|

市場調查報告書

商品編碼

1911474

法國POS終端市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)France POS Terminal - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

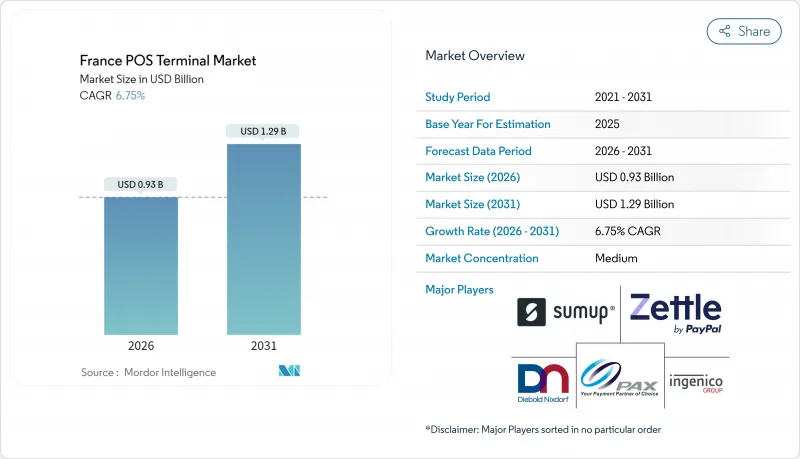

法國POS終端市場預計將從2025年的8.7億美元成長到2026年的9.3億美元,到2031年達到12.9億美元,2026年至2031年的複合年成長率為6.75%。

強勁的需求主要受非接觸式支付使用量成長、PSD2(支付服務指令II)相關監管要求和強客戶認證以及歐洲支付舉措組織 (EPI) wero 服務的推廣等因素驅動,這些因素都促使商家升級舊終端。硬體供應商受惠於覆蓋約230萬個商家分行的更新換代週期,而軟體供應商則透過降低小規模企業總體擁有成本 (TCO) 的 SoftPOS 解決方案不斷擴大市場佔有率。儘管固定終端在高交易量零售環境中仍佔據主導地位,但隨著飯店、零工經濟和路邊取貨業者優先考慮支付柔軟性,行動終端正在逐步成長。市場競爭依然適中。 Worldline 透過 Ingenico 佔據 35% 的市場佔有率,而 Verifone、PAX Technology 和快速成長的 SoftPOS參與企業正在加劇價格競爭並加速產品創新。

法國POS終端市場趨勢與洞察

非接觸式支付的激增正在重塑終端要求。

到2024年,法國消費者將推動非接觸式支付在POS交易中的比例達到70%,超過歐洲58%的平均水準。 50歐元的消費限額提高了平均交易額,促使商家優先考慮支援NFC和傳統非接觸式支付的雙介面終端。家樂福和歐尚等大型零售商已在商店交易中使用非接觸式支付,而隨著非接觸式支付率下降23%,老舊終端的更新換代正在加速。因此,法國POS終端市場正著力提升NFC性能、電池續航力以及適用於戶外市場和配送車輛的離線非接觸式功能。區域差異依然存在,法蘭西島大區的滲透率超過85%,而農村地區的滲透率僅為62%,這給提供連接最佳化解決方案的供應商造成了地理上的缺口。

全通路零售數位化加速基礎設施現代化

整合商務策略正迫使零售商透過整合設備同步線上、行動裝置和商店資料流。 Fnac-Darty在2024年部署了15,000台整合終端,這表明市場對能夠透過單一螢幕處理訂單、退貨和庫存查詢的系統有著強勁的需求。在銷售額超過1,000萬歐元的連鎖店中,約有68%計劃在2026年前完成升級,隨著零售商擴大從固定收銀台轉向可在店內移動的行動終端,法國POS終端市場也將隨之擴大。行動終端的普及縮短了顧客等待時間,提高了員工效率,並將忠誠度分析數據連接到雲端平台,這促使以軟體為中心的供應商將支付應用程式、客戶關係管理(CRM)和庫存管理工具打包成訂閱方案。

中小企業的成本意識是採用新技術的一大障礙。

約73%的法國中小企業表示,成本是升級硬體的主要障礙。設備價格從200歐元到800歐元不等,每月費用從15歐元到45歐元不等,這給利潤微薄、業務量大的企業帶來了沉重負擔。在仍需使用GPRS作為備用網路的遍遠地區,網路連線的不足進一步加劇了預算壓力。政府透過「法國遠距」(France Le Rance)計畫提供500歐元的補貼,但繁瑣的申請流程限制了參與,並將許多服務供應商排除在外。供應商正透過提供24至36個月的設備分期付款計劃和推廣SoftPOS應用程式來應對這一問題,但普及速度仍然緩慢。

