|

市場調查報告書

商品編碼

1910922

照護現場資料管理軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Point-of-Care Data Management Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

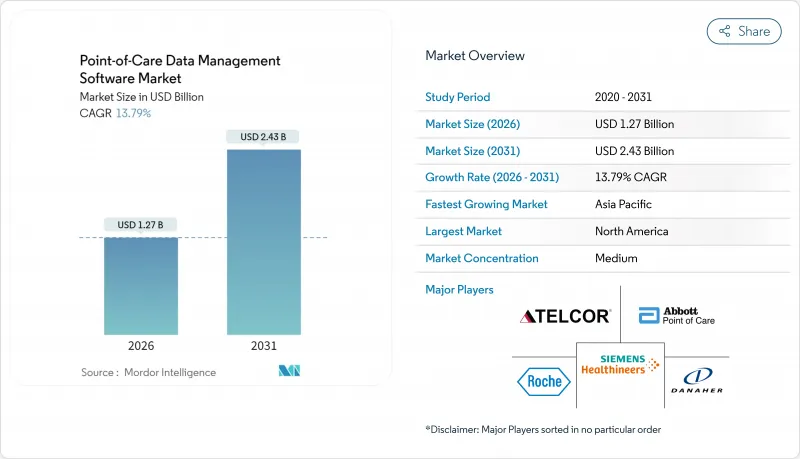

預計到 2025 年,照護現場資料管理軟體市場規模將達到 11.2 億美元,到 2026 年將達到 12.7 億美元,到 2031 年將達到 24.3 億美元,2026 年至 2031 年的複合年成長率為 13.79%。

這一快速成長是由醫療保健系統向即時診斷的轉型、政府對靈活連接投入的增加以及對按績效付費系統的日益青睞所驅動的。雲端遷移、人工智慧驅動的分析以及連接數百種設備的中間件如今已成為關鍵的採購標準。隨著醫院資料工作流程的標準化和居家照護項目的擴展,能夠整合軟體、服務和網路安全措施的供應商有望獲得市場佔有率。大型現有企業與利基創新者之間的整合並存,形成了一個集中度適中的市場環境,預計將支持穩定的交易活動。

全球照護現場資料管理軟體市場趨勢與洞察

靈活連接和介面解決方案的創新

在CMS互通性和病患存取規則的推動下,醫療系統需要能夠透過標準化的FHIR R4 API連接200多種不同類型的照護現場設備(POCT)的互通中間件。供應商正將連接性定位為核心基礎設施,而非附加功能,以避免數據孤島並加快臨床決策。 5G和邊緣運算節點的出現縮短了雲端原生部署的延遲,並使多站點營運商能夠協調不同分散式站點的工作流程。 FDA的數位健康軟體預認證計畫透過將連接性納入監管審查並獎勵持續的性能監控,進一步推進了連接性的發展。因此,採購方在授予合約時優先考慮中間件的深度和麵向未來的介面藍圖。

擴大醫療基礎設施預算

預計各國政府將在2024年投入2,000億美元用於醫療基礎設施計劃,其中相當一部分資金將用於數位平台,包括床邊資料管理軟體。印度的國家數位健康使命和中國的「健康中國2030」等項目正在投資IT現代化,這為符合各國數據本地化法規的供應商打開了市場大門。公私合營( PPP)專案擴大將軟體條款納入建設競標,將可選技術轉變為必備設備。新建醫院和診斷中心正在指定使用分析套件,為基於價值的醫療保健儀錶板提供數據,從而使軟體採購與設施建設進度保持一致。這波支出激增擴大了中等收入國家的潛在基本客群,並透過長期維護合約提高了供應商的收入可見度。

高昂的實施和整合成本

全面實施該系統,每個醫療機構的成本在 50 萬至 200 萬美元之間,這對於小規模農村醫院而言構成了一大障礙,因為這些醫院 40% 的 IT 職位空缺。異質的舊有系統增加了介面編碼和工作流程重新設計的負擔,通常會使實施週期超出預算。年度維護成本、員工培訓成本和升級合約費用進一步增加了總擁有成本。收費量較低的醫療機構,由於投資報酬率仍然較低,往往傾向於選擇津貼資金籌措或分級付費的 SaaS 方案。提供價格合理的模組化雲端託管服務的供應商可以刺激潛在需求,並克服這種複合年成長率的限制。

