|

市場調查報告書

商品編碼

1934593

數位鑑識:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Digital Forensics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

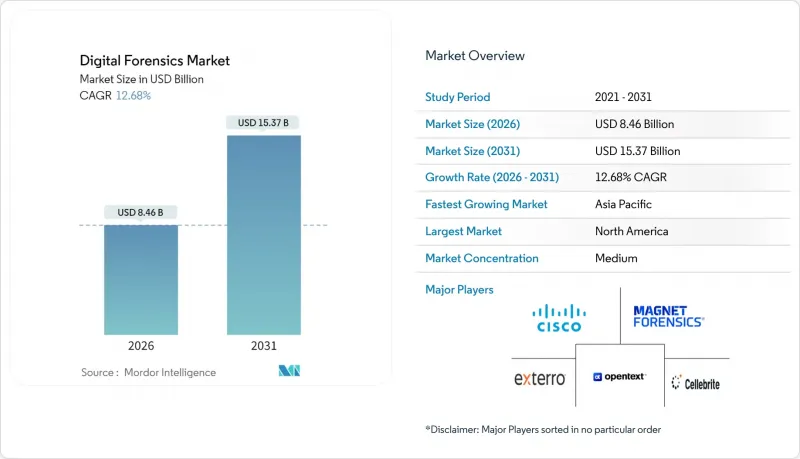

數位鑑識市場預計到 2026 年價值將達到 84.6 億美元,高於 2025 年的 75.1 億美元。

預計到 2031 年將達到 153.7 億美元,2026 年至 2031 年的複合年成長率為 12.68%。

數位取證技術與雲端原生SaaS調查、深度造假防範措施以及擴展的檢測和回應平台相融合,推動了市場成長。法律強制要求的移動取證以及公共部門的持續投資進一步支撐了市場需求。同時,預設加密和調查人員短缺造成了營運摩擦,並推動了自動化、基於雲端的證據保存技術的創新。由於現有供應商紛紛採用人工智慧和區塊鏈技術來增強自身競爭力,市場競爭格局仍保持中等程度的分散。

全球數位鑑識市場趨勢與洞察

雲端原生SaaS的快速普及催生了對雲端取證的需求。

雲端遷移正在取代傳統的磁碟鏡像,推動了取證平台的普及。這些平台能夠在分散式、多租戶環境中擷取易失性數據,同時滿足 ISO/IEC 27035-4:2024 證據可採納性標準。證據隔離要求以及自動化證據管理和追蹤的需求,促使市場對預先整合超大規模資料中心業者保全服務的解決方案產生需求。因此,提供雲端原生採集 API 的供應商正加速被企業採用,尤其是在那些跨越複雜司法管轄區的跨國公司中。

深度造假詐騙的激增推動了對高級多媒體分析的需求。

隨著機器產生的音訊和影片詐騙滲透到即時互動中,實驗室不得不以神經檢測演算法取代傳統的認證技術,這些演算法在低解析度內容上也能達到 91.82% 的準確率。銀行、金融服務和保險 (BFSI) 機構正在整合區塊鏈溯源方案以保護高價值交易,而執法機關則在投資即時篩檢工具,以便在調查取證過程中保存證據。

iOS/Android 的預設加密增加了證據收集的複雜性和成本。

基於硬體的加密已將現代設備上的資料提取成功率降低至 40% 以下,迫使人們依賴昂貴的解密工具和基於雲端的證據替代方案。小規模的機構面臨預算限制,這加劇了調查方面的差距,並引發了關於合法訪問合作的政策討論。

細分市場分析

到2025年,軟體將維持44.62%的數位取證市場佔有率,這主要得益於針對加密和雲端證據的高級分析技術。雖然實體取證對硬體的使用有限,但解密加速器將為調查處理提供支援。尋求承包擴展服務的企業將受益於託管服務,而專業服務在持續的人才短缺環境下將以14.43%的複合年成長率成長。

服務供應商正利用中小企業對取證即服務(Fensics-as-a-Service)的接受度,將事件回應和專家證詞打包提供。供應商正在整合區塊鏈譜系追蹤和人工智慧驅動的故障分類功能,以縮短分析週期,從而增強其軟體優勢。平台授權和持續服務的策略性互動提高了收入的可預測性,並使供應商能夠交叉銷售相關的安全功能。

到2025年,電腦鑑識將佔總營收的36.55%,其中雲端取證目前正經歷最快的複合年成長率(CAGR),達到12.96%,這主要得益於企業工作負載在多重雲端環境中的成長。儘管面臨加密方面的挑戰,行動取證仍將保持成長,這得益於不斷演進的繞過工具包。隨著零信任架構的普及和聯網設備的增加,網路、資料庫和物聯網調查將會擴展,因為這些調查會產生多樣化的證據流。

銀行、金融服務和保險 (BFSI) 領域的監管審核正在推動對持續雲端取證支援的需求,從而為專業的雲端原生供應商拓展了機會。隨著對軟體即服務 (SaaS) 的依賴日益加深,預計到 2031 年,雲端調查的數位取證市場規模將與電腦取證市場規模相近。因此,供應商正優先考慮基於 API 的資料收集、揮發性資料儲存以及按司法管轄區分類的資料細分,以推動雲端取證技術的普及。

區域分析

北美地區將佔2025年收入的34.65%,這得益於第14144號行政命令和強勁的聯邦預算,這些措施加速了人工智慧驅動型研究的普及。以Palantir 12億美元的政府收入為代表的公共部門平台採購,正在推動更廣泛的生態系統現代化。

亞太地區以 13.16% 的複合年成長率引領成長,這反映了電子商務的擴張和網路犯罪成本的上升,預計到 2025 年,網路犯罪成本將達到 3.3 兆美元。監管方面的改進,例如中國放寬跨境轉移豁免,正在逐步減少跨國取證服務提供者的調查摩擦。

在歐盟人工智慧法律和資料隱私法規的推動下,歐洲維持了均衡成長;中東和非洲地區正在撥出網路安全預算來保護能源和金融走廊;拉丁美洲在區域數位化政策的支持下取得了逐步進展,但受到人才短缺的限制。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 雲端原生SaaS的快速普及催生了對雲端取證的需求。

- 深度造假詐騙的激增推動了對高級多媒體分析的需求。

- 擴展型檢測與回應 (XDR) 部署需要整合式數位取證與事件回應 (DFIR) 平台。

- 美國和歐盟對執法機關的行動裝置分析要求

- 基於區塊鏈的證據鏈試點計畫推動取證軟體升級

- 聯邦政府加大網路安全投資和監管合規要求推動了取證技術的應用

- 市場限制

- iOS/Android 的預設加密會增加部署的複雜性和成本。

- 主要城市以外地區法院認證的專家證人短缺

- 工具分散和互通性差會增加中小企業的整體擁有成本。

- 由於資料居住規則(例如,中國CSL)對跨境證據轉移的限制

- 價值鏈分析

- 監理展望

- 技術展望

- 波特五力分析

- 買方的議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按組件

- 硬體

- 取證系統、設備和寫入保護設備

- 影像處理和複製設備

- 其他硬體

- 軟體

- 法醫數據分析與視覺化

- 審查和報告

- 法證解密

- 其他軟體模組

- 服務

- 專業服務

- 事件回應和違規分析

- 諮詢和培訓

- 託管取證服務

- 專業服務

- 硬體

- 按類型

- 電腦取證

- 行動裝置取證

- 網路取證

- 雲取證

- 資料庫取證

- 物聯網和嵌入式設備取證

- 透過工具

- 資料收集和存儲

- 資料恢復與重建

- 法醫數據分析

- 審查和報告

- 法證解密與密碼破解

- 按組織規模

- 主要企業

- 小型企業

- 終端用戶產業

- 政府和執法機關

- BFSI

- 資訊科技和電信

- 衛生保健

- 零售與電子商務

- 能源與公共產業

- 製造業

- 運輸/物流

- 國防/航太

- 教育

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 肯亞

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- OpenText Corporation

- Cellebrite DI Ltd.

- Exterro Inc.

- Magnet Forensics Inc.

- Cisco Systems Inc.

- FireEye Inc.(Mandiant)

- LogRhythm Inc.

- KLDiscovery Inc.

- Paraben Corporation

- MSAB AB

- Oxygen Forensics Inc.

- Kroll LLC

- Hexagon AB(Qognify)

- ADF Solutions Inc.

- BAE Systems plc

- Broadcom Inc.(Symantec Enterprise DFIR Tools)

- Micro Systemation AB

- Digital Detective Group

- Nuix Pty Ltd

- Passware Inc.

第7章 市場機會與未來展望

Digital forensics market size in 2026 is estimated at USD 8.46 billion, growing from 2025 value of USD 7.51 billion with 2031 projections showing USD 15.37 billion, growing at 12.68% CAGR over 2026-2031.

Growth pivots on cloud-native Software-as-a-Service investigations, deepfake countermeasures, and the integration of digital forensics within Extended Detection and Response platforms. Legislated mobile device extraction mandates and steady public-sector investments further underpin demand. Conversely, encryption-by-default and examiner shortages introduce operational friction yet also spur innovation in automated, cloud-based evidence preservation. Competitive dynamics remain moderately fragmented as established vendors embed artificial intelligence and blockchain-enabled chain-of-custody features to secure differentiation.

Global Digital Forensics Market Trends and Insights

Rapid Proliferation of Cloud-Native SaaS Creating Demand for Cloud Forensics

Cloud migrations are displacing traditional disk imaging, prompting the deployment of forensic platforms that capture volatile data across distributed, multi-tenant environments while meeting ISO/IEC 27035-4:2024 admissibility standards. Evidence isolation requirements and automated chain-of-custody tracking elevate demand for solutions pre-integrated with hyperscaler security services. As a result, vendors offering cloud-native acquisition APIs experience accelerated adoption among enterprises, particularly multinational corporations that navigate complex jurisdictional boundaries.

Surge in Deepfake-Enabled Fraud Driving Advanced Multimedia Analysis Needs

Machine-generated audio and video fraud now penetrates live interactions, forcing laboratories to replace legacy authentication with neural detection algorithms that achieve 91.82% accuracy on low-resolution content. BFSI institutions integrate blockchain provenance schemes to secure high-value transactions, while law-enforcement agencies invest in real-time screening tools to preserve evidentiary integrity during investigative interviews.

Encryption-by-Default on iOS/Android Elevating Acquisition Complexity and Cost

Hardware-backed encryption reduces extraction success to below 40% on recent devices, forcing reliance on premium decryption utilities and cloud-based evidence substitutes. Small agencies face budgetary barriers, widening investigative disparity and prompting policy debate on lawful access collaboration.

Other drivers and restraints analyzed in the detailed report include:

- Extended Detection and Response Adoption Necessitating Integrated DFIR Platforms

- Legislated Mobile Device Extraction Mandates in U.S. and EU Law-Enforcement

- Shortage of Court-Certified Examiners Outside Tier-1 Cities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software retained 44.62% of the digital forensics market share in 2025, underpinned by advanced analytics for encrypted and cloud evidence. Hardware usage remains niche for physical acquisitions, yet decryption accelerators support investigative throughput. Managed offerings capture enterprises seeking turnkey scalability, while professional services climb 14.43% CAGR as talent shortages persist.

Service providers capitalize on forensic-as-a-service adoption among SMEs, bundling incident response and expert testimony. Vendors integrate blockchain lineage and AI triage to compress analysis cycles, reinforcing software primacy. The strategic interplay between platform licensing and recurring services broadens revenue predictability, positioning vendors for cross-sell of adjacent security capabilities.

Computer forensics controlled 36.55% of 2025 revenue; however, cloud forensics now logs the fastest 12.96% CAGR amid multi-cloud enterprise workloads. Mobile forensics sustains growth despite encryption headwinds, supported by evolving bypass toolkits. Network, database, and IoT investigations expand as zero-trust architectures and connected devices generate diversified evidence streams.

Regulatory audits in BFSI amplify demand for continuous cloud evidence readiness, widening opportunities for specialized cloud-native vendors. Digital forensics market size for cloud investigations is poised to narrow the gap with computer forensics by 2031 as SaaS reliance deepens. Tool vendors therefore prioritize API-based collection, volatility preservation, and jurisdictional segmentation to boost adoption.

The Digital Forensics Market Report is Segmented by Component (Hardware, Software, and More), Type (Computer Forensics, Mobile Device Forensics, and More), Tool (Data Acquisition and Preservation, Forensic Data Analysis, and More), Organization Size (Large Enterprises, and Small and Medium Enterprises), End-User Vertical (BFSI, IT and Telecom and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 34.65% of 2025 revenue, aided by Executive Order 14144 and robust federal budgets that accelerate AI-driven investigative adoption. Public-sector platform procurements, exemplified by Palantir's USD 1.20 billion government revenue, cascade into broader ecosystem modernization.

Asia Pacific leads in growth at 13.16% CAGR, reflecting e-commerce expansion and rising cybercrime costs forecast at USD 3.3 trillion by 2025. Regulatory refinements, such as China's eased cross-border transfer exemptions, gradually reduce investigative friction for multinational forensics providers.

Europe sustains balanced expansion through the EU AI Act and data-privacy mandates driving privacy-preserving forensic tool demand. Middle East and Africa allocate cybersecurity budgets to defend energy and financial corridors, while Latin America shows incremental progress constrained by skill shortages yet supported by regional digitalization policies.

- OpenText Corporation

- Cellebrite DI Ltd.

- Exterro Inc.

- Magnet Forensics Inc.

- Cisco Systems Inc.

- FireEye Inc. (Mandiant)

- LogRhythm Inc.

- KLDiscovery Inc.

- Paraben Corporation

- MSAB AB

- Oxygen Forensics Inc.

- Kroll LLC

- Hexagon AB (Qognify)

- ADF Solutions Inc.

- BAE Systems plc

- Broadcom Inc. (Symantec Enterprise DFIR Tools)

- Micro Systemation AB

- Digital Detective Group

- Nuix Pty Ltd

- Passware Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Proliferation of Cloud-Native SaaS Creating Demand for Cloud Forensics

- 4.2.2 Surge in Deepfake-Enabled Fraud Driving Advanced Multimedia Analysis Needs

- 4.2.3 Extended Detection and Response (XDR) Adoption Necessitating Integrated DFIR Platforms

- 4.2.4 Legislated Mobile Device Extraction Mandates in U.S. and EU Law-Enforcement

- 4.2.5 Blockchain-Based Evidence Chain-of-Custody Pilots Boosting Forensic Software Upgrades

- 4.2.6 Federal Cybersecurity Investments and Regulatory Compliance Requirements Expanding Forensic Deployments

- 4.3 Market Restraints

- 4.3.1 Encryption-by-Default on iOS/Android Elevating Acquisition Complexity and Cost

- 4.3.2 Shortage of Court-Certified Examiners Outside Tier-1 Cities

- 4.3.3 Fragmented Tool Inter-Operability Increasing Total Cost of Ownership for SMEs

- 4.3.4 Data-Residency Rules Limiting Cross-Border Evidence Transfers (e.g., China CSL)

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.1.1 Forensic Systems, Devices and Write Blockers

