|

市場調查報告書

商品編碼

1934740

深度過濾:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031)Depth Filtration - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

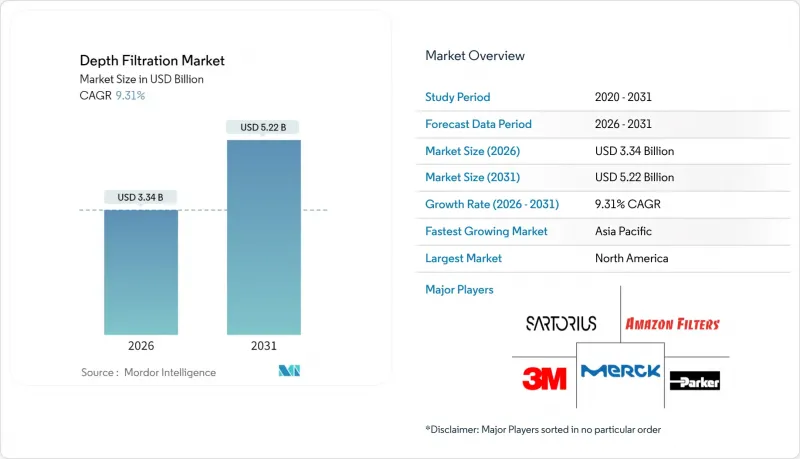

預計深度過濾市場將從 2025 年的 30.6 億美元成長到 2026 年的 33.4 億美元,到 2031 年將達到 52.2 億美元,2026 年至 2031 年的複合年成長率為 9.31%。

生物製藥廠商必須滿足最新的病毒安全法規,因此對深度過濾器的需求強勁,加之經濟高效的一次性使用技術,共同推動了這一領域的擴張。濾芯和濾囊的創新使得深度過濾器的更換率居高不下,因為製藥、食品、飲料和水處理公司都將深度過濾器視為抵禦顆粒物和微生物污染物的第一道重要屏障。設備供應商的整合、向不含 PFAS 的濾材過渡的趨勢以及亞太地區產能的快速擴張,都在擴大市場機會的同時加劇競爭。矽藻土原料供應的緊張和日益嚴格的廢棄物處理法規雖然抑制了成長,但也為永續纖維素替代品創造了新的市場機會。

全球深度過濾市場趨勢與洞察

生物製藥需求不斷成長

隨著生物製劑產能的擴張,對能夠實現高細胞密度下大規模批量純化的深度過濾器的需求持續成長。FUJIFILM在北卡羅來納州投資12億美元擴建的16萬公升反應器項目,清楚展現了大型不鏽鋼和一次性生產線如何推動對純化產能的需求。抗體市場預計到2030年將以每年8%的速度成長,這迫使像AGC Biologics這樣的契約製造生產商將其一次性生物反應器的產能翻番,從而直接提高了過濾器的更換頻率。高產量目標要求深度過濾器兼具高通量和低產品損失,這賦予了供應商更高的定價權。雖然生物相似藥的上市加劇了成本壓力,但由於純度規格很少會受到影響,因此預計這一趨勢將長期持續下去。

過渡到一次性深度過濾器系統

一次性膠囊和堆疊式圓盤模組最大限度地減少了清潔驗證工作,降低了交叉污染風險,並縮短了換型時間。 Cytiva 和 Pall 已投資 3 億美元,在全球 13 個地點擴大一次性產品產能,這再次表明了他們對該技術未來發展的信心。旭化成 (Asahi Kasei) 的 Planova SU-VFC 裝置整合了與 cGMP 設施相容的自動化壓力控制系統,減少了操作人員的干涉。食品和飲料加工商也紛紛效仿,在不增加水或化學品消耗的情況下滿足過敏原管理要求。儘管人們對可回收性仍有擔憂,但監管機構對一次性生產線的持續支持正在推動其普及應用。

由於膜分離和切向流過濾等替代技術的出現,市場佔有率受到侵蝕。

切向流系統可在單一連續設備中實現濃縮和過濾,從而減少殘留體積和操作人員接觸點。 Repligen 的自動化盒式設備配備在線連續紫外線監測功能,可提高製程控制和擴充性,並協助企業避免深度過濾瓶頸。膜成本的下降和精確的分子量截留使得切向流過濾在某些高價值治療藥物領域具有經濟競爭力。連續生產模式正在加速切向流過濾技術的應用,尤其是在可以避免使用傳統間歇式設備的新建工廠。因此,深度過濾供應商必須不斷創新,否則將面臨市場佔有率流失的風險。

