|

市場調查報告書

商品編碼

1911829

印度家具金屬製品市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)India Furniture Hardware - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

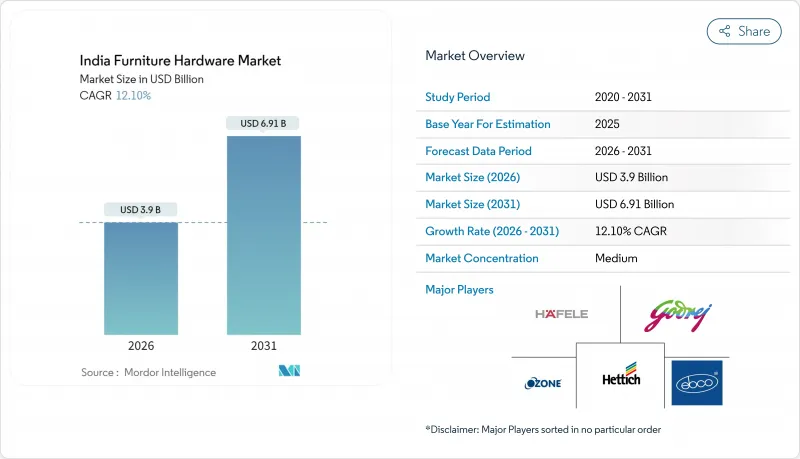

據估計,印度家具金屬製品市場到 2026 年的價值將達到 39 億美元,高於 2025 年的 34.8 億美元。

預計到 2031 年將達到 69.1 億美元,2026 年至 2031 年的複合年成長率為 12.1%。

受都市區住宅快速建設、零售網路擴張和數位化通路普及等因素的推動,印度家具金屬製品市場保持著兩位數的成長動能。可支配收入的增加帶動了高階五金和緩閉系統的需求,而政府的品質標準也促進了認證產品的銷售。目前市場競爭格局依然分散,全球品牌透過設計差異化來捍衛市場佔有率,而靈活的本土企業則在價格上競爭。近期成長要素包括強勁的住宅項目、不斷擴張的商業室內裝飾市場以及網際網路普及率的提高,這些因素正在推動消費者和小規模承包商轉向線上採購。

印度家具金屬製品市場趨勢與洞察

快速的住宅建設和都市化

預計未來十年印度將新增約1億住宅,其中孟買、浦那和清奈等大都會圈的需求量最大,直接推動了鉸鏈、鉸鏈和建築五金的需求。老舊住宅存量的現代化改造進一步增加了對傳統鉸鏈的需求,人們希望用緩閉式和耐腐蝕鉸鏈來取代舊鉸鏈。沿海地區的開發商擴大指定使用耐潮濕的不銹鋼材質,推高了平均售價。集中在工業中心(尤其是馬哈拉斯特拉邦製造業帶)的建設計劃創造了區域性需求,有利於附近的供應商。新計畫和替換需求的結合,為印度家具金屬製品市場打造了一個強大且地理多元化的基礎。

加速模組化和RTA家具的電子商務

組裝衣櫃和廚房模組現在以平板包裝形式出貨,包裝內包含螺絲、凸輪和導軌等組件,這些組件必須符合嚴格的公差要求。由於網購消費者自行安裝五金件,品牌方更加重視直覺的設計、帶有QR碼的影片指南以及完整的緊固件套裝。主要市場快速的產品更新周期要求五金供應商將產品庫存單位 (SKU) 與家具製造商的更新計劃同步,從而促進價值鏈上更深入的合作。顧客評估數據顯示,鉸鏈缺陷是產品退貨的主要原因,因此品質一致性成為關鍵的差異化因素。數位通路 14.36% 的複合年成長率直接轉化為標準化五金件銷量的成長,同時也提高了印度家具五金市場的價格透明度。

來自非正規部門的價格壓力和物流挑戰

成千上萬的小規模作坊聚集在拉傑果德和莫拉達巴德,它們規避了認證費用,直接向當地木工銷售產品,從而能夠以比品牌製造商低30%的價格出售產品。它們能夠迅速複製熱門產品,這給印度家具金屬製品市場的入門級利潤率帶來了壓力。笨重的金屬滑軌和籃子重量與價值比低,而且運往偏遠地區時會增加運費。東北地區落後的交通網路延長了前置作業時間,迫使經銷商增加安全庫存,增加了流動資金。雖然印度標準協會(BIS)的法規旨在消除不合格產品,但主要港口以外地區執法不力,導致了持續的價格戰。

細分市場分析

2025年,升降系統的收入微乎其微,但預計將以12.62%的複合年成長率快速成長,這主要得益於都市區廚房對上開式櫥櫃以提高空間利用率的需求。鉸鏈仍是領先產品,佔印度家具金屬製品市場佔有率的26.88%。然而,消費者價值念的轉變使得隱藏式和緩閉式鉸鏈更受青睞,因此價格也更高。滑軌系統的需求持續成長,模組化廚房需要更安靜且可完全拉出的抽屜。把手、把手和旋鈕的需求主要受設計主導,消費者更傾向於選擇與室內主題相協調的配色系列。雖然緊固件是銷量最大的SKU,但由於市場參與者分散,其利潤率正在下降。然而,BIS標準的實施可能會促使注重品質的消費者轉向品牌產品。諸如滑動門系統和金屬絲籃等專業子類別提供了更多功能選擇,從而豐富了產品種類,並提升了其在印度整體家具金屬製品市場的競爭力。

次生影響力正在重塑各產品領域的競爭性投資格局。升降輔助阻尼器和伺服驅動開門器需要精確的氣彈簧調節,這推動了本地工廠的自動化生產。隱藏式鉸鏈需要微米級沖壓模具,小規模工廠難以維護,這進一步擴大了正規生產商和非正規生產商之間的能力差距。高階箱體系統的成長與衣櫃模組化程度的提高一致,供應商提供導軌、支架和把手等整合套件。落地玻璃面板的滑動機構正在開拓高階住宅和辦公室內市場,在這些市場中,框架厚度越薄越好。這些趨勢共同作用,正在推動收入結構向工程機械領域轉移,並擴大印度家具金屬製品市場的價值基礎。

由於鋼材經久耐用且單位成本低廉,預計到2025年,鋼材將佔印度家具金屬製品市場規模的41.88%。鋅合金因其耐腐蝕性,在沿海和潮濕地區備受青睞;而鋁材則因其輕巧的特性,被用於電梯系統等高階應用領域。另一方面,塑膠和其他聚合物基五金預計將以12.33%的複合年成長率快速成長,因為製造商利用射出成型的柔軟性來製造複雜形狀並整合阻尼功能。黃銅在豪華酒店業擁有獨特的裝飾應用,其獨特的銅綠美感使其價格也顯得合理。

如今,可回收性已成為材料選擇的重要組成部分,都市區消費者在購買前也會考慮產品的環保性能。先進的玻璃纖維增強尼龍材料兼具金屬般的強度和更輕的重量,從而降低了電商配送的運輸成本。射出成型的投資也縮短了生產週期,使企業能夠快速提升產能,以滿足線上限時搶購的激增需求。同時,SS-304 和 SS-316 等優質不銹鋼在高階廚房市場中佔據越來越大的佔有率,因為易於清潔和經久耐用是高階廚房的關鍵特性。先進塑膠和不銹鋼合金的同步發展,標誌著印度家具金屬製品市場的分化,兼具輕量化和高階性能。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章:目錄——印度家具金屬製品市場

第2章 引言

- 研究假設和市場定義

- 調查範圍

第3章調查方法

第4章執行摘要

第5章 市場情勢

- 市場概覽

- 市場促進因素

- 住宅房地產快速成長與都市化

- 在網上購買的模組化/RTA家具數量激增

- 優質化和設計主導的需求促使人們對高品質金屬製品產生需求。

- 拓展有組織的零售和DIY通路

- 透過BIS品管指令提高績效標準

- 身心障礙者標準推動了人體工學硬體的發展。

- 市場限制

- 分散的非正規部門和激烈的競爭

- 鋼材、鋅和聚合物成本波動

- 大型重型零件的物流效率低下

- 滿足新的永續性和無障礙標準所需的成本

- 產業價值鏈分析

- 波特五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 洞察市場最新趨勢與創新

- 深入了解市場近期發展動態(新產品發表、策略性舉措、投資、合作、合資、擴張、併購等)

- 對硬體行業法規結構和行業標準的深入了解

第6章 市場規模及成長預測(以金額為準,2020-2030 年)

- 依產品類型

- 鉸鏈

- 跑步系統

- 升降系統

- 箱式系統

- 金屬絲籃

- 滑動門系統

- 把手、把手、旋鈕

- 緊固件(螺絲、螺栓、螺帽等)

- 其他

- 材料

- 鋼

- 鋅合金

- 鋁

- 塑膠和聚合物基

- 黃銅和其他金屬

- 最終用戶

- 住宅家具

- 辦公家具

- 飯店和零售設施

- 公共利益(醫療保健、教育)

- 透過分銷管道

- 線下 - 經銷商和零售商

- 線上 - 電子商務和品牌 D2C

- 按地區(印度)

- 印度北部

- 西印度群島

- 南印度

- 印度東部和東北部

第7章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Hettich India Pvt. Ltd.

- Hafele India Pvt. Ltd.

- Godrej Locks & Architectural Fittings & Systems

- Ebco Pvt. Ltd.

- Ozone Overseas Pvt. Ltd.

- Dorset Industries Pvt. Ltd.

- Blum India

- Sugatsune Kogyo India

- H Hafele(Hafele brand stores)

- Hettich PODs & Studio Partners

- Kich Architectural Products

- PEGO Hardware

- Quba Group

- Vinay Wire & Polyproduct Pvt. Ltd.

- Dorset Smart Locks

- Ozone Securitas

- Evershine Appliances(Oliveworld)

- Italik Metalware Pvt. Ltd.

- DP Garg & Company(Garg Hinges)

- SIFON Hardware

第8章:市場機會與未來展望

- 有組織的零售業擴張促進了品牌五金的發展。

- 智慧機制革新模組化家具系統

India furniture hardware market size in 2026 is estimated at USD 3.90 billion, growing from 2025 value of USD 3.48 billion with 2031 projections showing USD 6.91 billion, growing at 12.1% CAGR over 2026-2031.

Demand momentum is anchored in rapid urban housing creation, swelling organized retail footprints, and digital channel adoption that keep the India furniture hardware market on a double-digit growth curve. Rising disposable incomes promote premium fittings and soft-close systems, while government quality mandates steer buyers toward certified products. Global brands safeguard share with design differentiation, whereas nimble regional firms battle on price, sustaining a fragmented competitive field. Near-term upside stems from a strong residential pipeline, expanding commercial interiors, and online penetration that moves both consumer and small-contractor purchases to click-based journeys.

India Furniture Hardware Market Trends and Insights

Rapid residential build-out and urbanization

India must add roughly 100 million homes this decade, and metros such as Mumbai, Pune and Chennai account for a large share of that pipeline, directly lifting demand for hinges, runners and architectural fittings. Modernization of aging housing stock further multiplies retrofit volumes as owners swap legacy hinges for soft-close or corrosion-resistant versions. Developers in coastal belts increasingly specify stainless-steel grades to withstand humidity, nudging average selling prices higher. Construction clusters around industrial nodes, especially Maharashtra's manufacturing belts, create localized demand pockets that favor nearby suppliers. Together, greenfield projects and replacements underpin a robust, geographically diversified base for the India furniture hardware market.

E-commerce acceleration in modular and RTA furniture

Ready-to-assemble wardrobes and kitchen modules now ship in flat-packs bundled with screws, cams and runners that must meet tight tolerances. Online buyers install fittings themselves, so brands emphasize intuitive designs, QR-code video guides and complete fastener kits. Rapid product cycles on leading marketplaces force hardware suppliers to synchronize SKUs with furniture makers' refresh calendars, deepening collaboration along the value chain. Customer-review data reveal hinge failures as a leading cause of returns, making quality consistency a vital differentiator. The 14.36% CAGR logged by digital channels thus converts directly into incremental standardized-hardware sales while injecting pricing transparency into the India furniture hardware market.

Price pressure from the unorganized sector plus logistics hurdles

Thousands of small workshops clustered in Rajkot and Moradabad undercut branded players by up to 30% because they sidestep certification costs and sell direct to local carpenters. Their agility in copying popular SKUs squeezes margins on entry-level lines within the India furniture hardware market. Bulky metal slides and baskets suffer unfavorable weight-to-value ratios, inflating freight costs when shipped to distant regions. Poor connectivity in the North-East lengthens lead times and forces distributors to hold larger safety stocks, raising working capital. Although BIS mandates aim to weed out sub-par goods, patchy enforcement outside major ports allows price-led competition to persist.

Other drivers and restraints analyzed in the detailed report include:

- Premiumization, design focus and regulatory quality cues

- Rise of organized retail, DIY and accessibility needs

- Raw-material and compliance cost volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lift systems captured only modest revenue in 2025 but are forecast to grow at a 12.62% CAGR, the quickest pace among categories, as urban kitchens seek overhead cabinets that open upwards for space efficiency. Hinges remained the workhorse with 26.88% of the India furniture hardware market share, yet value migration favors concealed and soft-close variants that attract price premiums. Runner systems continue to gain traction in modular kitchens whose drawers require silent, full-extension slides. Handles, pulls and knobs benefit from design-led demand, supporting color-matched collections that complement interior themes. Fasteners are the highest-volume SKU yet face margin erosion from unorganized players; still, BIS standards could lift quality-conscious buyers toward branded options. Specialized sub-categories such as sliding-door systems and wire baskets broaden functionality choices, reinforcing product breadth as a competitive lever across the India furniture hardware market.

Second-order effects shape competitive investments across product verticals. Lift-assist dampers and servo-driven openers rely on precise gas-spring calibration, encouraging automation in local factories. Concealed hinges require micron-level stamping dies that smaller shops struggle to maintain, widening the capability gap between organized and informal producers. Growth in premium box systems aligns with rising wardrobe modularization, prompting suppliers to bundle runners, brackets and handles as integrated kits. Sliding mechanisms designed for floor-to-ceiling glass panels tap into premium residential and office interiors, where minimal frame thickness is prized. Together these trends shift revenue mix toward engineered mechanisms, expanding the value pool of the India furniture hardware market.

Steel delivered 41.88% of the India furniture hardware market size in 2025 thanks to its durability and low unit cost. Zinc alloy follows in coastal and high-humidity zones for its corrosion resistance, while aluminum's light weight attracts premium applications such as lift systems. Plastic and other polymer-based fittings, however, clock the fastest 12.33% CAGR as makers exploit injection-mold flexibility to create complex geometries and integrate damping functions. Brass serves niche decor roles in luxury hospitality where patina aesthetics justify higher price points.

Material selection now incorporates recyclability, with urban consumers querying environmental credentials before purchase. Advanced glass-fiber-reinforced nylon grades rival metal strength at lower weights, slashing freight costs for e-commerce shipments. Injection-molding investments also reduce per-unit cycle time, allowing rapid ramp-up to serve flash sale spikes online. Conversely, high-grade stainless variants such as SS-304 and SS-316 earn share in premium kitchens where ease of cleaning and long life matter. The simultaneous rise of advanced plastics and stainless alloys signals bifurcation toward both lightweight economy and high-end performance within the India furniture hardware market.

The India Furniture Hardware Market Report is Segmented by Product Type (Hinges, Runner Systems, Lift Systems, Box Systems, Wire Baskets, and More), Material (Steel, Zinc Alloy, Aluminium, and More), End-User (Residential, Office, Hospitality & Retail, Institutional), Distribution Channel (Offline, Online), and Geography (North, West, South, and More). Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Hettich India Pvt. Ltd.

- Hafele India Pvt. Ltd.

- Godrej Locks & Architectural Fittings & Systems

- Ebco Pvt. Ltd.

- Ozone Overseas Pvt. Ltd.

- Dorset Industries Pvt. Ltd.

- Blum India

- Sugatsune Kogyo India

- H Hafele (Hafele brand stores)

- Hettich PODs & Studio Partners

- Kich Architectural Products

- PEGO Hardware

- Quba Group

- Vinay Wire & Polyproduct Pvt. Ltd.

- Dorset Smart Locks

- Ozone Securitas

- Evershine Appliances (Oliveworld)

- Italik Metalware Pvt. Ltd.

- DP Garg & Company (Garg Hinges)

- SIFON Hardware

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Table of Contents - India Furniture Hardware Market

2 Introduction

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

3 Research Methodology

4 Executive Summary

5 Market Landscape

- 5.1 Market Overview

- 5.2 Market Drivers

- 5.2.1 Rapid growth in residential real-estate & urbanisation

- 5.2.2 Surge in modular/RTA furniture bought online

- 5.2.3 Premiumisation & design-driven demand for high-quality fittings

- 5.2.4 Expanding organised retail & DIY channels

- 5.2.5 BIS quality-control orders upgrading performance standards

- 5.2.6 Accessibility standards for PwD driving ergonomic hardware

- 5.3 Market Restraints

- 5.3.1 Fragmented unorganised sector & intense price competition

- 5.3.2 Volatile steel/zinc/polymer costs

- 5.3.3 Logistics inefficiencies for bulky, weighty fittings

- 5.3.4 Compliance costs for new sustainability & accessibility norms

- 5.4 Industry Value Chain Analysis

- 5.5 Porter's Five Forces Analysis

- 5.5.1 Threat of New Entrants

- 5.5.2 Bargaining Power of Suppliers

- 5.5.3 Bargaining Power of Buyers

- 5.5.4 Threat of Substitutes

- 5.5.5 Competitive Rivalry

- 5.6 Insights into the Latest Trends and Innovations in the Market

- 5.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

- 5.8 Insights on Regulatory Framework and Industry Standards for the Hardware Industry

6 Market Size & Growth Forecasts (Value, 2020-2030)

- 6.1 By Product Type

- 6.1.1 Hinges

- 6.1.2 Runner Systems

- 6.1.3 Lift Systems

- 6.1.4 Box Systems

- 6.1.5 Wire Baskets

- 6.1.6 Sliding Door Systems

- 6.1.7 Handles, Pulls, and Knobs

- 6.1.8 Fasteners (Screw, Bolts, Nuts, etc.)

- 6.1.9 Others

- 6.2 By Material

- 6.2.1 Steel

- 6.2.2 Zinc Alloy

- 6.2.3 Aluminium

- 6.2.4 Plastic & Polymer-based

- 6.2.5 Brass & Other Metals

- 6.3 By End-user

- 6.3.1 Residential Furniture

- 6.3.2 Office Furniture

- 6.3.3 Hospitality & Retail Fixtures

- 6.3.4 Institutional (Healthcare, Education)

- 6.4 By Distribution Channel

- 6.4.1 Offline - Dealer & Retail

- 6.4.2 Online - E-commerce & Brand D2C

- 6.5 By Region (India)

- 6.5.1 North India

- 6.5.2 West India

- 6.5.3 South India

- 6.5.4 East & North-East India

7 Competitive Landscape

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 7.4.1 Hettich India Pvt. Ltd.

- 7.4.2 Hafele India Pvt. Ltd.

- 7.4.3 Godrej Locks & Architectural Fittings & Systems

- 7.4.4 Ebco Pvt. Ltd.

- 7.4.5 Ozone Overseas Pvt. Ltd.

- 7.4.6 Dorset Industries Pvt. Ltd.

- 7.4.7 Blum India

- 7.4.8 Sugatsune Kogyo India

- 7.4.9 H Hafele (Hafele brand stores)

- 7.4.10 Hettich PODs & Studio Partners

- 7.4.11 Kich Architectural Products

- 7.4.12 PEGO Hardware

- 7.4.13 Quba Group

- 7.4.14 Vinay Wire & Polyproduct Pvt. Ltd.

- 7.4.15 Dorset Smart Locks

- 7.4.16 Ozone Securitas

- 7.4.17 Evershine Appliances (Oliveworld)

- 7.4.18 Italik Metalware Pvt. Ltd.

- 7.4.19 DP Garg & Company (Garg Hinges)

- 7.4.20 SIFON Hardware

8 Market Opportunities & Future Outlook

- 8.1 Organized Retail Expansion Boosting Branded Hardware

- 8.2 Smart Mechanisms Transforming Modular Furniture Systems