細分市場分析

到2025年,本地部署仍將佔總收入的51.62%,這反映了以往直接在內部伺服器上管理資料的趨勢。然而,雲端解決方案正以15.88%的複合年成長率快速成長,這主要得益於其強大的災害復原能力、自動修補程式和可擴充儲存等優勢。混合部署方案為遷移提供了橋樑。許多系統將對延遲敏感的模組保留在本地,同時將分析處理遷移到符合HIPAA標準的雲端。多地點連鎖企業優先考慮以雲端為中心的儀表板,這些儀表板可以跨園區同步效能指標,從而減少冗餘基礎設施。美國食品藥物管理局(FDA)近期發布的指南將經過檢驗的雲端配置與本地安裝等同起來,這進一步緩解了資訊長(CIO)的擔憂,並鼓勵企業採用SaaS模式。因硬體更新延遲而節省的資金通常用於加強網路安全,從而加快遷移進程。

雲端供應商正大力宣傳 FedRAMP 和 HITRUST 認證,以贏得聯邦政府和學術機構的契約,這削弱了傳統本地部署服務商的領先優勢。勒索軟體威脅的日益加劇也促使人們需要異地備份,而這如今已成為許多雲端服務合約的標配。同時,處理基因組數據的研究機構仍依賴本地叢集來最大化計算吞吐量。然而,即便如此,容器化工作負載也能在高峰需求期間為雲端提供突發容量,這預示著未來混合架構將模糊本地與本地的界限。隨著時間的推移,基於服務的定價結構將使服務商的關注點從永久許可轉向以客戶維繫為中心的藍圖,並建立豐富的 AI 模組和 API 市場,從而促進生態系統參與的盈利。

到2025年,醫院和重症監護室仍將維持46.15%的市場佔有率,這主要由急診室吞吐量目標和快速提供檢測結果的要求所驅動。然而,居家醫療計畫將實現14.71%的複合年成長率,這主要得益於聯邦醫療保險(Medicare)擴大家庭醫院服務範圍以及人口老化的趨勢。攜帶式分析儀和遠端醫療設備的廣泛應用,推動了對輕量級、基於瀏覽器的控制面板的需求,以便看護者可以從患者家中存取這些控制面板。診斷中心正在整合自動化檢驗規則以應對檢體處理量的激增,而診所則正在利用照護現場數據,在固定費用支付系統下縮短諮詢週期。

居家照護供應商面臨寬頻品質不穩定的問題,這促使他們對「儲存後轉送」架構產生興趣,該架構可在網路連線恢復時進行同步。醫院持續投資於企業級中間件,用於檢測品管偏差並整合試劑庫存數據,以提高供應鏈效率。門診診所正在採用共用服務模式,在維持對本地設備池自主管理的同時,授權使用集中式分析工具。 「其他」類別擴展至包括長期照護機構和職業健康機構,推動了針對院外工作流程量身定做的模組化使用者介面皮膚的需求和商機。

區域分析

北美地區預計到2025年將保持38.21%的市場佔有率,這得益於美國國立衛生研究院(NIH)的津貼、生物醫學高級研究與發展局(BARDA)的DRIVe計畫以及成熟的電子健康記錄(EHR)應用。美國醫院正在採用分析工具來達到聯邦醫療保險優勢計劃(Medicare Advantage)的品質指標,而加拿大各省的醫療系統則透過中介互通性來投資改善農村地區的醫療服務。創業投資的湧入和可預測的FDA核准流程使該地區成為人工智慧密集型模組的試驗場,為供應商提供了早期回饋機制。

亞太地區預計將以16.52%的複合年成長率成為全球成長最快的地區。中國150億美元的醫療數位化預算正投入到渴望擁有雲端儀錶板的縣級醫院。印度的「阿尤斯曼·巴拉特數位使命」(Ayushman Bharat Digital Mission)強制要求互通性,引導採購方選擇符合標準的軟體。日本正利用「社會5.0」理念支持一項老年護理試點項目,該項目將家庭監測設備與集中式分析相結合。新加坡作為區域擴張中心,向東南亞輸出專業知識。不同的法規環境正在推動具備靈活資料主權切換能力和多語言介面的平台的價值。

歐洲正經歷著穩步推進的、由監管主導的數位轉型。德國的《數位健康法案》正在資助醫院IT系統的現代化改造,而英國的NHS數位轉型宣傳活動則致力於推動所有急診醫院採用通用的互通性標準。法國和西班牙正利用歐盟復甦基金對遠端醫療和檢查室IT系統進行現代化改造。嚴格的GDPR法規要求嵌入式同意管理和加密功能,雖然延長了引進週期,但也提高了可靠性。擁有預先檢驗的合規模板的供應商在競標中更具優勢。南美洲和中東/非洲的市佔率雖然落後於歐洲,但由於公私合營)和基礎建設從一開始就定義了數位化工具包,這些地區的成長率也達到了15%左右。

其他福利

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 靈活連接和介面解決方案的創新

- 擴大醫療基礎設施預算

- 政府資助即時檢測

- 支付方轉向以績效為基礎的薪酬體系

- 人工智慧驅動的抗生素合理使用分析模組

- 日益嚴格的網路安全合規要求

- 市場限制

- 高昂的實施和整合成本

- 資料隱私和網路安全威脅

- 碎片化的舊設備韌體環境

- 本地設施缺乏熟練的IT人員

- 宏觀經濟因素的影響

- 產業價值鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 透過部署模式

- 基於雲端的

- 本地部署

- 混合

- 最終用戶

- 醫院/加護病房

- 診斷中心

- 診所/門診

- 居家醫療

- 其他

- 透過使用

- 感染疾病預防設備

- 血糖監測

- 凝血監測

- 尿液檢查

- 心血管代謝監測

- 癌症標記

- 血液學

- 其他概念驗證用途

- 按組件

- 軟體平台

- 中介軟體

- 服務

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 其他歐洲

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞洲地區

- 中東

- 以色列

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 埃及

- 其他非洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Siemens Healthineers AG(Conworx)

- Abbott Point of Care Inc.(Alere Inc.)

- Danaher Corporation(HemoCue AB and Radiometer Medical ApS)

- F. Hoffmann-La Roche Ltd

- TELCOR Inc.

- Orchard Software Corporation

- Randox Laboratories Ltd

- Thermo Fisher Scientific Inc.

- EKF Diagnostics Holdings plc

- HORIBA Ltd

- Nova Biomedical Corporation

- Sysmex Corporation

- Werfen SA

- Alcor Scientific Inc.

- PTS Diagnostics LLC

- Masimo Corporation

- Becton, Dickinson and Company

- Beckman Coulter Inc.

- Medtronic plc

第7章 市場機會與未來展望

The point-of-care data management software market is expected to grow from USD 1.12 billion in 2025 to USD 1.27 billion in 2026 and is forecast to reach USD 2.43 billion by 2031 at 13.79% CAGR over 2026-2031.

This brisk expansion springs from health systems' pivot toward real-time diagnostics, wider government funding for flexible connectivity, and a rising preference for outcome-based reimbursement. Cloud migration, AI-driven analytics, and middleware that links hundreds of device types are now central buying criteria. Vendors able to bundle software, services, and cybersecurity safeguards stand to capture share as hospitals standardize data workflows and home-care programs scale. Consolidation among large incumbents coexists with niche innovators, creating a moderate-concentration landscape poised for steady deal activity.

