|

市場調查報告書

商品編碼

1934584

天線產業:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Antenna Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

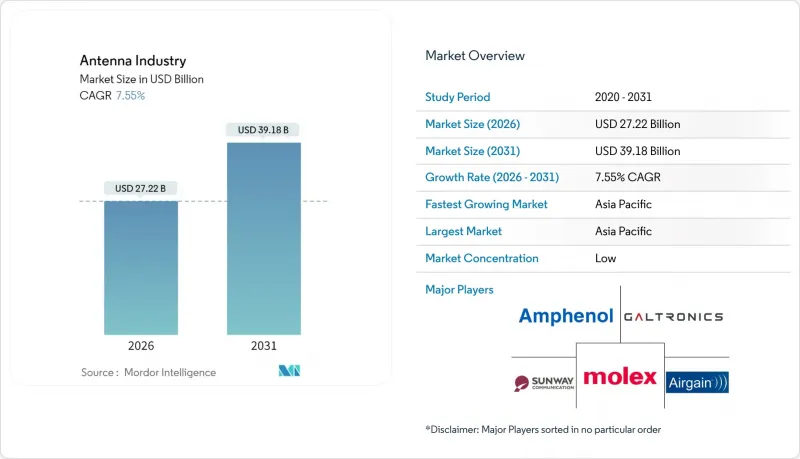

預計到 2026 年,天線市場規模將達到 272.2 億美元,高於 2025 年的 253.1 億美元,預計到 2031 年將達到 391.8 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 7.55%。

這一成長前景反映了5G的積極部署、物聯網節點數量的成長以及汽車連接需求的不斷提高,這些因素共同推動了對先進的多頻段和毫米波天線平台的需求。中頻寬頻譜密集化、高容量毫米波部署以及小型基地台的快速普及正在重塑基礎設施需求。同時,製造商正轉向液晶聚合物(LCP)和其他低損耗基板,以維持30 GHz以上頻段的性能。對相位陣列和大規模MIMO架構日益成長的興趣正促使供應商將波束成形邏輯整合到主動天線單元中。同時,低功耗片上天線模組在穿戴式裝置和資產追蹤設備中變得越來越普遍,加劇了分立元件供應商和半導體巨頭之間的競爭。

全球天線產業趨勢與洞察

加速5G毫米波基礎建設

通訊業者正在部署 64T64R 和 128T128R 大規模 MIMO 無線電模組,這些模組在單一機殼內整合了數百個輻射單元。愛立信 2024 年在印度的產能擴張計畫將支援這些主動天線系統在局部生產,以用於區域部署。美國聯邦通訊委員會 (FCC) 將於 2024 年開放 47-48 GHz 頻段的額外頻譜,通訊業者正在規劃固定無線存取 (FWA) 和高級行動寬頻(eMBB) 服務,這些服務需要亞波長星座間距和動態波束控制。這些需求將導致宏基地台和小型基地台對整合天線和無線電單元的需求增加。

物聯網設備的普及正在推動小型化

預計到2024年,全球物聯網節點數量將超過200億,設計人員面臨將多頻段效能整合到毫米級晶片尺寸的壓力。德克薩斯展示了一種片上天線解決方案,將輻射元件和射頻前端整合在單一晶粒上,適用於Sub-GHz頻段的工業鏈路。資產追蹤信標和穿戴式監測器需要更高的效率、更低的功耗和更堅固的機械設計,從而擴大了可觸及的天線市場。

毫米波頻段的功率效率挑戰

自由空間損耗在 30 GHz 以上呈指數級成長,迫使行動電話依賴由高線性度功率放大器驅動的多天線陣列。研究表明,毫米波陣列的功耗比 6 GHz 以下的同類天線高出 30-40%,導致緊湊型設備的電池續航時間縮短和熱負載增加。效率限制可能會減緩毫米波天線在大眾智慧型手機市場的普及,並抑制天線市場近期的成長。

細分市場分析

由於沖壓製程具有成本效益高且模具技術成熟,預計到2025年,其天線市佔率將維持在32.74%。同時,隨著液晶聚合物(LCP)天線在5G智慧型手機、汽車模組和毫米波固定無線設備的應用日益廣泛,其市場複合年成長率(CAGR)將達到8.55%。因此,在預測期內,LCP封裝天線的市場規模預計將比其他材料類別更快成長。

低損耗塑膠技術的進步正推動液晶聚合物(LCP)天線走向大規模生產的經濟化,但專用烘箱和嚴格的濕度控制通訊協定限制了合格供應商的數量。軟性印刷電路板和低介電常數(LDS)變體分別繼續滿足中端和細分市場的3D應用需求。隨著5G頻率攀升至71GHz,積極推動LCP加工的市場參與企業可望獲得更高的設計利潤。

由於印刷和軟性天線技術在入門級物聯網設備和傳統LTE設備中的主導地位,預計到2025年,它們將佔據天線市場規模的31.10%。隨著通訊業者不斷提高5G大型基地台和小型基地台的密度,整合式射頻積體電路相位陣列天線目前正以8.88%的複合年成長率成長。這種上升趨勢迫使天線供應商掌握涵蓋材料科學、射頻積體電路設計和熱工程等多學科領域的綜合能力。

在基板空間極為寶貴的穿戴式裝置和超小型追蹤器領域,封裝內天線 (AIP) 和晶片上天線 (AoC) 架構正變得越來越流行。同時,基礎設施級智慧天線提供數位波束控制、自我診斷和遠端傾斜控制等功能。除了硬體之外,整合軟體定義控制協定堆疊的供應商將更有利於在價格上超越同質化產品。

至2025年,1-6 GHz頻寬將佔天線市場規模的38.05%,涵蓋主流蜂巢網路、Wi-Fi和藍牙應用。然而,30 GHz以上的毫米波頻段將實現8.31%的複合年成長率,反映出市場對5G FR2(每秒影格速率)和新興汽車雷達應用的大量投資。毫米波產品面臨氧氣吸收和雨衰減等設計挑戰,需要高增益陣列和基於透鏡的定向控制。

美國和多個歐洲國家的監管機構已於2024年開放了47-48 GHz和64-71 GHz頻段的額外頻譜,為固定無線接取回程傳輸引入了新的頻寬。天線供應商正在開發超材料超支架和混合類比-數位波束形成器,以降低鏈路預算懲罰,同時將模組功耗控制在熱限制範圍內。

區域分析

亞太地區預計將在2025年佔據全球天線市場41.00%的佔有率,這主要得益於中國部署超過300萬個5G基地台以及印度「數位印度」光纖回程傳輸計畫的推動。日本汽車製造商正在引領V2X多埠組件的發展,而韓國的半導體生態系統則為先進基板製造提供了支援。區域製造群能夠帶來成本和物流的協同效應,但地緣政治摩擦正促使製造業分散到越南和印度。

北美正受益於美國聯邦通訊委員會 (FCC) 結構化的 5G 中頻段和毫米波頻譜競標,這些拍賣支援網路密集化和固定無線存取。持續進行的 Wi-Fi 7 企業更新週期正在增強對多頻段室內網路基地台天線的穩定需求。歐盟正在根據其 5G 行動計劃調整頻譜政策,而汽車 V2X 強制要求正在推動德國、法國和義大利在車輛天線方面的支出。

中東和非洲是成長最快的地區,複合年成長率達7.74%。波灣合作理事會(GCC)的智慧城市項目,例如NEOM和杜拜10X,優先發展邊緣連接和物聯網感測器網路,這需要強大的天線基礎設施。撒哈拉以南非洲的通訊業者正在透過低頻寬LTE和新興的非地面電波網路擴大遍遠地區的覆蓋範圍,從而為高增益面板和衛星平板陣列創造了更大的需求。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 5G和毫米波頻段部署的快速擴張正在推動對高密度主動天線的需求不斷成長。

- 物聯網終端的激增推動了多頻段、超緊湊型設計的發展。

- 美國和歐盟汽車V2X強制令推動多埠車用天線的發展

- 國防領域對堅固相位陣列陣天線和共形天線的需求

- 衛星平板的成長(用於行動和非地面電波網路(NTN))

- 用於醫療保健和消費性AR設備的軟性/穿戴式天線

- 市場限制

- 毫米波頻段射頻前端功率效率日益提高

- 供應鏈向東亞集中會帶來地緣政治風險

- 含氟天線基板的環境法規

- 整合式晶片天線模組的競爭將降低對分立元件的需求

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 消費者議價能力

- 供應商的議價能力

- 新進入者的威脅

- 競爭對手之間的競爭

- 替代品的威脅

第5章 市場規模和成長預測(價值和數量)

- 按類型

- 沖壓天線

- FPC天線

- LDS天線

- LCP天線

- MPI/超聚合物天線

- 透過技術

- 晶片上天線(AoC)

- 封裝式天線(AiP)

- 主動/智慧天線系統

- 印刷軟性天線

- 相位陣列與大規模MIMO天線

- 頻寬

- 1GHz 下列頻段(低頻段、高頻率、高頻率)

- 1 至 6 GHz(L波段、S 波段、C 波段)

- 6 至 30 GHz(X波段、 Ku波段、K 波段、 Ka波段)

- >30 GHz(毫米波、超高頻、5G FR2)

- 依產品

- 智慧型手機

- 筆記型電腦和平板電腦

- 穿戴式和可聽設備

- 網路設備(路由器、網路基地台)

- 其他連接的設備

- 透過使用

- 主要細胞

- Bluetooth/BLE

- Wi-Fi/WLAN

- GNSS/GPS

- NFC/RFID/UHF

- 透過安裝

- 嵌入式/內部

- 外部安裝類型/固定式

- 基礎設施和基地台

- 按最終用戶行業分類

- 家用電子電器

- 軍事/國防

- 汽車與出行

- 醫療和醫療設備

- 工業IoT和智慧城市

- 按地區

- 北美洲

- 美國

- 加拿大

- 南美洲

- 巴西

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 中東和非洲

- 以色列

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Molex

- Amphenol

- Airgain

- Galtronics

- Sunway Communication

- Luxshare Precision

- Murata Manufacturing

- TE Connectivity

- Qualcomm Technologies

- Texas Instruments

- AAC Technologies

- Fujikura

- KYOCERA-AVX

- Laird Connectivity

- Cobham Advanced Electronic Solutions

- CommScope

- Kathrein SE

- Huizhou SPEED Wireless

- Vishay Intertechnology

- Johanson Technology

- Nordic Semiconductor

- Intel Corporation

- Microchip Technology

- Harman International

- Kymeta Corporation

第7章 市場機會與未來展望

Antenna market size in 2026 is estimated at USD 27.22 billion, growing from 2025 value of USD 25.31 billion with 2031 projections showing USD 39.18 billion, growing at 7.55% CAGR over 2026-2031.

The growth outlook reflects aggressive 5G roll-outs, an expanding universe of IoT nodes, and rising automotive connectivity mandates that together raise demand for advanced multiband and mmWave antenna platforms. Mid-band spectrum densification, high-capacity mmWave deployments, and rapid small-cell proliferation are reshaping infrastructure requirements. Simultaneously, manufacturers are migrating toward Liquid Crystal Polymer and other low-loss substrates that sustain performance at 30 GHz and beyond. Heightened interest in phased-array and massive-MIMO architectures is pushing vendors to integrate beamforming logic within active antenna units. In parallel, power-efficient antenna-on-chip modules are expanding inside wearables and asset-tracking devices, tightening competition between discrete component suppliers and semiconductor incumbents.

Global Antenna Industry Trends and Insights

5G mmWave Infrastructure Acceleration

Operators are rolling out 64T64R and 128T128R massive-MIMO radios that embed hundreds of radiating elements within a single enclosure. Ericsson's 2024 capacity expansion in India underscores the push to localize production of these active antenna systems for regional deployments. The U.S. Federal Communications Commission unlocked additional 47-48 GHz spectrum in 2024, prompting carriers to plan fixed wireless access and enhanced mobile broadband services that demand sub-wavelength array spacing and dynamic beam steering. Such requirements translate into higher volumes of integrated antenna-radio units across macro and small-cell sites.

IoT Device Proliferation Driving Miniaturization

Global IoT node counts surpassed 20 billion in 2024, compelling designers to embed multiband performance into footprints measured in millimeters. Texas Instruments demonstrated antenna-on-chip solutions that collapse the radiating element and RF front end on a single die for sub-GHz industrial links. In asset-tracking beacons and wearable monitors, efficiency gains must coexist with low power budgets and rugged mechanical designs, enlarging the addressable antenna market.

Power-Efficiency Challenges at mmWave Frequencies

At 30 GHz and higher, free-space loss rises sharply, forcing handsets to rely on multiple antenna tiles driven by high-linearity power amplifiers. Studies show mmWave arrays draw 30-40% more energy than sub-6 GHz counterparts, compressing battery life and raising thermal loads in compact devices. Efficiency constraints can delay adoption in mass-market smartphones, tempering near-term growth of the antenna market.

Other drivers and restraints analyzed in the detailed report include:

- Automotive V2X Regulatory Mandates

- Defense Phased-Array System Expansion

- Supply-Chain Concentration Risks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The stamping category retained 32.74% of antenna market share in 2025 due to cost efficiency and entrenched tooling. LCP antennas, however, are on track for an 8.55% CAGR, gaining traction in 5G smartphones, automotive modules, and mmWave fixed wireless units. The antenna market size derived from LCP implementations will therefore expand more quickly than other material classes over the forecast horizon.

Advancements in low-dielectric-loss plastics allow LCP antennas to inch toward mass-production economies, though specialized ovens and tight moisture-control protocols limit the qualified supplier base. Flexible printed circuit and LDS variants continue to fill mid-tier and niche three-dimensional requirements respectively. Market participants active in LCP processing are expected to capture premium design-win margins as 5G frequencies climb toward 71 GHz.

Printed and flexible technologies held 31.10% share of antenna market size in 2025 because they dominate entry-level IoT and legacy LTE devices. Active phased-array units integrated with RFIC beamformers are now registering a 8.88% CAGR as operators densify 5G macro and small-cell layers. This upswing is pushing antenna vendors toward multidisciplinary competencies spanning materials science, RFIC design, and thermal engineering.

Antennas-in-package and antenna-on-chip architectures are proliferating in wearables and ultra-compact trackers where single-board real estate is scarce. At the opposite end of the spectrum, infrastructure-grade smart antennas feature digital beam steering, self-diagnostics, and remote tilt capabilities. Vendors that bundle software-defined control stacks alongside the hardware are positioned to differentiate beyond commodity price points.

The 1-6 GHz category represented 38.05% of antenna market size in 2025, covering mainstream cellular, Wi-Fi, and Bluetooth. Yet the >30 GHz mmWave slice is delivering an 8.31% CAGR, reflecting heavy investment in 5G FR2 and emerging automotive radar applications. mmWave products confront design hurdles such as oxygen absorption and rain attenuation, requiring higher-gain arrays and lens-based directivity control.

Regulators in the United States and several European nations freed additional 47-48 GHz and 64-71 GHz blocks in 2024, introducing new spectral real estate for fixed wireless access backhaul. Antenna suppliers are developing metamaterial superstrates and hybrid analog-digital beamformers to mitigate link-budget penalties while keeping module power within thermal envelopes.

The Antenna Market Report is Segmented by Type (Stamping, FPC, and More), Technology (AoC, Aip, and More), Frequency Range (Sub-1 GHz, 1-6 GHz, and More), Product (Smartphone, and More), Application (Cellular, Bluetooth/BLE, and More), Installation (Embedded/Internal, and More), End-User Industry (Consumer Electronics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific dominated the antenna market with a 41.00% share in 2025, anchored by China's installation of more than 3 million 5G base stations and India's Digital India fiber-backhaul mandates. Japan's vehicle OEMs pioneer V2X multi-port assemblies while South Korea's semiconductor ecosystem supports advanced substrate fabrication. Regional manufacturing clusters deliver cost and logistics synergies, yet geopolitical frictions spur diversification into Vietnam and India.

North America benefits from the FCC's structured 5G mid-band and mmWave auctions that underpin network densification and fixed wireless access. Ongoing Wi-Fi 7 enterprise refresh cycles reinforce steady demand for multi-band indoor access-point antennas. The European Union aligns spectrum policy under its 5G Action Plan, with automotive V2X mandates catalyzing vehicular antenna expenditures across Germany, France, and Italy.

The Middle East & Africa represent the fastest-growing region at an 7.74% CAGR. Gulf Cooperation Council smart-city programs such as NEOM and Dubai 10X emphasize edge connectivity and IoT sensor grids that require robust antenna infrastructure. Sub-Saharan operators are extending rural coverage through low-band LTE and emergent non-terrestrial networks, creating incremental opportunities for high-gain panel and satellite flat-panel arrays.

- Molex

- Amphenol

- Airgain

- Galtronics

- Sunway Communication

- Luxshare Precision

- Murata Manufacturing

- TE Connectivity

- Qualcomm Technologies

- Texas Instruments

- AAC Technologies

- Fujikura

- KYOCERA-AVX

- Laird Connectivity

- Cobham Advanced Electronic Solutions

- CommScope

- Kathrein SE

- Huizhou SPEED Wireless

- Vishay Intertechnology

- Johanson Technology

- Nordic Semiconductor

- Intel Corporation

- Microchip Technology

- Harman International

- Kymeta Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in 5G and mmWave roll-outs requiring high-density active antennas

- 4.2.2 Proliferation of IoT endpoints driving multi-band, ultra-compact designs

- 4.2.3 Automotive V2X mandates in US/EU boosting multi-port vehicular antennas

- 4.2.4 Defense demand for rugged phased-array and conformal antennas

- 4.2.5 Satellite flat-panel growth for mobility and non-Terrestrial Networks (NTN)

- 4.2.6 Flexible/wearable antennas for healthcare and consumer AR devices

- 4.3 Market Restraints

- 4.3.1 Rising RF front-end power-efficiency constraints at mmWave

- 4.3.2 Supply-chain concentration in East Asia creating geopolitical risk

- 4.3.3 Environmental regulations on fluorinated antenna substrates

- 4.3.4 Competition from integrated chip-antenna modules reducing discrete demand

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Consumers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Intensity of Competitive Rivalry

- 4.7.5 Threat of Substitutes

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Type

- 5.1.1 Stamping Antenna

- 5.1.2 FPC Antenna

- 5.1.3 LDS Antenna

- 5.1.4 LCP Antenna

- 5.1.5 MPI / Meta-Polymer Antenna

- 5.2 By Technology

- 5.2.1 Antenna-on-Chip (AoC)

- 5.2.2 Antenna-in-Package (AiP)

- 5.2.3 Active / Smart Antenna Systems

- 5.2.4 Printed and Flexible Antennas

- 5.2.5 Phased-Array and Massive-MIMO Antennas

- 5.3 By Frequency Range

- 5.3.1 Sub-1 GHz (LF, VHF, UHF)

- 5.3.2 1 to 6 GHz (L, S, C bands)

- 5.3.3 6 to 30 GHz (X, Ku, K, Ka)

- 5.3.4 > 30 GHz (mmWave, EHF, 5G FR2)

- 5.4 By Product

- 5.4.1 Smartphone

- 5.4.2 Laptop and Tablet

- 5.4.3 Wearables and Hearables

- 5.4.4 Networking Equipment (Routers, APs)

- 5.4.5 Other Connected Devices

- 5.5 By Application

- 5.5.1 Main Cellular

- 5.5.2 Bluetooth / BLE

- 5.5.3 Wi-Fi / WLAN

- 5.5.4 GNSS / GPS

- 5.5.5 NFC / RFID / UHF

- 5.6 By Installation

- 5.6.1 Embedded / Internal

- 5.6.2 External / Mounted

- 5.6.3 Infrastructure and Base-Station

- 5.7 By End-user Industry

- 5.7.1 Consumer Electronics

- 5.7.2 Military and Defense

- 5.7.3 Automotive and Mobility

- 5.7.4 Healthcare and Medical Devices

- 5.7.5 Industrial IoT and Smart Cities

- 5.8 By Geography

- 5.8.1 North America

- 5.8.1.1 United States

- 5.8.1.2 Canada

- 5.8.2 South America

- 5.8.2.1 Brazil

- 5.8.2.2 Rest of South America

- 5.8.3 Europe

- 5.8.3.1 Germany

- 5.8.3.2 United Kingdom

- 5.8.3.3 France

- 5.8.3.4 Russia

- 5.8.4 Asia-Pacific

- 5.8.4.1 China

- 5.8.4.2 Japan

- 5.8.4.3 South Korea

- 5.8.4.4 India

- 5.8.5 Middle East and Africa

- 5.8.5.1 Israel

- 5.8.5.2 Saudi Arabia

- 5.8.5.3 United Arab Emirates

- 5.8.5.4 South Africa

- 5.8.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Molex

- 6.4.2 Amphenol

- 6.4.3 Airgain

- 6.4.4 Galtronics

- 6.4.5 Sunway Communication

- 6.4.6 Luxshare Precision

- 6.4.7 Murata Manufacturing

- 6.4.8 TE Connectivity

- 6.4.9 Qualcomm Technologies

- 6.4.10 Texas Instruments

- 6.4.11 AAC Technologies

- 6.4.12 Fujikura

- 6.4.13 KYOCERA-AVX

- 6.4.14 Laird Connectivity

- 6.4.15 Cobham Advanced Electronic Solutions

- 6.4.16 CommScope

- 6.4.17 Kathrein SE

- 6.4.18 Huizhou SPEED Wireless

- 6.4.19 Vishay Intertechnology

- 6.4.20 Johanson Technology

- 6.4.21 Nordic Semiconductor

- 6.4.22 Intel Corporation

- 6.4.23 Microchip Technology

- 6.4.24 Harman International

- 6.4.25 Kymeta Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

GSM天線市場:2026-2032年全球市場預測(依天線類型、小區尺寸、安裝方式及最終用戶分類)軍用非定向天線市場:2026-2032年全球市場預測(按應用、最終用戶、頻率、天線類型和安裝方式分類)

GSM天線市場:2026-2032年全球市場預測(依天線類型、小區尺寸、安裝方式及最終用戶分類)軍用非定向天線市場:2026-2032年全球市場預測(按應用、最終用戶、頻率、天線類型和安裝方式分類) 2026年全球相位陣列天線市場報告

2026年全球相位陣列天線市場報告 智慧型手錶天線市場規模、佔有率和成長分析:按天線技術、連接通訊協定、基板材料、應用層和地區分類-2026-2033年產業預測汽車整合天線系統市場:依技術、安裝類型、天線形狀、車輛類型和應用分類-2026年至2032年全球市場預測2026年全球發射天線市場報告LCD天線市場:產品類型、頻段、部署方式、應用、最終用途-2026-2032年全球市場預測2026年全球GSM(全球行動通訊系統)天線市場報告2026年全球室外基地台(BTS)天線市場報告

智慧型手錶天線市場規模、佔有率和成長分析:按天線技術、連接通訊協定、基板材料、應用層和地區分類-2026-2033年產業預測汽車整合天線系統市場:依技術、安裝類型、天線形狀、車輛類型和應用分類-2026年至2032年全球市場預測2026年全球發射天線市場報告LCD天線市場:產品類型、頻段、部署方式、應用、最終用途-2026-2032年全球市場預測2026年全球GSM(全球行動通訊系統)天線市場報告2026年全球室外基地台(BTS)天線市場報告 全球RFID天線市場:按類型、輻射方向圖、外形規格和應用分類-預測(至2032年)

全球RFID天線市場:按類型、輻射方向圖、外形規格和應用分類-預測(至2032年)