佔據智慧追蹤器市場37.10%的佔有率,這主要得益於成熟的智慧型手機生態系統、高收入消費者以及支援高更新頻率的5G網路部署。美國法規在隱私和創新之間取得了平衡,從而促進了功能的快速改進。企業需求涵蓋車隊管理物流、醫療資產追蹤以及保險公司主導的損失預防項目。

亞太地區預計將成為全球成長最快的地區,到2031年複合年成長率將達到13.55%。印度和中國每年新增數百萬智慧型手機用戶,提高了網路密度和追蹤器的精準度。政府主導的智慧城市示範計畫正在為物聯網感測器提供資金,以支持公共和老年護理。日本的超老齡化社會預計到2040年將出現57萬名看護者的缺口,這正在加速醫療和家庭監測領域的應用。在東南亞,電子商務的成長進一步推動了對包裹追蹤的需求,增強了全部區域智慧追蹤器市場的發展勢頭。

歐洲保持溫和成長,這得益於嚴格的《一般資料保護規則》(GDPR)保障措施,這些措施增強了使用者對資料密集型服務的信任。成員國之間標準的協調統一簡化了跨境物流追蹤。隨著電信基礎設施的現代化,中東和非洲地區率先採用了智慧追蹤器,但射頻(RF)組件的進口關稅抑制了其高階價格。在南美洲,匯率波動導致設備成本上升,構成了一項挑戰,但都市區的安全顧慮正在推動中產階級消費者對追蹤器的接受度。各大洲成熟市場和新興市場並存的格局,為智慧追蹤器市場維持了平衡的全球前景。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 智慧型手機日益普及,使其能夠進行追蹤和監控

- 個人物品遺失案件增多

- 超寬頻 (UWB) 和低功耗藍牙 (Bluetooth LE) 技術的快速發展

- 低功耗無線晶片組的平均售價正在下降。

- 將追蹤器整合到多重通訊協定智慧家庭生態系統中

- 行動網路業者擴大物品追蹤服務

- 市場限制

- 缺乏全球互通性標準

- 對資料隱私和網路追蹤的擔憂

- 由於產品壽命縮短,電子廢棄物增加

- 新興市場關鍵射頻元件的進口關稅

- 產業價值鏈分析

- 宏觀經濟因素的影響

- 技術展望

- 智慧家庭物聯網整合趨勢

- 監管環境

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 投資分析

第5章 市場規模與成長預測

- 透過技術

- 行動電話

- Bluetooth

- GPS

- UWB

- NFC

- 透過使用

- 個人物品追蹤服務

- 行李追蹤服務

- 寵物追蹤

- 兒童和老年人的安全措施

- 企業庫存管理和資產追蹤

- 車輛追蹤

- 最終用戶

- 消費者

- 商業的

- 工業與物流

- 衛生保健

- 政府/國防

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 東南亞

- 亞太其他地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 肯亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Tile Inc.

- Samsung Electronics Co., Ltd.

- Apple Inc.

- Cube Tracker Inc.

- Kaltio Technologies Oy

- PB Inc.(Pebblebee)

- Chipolo doo

- XY Labs, Inc.

- Garmin Ltd.

- Jiobit Inc.

- Invoxia SA

- HButler International Pty. Ltd.(Orbit)

- Wistiki SAS

- Nut Technology Co., Ltd.

- Filo Srl

- Satotech Limited(TagoBee)

- Trackimo Inc.

- Loc8tor Ltd.

- Rinex Technology Co., Ltd.

第7章 市場機會與未來展望

The smart tracker market is expected to grow from USD 0.72 billion in 2025 to USD 0.81 billion in 2026 and is forecast to reach USD 1.47 billion by 2031 at 12.58% CAGR over 2026-2031.

Rapid smartphone penetration, ultra-wideband (UWB) precision ranging, and integration with smart-home ecosystems are expanding use cases from lost-item recovery to healthcare and enterprise asset management. Consumers increasingly view trackers as inexpensive insurance against time, stress, and productivity losses, while enterprises justify deployments through real-time visibility and regulatory compliance savings. Vendors differentiate through ecosystem breadth rather than hardware alone, as Apple's Find My and Samsung's SmartThings leverage network effects to boost location accuracy and coverage. Meanwhile, privacy safeguards mandated by regulators keep development costs elevated but also build trust in data-rich services.