Global Point-of-Care Data Management Software Market Trends and Insights

Innovation in Flexible Connectivity and Interface Solutions

Health systems are demanding interoperable middleware that links more than 200 distinct point-of-care devices through standardized FHIR R4 APIs, a capability spurred by CMS's Interoperability and Patient Access Rule. Vendors now treat connectivity as core infrastructure, not add-on code, to avoid data silos and accelerate clinical decision-making. The arrival of 5G and edge-computing nodes cuts latency for cloud-native deployments, letting multi-site operators harmonize workflows across dispersed facilities. FDA's Digital Health Software Precertification Program further elevates connectivity by embedding it in regulatory review, creating an incentive for continuous performance monitoring. As a result, buyers prioritize middleware depth and future-proof interface roadmaps when awarding contracts.

Expansion of Healthcare Infrastructure Budgets

Governments spent USD 200 billion on health-infrastructure projects in 2024, earmarking sizable funds for digital platforms that include point-of-care data management software. Programs like India's National Digital Health Mission and China's Healthy China 2030 channel budget toward IT modernization, opening doors for vendors able to meet country-specific data-localization rules. Private-public partnerships often bundle software clauses into construction tenders, effectively converting optional tech into mandatory kit. As new hospitals and diagnostic centers go live, they specify analytics suites that feed value-based care dashboards, ensuring software procurement aligns with bricks-and-mortar schedules. This spends surge enlarges the addressable base in mid-income economies and smooths revenue visibility for suppliers through long-term maintenance deals.

High Deployment and Integration Costs

Comprehensive rollouts cost USD 500,000-USD 2 million per facility, a hurdle that stalls adoption in smaller or rural hospitals where 40% of IT posts sit vacant. Legacy-system heterogeneity inflates interface coding and workflow redesign, often stretching timelines past budget cycles. Total cost of ownership widens when annual maintenance, staff training, and upgrade subscriptions enter the calculus. For facilities with thin patient volumes, payback models remain weak, nudging them toward grant funding or SaaS options with phased billing. Vendors able to package modular, cloud-hosted offerings at lower entry prices can unlock pent-up demand and counter this drag on CAGR.

Other drivers and restraints analyzed in the detailed report include:

- Government Funding Initiatives for POC Testing

- Data Privacy and Cybersecurity Threats

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

On-premises deployments still commanded 51.62% revenue in 2025, showing the historical sway of in-house servers for direct data custody. Yet cloud solutions are sprinting at a 15.88% CAGR, fuelled by robust disaster-recovery, auto-patching, and elastic storage benefits. A hybrid approach acts as a transition bridge: many systems keep latency-sensitive modules on-site while pushing analytics to HIPAA-compliant clouds. Multi-site chains prize cloud-centric dashboards that synchronize performance metrics across campuses, trimming duplicated infrastructure. FDA's recent guidance equating validated cloud configurations with local installations further eases CIO concerns, nudging purchase orders toward SaaS models. Savings from hardware refresh deferral often finance cybersecurity upgrades, accelerating the migration curve.

Cloud vendors tout FedRAMP and HITRUST credentials to win federal and academic accounts, denting the head-start enjoyed by legacy on-premises incumbents. Rising ransomware threats also make off-site backups imperative, a default feature in many cloud contracts. Conversely, research institutes handling genomic data still lean on local clusters to maximize compute throughput. Even here, containerized workloads permit burst capacity in the cloud during peak demand, showcasing a future where line-blurring hybrid architectures dominate. Over time, service-based pricing shifts vendor focus from perpetual licenses to retention-driven roadmaps rich in AI modules and API marketplaces that monetize ecosystem participation.

Hospitals and critical-care units retained the lion's 46.15% share in 2025, supported by emergency-department throughput targets and lab turnaround mandates. Nevertheless, home-health programs are clocking a 14.71% CAGR, buoyed by Medicare's Hospital-at-Home expansion and aging-population dynamics. Portable analyzers and telehealth kits feed a need for lightweight, browser-based dashboards that caregiver's access from patient residences. Diagnostic centers integrate auto-verification rules to handle ballooning specimen loads while clinics lean on point-of-care data to shorten visit cycles under capitated payment plans.

