|

市場調查報告書

商品編碼

1934650

歐洲油漆和塗料:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)Europe Paints And Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

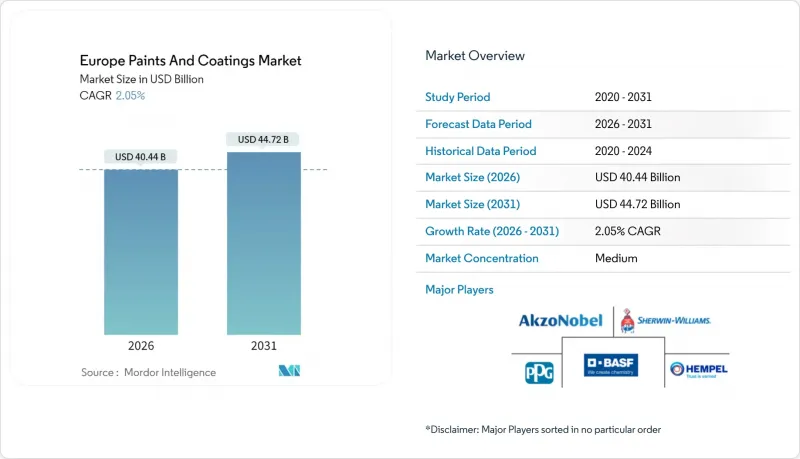

歐洲油漆和塗料市場預計將從 2025 年的 396.3 億美元成長到 2026 年的 404.4 億美元,預計到 2031 年將達到 447.2 億美元,2026 年至 2031 年的複合年成長率為 2.05%。

歐洲塗料市場在西方國家日益成熟,但維修活動、電動車生產和可再生能源基礎設施的建設確保了高價值需求的穩定成長。優質水性配方產品在提高施工效率的同時,也滿足了嚴格的VOC(揮發性有機化合物)法規,從而推動了市場成長。原料成本,尤其是二氧化鈦成本的壓力,正在促使企業調整籌資策略。對中國產品徵收的反傾銷稅促使企業尋求多元化的採購管道。區域分散抑制了價格競爭,但跨國公司正在加速工廠整合和技術升級,以捍衛市場佔有率。競爭的焦點正轉向永續性舉措,生物基黏合劑和奈米技術防護系統正從試點階段走向商業化應用。

歐洲塗料市場趨勢與分析

建築業維修熱潮推動了需求成長

受歐洲綠色交易推動的維修計畫將促使3,500萬棟建築在2030年前維修,其每平方公尺特種塗料消耗量將顯著超過新建計劃。室內底漆、彈性密封劑和低VOC面漆是節能磚石維修的標準配備。建築塗料開發商優先考慮透氣性和防潮性能,以滿足更嚴格的隔熱法規要求,同時避免歷史建築基材中水分滯留。公共部門津貼為中小企業創造了就業機會,而大型供應商憑藉整合配色系統和即時物流網路,在高階市場佔據主導地位。由於法國、義大利和西班牙的老舊住宅存量需要多層塗層系統才能達到U值目標,歐洲油漆和塗料市場正從中受益。零售專家也指出,由於消費者越來越傾向選擇抗菌和防污塗料,以創造更健康的家居環境,平均購買價格也在上漲。

加速風力發電機安裝

預計到2030年,離岸風力發電裝置容量將成長十倍,達到300吉瓦,這意味著每颱風力發電機塔筒、機艙和葉片都需要200-300公升耐腐蝕環氧聚氨酯複合塗料。防護塗料製造商正在研發可在北海低溫環境下固化的底漆,從而實現全年施工。資產所有者要求25年的耐久性質保,並且對附著力促進劑和含鋅犧牲層(用於減緩塗層下鏽蝕的蔓延)的興趣日益濃厚。歐洲塗料市場正在投資自動化混合撬裝設備和多成分噴塗設備,以實現高膜厚和最小過噴。塗料製造商正透過遠端監控和分析技術預測維護週期,從而獲得服務合約收入。預計波羅的海地區也將出現類似的成長,芬蘭和愛沙尼亞核准多個吉瓦級計劃,這將推動耐冰面漆的需求。

