|

市場調查報告書

商品編碼

1934615

化妝品包裝器材:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Cosmetic Packaging Machinery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

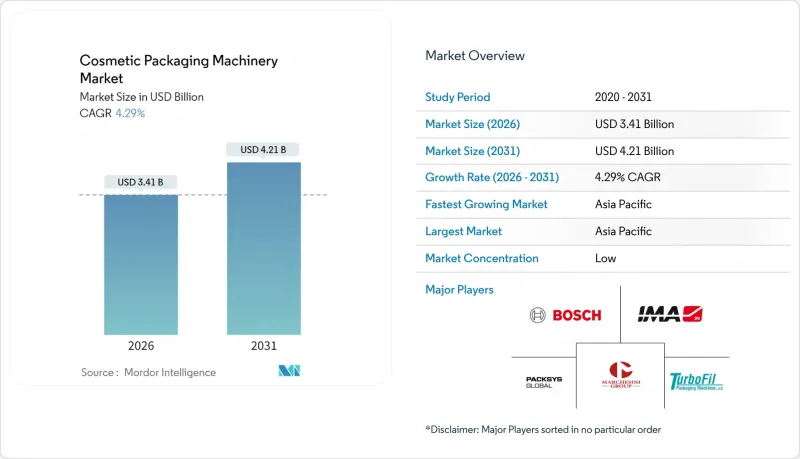

預計到 2026 年,化妝品包裝器材市場規模將達到 34.1 億美元,高於 2025 年的 32.7 億美元。

預計到 2031 年將達到 42.1 億美元,2026 年至 2031 年的複合年成長率為 4.29%。

穩定成長反映出市場對能夠適應各種包裝材料和產品規格的自動化、永續性線的需求日益成長。電子商務對輕巧、易於運輸包裝的需求,以及日益嚴格的回收目標,迫使製造商部署能夠快速切換軟性薄膜、可重複填充罐和高檔玻璃容器的設備。投資重點集中在人工智慧驅動的檢測設備和電動伺服驅動器上,這些設備能夠提高運轉率、減少對勞動力的依賴並降低能源消耗。競爭活動主要圍繞著收購展開,旨在擴展填充、密封和視覺檢測能力。同時,零件價格波動和出口限制帶來了成本和前置作業時間的風險。

全球化妝品包裝器材市場趨勢與洞察

對個人護理和美容產品的需求不斷成長

預計2024年至2025年,香水、護膚和高階彩妝系列將實現兩位數的銷售成長,因為製造商正致力於瓶型、瓶蓋和裝飾效果的多樣化。諸如Lumson的1500種設計組合等新產品,需要具備水性漆塗層、全像圖應用和符合人體工學的填充功能的機器。雅詩蘭黛在2024年向生物基聚合物的轉型表明,市場需要能夠處理非常規樹脂並同時確保產品完整性的精密填充、密封和貼標設備。設備供應商正擴大提供承包模組,使化妝品製造商能夠在廣泛的黏度範圍內同步進行填充、封蓋和檢測。持續的奢侈品趨勢將繼續推動對能夠靈活處理從高階玻璃容器到輕質包裝袋等各種產品的多功能生產線的高需求。

擴大工業自動化和智慧包裝生產線

由於85%的自動化公司都面臨熟練工人短缺的問題,化妝品製造商正在加速推進生產線的全面自動化。 Syntegon的SPC 1000系統減少了80%的人工干預,每年節省300小時的生產時間。電動線性致動器降低了能耗並縮小了安裝空間。玫琳凱2024年睫毛膏生產線安裝案例研究顯示:整合式機器人、分散式驅動裝置和數位雙胞胎縮短了產品規格切換時間,並提高了設備綜合效率(OEE)。對即插即用模組日益成長的需求,促使中型企業也開始引入協作機器人進行檢測、碼垛和清潔等工序,在擴展自動化能力的同時,降低了再培訓成本。

高初始資本投入

一條完整的高速生產線造價在 50 萬美元到 200 萬美元之間,迫使許多中小型製造商分階段購買或租賃。儘管 PMMI 預測到 2027 年訂單將保持強勁成長,但不斷上漲的利率將投資回收期延長至三到五年。根據 2024 年高峰會 Packaging 的一項調查,企業目前正著眼於逐步實現自動化,優先考慮貼標和裝箱,而非目視檢測。為此,設備開發商正在提供入門級熱成型機和風險共擔服務契約,以降低准入門檻。

