|

市場調查報告書

商品編碼

1934673

動態交聯熱可塑性橡膠(TPV):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Thermoplastic Vulcanizate (TPV) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

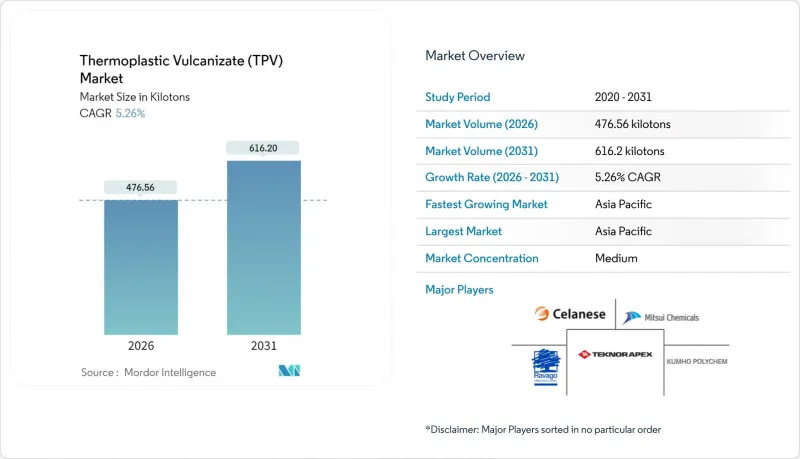

動態交聯熱可塑性橡膠(TPV)市場規模預計到 2026 年將達到 476.56 千噸,高於 2025 年的 452.75 千噸,預計到 2031 年將達到 616.2 千噸。

預計2026年至2031年年複合成長率(CAGR)為5.26%。

這一穩定成長反映了汽車製造商、醫療設備製造商和消費品製造商向可再生彈性體領域的果斷轉型。再生彈性體性能可與熱固性材料媲美,同時也能降低整體系統成本。電動車輕量化的趨勢、循環經濟監管壓力以及電子產品對柔軟觸感表面處理日益成長的需求,都在加速各地區的採用。成本分析表明,與三元乙丙橡膠 (EPDM) 相比,熱塑性彈性體 (TPV) 可將零件製造成本降低 60% 以上,這主要得益於更快的生產週期和省去後固化步驟。供應商目前正在推廣生物基和再生材料含量的產品,這些產品可將製造過程的碳足跡降低高達 50%,為原始設備製造商 (OEM) 實現科學排放目標提供了清晰的路徑。這些特性使得動態交聯熱可塑性橡膠(TPV) 市場成為首選材料解決方案。同時,丙烯和三元乙丙橡膠 (EPDM) 原料價格的波動限制了傳統熱固性材料的吸引力。

全球動態交聯熱可塑性橡膠(TPV)市場趨勢及洞察

汽車OEM製造商對輕量化的需求日益成長

汽車製造商正在加速材料替代,以減輕車輛重量並達到二氧化碳排放目標。熱塑性硫化橡膠 (TPV) 零件比同類三元乙丙橡膠 (EPDM) 密封件輕約 30%,同時保持了良好的抗壓縮永久變形性能,從而進一步延長了電池式電動車的續航里程。動態硫化技術的最新進展消除了長期疲勞性能的差距,使得 TPV 無需更換模具即可取代車門、玻璃滑軌和天窗系統中的熱固性材料。歐盟 2025 年二氧化碳排放上限的壓力正在加速這項變革,並確保熱塑性硫化橡膠市場需求的持續成長。

家用電子電器用TPV軟觸感組件的快速成長

攜帶式電子產品品牌正採用熱塑性聚苯乙烯(TPV)材料,以實現優質的觸感,同時避免噴漆和包覆成型等複雜工藝,從而簡化回收流程。這種樹脂表面可直接成型,無需二次塗層,降低了手柄、保險桿和穿戴式設備機殼等零件的總成本。添加25-40%的回收材料可進一步減少產品固有排放,同時降低資本門檻,使亞洲的代工製造商能夠使用標準射出成型機。更快的生產週期以及符合RoHS和REACH法規,正在推動TPV材料的進一步普及。

