|

市場調查報告書

商品編碼

1911333

圍籬:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Fencing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

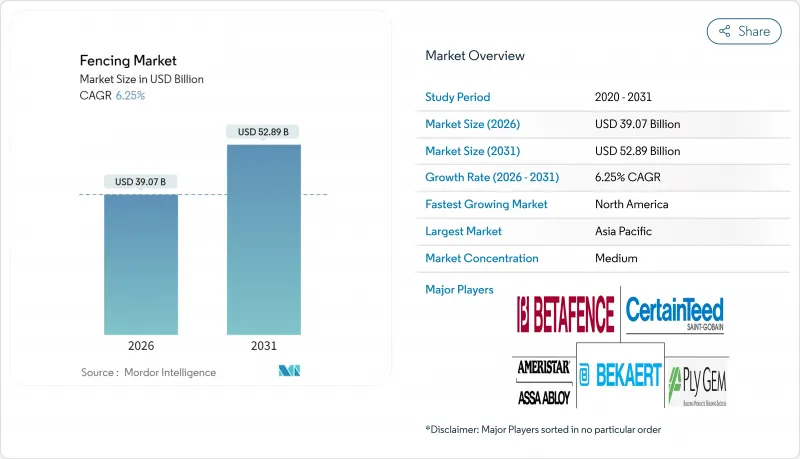

據估計,2026年圍籬市場規模將達到390.7億美元,高於2025年的367.7億美元,預計2031年將達到528.9億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 6.25%。

這一成長反映了電力網、資料中心和邊境安全措施的強制性加強,智慧邊境硬體的快速商業化,以及政府對基礎設施的持續投資。金屬製品因其耐用性和全生命週期成本優勢,繼續在大型計劃佔據主導地位,但由於氣候適應性設計要求,複合材料和PVC替代品正迅速普及。住宅的需求依然強勁,而農業和可再生能源設施正成為成長最快的領域。由於物聯網系統帶來的技術挑戰日益增加,專業承包商佔據了大部分收入,而成熟的住宅市場對DIY套件的需求也在增加。從區域來看,北美憑藉聯邦政府的支出計劃保持主導地位,但亞太地區預計將在數十億美元的邊境和工業項目的推動下超越其他所有地區。

全球圍籬市場趨勢與洞察

政府基礎設施支出推動了邊境安全需求。

國家安全優先事項體現在用於邊境防禦和關鍵資產保護的巨額多年預算中。印度已撥款3,250億盧比(約38.9億美元),用於在敏感邊境沿線建造圍欄和道路,並指定採用防切割和防攀爬的鋼結構設計,該撥款將持續到2034年。北美電力可靠性公司(NERC)修訂的指導方針要求在高影響電網控制中心安裝防撞大門,迫使電力公司維修老化的周界設施。美國聯邦建築規範現已納入「透過環境設計預防犯罪」(CPTED)原則,該原則規定採用多層屏障和電子門禁系統。這些法規推動了對高規格設備的需求,並有利於擁有安全許可的供應商。

智慧感測器圍欄系統越來越受歡迎

物聯網的整合正在將被動式圍欄轉變為主動式威脅偵測網路。 IEEE 的研究表明,與傳統光束偵測器相比,多感測器智慧圍欄可將誤報率降低 60%。美國近期更新了通訊標準,納入了安全的物聯網介面,這影響了商業產品藍圖。遵循美國國家安全航空聯盟最佳實踐的機場,現在指定採用整合影像分析、雷達和身份驗證資料庫的周界解決方案。國防安全保障部的檢驗通訊協客製化定了統一的性能指標,以加快採購週期。

鋼材、木材和PVC樹脂價格波動

能源成本和電氣化需求持續給金屬和樹脂市場帶來壓力。世界銀行金屬指數在2024年4月上漲了9%,預示2025年基底金屬價格將進一步上漲。世紀鋁業在國內減產凸顯了鋁供應對成本的敏感度。博伊西凱斯卡德公司2024年的收入下降表明,在住宅市場低迷時期,將木材價格上漲轉嫁給消費者面臨許多挑戰。儘管製造商通常會收取附加費,但價格波動仍在不斷擠壓利潤空間,並使競標定價更加複雜。