細分市場分析

至2025年,非接觸式終端將佔法國POS終端市場55.92%的佔有率,並將以8.11%的複合年成長率成長,到2031年成為市場主流。這項轉變與計畫於2026年推出的數位歐元密切相關,屆時將強制要求使用能夠進行央行數位貨幣(CBDC)交易的雙模終端。目前,高價值奢侈品和汽車經銷商在50歐元以上的交易中仍然依賴基於PIN碼的晶片認證,但消費者的偏好表明,近場通訊(NFC)具有明顯的優勢。

非接觸式支付的未來成長將主要得益於2023年起雙界面卡94%的發行率以及Carte Bancaire計劃中25歐元的離線非接觸式支付限額。這些因素將擴大非接觸式支付在戶外市場和網路連接較差的配送車輛中的應用,從而推動對小型化、節能型讀卡器的需求成長。區域差異依然存在:法蘭西島大區的非接觸式支付普及率已達85%,而農村地區的普及率仍僅為62%,這促使廠商推出低覆蓋範圍的讀卡器以挖掘尚未開發的潛在需求。隨著非接觸式支付部署的擴大,預計法國POS終端市場的非接觸式硬體銷售量將超過整體市場平均水平,這將促使供應商更加關注NFC無線電的可靠性、天線設計以及EMV 3級認證週期。

其他福利

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 法國消費者非接觸式支付方式普及率激增

- 全通路零售數位化加速POS系統更新周期

- 根據支付服務指令2 (PSD2) 制定的歐盟和各國無現金經濟促進措施和加強安全措施

- 基於智慧型手機的軟POS系統和非接觸式支付降低了中小型零售商的整體硬體擁有成本。

- 歐洲支付舉措(EPI) 正準備支持在傳統 POS 機上進行帳戶間QR CODE支付。

- 消費者對店內先買後付/短期分期付款選項的需求日益成長。

- 市場限制

- 對於法國的中小型企業來說,設備的初始成本和維護成本都非常高。

- PCI-DSS/SCA網路安全合規負擔加重

- 即將到來的後量子密碼技術升級將使韌體生命週期更加複雜。

- 隨著顧客流量從實體店轉向電子商務,傳統固定POS終端的運轉率正在下降。

- 產業價值鏈分析

- 監管環境

- 技術展望

- 宏觀經濟因素的影響

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 透過付款方式

- 聯繫類型

- 非接觸式

- 按POS類型

- 固定式POS系統

- 行動/可攜式POS系統

- 按最終用戶行業分類

- 零售

- 飯店業

- 衛生保健

- 運輸/物流

- 其他

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Ingenico Group SA(Worldline)

- Verifone Systems, Inc.

- PAX Technology Ltd.

- NCR Corporation

- Castles Technology Co., Ltd.

- SumUp Payments Limited

- Zettle(Paypal)

- myPOS World Ltd.

- NEC Corporation

- AURES Group SA

- Diebold Nixdorf

- BBPOS Limited

- Newland Payment Technology Co., Ltd.

- Shenzhen Xinguodu Technology Co., Ltd.

- Fujian Centerm Information Co., Ltd.

- Bitel Co., Ltd.

- Wiseasy Technology Co., Ltd.

- Fujian Landi Commercial Equipment Co., Ltd.

- dejamobile SAS

- Innovorder SAS

第7章 市場機會與未來展望

The France POS Terminal Market is expected to grow from USD 0.87 billion in 2025 to USD 0.93 billion in 2026 and is forecast to reach USD 1.29 billion by 2031 at 6.75% CAGR over 2026-2031.

Robust demand arises from rising contactless-payment usage, regulatory mandates linked to PSD2 and Strong Customer Authentication, and the rollout of the European Payments Initiative's wero service, all of which compel merchants to refresh legacy devices. Hardware suppliers benefit from a replacement cycle encompassing roughly 2.3 million merchant locations, while software vendors gain share through SoftPOS offerings that lower total cost of ownership for micro-enterprises. Fixed terminals still dominate high-volume retail environments, yet mobile devices capture incremental growth as hospitality, gig-economy and curbside-pickup operators prioritize payment flexibility. Competition remains moderate: Worldline commands a 35% position via Ingenico, but Verifone, PAX Technology and fast-scaling SoftPOS players intensify pricing pressure and speed product innovation.