與熱固性橡膠相比,其長期耐化學性和耐磨性較差。

在強酸性、油田或磨蝕性環境中,TPV在150°C以上會逐漸失去性能,因此特種熱固性樹脂仍是首選。聚丙烯酸酯改質TPV雖然可以延長使用壽命,但在腐蝕性介質中的管路應用方面仍屬於次要選擇。

細分市場分析

到2025年,標準EPDM/PP複合材料將佔據熱塑性硫化橡膠市場45.05%的佔有率,這主要得益於其低成本和廣泛的模具相容性。成熟的配方能夠滿足大多數密封條和內裝件的規格要求,並獲得OEM廠商認可的性能認證。製造商採用雙螺桿混煉生產線來平衡交聯密度和聚丙烯熔體流動性,從而在高產量下實現嚴格的尺寸公差。因此,在成本競爭力高於性能優勢的項目中,全球加工商仍優先考慮標準等級的產品。

生物基和再生材料產品的產量成長比例將持續提高,這與企業排放目標一致。在歐洲循環經濟合規要求的推動下,生物基熱塑性聚苯乙烯(TPV)預計將以6.76%的複合年成長率(CAGR)實現最快成長。工業廢棄物材料含量高達40%的TPV產品,為原始設備製造商(OEM)提供了一條無需更改零件設計即可快速滿足再生材料標準的途徑。高溫TPV產品雖然應用領域較為小眾,但其策略定位十分重要,例如渦輪增壓器軟管和引擎室墊片等需要在150°C高溫下持續使用的應用。

動態交聯熱可塑性橡膠(TPV) 報告按產品類型(例如,標準 EPDM/PP TPV、高性能/耐熱 TPV)、應用(例如,密封系統/密封條、室內/室外裝飾)、終端用戶行業(例如,汽車、建築/施工、消費品)和地區(例如,亞太地區、北美)進行細分。市場預測以千噸為單位。

區域分析

預計到2025年,亞太地區將佔全球收入的45.70%,複合年成長率達6.10%,成長率超過其他地區。中國每年超過2500萬輛的汽車產量支撐了對TPV密封條的快速需求,而日本在材料科學領域的專業優勢則推動了特種等級產品的研發。印度新興的汽車市場也刺激了市場需求,當地擠出製造商擴大用TPV取代EPDM型材以縮短生產週期。區域原料整合降低了聚丙烯和EPDM的成本,從而創造了單位成本優勢,並推動了對歐洲和北美市場的出口。 Avient計劃於2025年在中國擴大醫用級TPU的生產規模,這標誌著其對亞洲醫療設備OEM廠商的供應優勢將會加強。

在北美,需求集中在以密西根州為中心的汽車產業中心和墨西哥不斷擴張的組裝走廊,並保持穩定。通貨膨脹控制法案提供的電動車激勵措施正在加速電池組的生產,從而帶動低導電性TPV冷卻軟管訂單的成長。 Serenes在蘇州新成立的認證混煉廠為本地和出口市場的注塑成型製程供應亞洲產的Santoprene顆粒,體現了跨區域的供應鏈設計。歐洲是永續性發展應用的標竿地區,獲得ISCC-PLUS認證的TPV在豪華車和綠色建築外牆領域實現了兩位數的成長。報廢車輛指令要求原始設備製造商(OEM)對回收成分進行認證,從而推動了對PCR混合TPV的需求。南美、中東和非洲合計佔據動態交聯熱可塑性橡膠(TPV)市場較小但不斷成長的佔有率。在巴西,汽車生產的復甦正在活性化對當地擠出工廠的投資。沿岸地區的生產商正在探索利用豐富的C3和二烯原料進入下游TPV複合材料業務的機會。在非洲,建築業的蓬勃發展推動了基礎設施計劃對TPV防水型材的需求成長,但回收物流的限制延緩了完全循環經濟效益的實現。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 全球汽車製造商對輕型汽車的需求不斷成長

- 基於TPV的軟觸元件在家用電子電器的廣泛應用

- 原始設備製造商轉向可再生彈性體材料

- 電動車電池組密封技術的應用範圍不斷擴大

- 生物基熱塑性塑膠等級的崛起

- 市場限制

- 丙烯和三元乙丙橡膠原料價格波動

- 與熱固性橡膠相比,其長期耐化學性和耐磨性較差。

- 缺乏TPV廢料的閉合迴路回收基礎設施

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 依產品類型

- 標準EPDM/PP TPV

- 高性能/耐熱TPV

- 生物基TPV

- 含有回收材料的TPV

- 透過使用

- 密封系統和密封條

- 內裝和外飾

- 引擎室內部件

- 軟管和管件

- 電線電纜

- 醫療設備

- 消費品和體育用品零件

- 按最終用戶行業分類

- 車

- 建築/施工

- 消費品

- 衛生保健

- 其他終端用戶產業

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 印尼

- 馬來西亞

- 泰國

- 越南

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 俄羅斯

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 卡達

- 阿拉伯聯合大公國

- 奈及利亞

- 埃及

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Avient Corporation

- Celanese Corporation

- DuPont

- Elastron TPE

- FM Plastics

- HEXPOL AB

- Kumho Polychem

- LCY

- LOTTE Chemical CORPORATION

- Mitsubishi Chemical Group Corporation

- Mitsui Chemicals Inc.

- Orbia(Alphagary)

- Ravago

- RTP Company

- Shandong Dawn Polymer Materials Co. Ltd

- Teknor Apex

- Trinseo

- Zylog ElastoComp LLP

第7章 市場機會與未來展望

Thermoplastic Vulcanizate market size in 2026 is estimated at 476.56 kilotons, growing from 2025 value of 452.75 kilotons with 2031 projections showing 616.2 kilotons, growing at 5.26% CAGR over 2026-2031.

This steady expansion reflects a decisive shift by automakers, medical-device firms, and consumer-goods producers toward recyclable elastomers that offer thermoset-like performance at lower overall system costs. Lightweighting imperatives in electric vehicles, regulatory pressure for circular-economy compliance, and rising demand for soft-touch finishes in electronics amplify adoption across regions. Cost analyses show that TPVs can lower part manufacturing expenses by more than 60% versus EPDM rubber, mainly through shorter cycle times and elimination of post-curing steps. Suppliers now promote bio-based and recycled-content grades that cut cradle-to-gate carbon footprints by as much as 50%, providing a credible path for original equipment manufacturers (OEMs) to meet science-based emissions targets. These attributes position the Thermoplastic Vulcanizate market as a material solution of choice, while propylene and EPDM feedstock volatility limits the attractiveness of legacy thermosets.

Global Thermoplastic Vulcanizate (TPV) Market Trends and Insights

Rising Lightweighting Demand from Automotive OEMs

Automakers accelerate material substitution to cut vehicle mass and meet carbon-dioxide fleet targets. TPV components weigh roughly 30% less than comparable EPDM seals yet maintain compression-set resilience, allowing battery-electric models to gain additional driving range. Recent dynamic-vulcanization advances have closed the gap in long-term fatigue performance, enabling TPVs to replace thermosets in door, glass-run, and sunroof systems without altering tooling. Regulatory pressure under the European Union's 2025 CO2 cap magnifies this shift, ensuring sustained demand inflow to the Thermoplastic Vulcanizate market.

Surge in TPV-based Soft-Touch Parts for Consumer Electronics

Handheld electronics brands adopt TPVs to deliver a premium tactile feel while avoiding paint or over-mold steps that complicate recycling streams. The resin's direct-moldable surface eliminates secondary coatings and drops total part cost for grips, bumpers, and wearable-device housings. Integrating 25%-40% recycled content further slashes embodied emissions, and Asia-based contract molders can use standard injection machines, reducing capital barriers. Faster cycle times and compliance with RoHS and REACH regulations reinforce momentum.

Inferior Long-Term Chemical/Wear Resistance vs. Thermoset Rubber

High-acid, oil-field, or abrasive environments still favor specialty thermosets because TPVs can suffer gradual property loss beyond 150 °C. Although polyacrylate-modified TPVs extend service life, they remain a secondary choice for aggressive-media service lines.