- 5.1.1.2 Imaging and Duplication Devices

- 5.1.1.3 Other Hardware

- 5.1.2 Software

- 5.1.2.1 Forensic Data Analysis and Visualization

- 5.1.2.2 Review and Reporting

- 5.1.2.3 Forensic Decryption

- 5.1.2.4 Other Software Modules

- 5.1.3 Services

- 5.1.3.1 Professional Services

- 5.1.3.1.1 Incident Response and Breach Analysis

- 5.1.3.1.2 Consulting and Training

- 5.1.3.2 Managed Forensic Services

- 5.1.3.1 Professional Services

- 5.1.1 Hardware

- 5.2 By Type

- 5.2.1 Computer Forensics

- 5.2.2 Mobile Device Forensics

- 5.2.3 Network Forensics

- 5.2.4 Cloud Forensics

- 5.2.5 Database Forensics

- 5.2.6 IoT and Embedded Device Forensics

- 5.3 By Tool

- 5.3.1 Data Acquisition and Preservation

- 5.3.2 Data Recovery and Reconstruction

- 5.3.3 Forensic Data Analysis

- 5.3.4 Review and Reporting

- 5.3.5 Forensic Decryption and Password Cracking

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By End-user Vertical

- 5.5.1 Government and Law Enforcement Agencies

- 5.5.2 BFSI

- 5.5.3 IT and Telecom

- 5.5.4 Healthcare

- 5.5.5 Retail and E-commerce

- 5.5.6 Energy and Utilities

- 5.5.7 Manufacturing

- 5.5.8 Transportation and Logistics

- 5.5.9 Defense and Aerospace

- 5.5.10 Education

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Italy

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 Australia

- 5.6.4.5 South Korea

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Kenya

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 OpenText Corporation

- 6.4.2 Cellebrite DI Ltd.

- 6.4.3 Exterro Inc.

- 6.4.4 Magnet Forensics Inc.

- 6.4.5 Cisco Systems Inc.

- 6.4.6 FireEye Inc. (Mandiant)

- 6.4.7 LogRhythm Inc.

- 6.4.8 KLDiscovery Inc.

- 6.4.9 Paraben Corporation

- 6.4.10 MSAB AB

- 6.4.11 Oxygen Forensics Inc.

- 6.4.12 Kroll LLC

- 6.4.13 Hexagon AB (Qognify)

- 6.4.14 ADF Solutions Inc.

- 6.4.15 BAE Systems plc

- 6.4.16 Broadcom Inc. (Symantec Enterprise DFIR Tools)

- 6.4.17 Micro Systemation AB

- 6.4.18 Digital Detective Group

- 6.4.19 Nuix Pty Ltd

- 6.4.20 Passware Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

2026-2030年全球數位鑑識市場

2026-2030年全球數位鑑識市場 數位取證市場報告:按組件、類型、工具、最終用戶和地區分類(2026-2034 年)

數位取證市場報告:按組件、類型、工具、最終用戶和地區分類(2026-2034 年) 數位取證市場:按取證類型、組件、工具、產業和地區分類

數位取證市場:按取證類型、組件、工具、產業和地區分類 數位取證工具市場預測至2034年:按組件、取證類型、部署模式、組織規模、應用、最終用戶和地區分類的全球分析

數位取證工具市場預測至2034年:按組件、取證類型、部署模式、組織規模、應用、最終用戶和地區分類的全球分析 數位取證市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、設備、流程、部署模式和最終用戶分類

數位取證市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、設備、流程、部署模式和最終用戶分類 數位取證市場:2026-2032年全球市場預測(按解決方案、取證類型、應用、部署模式和最終用戶產業分類)

數位取證市場:2026-2032年全球市場預測(按解決方案、取證類型、應用、部署模式和最終用戶產業分類) 2026年全球數位鑑識市場報告無人機取證市場:按組件、部署方式、資料類型、無人機類型和應用程式分類,全球預測(2026-2032年)品牌建立服務市場:全球預測(2026-2032 年),按服務類型、交付管道、合作模式、組織規模、最終用戶產業和應用程式分類日本數位鑑識市場報告(按組件、類型、工具、最終用戶和地區分類,2026-2034 年)

2026年全球數位鑑識市場報告無人機取證市場:按組件、部署方式、資料類型、無人機類型和應用程式分類,全球預測(2026-2032年)品牌建立服務市場:全球預測(2026-2032 年),按服務類型、交付管道、合作模式、組織規模、最終用戶產業和應用程式分類日本數位鑑識市場報告(按組件、類型、工具、最終用戶和地區分類,2026-2034 年)