原料價格波動給利潤率帶來壓力。

目前,二氧化鈦佔許多配方商直接生產成本的40%,而對中國進口二氧化鈦徵收的每公斤0.25至0.74歐元的反傾銷稅,正促使他們轉向價格更高的歐洲產品。為了穩定供應,大型企業集團正透過與沙烏地阿拉伯和墨西哥的氯化鈦生產商簽訂多年承購協議來對沖供應風險。小型生產商則加速採用金紅石-鐵白雲石混合技術,該技術可在不降低遮蓋力的前提下增強遮蓋力。這導致歐洲塗料市場垂直合作日益加強,多家原始設備製造商(OEM)獲得了顏料的直接配額,從而保護塗料合作夥伴免受現貨市場價格波動的影響。創新預算正轉向最佳化填料技術,一些顏色穩定性計劃則被推遲。

細分市場分析

丙烯酸塗料將繼續佔據歐洲塗料市場最大佔有率,預計到2025年將佔銷售額的38.32%,年複合成長率為3.52%。其化學結構的極性使其具有良好的水性,成為符合歐盟法規的標準之選。醇酸塗料因其美觀的深光澤,在手工木製品保護領域佔據了一席之地,但由於乾燥時間長、溶劑含量高,其年銷售量正在下降。

環氧樹脂在貨艙襯裡和橋面塗料領域仍然佔據著不可替代的地位,其在歐洲油漆和塗料市場的佔有率保持在12.35%,儘管由於資產所有者延長了維護週期,其成長已趨於平緩。聚氨酯樹脂在風力發電機葉片生產線中的需求不斷成長,這些生產線優先考慮斷裂伸長率達到10%或以上的產品。丙烯酸樹脂在汽車透明塗層配方中也取得了進展,超支化丙烯酸樹脂在不增加黏度的情況下提供了耐刮擦性。聚酯樹脂因其快速固化特性而備受青睞,並受益於汽車鋁飾件的流行,從而提高了生產效率,可實現一步塗覆。

歐洲塗料市場報告按樹脂類型(丙烯酸樹脂、醇酸樹脂、聚氨酯樹脂等)、技術(水性塗料、溶劑型塗料、粉末塗料、UV固化塗料)、終端用戶行業(建築、汽車、木材、防護塗料等)以及地區(德國、英國、法國、義大利、西班牙、俄羅斯、土耳其、歐洲其他地區)進行細分。市場預測以美元(USD)為以金額為準。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 建築業維修熱潮提振了需求

- 加速風力發電機安裝

- 新型電動車塗料需求不斷成長

- 航太和海洋領域的需求不斷成長

- 在半導體和電子設備塗層中的應用日益廣泛

- 市場限制

- 原料價格波動給利潤率帶來壓力。

- 加強對揮發性有機化合物排放的監管

- 西歐各地熟練安裝人員短缺

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 依樹脂類型

- 丙烯酸纖維

- 醇酸樹脂

- 聚氨酯

- 環氧樹脂

- 聚酯纖維

- 其他樹脂類型(乙烯基樹脂、氟樹脂等)

- 透過技術

- 水溶液

- 溶劑型

- 粉末塗料

- 紫外線固化塗料

- 按最終用戶行業分類

- 建築學

- 車

- 木頭

- 保護漆

- 一般工業

- 運輸

- 包裝

- 按地區

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 土耳其

- 其他歐洲地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- ADLER

- Akzo Nobel NV

- Axalta Coating Systems, LLC

- BASF

- Beckers Group

- Brillux GmbH & Co. KG

- CIN, SA

- Cromology

- DAW SE

- Hempel A/S

- Jotun

- Kansai Paint Co. Ltd.

- Mankiewicz Gebr. & Co.

- Metlac SpA

- PPG Industries Inc.

- RPM International Inc.

- Sniezka SA

- Stahl Holdings BV

- Teknos Group

- The Sherwin-Williams Company

- Tiger Surface Technology New Materials(Suzhou)Co., Ltd.

- Tikkurila

第7章 市場機會與未來展望

The Europe Paints And Coatings market is expected to grow from USD 39.63 billion in 2025 to USD 40.44 billion in 2026 and is forecast to reach USD 44.72 billion by 2031 at 2.05% CAGR over 2026-2031.

The European paints and coatings market is maturing in Western economies, yet renovation activity, electric-vehicle output, and renewable-energy infrastructure ensure a steady volume of high-value demand. Growth remains anchored in premium, water-borne formulations that satisfy stringent VOC caps while improving application efficiency. Raw-material cost pressures, notably for titanium dioxide, are reshaping sourcing strategies as anti-dumping duties on Chinese grades compel procurement diversification. Regional fragmentation keeps pricing disciplined, but multinationals are accelerating factory consolidations and technology upgrades to defend their share. Competition now hinges on sustainability credentials, with bio-based binders and nano-enabled protective systems moving from pilot scale toward commercial adoption.