Home-care operators grapple with variable broadband quality, propelling interest in store-and-forward architecture that syncs when connectivity resumes. Hospitals continue to invest in enterprise-wide middleware that flags quality-control drifts and consolidates reagent inventory data, improving supply chain efficiency. Outpatient clinics adopt shared-service models, licensing centralized analytics but maintaining autonomy over local device pools. The growing "other" category spanning long-term care and occupational-health sites creates opportunities for modular UI skins tailored to non-hospital workflows, widening addressable revenue.

The Point-Of-Care Data Management Software Market Report is Segmented by Deployment Mode (Cloud-Based, On-Premise, and Hybrid), End User (Hospitals/Critical Care Units, Diagnostic Centers, Clinics/Outpatient, Home Healthcare, and More), Application (Infectious Disease Devices, Glucose Monitoring, and More), Component (Software Platform, and Services), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America maintained a 38.21% share in 2025, anchored by NIH grants, BARDA's DRIVe program, and mature EHR penetration. U.S. hospitals deploy analytics to satisfy Medicare Advantage quality metrics, whereas Canada's provincial systems fund rural-access upgrades that hinge on middleware interoperability. Venture capital flows and predictable FDA pathways make the region a test bed for AI-rich modules, giving suppliers early feedback loops.

Asia Pacific is set to compound at 16.52% CAGR, the fastest worldwide. China's USD 15 billion health-digitization budget funnels into county-level hospitals eager for cloud-hosted dashboards. India's Ayushman Bharat Digital Mission enforces interoperability, nudging buyers toward standards-compliant software. Japan leverages Society 5.0 to back aging-care pilots that marry home-monitoring kits with centralized analytics. Singapore acts as the regional deployment hub, exporting expertise across Southeast Asia. The mosaic of regulations rewards platforms sporting flexible data-sovereignty toggles and multilingual interfaces.

Europe exhibits steady, regulation-driven uptake. Germany's Digital Healthcare Act finances hospital IT overhauls, while the United Kingdom's NHS Digital campaign pushes all acute trusts onto a shared interoperability standard. France and Spain tap EU Recovery funds for telemedicine and lab IT modernization. Strict GDPR rules require baked-in consent management and encryption, extending deployment cycles but enhancing trust. Suppliers that pre-validate compliance templates gain bidding advantages. South America, the Middle East, and Africa trail in share but post mid-teens growth as public-private buildouts stipulates digital kits from the outset.

- Siemens Healthineers AG (Conworx)

- Abbott Point of Care Inc. (Alere Inc.)

- Danaher Corporation (HemoCue AB and Radiometer Medical ApS)

- F. Hoffmann-La Roche Ltd

- TELCOR Inc.

- Orchard Software Corporation

- Randox Laboratories Ltd

- Thermo Fisher Scientific Inc.

- EKF Diagnostics Holdings plc

- HORIBA Ltd

- Nova Biomedical Corporation

- Sysmex Corporation

- Werfen S.A.

- Alcor Scientific Inc.

- PTS Diagnostics LLC

- Masimo Corporation

- Becton, Dickinson and Company

- Beckman Coulter Inc.

- Medtronic plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Innovation in Flexible Connectivity and Interface Solutions

- 4.2.2 Expansion of Healthcare Infrastructure Budgets

- 4.2.3 Government Funding Initiatives for POC Testing

- 4.2.4 Payor Shift Toward Outcome-Based Reimbursement

- 4.2.5 AI-Driven Analytics Modules for Antimicrobial Stewardship

- 4.2.6 Growing Cybersecurity Compliance Requirements

- 4.3 Market Restraints

- 4.3.1 High Deployment and Integration Costs

- 4.3.2 Data Privacy and Cybersecurity Threats

- 4.3.3 Fragmented Legacy Device Firmware Ecosystem

- 4.3.4 Shortage of Skilled IT Staff in Rural Facilities

- 4.4 Impact of Macroeconomic Factors

- 4.5 Industry Value-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud-Based

