|

市場調查報告書

商品編碼

1911741

印度鋼鐵:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)India Steel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

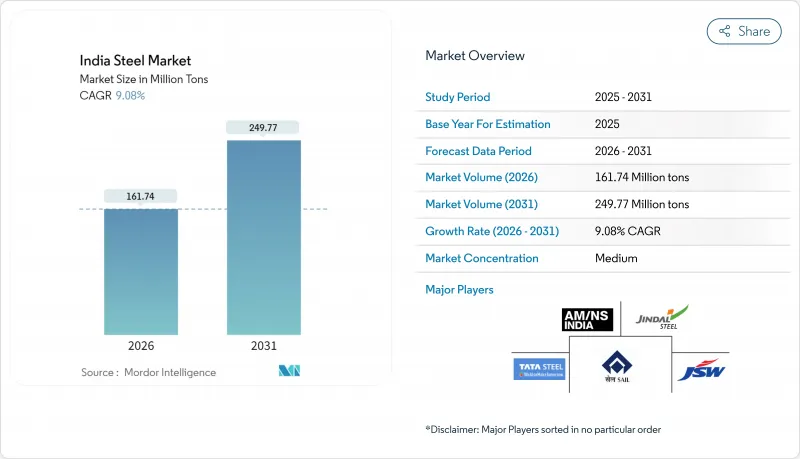

預計到 2026 年,印度鋼鐵市場規模將達到 1.6174 億噸,高於 2025 年的 1.4828 億噸。

預計到 2031 年產量將達到 2.4977 億噸,2026 年至 2031 年的複合年成長率為 9.08%。

2030年產能擴張至3億噸的目標、加速的基礎設施投資以及政策獎勵,正支撐印度鋼鐵業的成長軌跡,並使其成為世界第二大鋼鐵生產國。大型政府主導計劃(例如,34,800公里長的「印度公路網」(Bharatmala)、「總理住宅計畫」(PM-AWAS)和「智慧城市2.0」計畫)正在創造持續的國內需求,而新興的綠色鋼鐵政策體係正在刺激對低碳技術的投資。主要生產商競相確保現有和新增產能,對沖進口激增的風險,並遵守歐盟碳邊境調節機制(CBAM)等出口相關環境法規,因此競爭依然激烈。同時,各邦在原料供應和物流網路方面的優勢正在推動生產向東部轉移,從而促進區域經濟發展並最佳化供應鏈成本。儘管印度鋼鐵業增加了脫碳支出、提高了資本效率並採取了增值產品策略,但這些措施在原料價格波動的情況下仍有助於保護營運利潤率,從而增強了印度鋼鐵業的整體韌性。

印度鋼鐵市場趨勢與洞察

強而有力的政策支持

國家鋼鐵政策設定的3億噸產能目標、特種鋼生產關聯激勵計畫(PLI)以及國內鋼鐵強制生產規定,共同建構了一個全面的框架,為整個印度鋼鐵業的需求確定性提供了保障。生產連結獎勵計畫(總額達2,710.6億盧比)已在特種鋼領域創造了790萬噸產能,並創造了約1.5萬個就業機會。政府採購中15%至50%的增值優惠標準為國內供應商提供了支持,而透過鋼鐵進口監控系統進行的即時進口監控則有助於完善貿易救濟措施。透過總理成長能力計畫(PM-Gati Shakti)實現的基礎設施整合,可將物流成本降低高達15%,進而提升礦產資源豐富地區生產商的競爭力。最後,印度標準局(BIS)執行的嚴格品質標準確保新增產能能夠生產符合國際標準的優質產品,以滿足出口市場需求。

國內外對棕地和待開發區設施的資本投資迅速增加

印度鋼鐵業的投資週期正在加速,公私合營投資總額已超過250億美元。產業主要企業紛紛進入該領域,現有企業也不斷擴張。安賽樂米塔爾日本鋼鐵公司在安得拉邦投資15兆盧比的鋼鐵廠,正是以技術轉移主導的先進高強度鋼現代化改造的典範。印度鋼鐵管理局(SAIL)計劃透過2025會計年度分階段的資本支出預算撥款,到2031年將其產能從2000萬噸擴大到3565萬噸,這表明公共部門與國家目標保持一致。戰略性外國直接投資(FDI)的流入正在引入低碳技術專長,而礦產資源豐富的東部叢集正在縮短原料供應線,並實現規模經濟。就業乘數效應,加上邦政府的支持,正在印度鋼鐵業形成技能發展和產業成長的良性循環。

人均鋼鐵消費量仍低於世界平均水平

預計到2023年,印度人均鋼鐵消費量將達到93.44公斤,遠低於230公斤的全球平均水準。這不僅顯示印度鋼鐵業潛力尚未充分發揮,也凸顯了結構性瓶頸。由於基礎設施覆蓋率低和收入限制,佔印度人口65%的農村市場需求仍顯著偏低。消費量差異使得生產力計畫決策更加複雜,因為生產者必須在擴大供應的同時兼顧實際的區域需求曲線。這些趨勢表明,為了充分發揮印度鋼鐵業的潛力,必須同步投資農村基礎建設。

細分市場分析

截至2025年,高爐-氧氣轉爐(BF-BOF)製程將佔印度鋼鐵業46.12%的佔有率,證實了一體化工廠的堅實基礎,此類工廠在大批量生產方面仍具有成本優勢。隨著生產商制定脫碳藍圖並最佳化現有設施,預計印度BF-BOF市場規模將以8.77%的複合年成長率成長。透過部分氫氣注入實現效率的逐步提高和單位排放的降低,顯示轉型步伐切實可行。電弧爐在廢鋼豐富的都市區越來越受歡迎,這預示著未來產能將重新配置到低碳地區。新興的氫氣直接還原鐵(DRI)先導工廠提供了第三種選擇,但其商業化取決於綠色氫氣的成本競爭力,預計要到2030年或更晚才能實現。

中期來看,高爐-氧氣轉爐聯合煉鋼廠將透過改進熱風爐、上壓回收渦輪機和爐渣造粒設備來提升能源回收和產品品質。技術合作將加速製程控制的數位化,從而擴大最佳實踐工廠與普通工廠之間的產量差距。同時,二次煉鋼企業將利用電弧爐的柔軟性,靈活應對特殊鋼材供應和不斷變化的建築標準。多種煉鋼路徑並存反映了印度鋼鐵市場的規模和廢鋼供應的區域差異,顯示技術重組將是一個漸進的過程,而不是突飛猛進。

粗鋼是整體基礎鋼種,預計將以7.73%的複合年成長率成長,這反映了上游綜合鋼廠和二級鋼廠產能的擴張。約80%的高產運轉率表明,在需要大規模新建設之前,產能潛力巨大。奧裡薩邦、恰蒂斯加爾邦和卡納塔克邦的鐵礦石自給自足,使粗鋼生產商相對於東南亞依賴進口的同行擁有持續的原料優勢,從而鞏固了印度鋼鐵業的區域地位。

印度鋼鐵市場產量成長得益於一系列扶持政策,例如礦場自用配額和快速核准擴建計劃環境影響評估。同時,廢鋼回收政策將廢鋼利用率從25%提高到70%,提升了生產效率。鋼鐵生產商正在加速採用預測性維護分析和製程最佳化軟體,以縮小與行業領先水平的差距並降低能源消耗強度。這些共同努力鞏固了鋼鐵業作為印度鋼鐵產業核心組成部分的地位。

印度鋼鐵市場報告按技術(高爐/鹼性氧氣轉爐、電弧爐、其他技術)、基本形態(粗鋼)、最終形態(成品鋼)和終端用戶行業(汽車及運輸設備、建築施工、工具及機械、消費品、能源、其他終端用戶行業)進行細分。市場預測以百萬噸為單位。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 強而有力的政策支持

- 國內外棕地及待開發區設施資本支出(CAPEX)快速成長

- 大型基礎建設項目(Bharatmala計劃、PM-AWAS計劃、智慧城市2.0)

- 汽車原始設備製造商轉向高強度先進高強度鋼和電動汽車用鋼

- 氫基直接還原鐵試驗計畫及廢鋼替代推廣

- 市場限制

- 人均鋼鐵消費量仍低於全球平均水平

- 原料和能源成本波動

- 與環境、社會及公司治理(ESG)掛鉤的出口碳關稅(例如歐盟碳排放交易體系)

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭程度

第5章 市場規模與成長預測

- 透過技術

- 高爐-轉爐(BF-BOF)

- 電弧爐(EAF)

- 其他技術

- 按基本形式

- 粗鋼

- 最終形式

- 成品鋼材

- 按最終用戶行業分類

- 汽車/運輸設備

- 建築/施工

- 工具/機器

- 消費品

- 能源

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、合資、資本支出、綠色鋼鐵交易)

- 市佔率(%)/排名分析

- 公司簡介

- AM/NS India

- Godawari Power and Ispat

- Jindal Steel & Power Limited

- JSW Steel Limited

- Kalyani Steels

- Mukand Ltd.

- NMDC Steel Limited

- Rashtriya Ispat Nigam Limited

- Steel Authority of India Limited(SAIL)

- Tata Steel

- Vedanta Limited

- VISA STEEL

第7章 市場機會與未來展望

India Steel Market size in 2026 is estimated at 161.74 million tons, growing from 2025 value of 148.28 million tons with 2031 projections showing 249.77 million tons, growing at 9.08% CAGR over 2026-2031.

Expanding capacity targets of 300 million tons by 2030, accelerating infrastructure spending, and policy incentives together anchor this trajectory, positioning the India steel industry as the world's second-largest producer cohort. Government-backed megaprojects such as Bharatmala's 34,800 km highway build-out, PM-AWAS's large-scale housing programs, and Smart Cities 2.0 create durable domestic offtake, while an emerging green-steel policy ecosystem channels investment toward low-carbon technologies. Competitive intensity remains high, as leading producers race to secure brown- and green-field capacity, hedge against import surges, and comply with export-linked environmental mandates, such as the EU's CBAM. Simultaneously, state-level advantages in raw material availability and logistics connectivity spur an eastward production shift, supporting regional economic development and optimizing supply chain costs. Despite rising decarbonization outlays, capital efficiency gains, and value-added product strategies, these help shield operating margins amid volatile raw-material prices, thereby strengthening the overall resilience of the India steel industry.

India Steel Market Trends and Insights

Strong Policy Support

A comprehensive framework, combining the National Steel Policy's 300 million ton capacity target, the PLI scheme for specialty steel, and the mandate for domestically manufactured iron and steel products, underpins demand certainty across the India steel industry. Production-linked incentives worth INR 27,106 crore have already unlocked 7.9 million tons of specialty capacity and nearly 15,000 jobs. Preferential procurement thresholds of 15-50% value-added bolster domestic suppliers in government tenders, while real-time import monitoring via the Steel Import Monitoring System refines trade remedy decisions. Infrastructure integration through PM-Gati Shakti lowers logistics costs by up to 15%, sharpening competitiveness for producers in mineral-rich regions. Finally, the Bureau of Indian Standards enforces quality compliance, ensuring that new capacity delivers globally acceptable product grades that align with export market requirements.

Surge in Domestic and Foreign CAPEX for Brown-/Green-field Capacity

Private and public commitments exceeding USD 25 billion have amplified the India Steel investment cycle, drawing marquee entrants and expanding incumbents. ArcelorMittal Nippon Steel's INR 1.5 lakh crore Andhra Pradesh complex exemplifies technology-transfer driven upgrades in advanced high-strength grades. SAIL's trajectory from 20 million tons to 35.65 million tons capacity by 2031, supported by incremental FY25 capex allocations, highlights public-sector alignment with national targets. Strategic FDI flows embed knowledge of low-carbon technologies, while mineral-rich eastern clusters shorten raw material supply lines and enable economies of scale. Employment multipliers reinforce state support, creating virtuous cycles of skill development and industrial growth across the India Steel industry.