細分市場分析

到2025年,受乳霜、精華液和擦拭巾產品對集稱重、封口和製袋於一體的設備需求的推動,成型-灌裝-封口一體機將佔據化妝品包裝器材市場28.03%的佔有率。 IMA的小袋線擁有16條生產線,每分鐘可完成80個循環,充分滿足護膚和香水填充所需的產能。包裝和捆紮設備將以6.56%的複合年成長率成為成長最快的設備,這主要得益於電商通路對具有抗衝擊保護功能的多件裝產品的需求。目前,所有灌裝機均已整合人工智慧檢測模組,確保產品達到高階品質。隨著可重複填充產品的普及,封蓋、裝盒和裝箱設備的需求將保持穩定。

對柔軟性薄膜的持續投資促使機械製造商改進生物基複合材料的溫度控制和封條輪廓。雷射劃線技術的進步提高了開啟性,同時又不影響阻隔性。隨著硬質包裝向軟性包裝的轉變加速,化妝品包裝器材市場受益於能夠在單一機架上同時處理三邊封小袋和立式袋的生產線。安裝在每個模組後面的視覺偵測攝影機將資料傳輸到分析儀表板,從而引導即時速度調整。

預計到2025年,全自動化生產線將佔總營收的64.87%,維持5.58%的複合年成長率,繼續保持領先地位。整合的機器人揀選、定向和封蓋速度可確保零售產品的美觀性和衛生性。 Syntegon的RMA(退貨、再製造和維護)設備支援受控的小批量生產,並允許生產商透過將人工送料器與機器人組裝相結合,逐步過渡到全自動化生產。基於振動感測器的預測性維護可減少非計劃性停機時間並延長零件壽命。

半自動化平台對於手工製品和季節性產品仍然至關重要,但隨著方便用戶使用型程式設計降低了全線應用的技術門檻,其成長已趨於平緩。自動化促進協會 (Automation Advancement Association) 的專案旨在協助營運商從外掛式填充機過渡到可與上游工程共用生產資料的全連網單元。雲端儀錶板能夠提醒管理人員注意阻塞風險,讓小規模品牌無需增加人手即可達到量販店品質。

化妝品包裝器材市場按機器類型(填充封口機、貼標機等)、自動化程度(全自動系統、半自動系統)、包裝類型(硬質容器/罐、軟管、小袋/包裝袋等)、化妝品類型(護膚品、護髮品等)和地區進行細分。市場預測以美元計價。

區域分析

到2025年,亞太地區將佔全球營收的38.05%,年複合成長率將達到7.03%,成為成長最快的地區。該地區的生產商正在整合工業4.0改裝,以保持成本優勢並滿足全球品牌審核。中國、韓國和印度的強勁內需正在推動工廠擴張,並引進西方和本地採購的機械設備。政府對智慧製造的激勵措施進一步加速了人工智慧檢測和節能驅動裝置的應用。

北美仍然是高階設備的主要採購地區。獨立品牌正湧入市場,快速印刷機、模組化灌裝機和視覺系統等產品廣受歡迎,使企業能夠以工業化的速度實現精湛的工藝創作。再生材料含量法規正推動跨國公司和合約包裝商升級設備,採用PCR樹脂和單材料複合生產線。零件生產的回流在一定程度上抵消了關稅帶來的成本上漲。

歐洲擁有最嚴格的永續性法規。當地品牌正在逐步淘汰含 PFAS 的阻隔材料,並採用數位護照進行包裝追蹤,這需要將高速數據載體整合到印刷、灌裝和封口機中。當地的原始設備製造商 (OEM) 正在率先採用伺服馬達驅動和封閉回路型CIP 清洗系統,以減少水和化學品的使用。新的化妝品工廠正在南歐和東歐興建,這些工廠既能享受稅收優惠,又能接近性歐盟市場。

在中東和非洲,隨著當地化妝品品牌從高階香水領域拓展至護膚,設備安裝量正在持續成長。針對高溫環境穩定性最佳化的承包線越來越受歡迎。在南美洲,巴西對低維護成本的柔版貼標機和製袋機的需求日益成長,這些設備即使在間歇性斷電的情況下也能運作。由於外匯波動,遠距離診斷和本地備件供應對於設備安裝至關重要。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 個人護理和美容產品需求不斷成長

- 工業自動化和智慧包裝生產線的興起

- 電子商務轉向更小的 SKU 和更靈活的包裝形式

- 永續性法規對環保包裝提出了壓力。

- 人工智慧驅動的視覺檢測可提高生產力

- 獨立化妝品品牌需要靈活、快速週轉的設備

- 市場限制

- 高初始投資

- 精密零件和鋼材價格波動

- 熟練的機電工程師短缺

- 先進伺服驅動器和感測器的出口限制

- 供應鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 競爭對手之間的競爭

- 替代品的威脅

- 主要宏觀經濟趨勢的影響

第5章 市場規模與成長預測

- 按模型

- 灌裝/封口機

- 貼標機

- 封蓋機

- 包裝和裝訂機械

- 裝盒和裝箱包裝器材

- 檢測和視覺系統

- 其他機器類型

- 按自動化級別

- 全自動系統

- 半自動化系統

- 按包裝類型

- 硬質容器和罐子

- 管狀、袋狀、小袋狀

- 瓶子、泵浦、分配器

- 軟性薄膜和包裝

- 透過化妝品

- 護膚品

- 護髮產品

- 化妝品和彩妝品

- 香水和除臭劑

- 其他個人保健產品

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東地區

- 非洲

- 南非

- 肯亞

- 其他非洲地區

- 中東

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Syntegon Technology GmbH

- IMA Industria Macchine Automatiche SpA

- Marchesini Group SpA

- Coesia SpA(PackSys Global etc.)

- ProMach Inc.

- Accutek Packaging Equipment Co.

- Krones AG

- Sidel Group

- Optima Packaging Group GmbH

- Norden Machinery AB

- Barry-Wehmiller(Pneumatic Scale Angelus)

- Uhlmann Packaging Systems

- ProSys Innovative Packaging Equipment

- TurboFil Packaging Machines LLC

- Vetraco Group

- Zhejiang Rigao Machinery Corp.

- Wimco Ltd

- Liquid Packaging Solutions Inc.

- APACKS

- Shemesh Automation

第7章 市場機會與未來展望

The cosmetic packaging machinery market size in 2026 is estimated at USD 3.41 billion, growing from 2025 value of USD 3.27 billion with 2031 projections showing USD 4.21 billion, growing at 4.29% CAGR over 2026-2031.

Steady growth mirrors rising demand for automated, sustainability-ready lines that support a widening mix of packaging materials and product formats. E-commerce pressure for lightweight, shipment-friendly packs, coupled with stricter recyclability targets, compels manufacturers to install equipment that can switch rapidly between flexible films, refillable jars, and premium glass. Investments concentrate on AI-enabled inspection and electric servo drives that lift uptime, curb labor dependence, and reduce energy use. Competitive activity centers on acquisitions that extend filling, sealing, and vision capabilities, while component price volatility and export controls create cost and lead-time risk.

Global Cosmetic Packaging Machinery Market Trends and Insights

Growing Demand for Personal Care and Beauty Products

Fragrance, skincare, and premium color lines recorded double-digit sales in 2024-2025, pushing producers to widen bottle shapes, caps, and decoration effects. New launches such as Lumson's 1,500 design combinations require machinery capable of water-based lacquering, hologram application, and ergonomic refillable features. Estee Lauder's 2024 switch to bio-based polymers illustrates the need for precise form/fill/seal and labeling units that protect product integrity while handling non-traditional resins. Equipment suppliers increasingly package turnkey modules so that beauty houses can synchronize filling, capping, and inspection across wider viscosity ranges. Continuous premiumization keeps demand high for versatile lines that can flex between luxury glass and lightweight pouches.