Global Smart Tracker Market Trends and Insights

Rapid Advancements in Ultra-Wideband and Bluetooth LE Technologies

UWB has shifted trackers from proximity alerts to centimeter-level precision, enabling indoor navigation and high-value asset monitoring. Apple embedded second-generation UWB chips in AirTag updates, while Samsung integrated UWB into SmartTag 2 for Galaxy devices, signaling mainstream adoption. The FiRa Consortium's interoperability profiles address earlier fragmentation, making enterprise pilots viable for factories and hospitals. Parallel gains in Bluetooth LE lengthen battery life beyond two years and push range past 100 meters in ideal conditions. Together, these protocols unlock multiprotocol devices that switch seamlessly to the most efficient radio, reducing cost of ownership and widening the addressable base for the smart tracker market.

Growing Penetration of Smartphones Enabling Tracking and Monitoring

Each new smartphone effectively becomes a node in a global crowd-sourced location network. Apple's Find My spans more than 1 billion devices, and Samsung's SmartThings network continues to grow across Android hardware. Affordable sub-USD 100 Android handsets ignite first-time internet access across India, Nigeria, and Indonesia, multiplying potential tracker pings. Network externalities elevate tracker utility: denser smartphone clusters shorten the time to locate a lost item, which in turn pulls more users into the ecosystem. Mobile network operators recognize the traffic-driven revenue opportunity and now bundle tracking services into 5G IoT plans, exemplified by Verizon's fleet offerings.

Data-Privacy and Cyber-Stalking Concerns

Regulations such as GDPR require explicit consent and minimal data retention, complicating global crowd-location features. Following reports of AirTags enabling unauthorized tracking, Apple and Google introduced periodic beeps, rotating identifiers, and automatic notifications to nearby users. These measures build trust but reduce battery life and granularity of location updates, slightly dampening user experience. Ongoing IETF work on unwanted-tracking detection protocols aims to standardize mitigations across vendors, but compliance increases development cost and slows feature rollouts in the smart tracker market.

Other drivers and restraints analyzed in the detailed report include:

- Integration of Trackers into Multiprotocol Smart-Home Ecosystems

- Rising Incidences of Misplaced Personal Items

- Lack of Global Interoperability Standards

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bluetooth retained 54.10% smart tracker market share in 2025, aligned with nearly every modern smartphone and smartwatch. UWB, although nascent, is accelerating at a 13.02% CAGR as consumers pay for sub-10-centimeter precision that pinpoints items under furniture or within crowded warehouses. GPS and cellular variants target outdoor asset tracking where phone density is sparse, accepting higher power draw in exchange for global reach. Multiprotocol chipsets combining Bluetooth, UWB, and GPS now dominate premium product designs, letting devices switch radios based on context to conserve battery.

As UWB chips reach economies of scale, average selling prices are falling, encouraging mid-tier vendors to include the protocol. Nevertheless, Bluetooth remains the volume cornerstone, especially in emerging economies where affordable phones anchor initial adoption. Enterprise pilots increasingly specify UWB plus Bluetooth to future-proof deployments, reinforcing the technology's climb within the smart tracker market.

The Smart Tracker Market Report is Segmented by Technology (Cellular, Bluetooth, GPS, UWB, and NFC), Application (Personal Item Tracking, Luggage Tracking, Pet Tracking, Kids and Senior Safety, Enterprise Inventory and Asset Tracking, and Vehicle Tracking), End User (Consumer, Commercial, Industrial and Logistics, Healthcare, and Government and Defense), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 37.10% smart tracker market share in 2025, buoyed by mature smartphone ecosystems, affluent consumers, and 5G rollouts that support high update frequencies. U.S. regulations strike a balance between privacy and innovation, allowing rapid feature iterations. Enterprise demand spans fleet logistics, healthcare asset tracking, and insurance-sponsored loss-prevention programs.

