|

市場調查報告書

商品編碼

1934592

南美洲殺軟體動物劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)South America Molluscicides - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

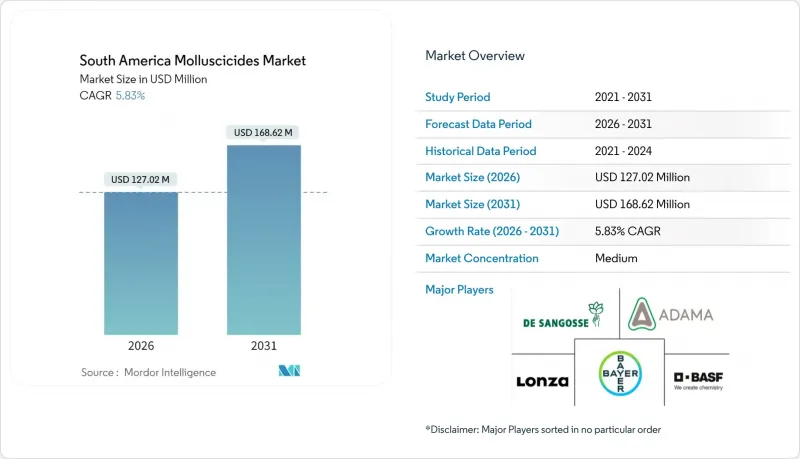

預計南美洲殺軟體動物劑市場將從 2025 年的 1.2 億美元成長到 2026 年的 1.2702 億美元,到 2031 年將達到 1.6862 億美元,2026 年至 2031 年的複合年成長率為 5.83%。

南美洲的殺螺劑市場受益於氣候變遷導致的濕度激增,這加速了腹足類動物的繁殖週期;同時,市場迅速轉向更安全的磷酸鐵基活性成分,以及鼓勵採用綜合蟲害管理(IPM)措施的公共補貼計劃。巴西在園藝產品大規模出口、咖啡和甘蔗面積龐大以及政府信貸額度(將貸款合格與永續蟲害控制通訊協定掛鉤)方面保持主導地位。哥倫比亞的特色作物蓬勃發展和智利的出口品質標準進一步增強了區域需求,推動了優質耐雨顆粒劑的創新。儘管競爭程度適中,五家供應商佔據了相當大的市場佔有率,但專注於特定領域的本地配方生產商仍然是關鍵參與者,他們根據微氣候和抗藥性管理需求量身定做產品。

南美殺軟體動物劑市場趨勢與洞察

氣候變遷導致濕度上升,蛞蝓和蝸牛造成的損害急劇增加。

氣溫升高和降雨量增加正在縮短地錢屬(Deloceras)和福壽螺屬(Pomacea)蛞蝓的休眠期,加劇了這些腹足類動物對大豆、咖啡和蔬菜的危害。田間研究表明,氣溫升高攝氏2度,降雨量增加20%,可能導致其繁殖率增加兩倍,迫使種植者將防治期延長至收穫期。在巴西塞拉多地區,越來越多的農場為了保護早熟的園藝作物,每個生長季要額外施用兩次顆粒劑。哥倫比亞安第斯山谷也出現了類似的趨勢,那裡露水持續時間長,即使在傳統的旱季,蛞蝓也能在夜間覓食。這種危害的加劇推高了每公頃的殺螺劑支出,尤其是那些能夠承受反覆降雨的高效顆粒劑。

政府對永續咖啡、甘蔗和園藝產品生產的補貼計劃

巴西國家家庭農業強化計劃僅向生產者提供補貼貸款,前提是他們必須提交一份綜合蟲害管理計劃,該計劃優先使用磷酸鐵而非甲醛。哥倫比亞的咖啡產業現代化津貼在使用GPS導航噴霧器時,可報銷高達30%的殺螺劑費用,從而鼓勵採用可變劑量顆粒劑。阿根廷於2025年擴大了其永續農業稅收體系,將殺螺劑抗性管理計畫納入稅額扣抵,間接促進了對雙效誘餌的需求。這些財政獎勵促使消費者從追求最低成本產品轉向更安全、能通過殘留審核的產品。由於補貼與貸款期限掛鉤,即使在商品價格走低的情況下,需求依然強勁。