Europe Paints And Coatings Market Trends and Insights

Construction-Sector Renovation Boom Boosts Demand

Renovation programmes backed by the European Green Deal are stimulating refurbishment of 35 million buildings by 2030, lifting specialty-coatings consumption per square metre well above that of new-build projects. Interior primers, elastomeric sealers, and low-VOC topcoats are now standard specifications for masonry upgrades that target energy efficiency. Architectural formulators emphasise breathability and moisture-barrier performance to meet stricter thermal regulations without trapping humidity in historic substrates. Public-sector grants channel work toward SMEs, yet large suppliers dominate premium segments through integrated tint systems and just-in-time logistics networks. The European paints and coatings market benefits as older housing stock across France, Italy, and Spain requires multiple-layer coating systems to achieve U-value targets. Retail professionals also report higher average ticket values as householders opt for antibacterial and stain-resistant finishes to enhance indoor wellness.

Accelerating Wind-Turbine Installations

Offshore wind capacity is set to jump tenfold to 300 GW by 2030, and every turbine tower, nacelle, and blade demands corrosion-resistant epoxy-polyurethane stacks of 200-300 litres per unit. Protective coatings suppliers now develop surface-tolerant primers that cure at low North Sea temperatures, allowing year-round deployment. Asset owners specify 25-year durability warranties, intensifying focus on adhesion promoters and sacrificial zinc-rich layers that slow under-film rust creep. The European paints and coatings market attracts investment in automated mixing skids and plural-component spray equipment that achieve high-build thickness with minimal overspray. Coating producers capture service-contract revenue through remote-monitoring analytics that predict maintenance intervals. Growth in the Baltic Sea mirrors North Sea momentum as Finland and Estonia approve multi-GW projects, extending demand for ice-resistant topcoats.

Volatile Feedstock Prices Squeezing Margins

Titanium dioxide now represents 40% of direct production costs for many formulators, and anti-dumping levies of EUR 0.25-0.74 kg on Chinese imports have forced substitution toward higher-priced European capacity. To stabilise procurement, large groups hedge through multi-year offtake contracts with chloride-route producers in Saudi Arabia and Mexico. Smaller firms accelerate rutile-ankerite blends that extend hiding power without compromising opacity. The European paints and coatings market thus witnesses greater vertical cooperation; several OEMs secure direct pigment allocations to insulate their coating partners from spot-market spikes. Innovation budgets shift toward extender-technology optimisation, delaying certain colour-stability projects.

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand for Coatings from New Electric Vehicles

- Rising Demand from the Aerospace and Marine Sector

- Stricter Regulations Related to VOC Emissions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Acrylic systems delivered 38.32% of 2025 sales and are pacing a 3.52% CAGR, commanding the largest slice of the Europe paints and coatings market. The chemistry's polarity promotes water dispersion, making it the default for EU regulatory compliance. Alkyds cling to artisan woodcare niches because of depth-of-gloss aesthetics; however, longer drying times and higher solvent content shrink their volume annually.

Epoxies remain irreplaceable for cargo hold linings and bridge decks, where Europe's paints and coatings market share for the class stays at 12.35% but with flat growth as asset owners elongate maintenance cycles. Polyurethanes flourish in wind-blade production lines that value elongation-at-break above 10%. Acrylics also advance in automotive clearcoat blends, where hyper-branched variants deliver scratch resistance without raising viscosity. Polyester resins, preferred in powder coatings, ride automotive aluminium-trim popularity, with throughput gains from faster curing profiles that permit single-pass application.

The Europe Paints and Coatings Report is Segmented by Resin Type (Acrylic, Alkyd, Polyurethane, and More), Technology (Water-Borne, Solvent-Borne, Powder Coatings, and UV-Cured Coatings), End-User Industry (Architectural, Automotive, Wood, Protective Coatings, and More), and Geography (Germany, United Kingdom, France, Italy, Spain, Russia, Turkey, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- ADLER

- Akzo Nobel N.V.

- Axalta Coating Systems, LLC

- BASF

- Beckers Group

- Brillux GmbH & Co. KG

- CIN, S.A.

- Cromology

- DAW SE

- Hempel A/S

- Jotun

- Kansai Paint Co. Ltd.

- Mankiewicz Gebr. & Co.

- Metlac SpA

- PPG Industries Inc.

- RPM International Inc.

- ?nie?ka SA

- Stahl Holdings B.V.

- Teknos Group

- The Sherwin-Williams Company

- Tiger Surface Technology New Materials (Suzhou) Co., Ltd.

- Tikkurila

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Construction-Sector Renovation Boom Boosts Demand

- 4.2.2 Accelerating Wind-Turbine Installations

- 4.2.3 Growing Demand for Coatings from New Electric Vehicles

- 4.2.4 Rising Demand from the Aerospace and Marine Sector

- 4.2.5 Increasing Utilization from Semiconductor and Electronics Coatings

- 4.3 Market Restraints

- 4.3.1 Volatile Feedstock Prices Squeezing Margins

- 4.3.2 Stricter Regulations Related to VOC Emissions

- 4.3.3 Skilled-Applicator Labour Shortage Across Western Europe

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Acrylic

- 5.1.2 Alkyd

- 5.1.3 Polyurethane

- 5.1.4 Epoxy

- 5.1.5 Polyester

- 5.1.6 Other Resin Types (Vinyl, Fluoropolymers, etc.)

- 5.2 By Technology

- 5.2.1 Water-borne

- 5.2.2 Solvent-borne

- 5.2.3 Powder Coatings

- 5.2.4 UV-Cured Coatings

- 5.3 By End-User Industry

- 5.3.1 Architectural

- 5.3.2 Automotive

- 5.3.3 Wood

- 5.3.4 Protective Coatings

- 5.3.5 General Industrial

- 5.3.6 Transportation

- 5.3.7 Packaging

- 5.4 By Geography

- 5.4.1 Germany

- 5.4.2 United Kingdom

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 Russia

- 5.4.7 Turkey

- 5.4.8 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ADLER

- 6.4.2 Akzo Nobel N.V.

- 6.4.3 Axalta Coating Systems, LLC

- 6.4.4 BASF

- 6.4.5 Beckers Group

- 6.4.6 Brillux GmbH & Co. KG

- 6.4.7 CIN, S.A.

- 6.4.8 Cromology

- 6.4.9 DAW SE

- 6.4.10 Hempel A/S

- 6.4.11 Jotun

- 6.4.12 Kansai Paint Co. Ltd.

- 6.4.13 Mankiewicz Gebr. & Co.

- 6.4.14 Metlac SpA

- 6.4.15 PPG Industries Inc.

- 6.4.16 RPM International Inc.

- 6.4.17 Sniezka SA

- 6.4.18 Stahl Holdings B.V.

- 6.4.19 Teknos Group

- 6.4.20 The Sherwin-Williams Company

- 6.4.21 Tiger Surface Technology New Materials (Suzhou) Co., Ltd.

- 6.4.22 Tikkurila

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Nano-Enabled Functional Coatings

- 7.3 Bio-based and Carbon-Negative Binders

煅燒頁岩市場:2026-2032年全球市場預測(依產品類型、應用、終端用戶產業及通路分類)

煅燒頁岩市場:2026-2032年全球市場預測(依產品類型、應用、終端用戶產業及通路分類) 2026-2030年全球油漆塗料市場

2026-2030年全球油漆塗料市場 塗料市場分析及預測(至2035年):依類型、產品類型、技術、應用、材料類型、製程、最終用戶、功能、安裝類型及解決方案分類

塗料市場分析及預測(至2035年):依類型、產品類型、技術、應用、材料類型、製程、最終用戶、功能、安裝類型及解決方案分類 亞太地區油漆塗料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

亞太地區油漆塗料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 日本工業塗料市場規模、佔有率、趨勢及預測(依產品類型、應用、最終用戶及地區分類),2026-2034年

日本工業塗料市場規模、佔有率、趨勢及預測(依產品類型、應用、最終用戶及地區分類),2026-2034年 2026年全球建築塗料市場報告2026年全球油漆塗料市場報告2026年全球液體粉末和特殊塗料設備市場報告

2026年全球建築塗料市場報告2026年全球油漆塗料市場報告2026年全球液體粉末和特殊塗料設備市場報告 油漆和塗料市場:2030 年全球預測(按樹脂類型、技術、終端用途產業和地區分類)

油漆和塗料市場:2030 年全球預測(按樹脂類型、技術、終端用途產業和地區分類) 塗料市場-全球產業規模、佔有率、趨勢、機會和預測:按技術、樹脂、銷售管道、最終用戶、地區和競爭對手分類,2021-2031年

塗料市場-全球產業規模、佔有率、趨勢、機會和預測:按技術、樹脂、銷售管道、最終用戶、地區和競爭對手分類,2021-2031年