Asia Pacific is projected to log a 13.55% CAGR through 2031, the fastest worldwide. India and China add millions of first-time smartphone users annually, elevating network density and tracker accuracy. Government-backed smart city pilots allocate funding for IoT sensors, supporting public safety and elderly care. Japan's super-aged society drives healthcare and home-monitoring deployments as the nation grapples with a forecast 570,000 caregiver shortfall by 2040. Southeast Asian e-commerce growth further increases parcel-tracking demand, reinforcing region-wide momentum in the smart tracker market.

Europe maintains moderate expansion, aided by stringent GDPR safeguards that engender user trust in data-heavy services. Standards harmonization across member states simplifies cross-border logistics tracking. Middle East and Africa witness early-stage adoption tied to telecom infrastructure modernization, though import tariffs on RF components temper premium pricing. South America faces currency fluctuations that raise device costs, but urban safety concerns propel tracker uptake among middle-class consumers. The blend of mature and emerging scenarios across continents preserves a balanced global outlook for the smart tracker market.

- Tile Inc.

- Samsung Electronics Co., Ltd.

- Apple Inc.

- Cube Tracker Inc.

- Kaltio Technologies Oy

- PB Inc. (Pebblebee)

- Chipolo d.o.o.

- XY Labs, Inc.

- Garmin Ltd.

- Jiobit Inc.

- Invoxia SA

- HButler International Pty. Ltd. (Orbit)

- Wistiki SAS

- Nut Technology Co., Ltd.

- Filo S.r.l.

- Satotech Limited (TagoBee)

- Trackimo Inc.

- Loc8tor Ltd.

- Rinex Technology Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing penetration of smartphones enabling tracking and monitoring

- 4.2.2 Rising incidences of misplaced personal items

- 4.2.3 Rapid advancements in ultra-wideband and Bluetooth LE technologies

- 4.2.4 Declining average selling prices of low-power wireless chipsets

- 4.2.5 Integration of trackers into multiprotocol smart-home ecosystems

- 4.2.6 Expansion of item tracking services bundled by mobile network operators

- 4.3 Market Restraints

- 4.3.1 Lack of global interoperability standards

- 4.3.2 Data-privacy and cyber-stalking concerns

- 4.3.3 Short product replacement cycles increasing e-waste

- 4.3.4 Import tariffs on key RF components in emerging markets

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors

- 4.6 Technological Outlook

- 4.6.1 Smart-home IoT integration trends

- 4.7 Regulatory Landscape

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Cellular

- 5.1.2 Bluetooth

- 5.1.3 GPS

- 5.1.4 UWB

- 5.1.5 NFC

- 5.2 By Application

- 5.2.1 Personal Item Tracking

- 5.2.2 Luggage Tracking

- 5.2.3 Pet Tracking

- 5.2.4 Kids and Senior Safety

- 5.2.5 Enterprise Inventory and Asset Tracking

- 5.2.6 Vehicle Tracking

- 5.3 By End User

- 5.3.1 Consumer

- 5.3.2 Commercial

- 5.3.3 Industrial and Logistics

- 5.3.4 Healthcare

- 5.3.5 Government and Defense

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 France

- 5.4.2.3 United Kingdom

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Southeast Asia

- 5.4.3.7 Rest of Asia Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Turkey

- 5.4.5.4 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Nigeria

- 5.4.6.3 Kenya

- 5.4.6.4 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Tile Inc.

- 6.4.2 Samsung Electronics Co., Ltd.

- 6.4.3 Apple Inc.

- 6.4.4 Cube Tracker Inc.

- 6.4.5 Kaltio Technologies Oy

- 6.4.6 PB Inc. (Pebblebee)

- 6.4.7 Chipolo d.o.o.

- 6.4.8 XY Labs, Inc.

- 6.4.9 Garmin Ltd.

- 6.4.10 Jiobit Inc.

- 6.4.11 Invoxia SA

- 6.4.12 HButler International Pty. Ltd. (Orbit)

- 6.4.13 Wistiki SAS

- 6.4.14 Nut Technology Co., Ltd.

- 6.4.15 Filo S.r.l.

- 6.4.16 Satotech Limited (TagoBee)

- 6.4.17 Trackimo Inc.

- 6.4.18 Loc8tor Ltd.

- 6.4.19 Rinex Technology Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment