|

市場調查報告書

商品編碼

1911810

歐洲諮詢服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Europe Consulting Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

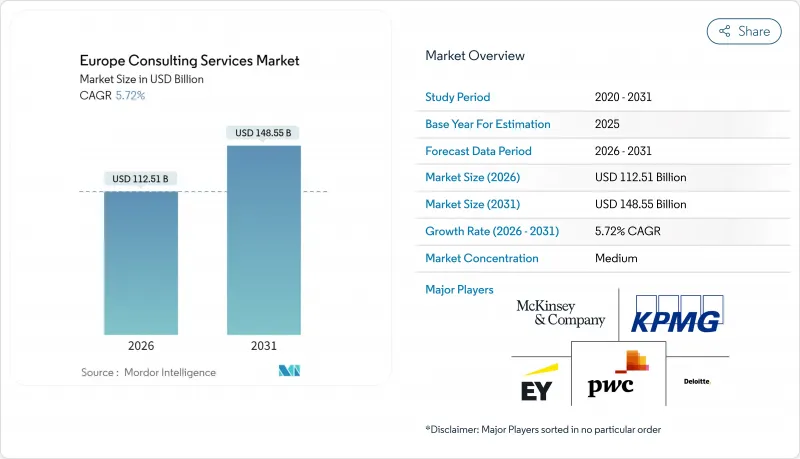

歐洲諮詢服務市場預計將從 2025 年的 1,064.2 億美元成長到 2026 年的 1,125.1 億美元,預計到 2031 年將達到 1,485.5 億美元,2026 年至 2031 年的複合年成長率為 5.72%。

這一穩步成長表明,專業服務公司已成功適應經濟不確定性、數位轉型以及日益嚴格的永續發展法規。歐盟委員會的「數位歐洲」計畫將投入79億歐元用於技術應用,不僅提振了市場需求,也使服務供應商能夠拓展跨境業務。地緣政治供應鏈的緊張局勢使得卓越營運計劃始終是客戶的優先事項,而主要企業對人工智慧的大規模投資正將新興技術轉化為常規諮詢服務。歐盟復甦與韌性基金(RRF)的資金支持正在加速中小企業採用外部專業知識,擴大基本客群,並降低其對大型企業預算的依賴。隨著四大會計師事務所投資超過40億美元用於人工智慧能力建設,日益激烈的競爭正在重塑服務交付的經濟格局,而中型企業則被迫專注於特定領域。

歐洲諮詢服務市場趨勢與洞察

跨境服務監理趨同

歐盟正在協調數位化法規,減少行政摩擦,使諮詢公司能夠以更少的合規性審查跨境複製解決方案。德國和法國將於2024年正式啟動公共部門軟體互通性的合作,這將使領先採用者有機會開發可重複使用的方案,從而縮短計劃前置作業時間。中型服務提供者因無需在每個國家都配備完整的法律團隊而獲得了新的機會。雖然全面協調要到2027年才能實現,但現在投資於多語言監管專業知識的公司可能會在各國政府擴大聯合服務範圍時獲得多年框架合約。

加速客戶對人工智慧驅動的生產力諮詢的需求

經營團隊將人工智慧視為控制成本和促進成長的必然選擇,這促成了大規模諮詢交易的達成。光是德國的人工智慧市場就以每年15%的速度成長,到2030年可望為GDP貢獻4,300億歐元,進而推動人工智慧策略、資料工程和變革管理交易的激增。德勤的新平台Zora和安永的150個人工智慧代理商展示了大型公司如何將其智慧財產權產品化,並為客戶帶來25%至40%的生產力提升。隨著基礎自動化逐漸普及,規模較小的顧問公司如果不轉向高度專業化的人工智慧應用,將面臨利潤率下降的風險。

高階分析領域人才持續短缺

歐洲顧問公司正面臨資料科學家招募難題。歐洲職業培訓發展中心(CEDEFOP)發布的勞動力和技能短缺指數顯示,到2035年,分析和人工智慧相關職位將面臨嚴重的人才短缺。儘管技術崗位的就業人數創歷史新高,但德國和法國政府仍報告人才持續短缺,迫使企業支付更高的薪資或將工作外包。人才短缺推高了計劃成本,延長了交付週期,並降低了高階分析工作的能力。規模較小的顧問公司受到的影響最大,因為它們無法與四大顧問公司相媲美,這加劇了市場整合的風險。

細分市場分析

營運諮詢將佔據最大的收入佔有率,到2025年將佔歐洲諮詢服務市場28.12%的佔有率,這主要得益於企業在當前地緣政治緊張局勢下尋求供應鏈韌性和降低成本。精實生產、流程重組和營運資本最佳化仍然是歐洲諮詢服務市場的重點,為專業人士提供了穩定的收入來源。同時,在人工智慧、雲端遷移和永續發展儀錶板的驅動下,數位轉型諮詢正以7.49%的複合年成長率在所有細分市場中成長最快。

儘管策略、財務諮詢和人力資源/變革管理仍發揮重要作用,但市場需求日益集中於整合技術、風險管理和人才發展的全面轉型解決方案。由於網路威脅日益加劇和雲端架構碎片化,技術諮詢的重要性也日益凸顯。隨著企業將碳會計納入工作流程,永續發展和ESG諮詢正與核心業務需求相互融合。隨著歐洲諮詢服務市場從孤立的項目轉向基於平台、以結果為導向的項目,能夠根據產業專用的策略組建多學科團隊的服務供應商將保持競爭優勢。

資訊通訊技術與媒體產業預計將佔2025年總收入的29.56%,反映出該產業持續的技術更新週期和活躍的軟體創新。該行業客戶群持續試點生成式人工智慧、5G貨幣化和邊緣運算計劃,支撐了歐洲諮詢服務市場的強勁需求。同時,受全通路投資加速、末端物流和數據驅動型商品行銷的推動,消費品與零售業預計到2031年將維持7.41%的複合年成長率。

在金融服務領域,儘管面臨股本監管和數位銀行的競爭,諮詢支出依然居高不下。製造業則專注於工業4.0藍圖和節能型工廠維修。在醫療保健領域,電子健康記錄整合和基於雲端的ERP遷移正在加速推進,Asklepios Kliniken的SAP S/4HANA實施就需要18個月的外部支援。在能源和公共產業,對電網數位化和氫能基礎設施規劃的需求,為專注於永續發展的顧問創造了獨特的市場機會。

歐洲諮詢服務市場按服務類型(營運諮詢、策略諮詢、財務顧問等)、客戶行業(銀行、金融服務和保險、製造/工業等)、公司規模(大型企業、中小企業)、交付模式(現場服務、遠端/虛擬、混合模式)和國家/地區進行細分。市場預測以美元計價。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 跨境服務監理趨同

- 加速客戶對人工智慧驅動的生產力諮詢的需求

- 應對歐盟綠色交易和企業永續發展報告指令 (CSRD) 的壓力

- 歐盟復甦基金津貼幫助中小企業提升數位成熟度

- 轉向基於績效的定價模式

- 由於供應鏈中的地緣政治風險,近岸外包成為可能

- 市場限制

- 高階分析領域人才持續短缺

- 透過採購主導的談判降低費用

- 利用 DIY 生成式 AI 工具包簡化基礎工作

- 大型整合商和顧問公司之間併購的監管審查

- 產業價值鏈分析

- 監管環境

- 技術展望

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭對手之間的競爭

- 宏觀經濟因素如何影響市場

第5章 市場規模與成長預測

- 按服務類型

- 營運諮詢

- 策略諮詢

- 財務諮詢

- 技術諮詢

- 人力資源與變革管理

- 永續發展與ESG諮詢

- 數位轉型諮詢

- 按客戶產業

- BFSI

- 製造業和工業

- 醫療保健和生命科學

- 能源與公共產業

- 資訊與通訊科技與媒體

- 消費品和零售

- 其他客戶產業

- 按公司規模

- 主要企業

- 中小企業

- 按交付模式

- 現場支援

- 遠端/虛擬

- 混合模式

- 按國家/地區

- 英國

- 德國

- 法國

- 比荷盧經濟聯盟

- 義大利

- 北歐國家

- 西班牙

- 中歐和東歐(包括波蘭)

- 其他歐洲地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Deloitte Touche Tohmatsu Limited

- Ernst & Young Global Limited

- KPMG International

- PricewaterhouseCoopers LLP

- McKinsey & Company

- Boston Consulting Group

- Bain & Company

- Accenture PLC

- Kearney

- Roland Berger

- Capgemini Invent

- BearingPoint

- Oliver Wyman

- LEK Consulting

- Alvarez & Marsal

- Grant Thornton International

- BDO Advisory

- PA Consulting Group

- IBM Consulting

- Infosys Consulting

- Atos Consulting

- Wipro Consulting Services

- NTT DATA Business Solutions

- CGI Inc.

- Tata Consultancy Services(TCS)Consulting

第7章 市場機會與未來趨勢

- 評估差距和未滿足的需求

The Europe Consulting Services Market is expected to grow from USD 106.42 billion in 2025 to USD 112.51 billion in 2026 and is forecast to reach USD 148.55 billion by 2031 at 5.72% CAGR over 2026-2031.

This steady climb underscores how professional services firms have adapted to economic uncertainty, digital-first mandates, and tightening sustainability rules. Demand strengthens as the European Commission's Digital Europe Programme channels EUR 7.9 billion toward technology adoption, allowing service providers to expand cross-border engagements. Geopolitical supply-chain stress keeps operational excellence projects at the top of client agendas, while heavy AI investment by leading firms converts emerging technology into day-to-day consulting deliverables. Funding from the EU Recovery and Resilience Facility (RRF) accelerates small-business adoption of external expertise, widening the customer base and reducing dependence on large-enterprise budgets. Competitive intensity rises as the Big Four plough more than USD 4 billion into AI capabilities, reshaping service delivery economics and pushing mid-tier players toward niche specialisms.

Europe Consulting Services Market Trends and Insights

Regulatory Convergence for Cross-Border Services

The European Union is reducing administrative friction by aligning digital regulations, letting consulting firms replicate solutions across borders with fewer compliance checks. Germany and France formalized cooperation on interoperable public-sector software in 2024, giving early movers a chance to develop reusable playbooks that cut project lead times. Mid-sized providers gain new reach because they no longer need full legal teams for each country. While complete harmonization will not occur until 2027, firms that invest now in multilingual regulatory expertise stand to win multiyear frameworks as governments scale joint services.

Accelerated Client Demand for AI-Enabled Productivity Consulting

C-suites view artificial intelligence as an essential lever for cost containment and growth, translating into sizeable advisory pipelines. Germany's AI market alone is growing 15% annually and could add EUR 430 billion to GDP by 2030, underpinning a surge in AI strategy, data engineering, and change-management engagements. Deloitte's new Zora platform and EY's fleet of 150 AI agents illustrate how the largest firms are productizing intellectual property to deliver 25-40% productivity gains for clients. Smaller consultancies must pivot to hyper-specialized AI applications or risk margin squeeze as basic automation becomes commoditized.

Persistent Talent Deficit in Advanced Analytics

European consultancies cannot hire data scientists fast enough. CEDEFOP's Labour and Skills Shortage Index flags analytics and AI roles as high-pressure occupations through 2035. German and French governments report persistent gaps despite record tech job creation, forcing firms to pay premiums or offshore work. Scarcity inflates project costs and slows delivery, reducing the addressable volume for advanced analytics engagements. Smaller providers feel the pinch hardest because they struggle to match Big Four compensation packages, thereby intensifying market consolidation risks.

Other drivers and restraints analyzed in the detailed report include:

- EU Green Deal and CSRD Compliance Pressures

- SME Digital-Maturity Funding via EU RRF Grants

- Fee-Compression from Procurement-Led Negotiations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Operations consulting generated the largest revenue slice, capturing 28.12% of the European consulting services market share in 2025 as companies sought supply-chain resilience and cost savings amid geopolitical strains. The European consulting services market continues to prioritise lean manufacturing, process re-engineering, and working-capital optimization, anchoring steady fee streams for specialists. In parallel, digital transformation consulting is growing at a 7.49% CAGR, the fastest among all segments, powered by AI, cloud migration, and sustainability dashboards.

Strategy, financial advisory, and HR/change management retain essential roles, yet demand increasingly converges around integrated transformation offerings blending technology, risk management, and workforce enablement. Technology advisory enjoys heightened relevance because cyber threats multiply and cloud architectures fragment. Sustainability and ESG consulting now overlap with core operational mandates as firms embed carbon accounting into process flows. Service providers that create multidisciplinary squads around sector-specific playbooks will defend relevance as the European consulting services market shifts from siloed engagements toward platform-based, outcome-linked programmes.

The ICT and Media sector contributed 29.56% of 2025 revenue, reflecting constant technology refresh cycles and heavy software innovation. This client group continues to pilot generative AI, 5G monetization, and edge computing projects, sustaining robust demand within the European consulting services market. Consumer and Retail, however, is registering a 7.41% CAGR to 2031 as omnichannel investment, last-mile logistics, and data-driven merchandising accelerate.

Financial services keep consulting spend elevated on account of capital adequacy regulations and digital banking competition, while manufacturing turns to Industry 4.0 roadmaps and energy-efficient plant retrofits. Healthcare clients ramp up electronic-medical-record consolidation and cloud-hosted ERP migrations such as Asklepios Kliniken's SAP S/4HANA rollout, which required 18 months of external support. Energy and Utilities look for grid digitization and hydrogen-ready infrastructure planning, creating niche opportunities for sustainability-focused advisers.

Europe Consulting Services Market is Segmented by Service Type (Operations Consulting, Strategy Consulting, Financial Advisory, and More), Client Industry (BFSI, Manufacturing and Industrials, and More), Enterprise Size (Large Enterprises and Small and Medium Enterprises), Delivery Model (On-Site Engagement, Remote/Virtual, and Hybrid Model), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Deloitte Touche Tohmatsu Limited

- Ernst & Young Global Limited

- KPMG International

- PricewaterhouseCoopers LLP

- McKinsey & Company

- Boston Consulting Group

- Bain & Company

- Accenture PLC

- Kearney

- Roland Berger

- Capgemini Invent

- BearingPoint

- Oliver Wyman

- L.E.K. Consulting

- Alvarez & Marsal

- Grant Thornton International

- BDO Advisory

- PA Consulting Group

- IBM Consulting

- Infosys Consulting

- Atos Consulting

- Wipro Consulting Services

- NTT DATA Business Solutions

- CGI Inc.

- Tata Consultancy Services (TCS) Consulting

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory convergence for cross-border services

- 4.2.2 Accelerated client demand for AI-enabled productivity consulting

- 4.2.3 EU Green Deal and CSRD compliance pressures

- 4.2.4 SME digital-maturity funding via EU RRF grants

- 4.2.5 Shift to outcome-based pricing models

- 4.2.6 Near-shoring driven by geopolitical risk in supply chains

- 4.3 Market Restraints

- 4.3.1 Persistent talent deficit in advanced analytics

- 4.3.2 Fee-compression from procurement-led negotiations

- 4.3.3 Generative-AI DIY toolkits reducing entry-level work

- 4.3.4 Regulatory scrutiny on large integrator-consultant M&A

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Service Type

- 5.1.1 Operations Consulting

- 5.1.2 Strategy Consulting

- 5.1.3 Financial Advisory

- 5.1.4 Technology Advisory

- 5.1.5 HR and Change Management

- 5.1.6 Sustainability and ESG Consulting

- 5.1.7 Digital Transformation Consulting

- 5.2 By Client Industry

- 5.2.1 BFSI

- 5.2.2 Manufacturing and Industrials

- 5.2.3 Healthcare and Life Sciences

- 5.2.4 Energy and Utilities

- 5.2.5 ICT and Media

- 5.2.6 Consumer and Retail

- 5.2.7 Other Client Industries

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By Delivery Model

- 5.4.1 On-site Engagement

- 5.4.2 Remote/Virtual

- 5.4.3 Hybrid Model

- 5.5 By Country

- 5.5.1 United Kingdom

- 5.5.2 Germany

- 5.5.3 France

- 5.5.4 Benelux

- 5.5.5 Italy

- 5.5.6 Nordics

- 5.5.7 Spain

- 5.5.8 Central and Eastern Europe (incl. Poland)

- 5.5.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Deloitte Touche Tohmatsu Limited

- 6.4.2 Ernst & Young Global Limited

- 6.4.3 KPMG International

- 6.4.4 PricewaterhouseCoopers LLP

- 6.4.5 McKinsey & Company

- 6.4.6 Boston Consulting Group

- 6.4.7 Bain & Company

- 6.4.8 Accenture PLC

- 6.4.9 Kearney

- 6.4.10 Roland Berger

- 6.4.11 Capgemini Invent

- 6.4.12 BearingPoint

- 6.4.13 Oliver Wyman

- 6.4.14 L.E.K. Consulting

- 6.4.15 Alvarez & Marsal

- 6.4.16 Grant Thornton International

- 6.4.17 BDO Advisory

- 6.4.18 PA Consulting Group

- 6.4.19 IBM Consulting

- 6.4.20 Infosys Consulting

- 6.4.21 Atos Consulting

- 6.4.22 Wipro Consulting Services

- 6.4.23 NTT DATA Business Solutions

- 6.4.24 CGI Inc.

- 6.4.25 Tata Consultancy Services (TCS) Consulting

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-Space and Unmet-Need Assessment

諮詢4.0市場:2026-2032年全球預測(依產品類型、技術、應用、最終用戶及通路分類)企業敏捷轉型服務市場:2026-2032年全球市場預測(依服務類型、調查方法、轉型階段、合約模式、部署模式、產業及組織規模分類)

諮詢4.0市場:2026-2032年全球預測(依產品類型、技術、應用、最終用戶及通路分類)企業敏捷轉型服務市場:2026-2032年全球市場預測(依服務類型、調查方法、轉型階段、合約模式、部署模式、產業及組織規模分類) 2026年全球IT諮詢市場報告2026年全球企業敏捷轉型服務市場報告

2026年全球IT諮詢市場報告2026年全球企業敏捷轉型服務市場報告 企業敏捷轉型服務市場規模、佔有率、趨勢和預測:按方法論、服務類型、組織規模、產業和地區分類,2026-2034 年2026年全球公司秘書服務市場報告2026年全球房地產諮詢服務市場報告2026年全球精算諮詢服務市場報告2026年全球設計、研究、促銷與諮詢服務市場報告

企業敏捷轉型服務市場規模、佔有率、趨勢和預測:按方法論、服務類型、組織規模、產業和地區分類,2026-2034 年2026年全球公司秘書服務市場報告2026年全球房地產諮詢服務市場報告2026年全球精算諮詢服務市場報告2026年全球設計、研究、促銷與諮詢服務市場報告 2026-2030年全球行銷諮詢市場

2026-2030年全球行銷諮詢市場