加強南美洲金屬醛殘留法規

巴西國家衛生監督局 (ANVISA) 於 2024 年將殘留基準值與歐洲標準接軌,迫使生產商降低噴灑量或改用磷酸鐵處理出口產品。阿根廷國家農業衛生安全局 (SENASA) 增加了緩衝區和時間限制,使得雨季期間甲醛噴灑的計畫更加複雜。合規性審核往往與收穫高峰期重合,加劇了因殘留罰款而導致的貨物運輸中斷的經濟風險。在以咖啡和漿果為主要作物的地區,經銷商報告說甲醛處理量下降了 15%。因此,儘管傳統化學品具有成本優勢,但監管限制阻礙了其應用範圍的擴大。

細分市場分析

由於甲醛在黃豆、玉米和園藝作物中數十年來一直具有成本效益,2025年,其在南美殺螺劑市場佔了59.35%的佔有率。然而,由於出口認證機構和國內監管機構對殘留物的限制更加嚴格,磷酸鐵的銷售額預計將以9.26%的複合年成長率成長。到2031年,南美洲磷酸鐵殺螺劑的市場規模預計將翻倍。高價值的水果、蔬菜和觀賞植物領域預計將吸收高階需求。第二代活性成分,例如滅蟲威,將繼續保持其重要性,尤其是在觀賞植物領域,因為在分銷給都市區零售商之前需要快速控制蟲害。

隨著連作系統中抗藥性的出現,結合多種作用機制的複配產品正日益受到關注。尼克醯胺和西維因複配產品的專利申請表明,業界正努力在滿足不斷提高的安全標準的同時,分散化學壓力。供應商也在探索生物復配製劑,以改善偏好並調節飼料水分,從而延長潮濕微氣候下的田間保存期限。總而言之,這些創新進一步鞏固了南美殺螺劑市場對未來活性成分應用趨勢的認知,即有效的管理和對安全標準的嚴格遵守將決定未來活性成分的使用趨勢。

由於接觸型製劑具有廣譜殺滅能力、易於配製且與現有顆粒撒播器相容等優點,預計到2025年,其將佔南美洲殺螺劑市場規模的40.75%。目前,市場重點正轉向新一代驅避劑化學技術,可在最短時間內形成持續2-3週的保護屏障,從而最大限度地減少人員重返作業的間隔,尤其受到勞動力成本高昂的特種作物種植者的青睞。預計到2031年,驅避劑的銷售額將以8.87%的複合年成長率成長。

餌劑仍然是溫室周邊防禦的主要手段,而內吸性產品則在水生環境中有著特定的應用,它們透過溶解和吸收作用來控制入侵性蝸牛。巴西和阿根廷的監管機構越來越建議輪調使用接觸性、驅避性和餌劑類產品,以降低抗藥性的風險。隨著綜合蟲害管理(IPM)的普及,人們對能夠清楚標示作用機制的產品需求日益成長,這有助於種植者更好地規劃整個生長季節的輪換使用。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 氣候變遷導致濕度驟升,進而加劇了蛞蝓和蝸牛造成的傷害。

- 政府對永續咖啡、甘蔗和園藝產品生產的補貼計劃

- 園藝產品出口激增,帶動了對無瑕疵農產品的需求。

- 推出耐雨、具有殘留效應的顆粒配方

- 安第斯山脈特種作物的擴張加劇了高地軟體動物害蟲的壓力。

- 歐盟禁止使用金屬醛將更安全的磷酸鐵生產能力轉移到巴西

- 市場限制

- 加強南美洲金屬醛殘留法規

- 磷酸鐵活性成分的高成本溢價

- 軟體動物對單效化學物質的抗藥性日益增強

- 非官方的仿冒農藥交易

- 監管環境

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按活性成分

- 甲醛

- 磷酸鐵

- 其他化學活性成分(例如,甲硫威)

- 透過作用機制

- 接觸

- 口服型

- 滲透性

- 驅蟲劑

- 配方

- 顆粒

- 顆粒

- 液體

- 粉末

- 按作物類型

- 水果和蔬菜

- 穀類/豆類

- 油籽和豆類

- 觀賞植物

- 飼料和牧草作物

- 透過應用方法

- 農地

- 水體

- 工業和商業設施

- 住宅花園

- 按地區

- 巴西

- 阿根廷

- 智利

- 哥倫比亞

- 秘魯

- 其他南美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Bayer AG

- BASF SE

- Syngenta AG

- De Sangosse Ltd.

- Lonza Group AG

- Adama Ltd.

- American Vanguard Corporation(AMVAC)

- ANASAC

- UPL Ltd.

- Bequisa

- Certis Biologicals

- Nufarm Limited

第7章 市場機會與未來展望

The South America molluscicides market is expected to grow from USD 120 million in 2025 to USD 127.02 million in 2026 and is forecast to reach USD 168.62 million by 2031 at 5.83% CAGR over 2026-2031.

The South America molluscicides market is benefiting from climate-induced humidity spikes that accelerate gastropod breeding cycles, a swift transition toward safer iron-phosphate actives, and public subsidy programs that reward integrated pest management compliance. Brazil retains leadership in large-scale horticulture exports, robust coffee and sugarcane acreage, and government credit lines that link loan eligibility to sustainable pest-control protocols. Colombia's specialty-crop boom and Chile's export-quality mandates further reinforce regional demand while favoring premium, rain-fast pellet innovations. Competitive intensity is moderate, with five suppliers capturing significant revenue share, yet niche local formulators remain relevant by tailoring products to micro-climates and resistance-management needs.

South America Molluscicides Market Trends and Insights

Escalating Slug and Snail Infestations from Climate-Change-Driven Humidity Spikes

Warmer temperatures and heavier rainfall shorten the dormancy period for Deroceras and Pomacea species, intensifying gastropod attacks in soybeans, coffee, and vegetables. Field studies show that a 2 °C temperature increase combined with 20% more precipitation can triple reproductive rates, forcing growers to extend baiting windows well into harvest. Brazilian Cerrado farms now schedule two additional pellet applications per season to protect early-maturing horticulture crops. Similar trends surface in Colombia's Andean valleys, where persistent dew films allow slugs to feed overnight even during traditionally dry months. The expanded pressure elevates per-hectare molluscicide spending, especially on high-potency pellets that survive recurring rain events.

Government Subsidy Programs for Sustainable Coffee, Sugarcane, and Horticulture Production

Brazil's National Program for Strengthening Family Agriculture offers subsidized credit only when growers document integrated pest-management plans that favor ferric-phosphate over metaldehyde. Colombia's coffee-sector modernization grants reimburse up to 30% of molluscicide costs if GPS-guided spreaders are used, spurring adoption of variable-rate pellets. Argentina widened its sustainable-farming tax code in 2025 to credit molluscicide resistance-management plans, indirectly lifting demand for dual-mode baits. These financial carrots shift purchasing decisions away from lowest-cost options toward safer formulations that pass residue audits. As subsidies tie compliance to loan terms, demand remains resilient even when commodity prices soften .

Tightening South American Regulations on Metaldehyde Residues

Brazil's ANVISA harmonized maximum-residue limits with European thresholds in 2024, forcing growers to lower field rates or pivot to ferric-phosphate for export-bound produce. Argentina's SENASA added buffer-zone and timing rules that complicate metaldehyde scheduling during rainy seasons. Compliance audits often coincide with peak harvest, magnifying economic risk if residue fines suspend shipments. Distributors report a 15% drop in metaldehyde volume where coffee and berries are dominant. Regulatory drag, therefore, tempers the expansion of legacy chemistries despite their cost advantage.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Horticulture Exports Demanding Blemish-Free Produce

- Launch of Rain-Fast, Extended-Residual Pellet Formulations

- High Cost Premium of Iron-Phosphate Active Ingredient

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metaldehyde held 59.35% of South America's molluscicides market share in 2025, due to decades of cost-effective performance across soybeans, maize, and horticulture. Even so, iron-phosphate revenue is climbing at a 9.26% CAGR as export-certification bodies and domestic regulators impose stricter residue controls. The South America molluscicides market size for iron-phosphate products is forecast to almost double by 2031, with high-value fruit, vegetable, and ornamental segments absorbing the premium. Second-tier actives such as methiocarb maintain pockets of relevance in ornamentals, especially where rapid knockdown is required before shipment to urban retailers.

Combination products linking multiple modes of action are gaining traction as resistance emerges in continuous-cropping systems. Patent filings that pair niclosamide with carbaryl illustrate industry efforts to diversify chemical pressure while meeting evolving safety thresholds . Suppliers also explore biological co-formulants that improve palatability and regulate bait moisture, extending field life in humid micro-climates. These innovations collectively reinforce the perception that robust stewardship and safety compliance will dictate future active-ingredient adoption trajectories across the South America molluscicides market.

Contact formulations generated 40.75% of the South America molluscicides market size in 2025 due to proven broad-spectrum lethality, simple calibration, and compatibility with existing pellet spreaders. Marketing focus now pivots to next-generation repellent chemistries that create protective barriers for 2-3 weeks with minimal re-entry intervals, appealing to specialty-crop growers with high labor costs. Repellent revenues are forecast to expand at a 8.87% CAGR through 2031.

Ingestive baits remain a staple for perimeter defense around greenhouses, while systemic options serve niche aquatic uses where dissolved uptake curbs invasive snails. Regulatory agencies in Brazil and Argentina increasingly encourage rotation among contact, repellent, and ingestive modes to reduce resistance risk. As integrated pest management becomes mainstream, demand tilts toward labeled products that clearly specify mode-of-action groups, enabling growers to plan season-long rotation calendars.

The South America Molluscicides Market Report is Segmented by Active Ingredient (Metaldehyde, Iron Phosphate and More), by Mode of Action (Contact, Ingestive and More), by Formulation (Pellets, Liquids and More), by Crop Type (Cereals and Grains, and More), by Application Method (Agricultural Fields and More), and by Geography (Brazil, Argentina, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Bayer AG

- BASF SE

- Syngenta AG

- De Sangosse Ltd.

- Lonza Group AG

- Adama Ltd.

- American Vanguard Corporation (AMVAC)

- ANASAC

- UPL Ltd.

- Bequisa

- Certis Biologicals

- Nufarm Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating slug and snail infestations from climate-change-driven humidity spikes

- 4.2.2 Government subsidy programs for sustainable coffee, sugarcane, and horticulture production

- 4.2.3 Surge in horticulture exports demanding blemish-free produce

- 4.2.4 Launch of rain-fast, extended-residual pellet formulations

- 4.2.5 Andean shift toward specialty crops increasing mollusk pressure in high-altitude zones

- 4.2.6 EU metaldehyde ban diverting safer iron-phosphate production capacity to Brazil

- 4.3 Market Restraints

- 4.3.1 Tightening South American regulations on metaldehyde residues

- 4.3.2 High-cost premium of the iron-phosphate active ingredient

- 4.3.3 Rising mollusk resistance to single-mode chemistries

- 4.3.4 Informal trade in counterfeit crop-protection inputs

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Active Ingredient

- 5.1.1 Metaldehyde

- 5.1.2 Iron Phosphate

- 5.1.3 Other Chemical Actives (e.g., Methiocarb)

- 5.2 By Mode of Action

- 5.2.1 Contact

- 5.2.2 Ingestive

- 5.2.3 Systemic

- 5.2.4 Repellent

- 5.3 By Formulation

- 5.3.1 Pellets

- 5.3.2 Granules

- 5.3.3 Liquids

- 5.3.4 Powders

- 5.4 By Crop Type

- 5.4.1 Fruits and Vegetables

- 5.4.2 Cereals and Grains

- 5.4.3 Oilseeds and Pulses

- 5.4.4 Ornamentals

- 5.4.5 Forage and Pasture Crops

- 5.5 By Application Method

- 5.5.1 Agricultural Fields

- 5.5.2 Aquatic Areas

- 5.5.3 Industrial and Commercial Premises

- 5.5.4 Residential Gardens

- 5.6 By Geography

- 5.6.1 Brazil

- 5.6.2 Argentina

- 5.6.3 Chile

- 5.6.4 Colombia

- 5.6.5 Peru

- 5.6.6 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Bayer AG

- 6.4.2 BASF SE

- 6.4.3 Syngenta AG

- 6.4.4 De Sangosse Ltd.

- 6.4.5 Lonza Group AG

- 6.4.6 Adama Ltd.

- 6.4.7 American Vanguard Corporation (AMVAC)

- 6.4.8 ANASAC

- 6.4.9 UPL Ltd.

- 6.4.10 Bequisa

- 6.4.11 Certis Biologicals

- 6.4.12 Nufarm Limited

7 Market Opportunities and Future Outlook

2026年全球生物殺軟體動物劑市場報告

2026年全球生物殺軟體動物劑市場報告 生物軟體動物殺蟲劑市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年殺軟體動物劑市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、形式、應用、地區和競爭細分,2020-2030 年)

生物軟體動物殺蟲劑市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年殺軟體動物劑市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、形式、應用、地區和競爭細分,2020-2030 年) 亞太殺軟體動物劑市場:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)歐洲殺軟體動物劑市場:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)殺軟體動物劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

亞太殺軟體動物劑市場:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)歐洲殺軟體動物劑市場:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)殺軟體動物劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 軟體動物驅除劑市場:各類別,不同形態,各用途,各地區,機會,預測,2018年~2032年

軟體動物驅除劑市場:各類別,不同形態,各用途,各地區,機會,預測,2018年~2032年