細分市場分析

金屬製品將佔2025年銷售額的50.05%,憑藉其久經考驗的強度和生命週期價值,為圍欄市場提供支撐。鋼材將在國防和公共產業計劃中主導,而鋁材因其耐腐蝕性,在住宅應用中的使用率不斷提高。木材在注重自然美的建築法規地區仍然很受歡迎,但歐盟收緊甲醛法規帶來了替代木材的風險。混凝土板雖然應用範圍有限,但在需要防爆的領域至關重要。

隨著設計師尋求低維護成本的替代方案並滿足無鉛法規的要求,複合材料和PVC系統正以8.25%的複合年成長率快速成長。採用消費後PVC回收材料和生物基穩定劑的製造商可望獲得綠色採購溢價。農光互補試點計畫表明,輕質複合複合材料可兼作太陽能板的支撐結構,從而拓展圍欄市場,使其成為多功能資產。

第二代複合材料兼具強度重量比和回收性,為供應商帶來長期優勢。歐盟日益嚴格的鉛含量限制和新的高度關注物質清單正在加速向鋅穩定聚氯乙烯(PVC)和再生高密度聚乙烯(HDPE)混合物的轉變。擁有擠出能力和工業廢棄物回收系統的供應商可以在價格上勝過原生樹脂生產商。永續性資訊揭露已成為許多公共採購的必要條件,進一步推動了這項轉變。

區域分析

到2025年,北美將佔全球銷售額的35.10%,這主要得益於聯邦政府對道路、電網和退伍軍人設施維修的補貼。北美電力可靠性委員會(NERC)的規則變更要求公用事業公司加強變電站的周邊防護,而「購買美國貨」條款也鼓勵企業在國內的輥壓成型和加工企業進行消費。不斷成長的住宅維修需求也支撐了該地區的近期前景。

亞太地區雖然目前規模較小,但預計到2031年將以7.05%的複合年成長率實現最快成長。印度已累計超過4億美元用於邊境圍欄建設,其中包括在高風險通道沿線安裝防攀爬鋼格柵。在中國,儘管房地產行業面臨不利因素,但基礎設施獎勵策略和城市更新計劃仍在支撐圍欄需求。日本和韓國正在推進智慧感測器的部署,而澳洲的礦業部門則繼續為偏遠營地採購臨時屏障。

歐洲市場以嚴格的生態設計法規和循環經濟目標為特徵。無鉛PVC的最後期限和歐盟2026年甲醛基準值正在推動材料替代,使創新者獲得競爭優勢。可再生能源的擴張,特別是陸域風電的更新,正在支撐公共產業需求。東歐受益於歐盟凝聚基金對交通走廊的津貼,這些走廊需要大距離的隔音和防盜圍欄。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 政府基礎設施支出推動了對邊境安全措施的需求

- 配備智慧感測器的圍欄系統越來越受歡迎

- 耐候性複合材料和PVC材料正變得越來越受歡迎。

- 成熟經濟體中DIY住宅維修文化的快速發展

- 關鍵資產(公共產業、資料中心)加強的強制性法規

- 農光互補和垂直農業設施的邊界安全需求

- 市場限制

- 鋼鐵、木材和PVC樹脂的價格波動

- 來自低成本非正規製造商的競爭

- 加強對木材防腐劑和PVC添加劑的環境監管

- 增加對電子監控系統的投入,以取代實體屏障

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 材料分析

- 地緣政治對圍籬市場的影響

第5章 市場規模與成長預測

- 材料

- 金屬

- 鋼

- 鋁

- 木頭

- 塑膠和複合材料

- 具體的

- 其他材料

- 金屬

- 最終用戶

- 住宅

- 農業

- 軍事/國防

- 政府

- 礦業

- 石油/化工產品

- 能源與電力

- 其他最終用戶

- 按安裝類型

- 專業承包商

- 其他 - 製造商、DIY/模組化套件

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美洲

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 其他歐洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 奈及利亞

- 其他中東和非洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 印尼

- 亞太其他地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- CertainTeed

- Bekaert

- Betafence

- Ameristar Perimeter Security

- Ply Gem

- Long Fence

- Gregory Industries

- A-1 Fence Products

- Specrail

- Jerith

- Trex Company

- Barrette Outdoor Living

- Master Halco

- ActiveYards

- Fortress Building Products

- Allied Tube & Conduit

- Eastern Wholesale Fence

- Merchants Metals

- ITOCHU Corporation(Sakura)

- Gentek Building Products

第7章 市場機會與未來展望

第8章附錄

- 總體經濟指標

- 主要生產、消費、進出口統計數據

Fencing market size in 2026 is estimated at USD 39.07 billion, growing from 2025 value of USD 36.77 billion with 2031 projections showing USD 52.89 billion, growing at 6.25% CAGR over 2026-2031.

This expansion reflects mandatory hardening of power grids, data centers and borders, the rapid commercialization of smart perimeter hardware, and steady government infrastructure outlays. Metal products continue to dominate large-scale projects because of durability and life-cycle economics, while composite and PVC alternatives are scaling quickly under climate-resilient design mandates. Residential demand remains robust, yet agriculture and renewable-energy installations are emerging as the fastest-moving opportunity set. Professional contractors capture most revenue as IoT-enabled systems raise the technical bar, although DIY kits are expanding in mature housing markets. Regionally, North America retains leadership because of federal spending packages, but Asia-Pacific is set to outpace all other regions on the back of multibillion-dollar border and industrial programs.

Global Fencing Market Trends and Insights

Government Infrastructure Spend Boosting Perimeter Safety Demand

National security priorities are translating into sizeable multiyear budgets devoted to border fortifications and critical-asset protection. India has earmarked INR 32,500 crore (USD 3.89 billion) for fencing and road construction along sensitive borders through 2034, specifying anti-cut and anti-climb steel designs. Updated North American Electric Reliability Corporation guidance requires crash-rated gates at high-impact grid control centers, prompting utilities to overhaul outdated perimeter lines. United States federal building standards now embed Crime Prevention Through Environmental Design principles that specify layered barriers and electronic access control. These mandates are fueling demand for high-specification installations and favoring suppliers with security clearances.

Rising Adoption Of Smart, Sensor-Enabled Fencing Systems

IoT integration is converting passive fences into active threat-detection networks. IEEE studies show multi-sensor smart fences cut false alarms by 60% relative to legacy beam detectors. The U.S. Department of Defense telecommunication standard, recently updated to incorporate secure IoT interfaces, is shaping commercial product roadmaps. Airports adhering to National Safe Skies Alliance best practices are now specifying perimeter solutions that merge video analytics, radar, and credential databases. Department of Homeland Security validation protocols have created uniform performance metrics that accelerate procurement cycles.

Volatile Steel, Timber & PVC Resin Prices

Metal and resin markets remain tight due to energy costs and electrification demand. The World Bank metals index rose 9% in April 2024 and indicates further upside for base metals in 2025. Century Aluminum's curtailed domestic output underscores cost sensitivity in aluminum supply. Boise Cascade's 2024 revenue dip illustrates timber price pass-through challenges during soft housing cycles. Manufacturers are issuing more frequent surcharges, but volatility still squeezes margins and complicates bid pricing.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory Critical-Asset Hardening Regulations

- Climate-Resilient Composite & PVC Materials Gaining Traction

- Competition From Low-cost Unorganised Manufacturers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metal products generated 50.05% of 2025 revenue, anchoring the fencing market through proven strength and lifecycle value. Steel commands defense and utility projects, while aluminum gains residential traction for corrosion resistance. Wood keeps a loyal following where planning codes favor natural aesthetics, though upcoming EU formaldehyde caps create substitution risk. Concrete panels stay niche but indispensable at blast-critical sites.