細分市場分析

到2025年,濾芯過濾器仍將佔據深度過濾市場最大佔有率,收入佔比達37.79%,這反映了其在現有不銹鋼管線和水務設施中的廣泛應用。由於終端用戶重視可預測的更換週期和廣泛的化學相容性,濾芯深度過濾市場規模持續穩定成長。然而,受一次性原料藥(API)生產需求的推動,膠囊式過濾器預計到2031年將以9.66%的複合年成長率成長。一次性原料原料藥生產受惠於無需CIP檢驗的封閉式更換系統。先進的膠囊式過濾器設計整合了預過濾器和排氣口,從而減少了在空間有限的無塵室中的面積。 《基因工程與生物技術新聞》報道稱,細胞和基因治療機構對膠囊式過濾器的應用日益廣泛,這標誌著一次性產品市場正迎來轉捩點。

產品創新進一步模糊了產品類別的界限,混合式疊盤式濾芯模組結合了過濾過濾層,在擴大處理能力的同時,也能保護下游病毒過濾器。為了符合新的歐洲法規,供應商如賽多利斯(Sartorius)計劃在2025年推出不含PFAS的高通量型號,同時提供與現有產品相當的流量性能。在葡萄酒、啤酒和血漿產業,過濾片和濾芯仍然至關重要,因為這些產業擁有數十年的營運經驗和較低的資本成本,足以抵消轉換成本。總體而言,產品發展趨勢表明,市場正朝著多功能濾芯和濾囊的方向發展,這些濾芯和濾囊能夠在不影響永續性目標的前提下提供可擴展的性能,從而保持深度過濾市場的競爭力和創新性。

矽藻土憑藉其高污泥截留能力和成本優勢,預計2025年將持續維持39.78%的市佔率。然而,依賴矽藻土介質的深層過濾市場正面臨挑戰,國際紙業公司關閉位於喬治城的工廠,導致美國絨毛漿產量減少5%,原料成本波動加劇。同時,隨著監管機構和買家優先考慮可堆肥和不含PFAS的介質,纖維素介質預計將以9.93%的複合年成長率成長。麻省理工學院正在開發的新型絲-纖維素複合材料預示著一系列生物基材料的出現,這些材料有望進一步減少對礦物開採的依賴。

活性碳複合複合材料負責去除飲料中的異味、異味和色澤,而珍珠岩仍是高溫化學製程的主要介質。供應商正在將吸附劑粉末摻入纖維素墊中,以製造多功能深層吸附層,無需單獨的過濾步驟即可捕獲微量有機物。隨著介質創新兼顧性能和環境指標,纖維素的可再生和廣泛的供應基礎為其市場佔有率成長提供了機遇,而矽藻土已確立的成本優勢和機械強度表明,在預測期內,兩者將並存。

區域分析

到2025年,北美將佔全球收入的41.92%,這主要得益於波士頓、舊金山和三角研究園區等成熟的生物製藥產業叢集,這些企業持續投資升級過濾器,以符合FDA關於病毒去除的指導方針。美國本土供應商正在加強其區域供應鏈,例如Purolite在賓州新建的樹脂工廠和Perle在新加坡的擴張計劃,這些都將繼續為美國客戶供應產品。美國對基因治療生產商的大力財政支持,以及對cGMP合規性的推動,正在推動市場對檢驗的病毒去除性能的高階深度濾芯的需求。

亞太地區將維持最快增速,到2031年複合年成長率將達到10.78%。中國臨床試驗的激增以及各省的優惠政策正在推動需要一次性澄清生產線的新型下游製程。在印度,更嚴格的環境法規以及藥品和特種化學品出口應對力的提升正在推動工業過濾的需求。區域政府資助的大型水處理大型企劃指定採用深度過濾來去除濁度、色度和全氟烷基物質(PFAS),進一步擴大了目標市場。

由於歐洲擁有歷史悠久的疫苗和血漿生產基地,其市場佔有率仍佔據較大佔有率。然而,能源成本上漲和英國脫歐帶來的物流挑戰增加了即時過濾器供應的複雜性,促使各地建立本地緩衝庫存。南美洲和中東及非洲地區尚不成熟,但蘊藏著巨大潛力,公共衛生投資和海水淡化計劃正在催生需求中心。然而,貨幣波動和政治風險正在減緩私部門的參與。在全球範圍內,深度過濾市場正受益於人們對水質的普遍關注、生物製藥活動的活性化以及監管趨同——這些因素共同認可了檢驗的深度過濾工藝作為污染控制的基礎。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 生物製藥需求不斷成長

- 向一次性深度過濾系統過渡

- 嚴格的GMP純度和病毒安全性法規

- 經濟高效的高密度灌注培養澄清方法

- 用於病毒載體和基因治療澄清的深度過濾裝置

- 市場限制

- 膜分離和TFF替代技術造成的佔有率侵蝕

- 遵守有關廢棄培養基處置的環境法規

- 特種纖維素和DE供應緊張

- 新型化學技術在黏稠原料處理的規模化限制。

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 依產品類型

- 濾芯過濾器

- 膠囊過濾器

- 過濾模組

- 濾紙

- 按媒體類型

- 矽藻土

- 活性碳

- 纖維素

- 珍珠岩

- 透過使用

- 最終產品加工

- 小分子加工

- 生物製品加工

- 細胞澄清

- 原料過濾

- 介質和緩衝液過濾

- 微生物附著量檢測

- 最終用戶

- 製藥和生物技術公司

- 食品和飲料製造商

- 水和污水處理設施

- 研究機構和學術研究機構

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 亞太其他地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- GCC

- 南非

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 市佔率分析

- 公司簡介

- 3M Company

- Danaher Corp.(Pall)

- Merck KGaA(MilliporeSigma)

- Sartorius AG(Sartorius Stedim Biotech)

- Eaton Corporation plc

- Parker-Hannifin Corporation

- Donaldson Company Inc.

- Alfa Laval AB

- MANN+HUMMEL GmbH

- Porvair PLC

- ErtelAlsop(Micronics)

- Meissner Filtration Products Inc.

- Amazon Filters Ltd.

- Pentair PLC

- Freudenberg Filtration Tech.

- Cummins Filtration

- Graver Technologies LLC

- Koch Separation Solutions

- Cobetter Biotech Co. Ltd.

第7章 市場機會與未來展望

The depth filtration market is expected to grow from USD 3.06 billion in 2025 to USD 3.34 billion in 2026 and is forecast to reach USD 5.22 billion by 2031 at 9.31% CAGR over 2026-2031.

Strong demand from biopharmaceutical manufacturers that must meet updated viral-safety rules, alongside cost-effective single-use technologies, underpins the expansion. Cartridge and capsule innovations keep replacement rates high, while pharma, food, beverage, and water processors view depth filters as an indispensable first barrier against particulate and microbial contaminants. Consolidation among equipment vendors, the push for PFAS-free media, and Asia-Pacific's rapid capacity additions enhance opportunities but also intensify competitive pressure. Raw-material supply constraints for diatomaceous earth and tighter waste-disposal regulations temper growth yet open white-space for sustainable cellulose alternatives.

Global Depth Filtration Market Trends and Insights

Rising Demand for Biopharmaceuticals

Capacity expansion in biologics drives sustained uptake of depth filters that must clarify larger batch volumes at higher cell densities. Fujifilm's USD 1.2 billion North Carolina expansion adding 160,000 L of reactors underscores how larger stainless and single-use trains elevate clarification throughput needs. Antibody segment growth at 8% annually through 2030 forces contract manufacturers such as AGC Biologics to double single-use bioreactor capacity, directly multiplying filter-change frequencies. Elevated output targets demand depth filters that combine high flux with low product loss, placing premium pricing power in suppliers' hands. The trend remains long-lived as biosimilar launches intensify cost-of-goods pressure yet rarely compromise on purity specifications.

Shift Toward Single-Use Depth-Filter Systems

Disposable capsules and stacked-disc modules minimize cleaning validation, reduce cross-contamination risk, and shorten changeover times. Cytiva and Pall committed USD 300 million to scale single-use capacity across 13 global sites, reaffirming confidence in the technology's future. Asahi Kasei's Planova SU-VFC unit integrates automated pressure control that fits cGMP suites and cuts operator intervention. Food and beverage processors have followed suit to meet allergen-control mandates without raising water and chemical consumption. Continued regulatory endorsement of disposable trains bolsters adoption, even as recyclability concerns linger.

Membrane & TFF Alternatives Eroding Share

Tangential-flow systems offer concentration and diafiltration in a single continuous unit, reducing hold-up volumes and operator touches. Repligen's automated cassettes with in-line UV monitoring sharpen process control and scalability, allowing users to bypass depth-filter bottlenecks. Falling membrane costs and precise molecular-weight cutoffs tilt the economics in favor of TFF for certain high-value therapeutics. Continuous-manufacturing paradigms accelerate adoption, particularly in green-field plants that can avoid legacy batch equipment. Depth-filter vendors must therefore innovate or risk share attrition.

Other drivers and restraints analyzed in the detailed report include:

- Stringent GMP Purity & Viral-Safety Rules

- Cost-Effective Clarification for High-Density Perfusion Cultures

- Environmental Compliance for Spent Media Disposal

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cartridge filters retained the largest slice of the depth filtration market in 2025, standing at 37.79% revenue share, reflecting entrenched usage across legacy stainless-steel lines and municipal-water facilities. The depth filtration market size for cartridge solutions continues to grow at a steady pace as end users value their predictable change-out intervals and broad chemical compatibility. Yet, capsule formats post a 9.66% CAGR through 2031, fueled by single-use drug-substance manufacturing that benefits from closed-system changeovers without CIP validation. Advanced capsule designs integrate pre-filters and vent ports, compressing skid footprints inside constrained clean-rooms. Genetic Engineering & Biotechnology News reports widening adoption across cell-gene therapy suites, hinting at an inflection favoring disposability.

Product innovation further blurs category lines, with hybrid stack-disc modules housing both depth and membrane layers to extend capacity while protecting downstream viral filters. Suppliers such as Sartorius unveiled PFAS-free high-throughput variants in 2025, positioning to comply with upcoming European legislation while providing equivalent flow performance. Filter sheets and modules maintain relevance in wine, beer, and plasma applications where decades of operating know-how and low capital needs outweigh changeover labor. Overall, product evolution suggests convergence toward multipurpose cartridges and capsules that deliver scalable performance without compromising sustainability targets, keeping the depth filtration market competitive and innovation-rich.

Diatomaceous earth dominated with 39.78% share in 2025 owing to its high dirt-holding capacity and favorable cost profile. The depth filtration market size tied to diatomite media faces headwinds after International Paper shuttered its Georgetown mill, removing 5% of U.S. fluff pulp output and raising input-cost volatility. Cellulose media, in contrast, is projected to grow at 9.93% CAGR as regulators and buyers prioritize compostable, PFAS-free options. Novel silk-cellulose hybrids under development at MIT signal a pipeline of bio-based materials that could further erode reliance on mined minerals.

Activated-carbon composites serve taste, odor, and color removal roles in beverages, while perlite remains the media of choice in high-temperature chemical processes. Vendors are blending adsorptive powders into cellulose mats to create multi-functional depth layers that capture trace organics without separate filtration passes. As media innovation tracks both performance and environmental metrics, cellulose's renewable nature and broad supply base position it for incremental share gains, but diatomaceous earth's entrenched cost advantage and mechanical strength signal coexistence over the forecast horizon.

The Depth Filtration Market Report is Segmented by Product Type (Cartridge Filters, Capsule Filters, and More), Media Type (Diatomaceous Earth, Activated Carbon, and More), Application (Final Product Processing, Small-Molecule Processing, and More), End User (Pharmaceutical & Biotechnology Cos., and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America captured 41.92% of global revenue in 2025, underpinned by mature biologics clusters in Boston, San Francisco, and Research Triangle Park that consistently invest in filter upgrades to comply with FDA guidance on viral reduction. Domestic suppliers strengthen regional supply chains, as highlighted by Purolite's new Pennsylvania resin plant and Pall's Singapore expansion that still funnels product back to U.S. customers. The United States benefits from robust funding for gene-therapy producers, whose adherence to cGMP pushes demand for high-end depth cartridges with validated log-reduction performance.

Asia-Pacific remains the fastest-growing region through 2031 at 10.78% CAGR. China's clinical-trial surge and generous provincial incentives spur new downstream suites requiring single-use clarification lines. India's industrial filtration demand grows on tightening environmental norms and the drive to improve export readiness in pharmaceuticals and specialty chemicals. Regional governments fund water-treatment megaprojects that specify depth filters for turbidity, color, and PFAS removal, further expanding the addressable base.

Europe retains a significant slice due to long-established vaccine and plasma manufacturing. Yet high energy costs and Brexit-related logistics add complexity to just-in-time filter deliveries, incentivizing local buffer stocks. South America and Middle East Africa remain nascent but opportunistic; public health investments and desalination projects create pockets of demand although currency volatility and political risk slow private-sector uptake. Globally, the depth filtration market benefits from universal focus on water quality, heightened biologics activity, and regulatory convergence that recognizes validated depth-filtration steps as foundational to contamination control.

- 3M

- Danaher Corp. (Pall)

- Merck KGaA (MilliporeSigma)

- Sartorius

- Eaton Corporation plc

- Parker Hannifin

- Donaldson Company Inc.

- Alfa Laval AB

- MANN+HUMMEL GmbH

- Porvair

- ErtelAlsop (Micronics)

- Meissner Filtration Products

- Amazon Filters Ltd.

- Pentair PLC

- Freudenberg Filtration Tech.

- Cummins Filtration

- Graver Technologies LLC

- Koch Separation Solutions

- Cobetter Biotech Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for biopharmaceuticals

- 4.2.2 Shift toward single-use depth-filter systems

- 4.2.3 Stringent GMP purity & viral-safety rules

- 4.2.4 Cost-effective clarification for high-density perfusion cultures

- 4.2.5 Depth filters for viral-vector & gene-therapy clarification

- 4.3 Market Restraints

- 4.3.1 Membrane & TFF alternatives eroding share

- 4.3.2 Environmental compliance for spent media disposal

- 4.3.3 Supply tightness of specialty cellulose & DE

- 4.3.4 Scale-up limits with novel chemistries for viscous feeds

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type (Value, USD)

- 5.1.1 Cartridge Filters

- 5.1.2 Capsule Filters

- 5.1.3 Filter Modules

- 5.1.4 Filter Sheets

- 5.2 By Media Type (Value, USD)

- 5.2.1 Diatomaceous Earth

- 5.2.2 Activated Carbon

- 5.2.3 Cellulose

- 5.2.4 Perlite

- 5.3 By Application (Value, USD)

- 5.3.1 Final Product Processing

- 5.3.2 Small-Molecule Processing

- 5.3.3 Biologics Processing

- 5.3.4 Cell Clarification

- 5.3.5 Raw-Material Filtration

- 5.3.6 Media & Buffer Filtration

- 5.3.7 Bioburden Testing

- 5.4 By End User (Value, USD)

- 5.4.1 Pharmaceutical & Biotechnology Cos.

- 5.4.2 Food & Beverage Manufacturers

- 5.4.3 Water & Waste-water Facilities

- 5.4.4 Research & Academic Labs

- 5.4.5 Others

- 5.5 By Geography (Value, USD)

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 GCC

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 3M Company

- 6.3.2 Danaher Corp. (Pall)

- 6.3.3 Merck KGaA (MilliporeSigma)

- 6.3.4 Sartorius AG (Sartorius Stedim Biotech)

- 6.3.5 Eaton Corporation plc

- 6.3.6 Parker-Hannifin Corporation

- 6.3.7 Donaldson Company Inc.

- 6.3.8 Alfa Laval AB

- 6.3.9 MANN+HUMMEL GmbH

- 6.3.10 Porvair PLC

- 6.3.11 ErtelAlsop (Micronics)

- 6.3.12 Meissner Filtration Products Inc.

- 6.3.13 Amazon Filters Ltd.

- 6.3.14 Pentair PLC

- 6.3.15 Freudenberg Filtration Tech.

- 6.3.16 Cummins Filtration

- 6.3.17 Graver Technologies LLC

- 6.3.18 Koch Separation Solutions

- 6.3.19 Cobetter Biotech Co. Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

2026年全球深度過濾市場報告

2026年全球深度過濾市場報告 全球深過濾市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球深過濾市場規模、佔有率、趨勢和成長分析報告(2026-2034) 深度過濾市場 - 全球產業規模、佔有率、趨勢、機會及預測(按產品、介質類型、應用、地區和競爭格局分類,2021-2031年)

深度過濾市場 - 全球產業規模、佔有率、趨勢、機會及預測(按產品、介質類型、應用、地區和競爭格局分類,2021-2031年) 深度過濾市場規模、佔有率和成長分析(按產品類型、過濾介質類型、應用、營運規模和地區分類)-2026-2033年產業預測

深度過濾市場規模、佔有率和成長分析(按產品類型、過濾介質類型、應用、營運規模和地區分類)-2026-2033年產業預測 深度過濾市場按應用、最終用戶行業、濾材類型、過濾格式、額定類型、孔徑、流量配置和系統配置分類 - 全球預測,2025-2032

深度過濾市場按應用、最終用戶行業、濾材類型、過濾格式、額定類型、孔徑、流量配置和系統配置分類 - 全球預測,2025-2032 深層過濾市場規模、佔有率、趨勢分析報告:按過濾介質、產品、最終用途、地區和細分市場進行預測,2025 年至 2030 年

深層過濾市場規模、佔有率、趨勢分析報告:按過濾介質、產品、最終用途、地區和細分市場進行預測,2025 年至 2030 年