Increasing Industrial Automation and Smart Packaging Lines

With 85% of automation employers reporting technician shortages, beauty manufacturers accelerate full-line automation. Syntegon's SPC 1000 reduced manual interventions by 80% and freed 300 production hours annually, while electric linear actuators lowered energy use and installation space. Case implementations such as Mary Kay's 2024 mascara line show how integrated robots, decentralized drives, and digital twins shorten format changeovers and raise OEE. Growing preference for plug-and-play modules means medium-sized firms adopt collaborative robots for inspection, palletizing, and wash-down cleaning, making automated capacity accessible without prohibitive retraining.

High Upfront Capital Expenditure

Complete high-speed lines cost USD 500,000-2 million, forcing many small producers to stagger purchases or lease. While PMMI projects strong order books through 2027, higher interest rates lengthen payback periods to 3-5 years. Summit Packaging's 2024 survey showed that firms now favor phased automation where labeling and case-packing receive priority before vision inspection. Equipment developers respond with entry-level thermoformers and shared-risk service contracts to lower barriers.

Other drivers and restraints analyzed in the detailed report include:

- E-commerce Shift Toward Smaller SKUs and Flexible Formats

- Sustainability Regulations Pressuring Eco-friendly Packaging

- Volatile Prices of Precision Components and Steel

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Form/fill/seal equipment accounted for 28.03% of cosmetic packaging machinery market share in 2025, supported by demand for integrated dosing, sealing, and pouch forming across creams, serums, and wipes. IMA's sachet line reaches 80 cycles per minute on 16 lanes, illustrating throughput that skincare and fragrance fillers require. Wrapping and bundling units post the highest 6.56% CAGR because e-commerce channels need protective multi-packs that withstand shipping shocks. Inspection modules equipped with AI now pair with every filler to guarantee luxury finish. Capping, cartoning, and case packing maintain stable uptake as refillable formats enter the mainstream.

Continuous investment in flexible films means machine builders refine temperature control and seal-bar profiles for bio-based laminates. Advance in laser-score technology eases openability without sacrificing barrier. As rigid-to-flexible conversions accelerate, the cosmetic packaging machinery market benefits from lines that handle both 3-side sachets and stand-up pouches on a single frame. Vision inspection cameras mounted after each module feed analytics dashboards that guide real-time speed balancing.

Fully automatic lines held 64.87% revenue in 2025 and will keep the lead with a 5.58% CAGR. Integrated robots pick, orient, and cap at rates that preserve retail aesthetics and hygiene. Syntegon's RMA machine covers regulated microlot runs, linking manual feeders with robotic assembly so producers transition to full automation in stages. Predictive maintenance based on vibration sensors trims unplanned downtime and extends part life.

Semi-automatic platforms still matter for artisan and seasonal products but growth plateaus as user-friendly programming lowers the skill barrier for full lines. Association for Advancing Automation programs help operators move from bolt-on fillers to fully networked cells that share production data upstream. Cloud dashboards alert supervisors to jam risk, ensuring smaller brands can reach mass-retail quality without high headcount.

Cosmetic Packaging Machinery Market is Segmented by Machine Type (Form/Fill/Seal Machinery, Labeling Machinery, and More), Automation Level (Fully-Automatic Systems, Semi-Automatic Systems), Packaging Type (Rigid Containers and Jars, Tubes, Sachets and Pouches, and More), Cosmetic Product (Skin-Care Products, Hair-Care Products, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific holds 38.05% of 2025 revenue and records the fastest 7.03% CAGR. Regional producers integrate Industry 4.0 retrofits to comply with global brand audits while maintaining cost leadership. Strong domestic demand in China, South Korea, and India fuels factory expansions that source both Western and local machinery. Government incentives for intelligent manufacturing further accelerate adoption of AI inspection and energy-efficient drives.

North America remains a premium equipment buyer. Indie labels crowd the market and encourage short-run presses, modular fillers, and vision systems that maintain artisanal creativity at industrial speed. Regulations on recycled content push both multinationals and contract packers to upgrade lines for PCR resins and monomaterial laminates. Domestic reshoring of component production partially offsets tariff-related cost spikes.

Europe enforces the strictest sustainability rules. The continent's brands replace PFAS barriers and add digital passports for pack traceability, requiring printers, fillers, and sealers to integrate data carriers at high speed. OEMs here pioneer servo-electric actuation and closed-loop CIP that lower water and chemical use. Southern and Eastern Europe see green-field cosmetic plants that combine tax incentives with proximity to EU markets.