Other drivers and restraints analyzed in the detailed report include:

- OEM Shift Toward Recyclable Elastomeric Materials

- Emergence of Bio-based TPV Grades

- Lack of Closed-Loop Recycling Infrastructure for TPV Scrap

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Standard EPDM/PP compounds accounted for 45.05% of the Thermoplastic Vulcanizate market size in 2025, thanks to lower cost and broad tooling compatibility. The mature formulations meet the majority of weather-seal and interior-trim specifications, offering OEM-qualified performance certifications. Manufacturers leverage twin-screw compounding lines to balance crosslink density and polypropylene melt-flow, enabling tight dimensional tolerances at high throughputs. As a result, global processors continue to prioritize standard grades for programs where cost competitiveness outweighs incremental performance gains.

Volume growth will increasingly originate from bio-based and recycled-content offerings that align with corporate emissions goals. Bio-attributed TPVs are projected to post the fastest 6.76% CAGR, aided by European mandates for circular-economy compliance. Recycled-content variants containing up to 40% post-industrial material give OEMs an immediate path to hit recycled-material thresholds without redesigning parts. High-temperature TPV grades remain niche but strategic, supplying turbo-charger hoses and under-hood gaskets that demand 150 °C continuous use.

The Thermoplastic Vulcanizate Report is Segmented by Product Type (Standard EPDM/PP TPV, High-Performance/Heat-Resistant TPV, and More), Application (Sealing Systems and Weather-Strips, Interior and Exterior Trim, and More), End-User Industry (Automotive, Building and Construction, Consumer Goods, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Volume (Kilo Tons).

Geography Analysis

Asia-Pacific led with a 45.70% revenue share in 2025 and is forecast to grow at 6.10% CAGR, outpacing other regions. China's annual production of over 25 million vehicles underpins surging demand for TPV weatherstrips, while Japan's material-science expertise spurs specialty-grade development. India's emerging car market adds incremental volume through local extrusion houses that substitute EPDM profiles with TPV to trim cycle times. Regional feedstock integration lowers polypropylene and EPDM costs, creating a unit-cost advantage that drives exports to Europe and North America. Avient's 2025 expansion of medical-grade TPU output in China evidences supplier commitment to serve Asia-based medical-device OEMs.

North America records steady demand concentrated in Michigan-centric automotive hubs and Mexico's expanding assembly corridors. The Inflation Reduction Act's EV incentives accelerate battery-pack production, boosting call-offs for low-conductivity TPV coolant hoses. Celanese's newly qualified compounder in Suzhou provides Asian-sourced Santoprene pellets for local and export molding operations, illustrating cross-regional supply-chain design. Europe remains the bellwether for sustainability adoption, where ISCC-PLUS-certified TPVs enjoy double-digit growth in premium vehicle lines and green-building facades. The End-of-Life Vehicles Directive pushes OEMs to document recycled content, lifting demand for PCR-infused TPV grades. South America, the Middle East, and Africa together occupy a smaller but rising stake in the Thermoplastic Vulcanizate market. Brazil's revived auto output sparks investments in local extrusion plants, while Gulf-region producers consider downstream TPV compounding leveraging abundant C3 and diene feedstocks. Africa's construction boom increases consumption of TPV water-stop profiles in infrastructure projects, yet limited recycling logistics delay full circularity benefits.

- Avient Corporation

- Celanese Corporation

- DuPont

- Elastron TPE

- FM Plastics

- HEXPOL AB

- Kumho Polychem

- LCY

- LOTTE Chemical CORPORATION

- Mitsubishi Chemical Group Corporation

- Mitsui Chemicals Inc.

