|

市場調查報告書

商品編碼

1934721

骨材:市佔率分析、產業趨勢與統計、成長預測(2026-2031)Aggregates - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

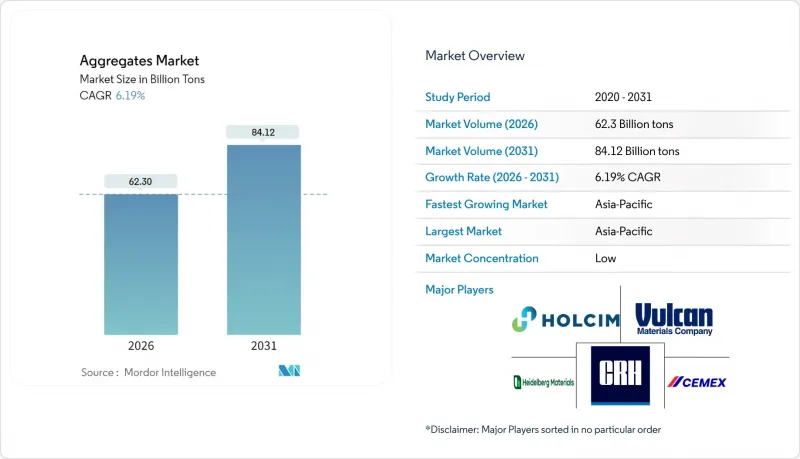

預計到 2026 年,骨材市場規模將達到 623 億噸,高於 2025 年的 586.7 億噸。

預計到 2031 年將達到 841.2 億噸,2026 年至 2031 年的複合年成長率為 6.19%。

政府不斷增加的資本支出計畫旨在實現公路、鐵路、港口和可再生能源設施的現代化,這支撐了成長前景。新興經濟體的快速都市化、預拌混凝土的日益普及以及公共部門對低碳建築材料的獎勵也推動了需求。主要生產商正在深化垂直整合,以共用採石場所有權,並提高瀝青和預拌混凝土業務的物流和採購效率。同時,循環經濟政策正在加速對再生骨材加工的投資。然而,柴油價格上漲推高了運輸成本,緩慢的環境核准流程延緩了新採石場的開發,而監管機構對再生材料微塑膠污染的審查日益嚴格,也帶來了合規方面的挑戰。

全球骨材市場趨勢與洞察

亞太新興市場基礎建設投資激增

中國的「十四五」規劃提出,到2025年將高速鐵路里程延長3800公里,光是安定器、砂和碎石就需要數千萬噸。同時,核能發電投資(裝置容量。核子反應爐2024-2025會計年度聯邦預算將資本支出增加17.1%,達到111兆印度盧比(約1340億美元),其中24.5%分配給了公路運輸和公路部。這將促進公路、橋樑和地鐵線路的採石場產量。預計2020年至2035年間,亞洲整體交通基礎設施需求將達到43兆美元,其中63%用於公路建設,這將鞏固該地區作為建築骨材市場關鍵成長引擎的地位。印尼、越南和菲律賓的智慧城市規劃對用於綠色路面和雨水管理系統的透水骨材產生了特殊需求。

擴大預拌混凝土的使用,這需要高規格的骨材

預拌混凝土攪拌站如今在都市區供應鏈中佔據主導地位,提高了高強度混凝土混合料對骨材粒徑分佈、形狀和潔淨度的要求。 Aggregate Industries公司將於2024年在伯明罕開設產能120立方公尺/小時的攪拌站,專注於生產低碳ECOPact混凝土。採石場作業中混合料的改進層出不窮,顯示對破碎和清潔程度更高的石材供應需求日益成長。隨著聯準會計畫在2025年中期將利率引導至5.5%,美國住宅建設產業的景氣預計將會增強,從而維持住宅和資料中心建設對高品質骨材的需求。由兩黨基礎設施法案資金籌措的高速公路維修需要使用Superpave瀝青混合料,而這種混合料需要使用由先進的立軸衝擊式破碎生產線生產的立方體、低吸水率骨材。新興的資料中心和人工智慧 (AI) 計算園區指定使用骨材來支撐混凝土混合物,以實現熱品質和電磁屏蔽,這為富含磁鐵礦和赤鐵礦的礦物填料開闢了一個利潤豐厚的細分市場。

運輸和處理成本不斷上漲

對於平均運輸距離超過 50 英里的路段,柴油燃料成本可高達交貨骨材的 25%。研究表明,縮短 15 英里的運輸路線每年可減少 1.78 億英里的卡車運輸里程,節省 2,300 萬加侖燃料,並避免 23.8 萬噸二氧化碳排放——相當於節省 4.46 億美元的物流成本。鐵路運輸的燃油效率是卡車運輸的三倍,但由於缺乏專用線和定價機制的不確定性阻礙了鐵路運輸的普及,美國祇有 9% 的運輸量採用鐵路運輸。地緣政治事件導致的燃料價格波動加劇了預算風險,而歐盟的碳定價機制提高了貨運附加費,迫使一些承包商為了控制計劃預算,不得不使用當地可獲得的低品質骨材。

細分市場分析

到2025年,砂將佔骨材市場的40.03%,這反映了其在預拌混凝土、抹灰和瀝青中的重要作用。砂的複合年成長率將維持在6.19%,與整體骨材市場趨勢一致,亞洲和中東的大型城市大型企劃是推動砂需求成長的主要因素。礫石緊隨其後,主要用於路基和排水層;而碎石則為結構混凝土和橋面提供了精確的粒徑分佈。儘管砂製骨材的骨材規模預計將穩定成長,但中國、越南和馬來西亞對河砂開採的限制正在促使市場需求轉向玄武岩和花崗岩等人工砂。

其他骨材(例如再生混凝土、人造砂和輕質合成骨材)是成長最快的細分市場,年複合成長率達7.6%。再生混凝土骨材目前已符合國家吸水率和洛杉磯磨耗試驗標準,並首次獲准在德國和荷蘭用於結構用途。 CEMEX位於柏林的工廠每年處理40萬噸建築廢棄物,證明了其商業規模的可行性,並為其他城市中心提供了借鑒。 2024年,倫敦一棟辦公大樓在其樓板中使用了25%的再生骨材,蘊藏量碳排放強度降低了12%——這項指標正日益被納入資產估值。隨著房地產開發商積極尋求綠色建築認證,預計再生材料在建築骨材市場中的佔有率將從目前的個位數成長。

骨材市場報告按骨材類型(砂、礫石、碎石、礦渣、其他骨材類型(再生骨材、人工骨材等))、應用領域(建築、隔熱材料、其他應用)和地區(亞太地區、北美地區、歐洲地區、南美地區、中東和非洲地區)進行細分。市場預測以噸為單位。

區域分析

到2025年,亞太地區將佔全球總量的52.07%,並在2031年之前以7.33%的複合年成長率成長。中國到2025年需要新建3800公里高速鐵路和新增11.9吉瓦核能發電發電容量,推動了採石場產量創歷史新高。同時,印度11.1兆盧比的資本計畫提振了對碎花崗岩的需求,特別是用於黃金四邊形高速公路的升級改造。日本對抗震交通幹線和防波堤維修的投資也維持了對碎硬岩的需求。

北美則位居第二:2023年美國採石場預計出貨量為25.2億噸(價值368億美元),較上年成長12.5%,這主要得益於兩黨共同支持的基礎設施立法以及製造業回流趨勢。在加拿大,安大略省和不列顛哥倫比亞省的鐵路分離工程正在加速推進;而在墨西哥,近岸外包推動了巴希奧地區和北部走廊沿線工業園區的建設,從而提振了石灰石需求。強勁的公共預算和預期中的降息週期將支撐2025-2026年的生產。

政策主導的消費將在歐洲保持穩定。歐盟強制推行的建築廢棄物回收政策正在推動對再生骨材的需求,尤其是在德國、法國和北歐國家,公共採購優先考慮低碳替代品。斯堪地那維亞國家對被動式房屋標準的重視也促進了對輕質保溫骨材的需求。南美洲和中東及非洲地區的需求相對滯後,但部分地區已呈現加速成長的跡象。沙烏地阿拉伯的NEOM(新未來)計劃利用國內採石場的花崗岩輝長岩,以及巴西重啟聯邦公路養護工程,都為全球建築骨材市場做出了貢獻。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 快速的基礎建設投資,尤其是在新興的亞太市場

- 預拌混凝土的日益普及推動了對高品質骨材的需求。

- 政府獎勵策略低碳建築解決方案

- 循環經濟政策鼓勵使用再生骨材。

- 物聯網賦能的「智慧骨材」用於結構健康監測

- 市場限制

- 高昂的運輸和處理成本

- 新採石場需要嚴格的環境許可

- 柴油價格波動會影響採石場的營運成本。

- 人們對再生骨材中微塑膠污染的擔憂

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 依骨材類型

- 沙

- 碎石

- 碎石

- 礦渣

- 其他骨材類型(再生骨材、人造骨材等)

- 透過使用

- 建造

- 大樓

- 鐵路

- 路

- 其他

- 隔熱材料

- 其他用途

- 建造

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Breedon Group plc

- Buzzi SpA

- Cemex SAB DE CV

- China Resources Building Materials Technology Holdings

- CRH

- Eurocem Limited

- Heidelberg Materials AG

- HOLCIM

- Luck Stone

- Martin Marietta Materials

- Rogers Group Inc.

- Vulcan Materials Company

第7章 市場機會與未來展望

Aggregates market size in 2026 is estimated at 62.3 Billion tons, growing from 2025 value of 58.67 Billion tons with 2031 projections showing 84.12 Billion tons, growing at 6.19% CAGR over 2026-2031.

Rising governmental capital-expenditure programs designed to modernize roads, railways, ports, and renewable-energy sites anchor the growth outlook. Demand also benefits from rapid urbanization in emerging economies, widening adoption of ready-mix concrete, and public-sector incentives for low-carbon building materials. Leading producers are deepening vertical integration so that quarry ownership, asphalt, and ready-mix operations share logistics and procurement efficiencies, while circular-economy mandates accelerate investments in recycled aggregates processing. However, high diesel costs inflate haulage expenses, time-consuming environmental approvals delay new quarries, and regulators increasingly scrutinize recycled materials for micro-plastic contamination, creating compliance hurdles.

Global Aggregates Market Trends and Insights

Surging Infrastructure Spending in Emerging Asia-Pacific Markets

China's five-year plan requires 3,800 km of additional high-speed rail lines by 2025, a target that alone necessitates tens of millions of tons of ballast, sand, and crushed stone. Parallel investments in nuclear energy from 58.08 million kW installed in 2024 to 70 million kW by 2025 further expand concrete demand for reactor bases and ancillary facilities. India's 2024-25 Union Budget raised capital outlays by 17.1% to INR 11.1 lakh crore (USD 134 billion), with 24.5% earmarked for the Ministry of Road Transport and Highways, propelling quarry output for highways, bridges, and metro corridors. Across Asia, transport infrastructure needs of USD 43 trillion between 2020 and 2035, of which 63% is dedicated to roads, cement the region's status as the prime growth engine for the construction aggregates market . Smart-city programs in Indonesia, Vietnam, and the Philippines add specialized demand for permeable aggregates used in green pavements and stormwater management systems.

Rising Adoption of Ready-mix Concrete Requiring High-Spec Aggregates

Ready-mix concrete plants now dominate urban supply chains, pushing baseline specifications for gradation, shape, and cleanliness of aggregates used in high-strength mixes. Aggregate Industries opened a 120 m3/hour plant in Birmingham in 2024, emphasizing low-carbon ECOPact concrete, illustrating how formulation changes ripple back to quarry operations that must supply more precisely crushed and washed stone. US residential-construction sentiment is expected to firm as the Federal Reserve guides policy rates to 5.5% by mid-2025, sustaining premium-grade aggregate demand in housing and data-center builds. Highway refurbishments funded by the Bipartisan Infrastructure Law require Superpave asphalt mixes demanding cubical, low-absorption aggregates derived from advanced vertical-shaft impact crushing lines. Emerging data-center and Artificial Intelligence (AI)-compute campuses specify aggregates that support concrete mixes engineered for thermal mass and electromagnetic shielding, opening high-margin niches for mineral fillers rich in magnetite or hematite.

High Transportation and Handling Costs

Diesel-fuel expenses can equal 25% of delivered aggregate price when average haul distances exceed 50 miles. Research shows that trimming haul routes by 15 miles could cut 178 million truck-miles, save 23 million gallons of fuel, and avoid 238,000 tons of CO2 yearly, translating into USD 446 million of logistical savings. Rail is 3-times more fuel-efficient than trucks, yet only 9% of United States shipments move by rail because limited sidings and opaque rate-setting deter adoption . Fuel-price volatility following geopolitical events magnifies budget risk, and carbon-pricing schemes in the EU raise freight surcharges, prompting some contractors to substitute locally available yet lower-quality aggregates to stay within project budgets.

Other drivers and restraints analyzed in the detailed report include:

- Government Stimulus for Low-Carbon Construction Solutions

- Circular-Economy Mandates Boosting Use of Recycled Aggregates

- Stringent Environmental Permitting for New Quarries

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sand commanded 40.03% of the Aggregates market in 2025, reflecting its indispensable role in ready-mix concrete, plaster, and asphalt. At 6.19% CAGR, sand remains aligned with the overall Aggregates market trajectory as urban mega-projects across Asia and the Middle East sustain bulk demand. Gravel follows, preferred for road bases and drainage layers, while crushed stone supplies precise gradation for structural concrete and bridge decks. The Aggregates market size attributed to sand is projected to climb steadily, but permit caps on river-sand extraction in China, Vietnam, and Malaysia shift volumes toward manufactured sand sourced from basalt and granite.

Other aggregate types, including recycled concrete, manufactured sand, and lightweight synthetics, represent the fastest-growing slice at a 7.6% CAGR. Recycled concrete aggregates now meet national-standard water-absorption and Los Angeles-abrasion limits, allowing use in structural elements for the first time in Germany and the Netherlands. Cemex's Berlin plant processes 400,000 tons of CDW annually, signalling commercial-scale viability and offering a template for other urban nodes . When a London office tower reused 25% recycled aggregate in its floor slabs in 2024, embodied-carbon intensity fell by 12%, a metric increasingly embedded in asset valuations. As property developers chase green-building credits, the construction aggregates market share of recycled materials is poised to widen beyond its current single-digit level.

The Aggregate Market Report is Segmented by Aggregate Type (Sand, Gravel, Crushed Stone, Slag, and Other Aggregate Types (Recycled, Manufactured, Etc. )), Application (Construction, Insulation, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (tons).

Geography Analysis

Asia-Pacific held 52.07% of global volume in 2025 and is pacing at 7.33% CAGR to 2031. China's need for 3,800 km of new high-speed rail by 2025 and a nuclear-power-capacity uplift of 11.9 million kW push quarry production to records, while India's INR 11.1 lakh crore capital program enriches demand for crushed granite, especially in the Golden Quadrilateral highway upgrades. Japan invests in earthquake-resilient transport arteries and seawall refurbishments, sustaining orders for hard-rock rip-rap.

North America ranks second: United States quarries shipped 2.52 billion tons in 2023 valued at USD 36.8 billion, a 12.5% year-over-year gain, on the back of the Bipartisan Infrastructure Law and manufacturing-onshoring wave. Canada accelerates rail-grade separations in Ontario and British Columbia, while Mexico's nearshoring adds industrial parks along the Bajio and northern corridors that favour limestone. Robust public budgets and an anticipated interest-rate easing cycle underpin 2025-26 pour volumes.

Europe maintains stable, policy-driven consumption. European Union (EU)-wide Construction and Demolition Waste (CDW) recycling mandates create pull-through for secondary aggregates, particularly in Germany, France, and the Nordics, where public procurement favors low-carbon alternatives. Scandinavia's emphasis on passive-house standards lifts demand for lightweight insulation aggregates. South America and the Middle East & Africa trail but exhibit pockets of acceleration: Saudi Arabia's NEOM (New Future) project sources granitic gabbro from domestic quarries, and Brazil revives its federal-road-maintenance backlog, each injecting incremental demand into the global construction aggregates market.

- Breedon Group plc

- Buzzi S.p.A.

- Cemex S.A.B DE C.V.

- China Resources Building Materials Technology Holdings

- CRH

- Eurocem Limited

- Heidelberg Materials AG

- HOLCIM

- Luck Stone

- Martin Marietta Materials

- Rogers Group Inc.

- Vulcan Materials Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Infrastructure Spending, Especially in Emerging Asia-Pacific Markets

- 4.2.2 Rising Adoption of Ready-mix Concrete Driving Demand for High-spec Aggregates

- 4.2.3 Government Stimulus for Low-Carbon Construction Solutions

- 4.2.4 Circular-economy Mandates Boosting Use of Recycled Aggregates

- 4.2.5 Internet of Things (IoT)-enabled "Smart Aggregates" for Structural Health Monitoring

- 4.3 Market Restraints

- 4.3.1 High Transportation and Handling Costs

- 4.3.2 Stringent Environmental Permitting for New Quarries

- 4.3.3 Volatility in Diesel Prices Impacting Quarry Opex

- 4.3.4 Micro-plastic Contamination Concerns in Recycled Aggregates

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Aggregate Type

- 5.1.1 Sand

- 5.1.2 Gravel

- 5.1.3 Crushed Stone

- 5.1.4 Slag

- 5.1.5 Other Aggregate Types (Recycled, Manufactured, etc.)

- 5.2 By Application

- 5.2.1 Construction

- 5.2.1.1 Buildings

- 5.2.1.2 Railways

- 5.2.1.3 Roadways

- 5.2.1.4 Others

- 5.2.2 Insulation

- 5.2.3 Other Applications

- 5.2.1 Construction

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Breedon Group plc

- 6.4.2 Buzzi S.p.A.

- 6.4.3 Cemex S.A.B DE C.V.

- 6.4.4 China Resources Building Materials Technology Holdings

- 6.4.5 CRH

- 6.4.6 Eurocem Limited

- 6.4.7 Heidelberg Materials AG

- 6.4.8 HOLCIM

- 6.4.9 Luck Stone

- 6.4.10 Martin Marietta Materials

- 6.4.11 Rogers Group Inc.

- 6.4.12 Vulcan Materials Company

7 Market Opportunities and Future Outlook

- 7.1 White-space and unmet-need assessment

- 7.2 Smart and Self-Healing Concrete Transforming Aggregate Market

建築骨材市場:按類型、材料和最終用途分類,全球預測(2026-2032年)

建築骨材市場:按類型、材料和最終用途分類,全球預測(2026-2032年) 骨材骨材市場規模、佔有率和成長分析:按產品類型、應用、最終用戶、原料來源、通路和地區分類-2026-2033年產業預測

骨材骨材市場規模、佔有率和成長分析:按產品類型、應用、最終用戶、原料來源、通路和地區分類-2026-2033年產業預測 2026年全球建築骨材市場報告

2026年全球建築骨材市場報告 建築骨材市場分析及預測(至2035年):依類型、產品、應用、材料類型、製程、最終用戶、技術、安裝類型、設備及解決方案分類

建築骨材市場分析及預測(至2035年):依類型、產品、應用、材料類型、製程、最終用戶、技術、安裝類型、設備及解決方案分類 日本建築骨材市場規模、佔有率、趨勢和預測:按類型、應用和地區分類,2026-2034年

日本建築骨材市場規模、佔有率、趨勢和預測:按類型、應用和地區分類,2026-2034年 建築骨材市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、最終用戶、地區和競爭對手分類,2021-2031年

建築骨材市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、最終用戶、地區和競爭對手分類,2021-2031年 建築骨材市場規模、佔有率和成長分析(按骨材類型、產品類型、尺寸、形狀、類別、應用、分銷管道和地區分類)-2026-2033年產業預測

建築骨材市場規模、佔有率和成長分析(按骨材類型、產品類型、尺寸、形狀、類別、應用、分銷管道和地區分類)-2026-2033年產業預測 再生建築骨材市場規模、佔有率及成長分析(依產品類型、形態、應用及地區分類)-2026-2033年產業預測

再生建築骨材市場規模、佔有率及成長分析(依產品類型、形態、應用及地區分類)-2026-2033年產業預測 全球再生建築材料市場:預測(至2032年)-按產品、材料、應用、最終用戶和地區分類的分析

全球再生建築材料市場:預測(至2032年)-按產品、材料、應用、最終用戶和地區分類的分析 2025-2029年全球骨材市場

2025-2029年全球骨材市場