France POS Terminal Market Trends and Insights

Contactless Payment Surge Reshapes Terminal Requirements

French consumers pushed contactless uptake to 70% of POS transactions in 2024, eclipsing the 58% European average. The higher EUR 50 limit enhanced average ticket values and motivated merchants to prioritize dual-interface devices that support both NFC and traditional contact entry. Retailers Carrefour and Auchan already see contactless exceeding 80% of in-store volume, accelerating refresh cycles as aging terminals correlate with 23% lower contactless rates. The France POS terminal market consequently concentrates on NFC performance, battery longevity and offline contactless functions that suit outdoor markets and delivery fleets. Regional disparities remain, penetration tops 85% in Ile-de-France but lags at 62% in rural departements, offering vendors geographic white space for connectivity-optimized solutions.

Omnichannel Retail Digitalisation Accelerates Infrastructure Modernisation

Unified commerce strategies compel retailers to synchronize online, mobile and in-store data streams through integrated devices. Fnac-Darty installed 15,000 unified terminals in 2024, showcasing demand for systems that process orders, returns and inventory queries from a single screen. Nearly 68% of chains above EUR 10 million revenue plan upgrades by 2026, boosting the France POS terminal market as operators replace fixed checkout lanes with mobile stations that roam shop floors. Mobile deployments shorten wait times, improve staff efficiency and feed loyalty analytics into cloud platforms, encouraging software-centric suppliers to bundle payment apps, CRM and inventory tools via subscription.

SME Cost Sensitivity Creates Adoption Friction

Almost 73% of French SMEs cite cost as the main barrier to hardware refresh, as devices priced at EUR 200-800 and monthly fees of EUR 15-45 erode thin margins. Connectivity gaps further inflate budgets in rural areas that still require GPRS fall-back. Though the government offers EUR 500 subsidies under France Relance, complex paperwork limits participation, leaving many service providers outside the program. Vendors respond by financing terminals over 24-36 months or promoting SoftPOS apps, yet penetration gains remain gradual.

Other drivers and restraints analyzed in the detailed report include:

- EU Policy Framework Mandates Security and Interoperability Upgrades

- SoftPOS Technology Reduces Barriers for Micro-Merchant Adoption

- Cybersecurity Compliance Burden Intensifies Operational Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Contact-based solutions controlled 55.92% of the France POS terminal market share in 2025, yet contactless devices are forecast to record an 8.11% CAGR, pushing the segment toward majority status well before 2031. This transition parallels the digital euro pilot slated for 2026, which requires dual-mode devices capable of CBDC transactions. High-value luxury and automotive merchants still lean on PIN-based chip entry for transactions above EUR 50, but consumer preference signals inexorable NFC dominance.

Subsequent growth in contactless acceptance stems from 94% dual-interface card issuance since 2023 and the Carte Bancaire scheme's offline-contactless limit of EUR 25. These features broaden applicability to outdoor markets and delivery vans with intermittent connectivity, spurring incremental volumes for compact, battery-efficient readers. Regional disparities persist: Ile-de-France logs 85% contactless penetration, whereas rural areas hover at 62%, encouraging suppliers to launch low-connectivity variants that exploit untapped potential. As these deployments scale, the France POS terminal market size for contactless hardware is set to outpace overall market averages, reinforcing vendors' focus on NFC radio integrity, antenna design and EMV Level 3 certification cycles.

The France POS Terminal Market Report is Segmented by Mode of Payment Acceptance (Contact-Based, and Contactless), POS Type (Fixed Point-Of-Sale Systems, and Mobile/Portable Point-Of-Sale Systems), End-User Industry (Retail, Hospitality, Healthcare, Transportation and Logistics, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Ingenico Group SA (Worldline)

- Verifone Systems, Inc.

- PAX Technology Ltd.

- NCR Corporation

- Castles Technology Co., Ltd.

- SumUp Payments Limited

- Zettle (Paypal)

- myPOS World Ltd.

- NEC Corporation

- AURES Group SA

- Diebold Nixdorf

- BBPOS Limited

- Newland Payment Technology Co., Ltd.

- Shenzhen Xinguodu Technology Co., Ltd.

- Fujian Centerm Information Co., Ltd.

- Bitel Co., Ltd.

- Wiseasy Technology Co., Ltd.

- Fujian Landi Commercial Equipment Co., Ltd.

- dejamobile SAS

- Innovorder SAS

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in contactless-payment penetration among French consumers

- 4.2.2 Omnichannel retail digitalisation accelerating POS refresh cycles

- 4.2.3 EU and national policies promoting cash-lite economy and PSD2-driven security upgrades

- 4.2.4 SoftPOS and Tap-to-Pay on smartphones slashing hardware TCO for micro-merchants

- 4.2.5 European Payments Initiative (EPI) preparing account-to-account QR acceptance on legacy POS

- 4.2.6 Rising demand for in-terminal BNPL / short-instalment options at checkout

- 4.3 Market Restraints

- 4.3.1 High upfront terminal and maintenance costs for French SMEs

- 4.3.2 Heightened PCI-DSS/SCA cybersecurity compliance burden

- 4.3.3 Looming post-quantum crypto upgrades complicating firmware lifecycles

- 4.3.4 Foot-traffic shift to e-commerce leaving legacy fixed POS capacity under-utilised

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Mode of Payment Acceptance

- 5.1.1 Contact-based

- 5.1.2 Contactless

- 5.2 By POS Type

- 5.2.1 Fixed Point-of-Sale Systems

- 5.2.2 Mobile / Portable Point-of-Sale Systems

- 5.3 By End-User Industry

- 5.3.1 Retail

- 5.3.2 Hospitality

- 5.3.3 Healthcare

- 5.3.4 Transportation and Logistics

- 5.3.5 Other End-user Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Ingenico Group SA (Worldline)

- 6.4.2 Verifone Systems, Inc.

- 6.4.3 PAX Technology Ltd.

- 6.4.4 NCR Corporation

- 6.4.5 Castles Technology Co., Ltd.

- 6.4.6 SumUp Payments Limited

- 6.4.7 Zettle (Paypal)

- 6.4.8 myPOS World Ltd.

- 6.4.9 NEC Corporation

- 6.4.10 AURES Group SA

- 6.4.11 Diebold Nixdorf

- 6.4.12 BBPOS Limited

- 6.4.13 Newland Payment Technology Co., Ltd.

- 6.4.14 Shenzhen Xinguodu Technology Co., Ltd.

- 6.4.15 Fujian Centerm Information Co., Ltd.

- 6.4.16 Bitel Co., Ltd.

- 6.4.17 Wiseasy Technology Co., Ltd.

- 6.4.18 Fujian Landi Commercial Equipment Co., Ltd.

- 6.4.19 dejamobile SAS

- 6.4.20 Innovorder SAS

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

電子資金轉帳市場:按支付方式、交易類型、組成部分和最終用戶分類-2026-2032年全球市場預測POS終端市場:按類型、連接方式、部署方式和最終用戶分類-2026-2032年全球市場預測EMV POS終端市場:2026-2032年全球市場預測(依產品類型、連接方式、部署方式、支付方式及最終用戶分類)近距離場通訊 (NFC) POS 終端和支付市場:按組件、產品類型、支付方式、部署模式、組織規模和產業分類-2026-2032 年全球市場預測

電子資金轉帳市場:按支付方式、交易類型、組成部分和最終用戶分類-2026-2032年全球市場預測POS終端市場:按類型、連接方式、部署方式和最終用戶分類-2026-2032年全球市場預測EMV POS終端市場:2026-2032年全球市場預測(依產品類型、連接方式、部署方式、支付方式及最終用戶分類)近距離場通訊 (NFC) POS 終端和支付市場:按組件、產品類型、支付方式、部署模式、組織規模和產業分類-2026-2032 年全球市場預測 2026年全球銷售點終端市場報告人工智慧終端市場:按組件、組織規模、部署模式、技術、應用和產業分類-2026-2032年全球預測2026年全球零售POS終端市場報告2026年全球餐飲POS終端市場報告POS終端市場按組件、部署方式、外形規格、最終用戶和銷售管道,全球預測,2026-2032年

2026年全球銷售點終端市場報告人工智慧終端市場:按組件、組織規模、部署模式、技術、應用和產業分類-2026-2032年全球預測2026年全球零售POS終端市場報告2026年全球餐飲POS終端市場報告POS終端市場按組件、部署方式、外形規格、最終用戶和銷售管道,全球預測,2026-2032年 POS終端市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶及功能分類

POS終端市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶及功能分類