The Middle East and Africa register rising installations as local cosmetic brands expand beyond premium fragrances into skincare. Turnkey lines optimized for hot climate stability gain traction. In South America, Brazil leads demand for low-maintenance flexo labelers and pouch formers that thrive despite episodic power outages. Exchange-rate volatility makes remote diagnostic and local spares hubs critical to adoption.

- Syntegon Technology GmbH

- IMA Industria Macchine Automatiche SpA

- Marchesini Group SpA

- Coesia S.p.A (PackSys Global etc.)

- ProMach Inc.

- Accutek Packaging Equipment Co.

- Krones AG

- Sidel Group

- Optima Packaging Group GmbH

- Norden Machinery AB

- Barry-Wehmiller (Pneumatic Scale Angelus)

- Uhlmann Packaging Systems

- ProSys Innovative Packaging Equipment

- TurboFil Packaging Machines LLC

- Vetraco Group

- Zhejiang Rigao Machinery Corp.

- Wimco Ltd

- Liquid Packaging Solutions Inc.

- APACKS

- Shemesh Automation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for personal care and beauty products

- 4.2.2 Increasing industrial automation and smart packaging lines

- 4.2.3 E-commerce shift toward smaller SKUs and flexible formats

- 4.2.4 Sustainability regulations pressuring eco-friendly packaging

- 4.2.5 AI-enabled vision inspection boosts throughput

- 4.2.6 Indie cosmetic brands need agile short-run equipment

- 4.3 Market Restraints

- 4.3.1 High upfront capital expenditure

- 4.3.2 Volatile prices of precision components and steel

- 4.3.3 Shortage of skilled mechatronics technicians

- 4.3.4 Export controls on advanced servo drives and sensors

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Intensity of Competitive Rivalry

- 4.7.5 Threat of Substitutes

- 4.8 Impact of Key Macroeconomic Trends

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Machine Type

- 5.1.1 Form/Fill/Seal Machinery

- 5.1.2 Labelling Machinery

- 5.1.3 Capping Machinery

- 5.1.4 Wrapping and Bundling Machinery

- 5.1.5 Cartoning and Case-Packing Machinery

- 5.1.6 Inspection and Vision Systems

- 5.1.7 Other Machine Types

- 5.2 By Automation Level

- 5.2.1 Fully-Automatic Systems

- 5.2.2 Semi-Automatic Systems

- 5.3 By Packaging Type

- 5.3.1 Rigid Containers and Jars

- 5.3.2 Tubes, Sachets and Pouches

- 5.3.3 Bottles, Pumps and Dispensers

- 5.3.4 Flexible Films and Wraps

- 5.4 By Cosmetic Product

- 5.4.1 Skin-care Products

- 5.4.2 Hair-care Products

- 5.4.3 Make-up and Color Cosmetics

- 5.4.4 Fragrances and Deodorants

- 5.4.5 Other Personal-care Products

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 France

- 5.5.2.3 United Kingdom

- 5.5.2.4 Italy

- 5.5.2.5 Russia

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 South Korea

- 5.5.3.4 India

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 UAE

- 5.5.4.1.3 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Kenya

- 5.5.4.2.3 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Syntegon Technology GmbH

- 6.4.2 IMA Industria Macchine Automatiche SpA

- 6.4.3 Marchesini Group SpA

- 6.4.4 Coesia S.p.A (PackSys Global etc.)

- 6.4.5 ProMach Inc.

- 6.4.6 Accutek Packaging Equipment Co.

- 6.4.7 Krones AG

- 6.4.8 Sidel Group

- 6.4.9 Optima Packaging Group GmbH

- 6.4.10 Norden Machinery AB

- 6.4.11 Barry-Wehmiller (Pneumatic Scale Angelus)

- 6.4.12 Uhlmann Packaging Systems

- 6.4.13 ProSys Innovative Packaging Equipment

- 6.4.14 TurboFil Packaging Machines LLC

- 6.4.15 Vetraco Group

- 6.4.16 Zhejiang Rigao Machinery Corp.

- 6.4.17 Wimco Ltd

- 6.4.18 Liquid Packaging Solutions Inc.

- 6.4.19 APACKS

- 6.4.20 Shemesh Automation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment