|

市場調查報告書

商品編碼

1934598

氣體感測器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Gas Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

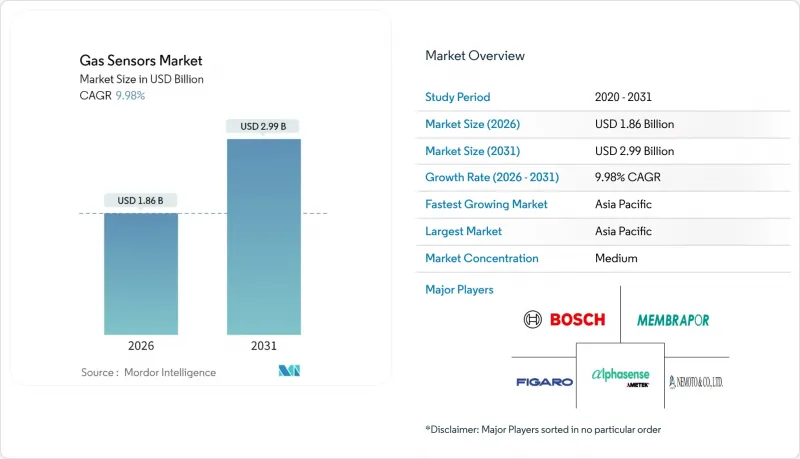

2025年氣體感測器市場價值為16.9億美元,預計到2031年將達到29.9億美元,高於2026年的18.6億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 9.98%。

歐7車載診斷系統的快速普及、日益嚴格的職場安全法規以及智慧城市空氣品質改善計畫正在加速感測器出貨量的成長。從電化學平台向微型化MEMS半導體光學平台的轉變正在推動這一趨勢,從而提高平均售價並實現基於人工智慧的選擇性。亞太地區佔據了汽車和電子產品製造地的最大區域佔有率。同時,受甲烷洩漏法規的推動,碳氫化合物和揮發性有機化合物(VOC)檢測設備成為成長最快的氣體檢測類型。現有廠商之間的整合正在重塑競爭格局,而諸如低於10 ppm的交叉靈敏度和晶圓價格波動等技術挑戰可能會限制其在對成本敏感的細分市場中的應用。

全球氣體感測器市場趨勢與洞察

日益嚴格的汽車診斷標準推動了感測器整合

歐盟7和EPA Tier 3排放標準要求汽車製造商在車輛整個生命週期內持續監測氮氧化物、顆粒物和碳氫化合物的排放,這推動了對能夠在-40°C至70°C溫度範圍內穩定運行的多氣體檢測陣列的需求。博斯的雷達感測模組和Honeywell的電池安全型電解檢測器表明,監管要求如今已涵蓋內燃機和電動平台。長達15年的耐久性要求推動了固體和非分散紅外線(NDIR)解決方案的發展,使壽命較短的電化學電池逐漸被淘汰。

職場安全法規推動工業界採用

全球對 ISO 45001、OSHA 密閉空間標準和 REACH 物質限量標準的廣泛採用,迫使工廠部署連續式固定探測器、個人徽章和攜帶式嗅探器。化工加工廠、電池生產線和半導體潔淨室正在升級為具備自校準功能並將資料記錄到雲端控制面板的 MEMS 陣列。與全廠數位雙胞胎平台的整合,實現了預測性維護,從而減少了停機時間和保險成本。

交叉敏感性問題限制了精密應用

實驗室測試表明,低成本甲醛感測元件會因臭氧和二氧化氮的干擾而產生假陽性結果,因此合格用於戶外監測站。農業氨監測器也面臨類似的干擾,而選擇性摻錫氧化銦薄膜僅在較窄的分析範圍內有效。金屬有機框架(MOF)過濾器和機器學習分類器雖然提高了識別精度,但也增加了元件成本,阻礙了它們在大眾市場穿戴式裝置中的廣泛應用。

細分市場分析

到2025年,一氧化碳偵測器仍將保持其在氣體感測器市場銷售上的主導地位,佔據26.05%的市場佔有率,這主要得益於家庭警報、鍋爐監控和車載安全應用領域的廣泛應用。然而,隨著OGMP 2.0甲烷法規強制能源公司追蹤排放,預計碳氫化合物和揮發性有機化合物(VOC)探測器將以11.95%的複合年成長率超越所有其他細分市場。這一轉變將使氣體感測器市場向多成分感測器陣列傾斜,這些感測器陣列可以同時測量甲烷、乙烷和苯,從而降低油氣營運商的整體擁有成本。新興的奈米電晶體探測器能夠以300納瓦的功率測量1至1000ppm的氫氣,其應用範圍將擴展到電池模組、無人機和住宅燃料電池系統等領域。

碳氫化合物的繁榮推動了氣體感測器市場的成長,這些感測器被環境監測承包商用於建造全市範圍的洩漏測繪專案。 OEM廠商對專用甲烷晶片的需求也推高了平均單價,部分抵消了成熟的一氧化碳和氧氣感測器價格的下降。同時,冶金和紙漿廠對缺氧檢測產品的需求保持穩定,而二氧化碳非分散紅外線(NDIR)感測器則受益於室內空氣品質法規的推動。專用的二氧化硫和硫化氫偵測器目前主要應用於煉油廠煙囪和礦井隧道,但對於高階供應商而言,它們代表著一個獨特的收入來源。

電化學感測元件仍將是工業安全儀器系統生態系統的核心,憑藉其久經考驗的現場可靠性和較低的初始成本,預計到2025年將維持31.65%的市場佔有率。市場格局正在快速變化,微機電系統(MEMS)半導體光學堆疊裝置預計將在2031年之前以15.60%的複合年成長率成長,這主要得益於其固有的選擇性、抗漂移能力以及與基於機器學習的模式庫的兼容性。這種快速成長將推動與汽車、暖通空調(HVAC)和消費性物聯網(IoT)設備相關的氣體感測器市場規模的擴大,這些設備需要無需校準的生命週期。

混合元件將光學、電化學和金屬氧化物技術整合到單一封裝中,取代了多個獨立的基板,簡化了採購流程。博世Sensortec的BME688「電子鼻」採用人工智慧技術,能夠偵測食品腐敗和森林火災徵兆。脈衝驅動的MEMS加熱器與深度神經網路結合,在識別氫氣、一氧化碳和氨氣方面實現了100%的準確率。隨著軟體的重要性日益凸顯,空中韌體更新已成為一項關鍵的差異化優勢,而以硬體為中心的競爭對手正在尋求與分析供應商建立合作關係。

氣體感測器市場按氣體類型(氧氣、一氧化碳等)、技術(電化學、光電離等)、外形規格(固定/現場安裝模組、攜帶式/手持設備等)、連接方式(有線、無線)、終端用戶行業(工業安全與製程控制、汽車動力傳動系統與暖通空調等)以及地區進行細分。市場預測以美元以金額為準。

區域分析

預計亞太地區將引領氣體感測器市場,到2025年將佔據42.90%的收入佔有率,並在2031年之前以13.72%的複合年成長率成長。中國的智慧城市計畫要求建造街區層級污染監測網路,這需要數萬個低成本節點。同時,印度推動ISO 45001認證的舉措正在加速汽車、水泥和特種化學品等行業的工廠維修。日本的氫能社會計劃推動了對亞ppm級安全監測設備的訂單,而韓國蓬勃發展的半導體產業正在為國內MEMS供應鏈奠定基礎。 Winsen Electronics和Figaro Engineering等本土主要企業正利用元件整合和勞動力套利優勢,同時服務出口和國內市場,從而鞏固其在氣體感測器市場的持續領先地位。

北美市場成熟且創新主導。美國環保署第三階段排放法規、超級發送器計畫以及加拿大75%的甲烷減量目標,都推動了對高精度洩漏偵測網路的需求。德克薩斯州和亞伯達的石油鑽探商正在部署衛星連接的光學甲烷檢測攝影機,而中西部地區的電池超級工廠擴建項目則採用多氣體電化學檢測架來保護工人。感測器原始設備製造商 (OEM) 與軟體公司成立的合資企業正在開發邊緣分析模組,這些模組可以壓縮資料量並保護智慧財產權,從而加速價值向服務的轉移。

歐洲仍以監管為中心。歐盟7排放標準正在推動輕型和重型車輛安裝氮氧化物後處理感測器,而將於2024年通過的歐盟範圍內的甲烷排放限制將要求上游能源公司持續監測火炬和壓縮機。德國一條綠色鋼鐵試點生產線正在將氧氣和氫氣探測器整合到封閉回路型燃燒器中,而斯堪地那維亞的城市正在為連接5G網路的自行車道空氣品質指示牌添加二氧化氮(NO2)和臭氧(O3)感測器。資料主權法正在推動本地伺服器和加密無線通訊協定,並影響跨國感測器叢集的採購規範。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 更嚴格的車載診斷系統(歐盟7,EPA Tier 3)

- 職場安全法規(OSHA、REACH、ISO 45001)

- 引入基於物聯網的空氣品質監測(智慧城市)

- 來自氫氣生產和燃料電池價值鏈(綠色氫氣)的快速需求

- 石油和天然氣產業甲烷外洩檢測新規(OGMP 2.0)

- 小型化MEMS多氣體陣列(小於3毫米)將推動平均售價上漲。

- 市場限制

- 混合氣體基質中濃度低於10 ppm時有交叉敏感度問題

- 矽供應不穩定推高了晶圓價格。

- 缺乏全球校準標準阻礙了相容性。

- 來自中國低成本電化學供應商的成本壓力(價格競爭)

- 價值/價值鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 依氣體類型

- 氧

- 一氧化碳(CO)

- 二氧化碳(CO2)

- 氮氧化物(NOx)

- 碳氫化合物(揮發性有機化合物/甲烷)

- 其他氣體(二氧化硫、硫化氫等)

- 透過技術

- 電化學

- 光電離(PID)

- 固體元件/MOS

- 觸媒珠

- 非色散紅外光譜(NDIR)

- 微機電系統、半導體和光學

- 按外形規格

- 固定/現場安裝模組

- 攜帶式/手持設備

- 穿戴式徽章/臂章

- 連結性別

- 有線(4-20 mA、CAN、RS-485)

- 無線(BLE、NB-IoT、LoRaWAN)

- 按最終用途行業分類

- 工業安全與製程(石油天然氣、化學)

- 汽車動力傳動系統及暖通空調

- 建築自動化/智慧家居

- 醫療和生命科學設備

- 食品飲料和低溫運輸物流

- 環境監測與智慧城市節點

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Robert Bosch GmbH

- Honeywell International Inc.-City Technology

- Dragerwerk AG & Co. KGaA

- Figaro Engineering Inc.

- Sensirion Holding AG

- AlphaSense Inc.

- Amphenol SGX Sensortech Ltd.

- Membrapor AG

- Nemoto and Co., Ltd.

- Niterra Co., Ltd.(NGK-NTK)

- Delphi Technologies(BorgWarner Inc.)

- Senseair AB(Asahi Kasei Microdevices)

- Dynament Ltd.

- Siemens AG-BT Sensors

- ABB Ltd.-Ability(TM)Gas Analytics

- Yokogawa Electric Corporation

- Emerson Electric Co.-Rosemount

- Teledyne FLIR LLC

- General Electric Company-Panametrics

- Zhengzhou Winsen Electronics Technology Co., Ltd.

第7章 市場機會與未來展望

The gas sensors market was valued at USD 1.69 billion in 2025 and estimated to grow from USD 1.86 billion in 2026 to reach USD 2.99 billion by 2031, at a CAGR of 9.98% during the forecast period (2026-2031).

Rapid adoption of Euro 7 on-board diagnostics, stricter workplace safety rules, and smart-city air-quality initiatives are accelerating sensor shipments. Momentum is reinforced by the transition from electrochemical to miniaturized MEMS-semiconductor optical platforms, which boost average selling prices and enable artificial-intelligence-based selectivity. Asia-Pacific commands the largest regional position thanks to its automotive and electronics manufacturing base, while hydrocarbon and volatile-organic-compound devices are the fastest expanding gas type on the back of methane leak regulations. Consolidation among incumbents is reshaping competitive dynamics, yet technical hurdles such as sub-10 ppm cross-sensitivity and wafer-price volatility may curb adoption in cost-sensitive niches.

Global Gas Sensors Market Trends and Insights

Stricter Vehicle On-Board Diagnostics Drive Sensor Integration

Euro 7 and EPA Tier 3 rules oblige automakers to continuously track nitrogen oxides, particulate matter, and hydrocarbons across the full vehicle life cycle, raising demand for robust, multi-gas arrays rated for -40 °C to 70 °C operation. Bosch's radar-enabled sensing modules and Honeywell's battery-safety electrolyte detectors illustrate how compliance requirements now encompass internal combustion and electric platforms alike. Long-term durability mandates of 15 years are pushing solid-state and NDIR solutions, sidelining short-lived electrochemical cells.

Work-Place Safety Mandates Spur Industrial Uptake

Global adoption of ISO 45001, OSHA's confined-space norms, and REACH substance caps compels factories to deploy continuous fixed detectors, personal badges, and portable sniffers. Chemical processors, battery-manufacturing lines, and semiconductor cleanrooms are upgrading to MEMS arrays that self-calibrate and log data to cloud dashboards. Integration with plant-wide digital-twin platforms supports predictive interventions that cut downtime and insurance premiums.

Cross-Sensitivity Challenges Limit Precision Applications

Laboratory tests show low-cost formaldehyde cells registering false positives from ozone and nitrogen dioxide, disqualifying them for outdoor stations. Agricultural ammonia monitors face similar interference, while selective tin-doped indium oxide films work only within narrow analyte windows. Metal-organic-framework filters and machine-learning classifiers improve discrimination yet add bill-of-materials cost, restraining uptake in mass-market wearables.

Other drivers and restraints analyzed in the detailed report include:

- IoT-Enabled Smart-City Deployments Accelerate Adoption

- Green-Hydrogen Value Chain Creates Premium Opportunities

- Silicon Supply Chain Volatility Pressures Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Carbon monoxide devices dominated 2025 volume thanks to household alarms, furnace monitoring, and vehicle cabin safety, securing 26.05% of the gas sensors market share. Hydrocarbon and VOC detectors, however, are projected to outpace all peers with a 11.95% CAGR as OGMP 2.0 methane rules force energy firms to track fugitive emissions. This shift rebalances the gas sensors market toward multi-species arrays that quantify methane, ethane, and benzene simultaneously, decreasing total cost of ownership for oil and gas operators. Emerging nano transistor-based detectors measuring 1-1,000 ppm hydrogen at 300 nW consumption extend monitoring into battery modules, drones, and residential fuel-cell systems.

The hydrocarbon boom widens the addressable gas sensors market size for environmental-monitoring contractors building citywide leak-mapping programs. OEM demand for methane-specific chips also boosts average revenue per unit, partially offsetting price erosion in mature carbon monoxide and oxygen categories. Meanwhile, steady oxygen-deficiency products retain relevance in metallurgy and pulp mills, and carbon-dioxide NDIR cells ride the wave of indoor-air-quality legislation. Specialty sulphur-dioxide and hydrogen-sulphide instruments stay confined to refinery stacks and mining tunnels, yet they anchor niche profitability for high-spec suppliers.

Electrochemical elements retained 31.65% share in 2025 due to proven field reliability and low initial cost, keeping them central to the industrial safety-instrument-system ecosystem. The landscape is changing quickly as MEMS-semiconductor optical stacks are forecast to clock a 15.60% CAGR to 2031, driven by their inherent selectivity, drift immunity, and compatibility with machine-learning-based pattern libraries. This surge will lift the gas sensors market size linked to automotive, HVAC, and consumer IoT endpoints that demand calibration-free life cycles.

Hybrid devices blend optical, electrochemical, and metal-oxide principles inside one package, replacing multiple discrete boards and streamlining procurement. Bosch Sensortec's BME688 "electronic nose" showcases AI-enabled signatures that flag food spoilage and forest-fire precursors. Pulse-driven MEMS heaters coupled with deep neural networks now reach 100% identification accuracy across hydrogen, carbon monoxide, and ammonia. As software weight rises, firmware over-the-air updates become a decisive differentiator, nudging hardware-centric rivals to form alliances with analytics vendors.