- 5.1.2 On-Premise

- 5.1.3 Hybrid

- 5.2 By End User

- 5.2.1 Hospitals / Critical Care Units

- 5.2.2 Diagnostic Centers

- 5.2.3 Clinics / Outpatient

- 5.2.4 Home Healthcare

- 5.2.5 Other End Users

- 5.3 By Application

- 5.3.1 Infectious Disease Devices

- 5.3.2 Glucose Monitoring

- 5.3.3 Coagulation Monitoring

- 5.3.4 Urinalysis

- 5.3.5 Cardiometabolic Monitoring

- 5.3.6 Cancer Markers

- 5.3.7 Hematology

- 5.3.8 Other POC Applications

- 5.4 By Component

- 5.4.1 Software Platform

- 5.4.2 Middleware

- 5.4.3 Services

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia

- 5.5.4 Middle East

- 5.5.4.1 Israel

- 5.5.4.2 Saudi Arabia

- 5.5.4.3 United Arab Emirates

- 5.5.4.4 Turkey

- 5.5.4.5 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank / Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Siemens Healthineers AG (Conworx)

- 6.4.2 Abbott Point of Care Inc. (Alere Inc.)

- 6.4.3 Danaher Corporation (HemoCue AB and Radiometer Medical ApS)

- 6.4.4 F. Hoffmann-La Roche Ltd

- 6.4.5 TELCOR Inc.

- 6.4.6 Orchard Software Corporation

- 6.4.7 Randox Laboratories Ltd

- 6.4.8 Thermo Fisher Scientific Inc.

- 6.4.9 EKF Diagnostics Holdings plc

- 6.4.10 HORIBA Ltd

- 6.4.11 Nova Biomedical Corporation

- 6.4.12 Sysmex Corporation

- 6.4.13 Werfen S.A.

- 6.4.14 Alcor Scientific Inc.

- 6.4.15 PTS Diagnostics LLC

- 6.4.16 Masimo Corporation

- 6.4.17 Becton, Dickinson and Company

- 6.4.18 Beckman Coulter Inc.

- 6.4.19 Medtronic plc

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

資料融合市場:2026年至2032年全球市場預測(依組件、業務功能、通路、部署類型、組織規模及最終用戶產業分類)資料遷移市場:按元件、資料類型、部署模式、產業和組織規模分類 - 全球預測(2026-2032 年)

資料融合市場:2026年至2032年全球市場預測(依組件、業務功能、通路、部署類型、組織規模及最終用戶產業分類)資料遷移市場:按元件、資料類型、部署模式、產業和組織規模分類 - 全球預測(2026-2032 年) 2035年床邊資料管理軟體市場分析及預測:按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和功能分類資料遷移市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、元件、應用、部署類型、最終使用者、流程和解決方案分類

2035年床邊資料管理軟體市場分析及預測:按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和功能分類資料遷移市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、元件、應用、部署類型、最終使用者、流程和解決方案分類 全球資料融合市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球資料融合市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 結構化資料管理軟體市場 - 全球產業規模、佔有率、趨勢、機會、預測:按部署方式、企業規模、最終用戶、地區和競爭對手分類,2021-2031 年資料管理廣告軟體市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、資料來源、最終用戶、地區和競爭對手分類,2021-2031年資料遷移市場 - 全球產業規模、佔有率、趨勢、機會及預測(按組件、部署模式、組織規模、資料類型、業務功能、最終用戶產業、地區和競爭格局分類),2021-2031年

結構化資料管理軟體市場 - 全球產業規模、佔有率、趨勢、機會、預測:按部署方式、企業規模、最終用戶、地區和競爭對手分類,2021-2031 年資料管理廣告軟體市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、資料來源、最終用戶、地區和競爭對手分類,2021-2031年資料遷移市場 - 全球產業規模、佔有率、趨勢、機會及預測(按組件、部署模式、組織規模、資料類型、業務功能、最終用戶產業、地區和競爭格局分類),2021-2031年 資料融合市場規模、佔有率和成長分析(按資料來源類型、技術、部署類型、產業應用和地區分類)-2026-2033年產業預測

資料融合市場規模、佔有率和成長分析(按資料來源類型、技術、部署類型、產業應用和地區分類)-2026-2033年產業預測 2025年即時診斷資料管理軟體全球市場報告

2025年即時診斷資料管理軟體全球市場報告