Per-Capita Steel Consumption Still Below Global Average

At 93.44 kg in 2023, India's per-capita steel usage remains far below the 230 kg global mean, signaling untapped potential but also revealing structural bottlenecks. Rural markets, which account for 65% of the population, have disproportionately low demand due to limited infrastructure penetration and income constraints. Consumption disparities complicate capacity-planning decisions, as producers must balance supply expansion with realistic regional demand curves. These patterns underline the need for parallel investments in rural infrastructure to unlock the full potential of the India Steel industry.

Other drivers and restraints analyzed in the detailed report include:

- Large Infrastructure Pipeline (Bharatmala, PM-AWAS, Smart Cities 2.0)

- Hydrogen-Based DRI Pilots and Scrap Substitution Push

- ESG-Linked Export Carbon Tariffs (EU CBAM)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The BF-BOF route held 46.12% India Steel industry share in 2025, a level underscoring the entrenched integrated-plant footprint that still delivers cost advantages on large volumes. The India steel market size for BF-BOF output is forecast to compound at an 8.77% CAGR as producers sweat existing assets even while charting decarbonization roadmaps. Declining unit emissions through incremental efficiency gains and partial hydrogen injection illustrate pragmatic transition pacing. Electric-arc furnaces are gaining traction in scrap-rich urban clusters, signaling a future redistribution of capacity toward low-carbon hubs. Emerging hydrogen DRI pilot plants introduce a third vector, although commercial uptake hinges on green-hydrogen cost parity, which is expected only beyond 2030.

In the medium term, BF-BOF complexes evolve through the use of hot-blast stoves, top-pressure recovery turbines, and slag granulation upgrades, thereby enhancing energy recovery and product quality. Technology partnerships accelerate process-control digitalization, widening yield spreads between best- and average-practice plants. Meanwhile, secondary producers leverage EAF flexibility to nimbly supply specialty grades and meet evolving construction standards. The coexistence of multiple routes reflects the India Steel market size and varied regional scrap-availability profiles, suggesting a gradual rather than abrupt technology realignment.

Crude steel constitutes the entire basic-form segment and is forecast to climb at a 7.73% CAGR, mirroring upstream capacity additions across integrated and secondary mills. High utilization rates of roughly 80% underscore latent headroom before extensive green-field builds are required. Iron-ore self-sufficiency across Odisha, Chhattisgarh, and Karnataka grants crude-steel producers a sustained raw-material edge compared with import-dependent peers in Southeast Asia, strengthening the india steel industry position in the region.

Enabling policies, such as captive mine allocations and express environmental clearances for expansion projects, expedite throughput gains in the India steel market. Simultaneously, the Steel Scrap Recycling Policy aims to lift scrap use from 25% to 70%, driving process efficiency. Crude steel players are increasingly integrating predictive maintenance analytics and process optimization software, narrowing the gap to best performance and trimming energy intensity. These moves collectively solidify the segment's centrality within the India steel industry.

The India Steel Report is Segmented by Technology (Blast Furnace-Basic Oxygen Furnace, Electric Arc Furnace, and Other Technologies), Basic Form (Crude Steel), Final Form (Finished Steel), and End-User Industry (Automotive and Transportation, Building and Construction, Tools and Machinery, Consumer Goods, Energy, and Other End-User Industries). The Market Forecasts are Provided in Terms of Volume (Million Tons).

List of Companies Covered in this Report:

- AM/NS India

- Godawari Power and Ispat

- Jindal Steel & Power Limited

- JSW Steel Limited

- Kalyani Steels

- Mukand Ltd.