Composite and PVC systems are scaling at an 8.25% CAGR as specifiers seek low-maintenance alternatives and compliance with lead-free directives. Manufacturers pursuing post-consumer PVC recovery and bio-based stabilizers stand to secure green-procurement premiums. Agrivoltaic pilots highlight how lightweight composites double as solar-panel sub-structures, expanding the fencing market size for multifunctional assets.

Second-generation composites position vendors for long-run advantage by balancing strength-to-weight ratios and recyclability. Restrictive EU rules on lead and novel SVHC listings are accelerating the pivot to zinc-stabilized PVC and recycled HDPE blends. Suppliers with extrusion capacity and closed-loop post-industrial scrap streams can undercut virgin-resin incumbents. Sustainability disclosures are now prerequisites for many public tenders, reinforcing the shift.

The Fencing Market Report is Segmented by Material (Metal, Wood, Plastic & Composite, Concrete, Other Materials), by End-User (Residential, Agricultural, Military & Defense, Government, Mining, and More), by Installation Type (Professional Contractor, Others - Fabricators, DIY / Modular Kits), and by Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 35.10% of 2025 global sales, propelled by federal grants for road, grid, and veterans facility upgrades. Updated NERC rules obligate utilities to fortify substation perimeters, while Buy-America provisions steer spend toward domestic roll-formers and fabricators. An expanding residential remodeling base supports the region's near-term outlook.

Asia-Pacific, though smaller today, is set to post the fastest 7.05% CAGR through 2031. India has budgeted more than USD 400 million for border fencing, including anti-climb steel grating along high-risk corridors. China's infrastructure stimulus and urban renewal projects cushion fencing demand despite property-sector headwinds. Japan and South Korea champion smart-sensor adoption, while Australia's mining sector continues to procure temporary barriers for remote camps.

Europe's market is framed by stringent eco-design laws and circular-economy targets. Lead-free PVC deadlines and the 2026 EU formaldehyde threshold spur material substitution, opening a competitiveness gap for innovators. Renewables build-out, particularly onshore wind repowering, sustains utility demand. Eastern Europe benefits from EU cohesion fund grants channelled into transport corridors that require long miles of acoustic and security fencing.

- CertainTeed

- Bekaert

- Betafence

- Ameristar Perimeter Security

- Ply Gem

- Long Fence

- Gregory Industries

- A-1 Fence Products

- Specrail

- Jerith

- Trex Company

- Barrette Outdoor Living

- Master Halco

- ActiveYards

- Fortress Building Products

- Allied Tube & Conduit

- Eastern Wholesale Fence

- Merchants Metals

- ITOCHU Corporation (Sakura)

- Gentek Building Products

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government infrastructure spend boosting perimeter safety demand

- 4.2.2 Rising adoption of smart, sensor-enabled fencing systems

- 4.2.3 Climate-resilient composite & PVC materials gaining traction

- 4.2.4 Surging DIY home-improvement culture in mature economies

- 4.2.5 Mandatory critical-asset hardening (utilities, data-centres) regulations

- 4.2.6 Demand for perimeter security in agrivoltaics & vertical farming sites

- 4.3 Market Restraints

- 4.3.1 Volatile steel, timber & PVC resin prices

- 4.3.2 Competition from low-cost unorganised manufacturers

- 4.3.3 Stricter environmental rules on wood preservatives & PVC additives

- 4.3.4 Rising substitute spend on electronic surveillance in lieu of physical barriers