Gas Sensors Market Segmented by Gas Type (Oxygen, Carbon Monoxide and More), Technology (Electro-Chemical, Photo-Ionization, and More), Form Factor (Fixed/In-situ Modules, Portable/Hand-held Devices and More), Connectivity (Wired, Wireless), End-Use Industry (Industrial Safety & Process, Automotive Powertrain & HVAC and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific anchors the gas sensors market with a 42.90% revenue share in 2025 and is poised for a 13.72% CAGR through 2031. China's smart-city blueprints mandate block-level pollution grids that demand tens of thousands of low-cost nodes, while India's drive to align with ISO 45001 fuels plant-floor retrofits across automotive, cement, and specialty-chemicals sectors. Japan's hydrogen-society ambitions accelerate orders for sub-ppm safety monitors, and South Korea's semiconductor expansions seed a domestic MEMS supply chain. Local champions such as Winsen Electronics and Figaro Engineering leverage component clustering and labour arbitrage to serve both export and internal markets, underpinning sustained leadership in the gas sensors market.

North America represents a mature yet innovation-led arena. EPA Tier 3 exhaust limits, the Super Emitter Program, and Canada's 75% methane-reduction target nurture demand for high-fidelity leak-detection networks. Oil-patch operators in Texas and Alberta deploy optical methane cameras networked to satellite feeds, while battery-gigafactory expansions in the United States Midwest specify multi-gas electro-chemical racks for worker protection. Joint ventures between sensor OEMs and software firms incubate edge-analytics modules that compress data volumes and protect IP, reinforcing value migration toward services.

Europe remains regulation centric. Euro 7 drives NOx after-treatment probes across light and heavy vehicles, and the EU-wide methane regulation adopted in 2024 compels upstream energy players to monitor flares and compressors continually. Germany's green-steel pilot lines integrate oxygen and hydrogen gauges into closed-loop burners, while Scandinavian cities add NO2 and O3 cells to bikeway air-quality signs connected over 5G. Data-sovereignty statutes encourage on-premises servers and encrypted wireless protocols, shaping procurement specifications for transnational sensor fleets.

- Robert Bosch GmbH

- Honeywell International Inc. - City Technology

- Dragerwerk AG & Co. KGaA

- Figaro Engineering Inc.

- Sensirion Holding AG

- AlphaSense Inc.

- Amphenol SGX Sensortech Ltd.

- Membrapor AG

- Nemoto and Co., Ltd.

- Niterra Co., Ltd. (NGK-NTK)

- Delphi Technologies (BorgWarner Inc.)

- Senseair AB (Asahi Kasei Microdevices)

- Dynament Ltd.

- Siemens AG - BT Sensors

- ABB Ltd. - Ability(TM) Gas Analytics

- Yokogawa Electric Corporation

- Emerson Electric Co. - Rosemount

- Teledyne FLIR LLC

- General Electric Company - Panametrics

- Zhengzhou Winsen Electronics Technology Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stricter vehicle on-board diagnostics (Euro 7, EPA Tier 3)

- 4.2.2 Work-place safety mandates (OSHA, REACH, ISO 45001)

- 4.2.3 IoT-enabled air-quality monitoring roll-outs (smart cities)

- 4.2.4 Surging demand from H? production and fuel-cell value chain (green hydrogen)

- 4.2.5 Emerging methane-leak detection rules for oil and gas (OGMP 2.0)

- 4.2.6 Miniaturised MEMS-based multi-gas arrays (? 3 mm) driving ASP uplift (under-reported)

- 4.3 Market Restraints

- 4.3.1 Sub-10 ppm cross-sensitivity challenges in mixed-gas matrices (under-reported)

- 4.3.2 Silicon supply volatility inflating wafer prices

- 4.3.3 Lack of global calibration standards hampers interchangeability

- 4.3.4 Cost-pressure from low-end Chinese electro-chemical suppliers (price war)

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Gas Type

- 5.1.1 Oxygen

- 5.1.2 Carbon Monoxide (CO)

- 5.1.3 Carbon Dioxide (CO2)

- 5.1.4 Nitrogen Oxides (NOx)

- 5.1.5 Hydrocarbons (VOC/CH4)

- 5.1.6 Other Gases (SO2, H2S, etc.)

- 5.2 By Technology

- 5.2.1 Electro-chemical

- 5.2.2 Photo-ionisation (PID)

- 5.2.3 Solid-state / MOS

- 5.2.4 Catalytic Bead

- 5.2.5 Non-Dispersive Infra-Red (NDIR)

- 5.2.6 MEMS-Semiconductor Optical

- 5.3 By Form Factor

- 5.3.1 Fixed / In-situ Modules

- 5.3.2 Portable / Hand-held Devices

- 5.3.3 Wearable Badges / Patches

- 5.4 By Connectivity

- 5.4.1 Wired (4-20 mA, CAN, RS-485)

- 5.4.2 Wireless (BLE, NB-IoT, LoRaWAN)

- 5.5 By End-use Industry

- 5.5.1 Industrial Safety and?Process (Oil?and?Gas, Chemicals)

- 5.5.2 Automotive Powertrain and HVAC

- 5.5.3 Building Automation / Smart Homes

- 5.5.4 Medical and Life-science Equipment

- 5.5.5 Food, Beverage and Cold-chain Logistics

- 5.5.6 Environmental Monitoring and Smart City Nodes

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Russia

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Robert Bosch GmbH

- 6.4.2 Honeywell International Inc. - City Technology

- 6.4.3 Dragerwerk AG & Co. KGaA

- 6.4.4 Figaro Engineering Inc.

- 6.4.5 Sensirion Holding AG

- 6.4.6 AlphaSense Inc.

- 6.4.7 Amphenol SGX Sensortech Ltd.

- 6.4.8 Membrapor AG

- 6.4.9 Nemoto and Co., Ltd.

- 6.4.10 Niterra Co., Ltd. (NGK-NTK)

- 6.4.11 Delphi Technologies (BorgWarner Inc.)

- 6.4.12 Senseair AB (Asahi Kasei Microdevices)

- 6.4.13 Dynament Ltd.

- 6.4.14 Siemens AG - BT Sensors

- 6.4.15 ABB Ltd. - Ability(TM) Gas Analytics

- 6.4.16 Yokogawa Electric Corporation

- 6.4.17 Emerson Electric Co. - Rosemount

- 6.4.18 Teledyne FLIR LLC

- 6.4.19 General Electric Company - Panametrics

- 6.4.20 Zhengzhou Winsen Electronics Technology Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

氫氣相容氣體感測器市場分析及預測(至2035年):依類型、產品、技術、組件、應用、材料類型、最終用戶、功能及安裝配置分類

氫氣相容氣體感測器市場分析及預測(至2035年):依類型、產品、技術、組件、應用、材料類型、最終用戶、功能及安裝配置分類 一氧化碳偵測器市場:依產品類型、技術、安裝類型、通路和最終用戶分類-2026-2032年全球預測光學氧分析儀市場:按類型、技術、分銷管道和最終用途分類,全球預測(2026-2032年)

一氧化碳偵測器市場:依產品類型、技術、安裝類型、通路和最終用戶分類-2026-2032年全球預測光學氧分析儀市場:按類型、技術、分銷管道和最終用途分類,全球預測(2026-2032年) 2026-2030年全球氣體感測器市場空氣淨化半導體裝置市場分析及預測(至2035年):依類型、產品、技術、組件、應用、外形、材料類型、最終用戶及功能分類

2026-2030年全球氣體感測器市場空氣淨化半導體裝置市場分析及預測(至2035年):依類型、產品、技術、組件、應用、外形、材料類型、最終用戶及功能分類 全球氣體感測器市場:按產品類型、技術、連接方式、輸出類型、外形規格、氣體類型、應用和地區分類-市場預測與分析(2026-2035 年)

全球氣體感測器市場:按產品類型、技術、連接方式、輸出類型、外形規格、氣體類型、應用和地區分類-市場預測與分析(2026-2035 年) 氣體感測器市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2026-2034 年)

氣體感測器市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2026-2034 年) 2026年全球氣體感測器市場報告

2026年全球氣體感測器市場報告 氣體感測器市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、技術、應用、地區和競爭格局分類,2021-2031年)光學氧氣感測器市場:按技術、外形規格、應用、分銷管道和最終用戶產業分類-全球預測,2026-2032年

氣體感測器市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、技術、應用、地區和競爭格局分類,2021-2031年)光學氧氣感測器市場:按技術、外形規格、應用、分銷管道和最終用戶產業分類-全球預測,2026-2032年