- NMDC Steel Limited

- Rashtriya Ispat Nigam Limited

- Steel Authority of India Limited (SAIL)

- Tata Steel

- Vedanta Limited

- VISA STEEL

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Strong Policy Support

- 4.2.2 Surge in Domestic and Foreign CAPEX for Brown-/Green-Field Capacity

- 4.2.3 Large Infrastructure Pipeline (Bharatmala, PM-AWAS, Smart Cities 2.0)

- 4.2.4 Auto OEM Pivot to High-Strength AHSS and EV-Grade Steels (Under-Reported)

- 4.2.5 Hydrogen-Based DRI Pilots and Scrap Substitution Push (Under-Reported)

- 4.3 Market Restraints

- 4.3.1 Per-Capita Steel Consumption Still Below Global Average.

- 4.3.2 Volatile Raw-Material and Energy Costs

- 4.3.3 ESG-Linked Export Carbon Tariffs (E.G., EU CBAM) (Under-Reported)

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products and Services

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Technology

- 5.1.1 Blast Furnace-Basic Oxygen Furnace (BF-BOF)

- 5.1.2 Electric Arc Furnace (EAF)

- 5.1.3 Other Technologies

- 5.2 By Basic Form

- 5.2.1 Crude Steel

- 5.3 By Final Form

- 5.3.1 Finished Steel

- 5.4 By End-user Industry

- 5.4.1 Automotive and Transportation

- 5.4.2 Building and Construction

- 5.4.3 Tools and Machinery

- 5.4.4 Consumer Goods

- 5.4.5 Energy

- 5.4.6 Other End-User Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (MandA, JVs, CAPEX, Green-steel deals)

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global-level overview, Market-level overview, Core segments, Financials, Strategic information, Market rank/share, Products and Services, Recent developments)

- 6.4.1 AM/NS India

- 6.4.2 Godawari Power and Ispat

- 6.4.3 Jindal Steel & Power Limited

- 6.4.4 JSW Steel Limited

- 6.4.5 Kalyani Steels

- 6.4.6 Mukand Ltd.

- 6.4.7 NMDC Steel Limited

- 6.4.8 Rashtriya Ispat Nigam Limited

- 6.4.9 Steel Authority of India Limited (SAIL)

- 6.4.10 Tata Steel

- 6.4.11 Vedanta Limited

- 6.4.12 VISA STEEL

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Circular Economy and Scrap Processing Hubs

- 7.3 Green-steel Premiums and Export Windows

2026-2030年全球鋼鐵製造市場

2026-2030年全球鋼鐵製造市場 2026年全球鍍鋅鋼板市場研究報告

2026年全球鍍鋅鋼板市場研究報告 2026年至2034年鋼鐵市場規模、佔有率、趨勢及預測(按類型、產品類型、應用及地區分類)日本鋼鐵市場報告:按類型、產品類型、應用和地區分類,2026-2034年

2026年至2034年鋼鐵市場規模、佔有率、趨勢及預測(按類型、產品類型、應用及地區分類)日本鋼鐵市場報告:按類型、產品類型、應用和地區分類,2026-2034年 2026年全球合金鋼市場報告2026年全球軋延和拉拔鋼材市場報告2026年全球鋼鐵產品市場報告2026年全球液壓沖剪機市場報告

2026年全球合金鋼市場報告2026年全球軋延和拉拔鋼材市場報告2026年全球鋼鐵產品市場報告2026年全球液壓沖剪機市場報告 W型鋼帶市場依產品類型、鋼材等級、表面處理、厚度及最終用途分類-全球預測(2026-2032年)低碳不銹鋼帶鋼市場按等級、製程、表面處理、厚度和應用分類,全球預測(2026-2032年)

W型鋼帶市場依產品類型、鋼材等級、表面處理、厚度及最終用途分類-全球預測(2026-2032年)低碳不銹鋼帶鋼市場按等級、製程、表面處理、厚度和應用分類,全球預測(2026-2032年)