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Materials Analysis

- 4.9 Impact of Geopolitics On Fencing Market

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Material

- 5.1.1 Metal

- 5.1.1.1 Steel

- 5.1.1.2 Aluminium

- 5.1.2 Wood

- 5.1.3 Plastic & Composite

- 5.1.4 Concrete

- 5.1.5 Other Materials

- 5.1.1 Metal

- 5.2 By End-User

- 5.2.1 Residential

- 5.2.2 Agricultural

- 5.2.3 Military & Defense

- 5.2.4 Government

- 5.2.5 Mining

- 5.2.6 Petroleum & Chemicals

- 5.2.7 Energy & Power

- 5.2.8 Other End-Users

- 5.3 By Installation Type

- 5.3.1 Professional Contractor

- 5.3.2 Others - Fabricators, DIY / Modular Kits

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Chile

- 5.4.2.4 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Netherlands

- 5.4.3.7 Rest of Europe

- 5.4.4 Middle East and Africa

- 5.4.4.1 Saudi Arabia

- 5.4.4.2 United Arab Emirates

- 5.4.4.3 South Africa

- 5.4.4.4 Nigeria

- 5.4.4.5 Rest of Middle East and Africa

- 5.4.5 Asia-Pacific

- 5.4.5.1 China

- 5.4.5.2 India

- 5.4.5.3 Japan

- 5.4.5.4 South Korea

- 5.4.5.5 Australia

- 5.4.5.6 Indonesia

- 5.4.5.7 Rest of Asia-Pacific

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, Recent Developments)

- 6.4.1 CertainTeed

- 6.4.2 Bekaert

- 6.4.3 Betafence

- 6.4.4 Ameristar Perimeter Security

- 6.4.5 Ply Gem

- 6.4.6 Long Fence

- 6.4.7 Gregory Industries

- 6.4.8 A-1 Fence Products

- 6.4.9 Specrail

- 6.4.10 Jerith

- 6.4.11 Trex Company

- 6.4.12 Barrette Outdoor Living

- 6.4.13 Master Halco

- 6.4.14 ActiveYards

- 6.4.15 Fortress Building Products

- 6.4.16 Allied Tube & Conduit

- 6.4.17 Eastern Wholesale Fence

- 6.4.18 Merchants Metals

- 6.4.19 ITOCHU Corporation (Sakura)

- 6.4.20 Gentek Building Products

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

8 Appendix

- 8.1 Macroeconomic Indicators

- 8.2 Key Production, Consumption, Export & Import Stats

圍籬市場:2026-2032年全球市場預測(依產品類型、材質、功能、高度、安裝方式、銷售管道及應用分類)

圍籬市場:2026-2032年全球市場預測(依產品類型、材質、功能、高度、安裝方式、銷售管道及應用分類) 2026年全球圍籬市場報告2026年全球鋁製金屬圍籬市場報告動物籠具市場:2026-2032年全球市場預測(依動物種類、材料、籠具類型、最終用戶及通路分類)水產養殖網箱市場:依系統類型、品種、網箱類型、箱網材質、養殖規模及最終用戶分類-2026-2032年全球市場預測2026年全球深水養殖網箱市場報告2026年全球漁網和水產養殖網箱市場報告防塵圍籬市場:依產品類型、材料、應用、最終用戶、通路分類,全球預測(2026-2032)全球畜牧用永久和臨時電圍欄市場(按類型、產品、動物、電壓和分銷管道分類)預測(2026-2032年)不鏽鋼楔形網市場依材料等級、網孔尺寸、應用、終端用戶產業及通路分類,全球預測(2026-2032年)

2026年全球圍籬市場報告2026年全球鋁製金屬圍籬市場報告動物籠具市場:2026-2032年全球市場預測(依動物種類、材料、籠具類型、最終用戶及通路分類)水產養殖網箱市場:依系統類型、品種、網箱類型、箱網材質、養殖規模及最終用戶分類-2026-2032年全球市場預測2026年全球深水養殖網箱市場報告2026年全球漁網和水產養殖網箱市場報告防塵圍籬市場:依產品類型、材料、應用、最終用戶、通路分類,全球預測(2026-2032)全球畜牧用永久和臨時電圍欄市場(按類型、產品、動物、電壓和分銷管道分類)預測(2026-2032年)不鏽鋼楔形網市場依材料等級、網孔尺寸、應用、終端用戶產業及通路分類,全球預測(2026-2032年)