- Orbia (Alphagary)

- Ravago

- RTP Company

- Shandong Dawn Polymer Materials Co. Ltd

- Teknor Apex

- Trinseo

- Zylog ElastoComp LLP

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Lightweighting Demand from Global Automotive OEMs

- 4.2.2 Surge in TPV-Based Soft-Touch Parts for Consumer Electronics

- 4.2.3 OEM Shift Toward Recyclable Elastomeric Materials

- 4.2.4 Expansion of EV Battery-Pack Sealing Applications

- 4.2.5 Emergence of Bio-Based TPV Grades

- 4.3 Market Restraints

- 4.3.1 Volatility in Propylene and EPDM Feedstock Prices

- 4.3.2 Inferior Long-Term Chemical/Wear Resistance Vs. Thermoset Rubber

- 4.3.3 Lack of Closed-Loop Recycling Infrastructure for TPV Scrap

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Standard EPDM/PP TPV

- 5.1.2 High-Performance / Heat-Resistant TPV

- 5.1.3 Bio-based TPV

- 5.1.4 Recycled-content TPV

- 5.2 By Application

- 5.2.1 Sealing Systems and Weather-strips

- 5.2.2 Interior and Exterior Trim

- 5.2.3 Under-the-Hood Components

- 5.2.4 Hose and Tubing

- 5.2.5 Wire and Cable

- 5.2.6 Medical Devices

- 5.2.7 Consumer and Sporting Goods Parts

- 5.3 By End-User Industry

- 5.3.1 Automotive

- 5.3.2 Building and Construction

- 5.3.3 Consumer Goods

- 5.3.4 Healthcare

- 5.3.5 Other End-user Industries

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Indonesia

- 5.4.1.6 Malaysia

- 5.4.1.7 Thailand

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Nordic Countries

- 5.4.3.7 Russia

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 Qatar

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 South Africa

- 5.4.5.7 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Avient Corporation

- 6.4.2 Celanese Corporation

- 6.4.3 DuPont

- 6.4.4 Elastron TPE

- 6.4.5 FM Plastics

- 6.4.6 HEXPOL AB

- 6.4.7 Kumho Polychem

- 6.4.8 LCY

- 6.4.9 LOTTE Chemical CORPORATION

- 6.4.10 Mitsubishi Chemical Group Corporation

- 6.4.11 Mitsui Chemicals Inc.

- 6.4.12 Orbia (Alphagary)

- 6.4.13 Ravago

- 6.4.14 RTP Company

- 6.4.15 Shandong Dawn Polymer Materials Co. Ltd

- 6.4.16 Teknor Apex

- 6.4.17 Trinseo

- 6.4.18 Zylog ElastoComp LLP

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

熱塑性硫化橡膠市場機會、成長要素、產業趨勢分析及2026-2035年預測。

熱塑性硫化橡膠市場機會、成長要素、產業趨勢分析及2026-2035年預測。 全球熱塑性硫化橡膠市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球熱塑性硫化橡膠市場規模、佔有率、趨勢和成長分析報告(2026-2034) 熱塑性硫化橡膠市場規模、佔有率和趨勢分析報告:按等級、加工方法、應用、地區和細分市場預測(2026-2033 年)

熱塑性硫化橡膠市場規模、佔有率和趨勢分析報告:按等級、加工方法、應用、地區和細分市場預測(2026-2033 年) 熱塑性硫化橡膠市場規模、佔有率和成長分析(按等級、加工方法和地區分類)-2026-2033年產業預測

熱塑性硫化橡膠市場規模、佔有率和成長分析(按等級、加工方法和地區分類)-2026-2033年產業預測 全球熱塑性硫化橡膠(TPV)市場

全球熱塑性硫化橡膠(TPV)市場 動態交聯熱可塑性橡膠(TPV) 市場,依類型、應用進行的需求分析,預測至 2034 年熱塑性硫化劑市場:現狀分析與未來預測 (2024年~2032年)動態交聯熱塑性彈性體(TPV)市場(2018-2034)全球熱塑性硫化橡膠(TPV)市場規模:依應用、競爭格局、區域格局、預測

動態交聯熱可塑性橡膠(TPV) 市場,依類型、應用進行的需求分析,預測至 2034 年熱塑性硫化劑市場:現狀分析與未來預測 (2024年~2032年)動態交聯熱塑性彈性體(TPV)市場(2018-2034)全球熱塑性硫化橡膠(TPV)市場規模:依應用、競爭格局、區域格局、預測