|

市場調查報告書

商品編碼

1910916

歐洲智慧停車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)Europe Smart Parking - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

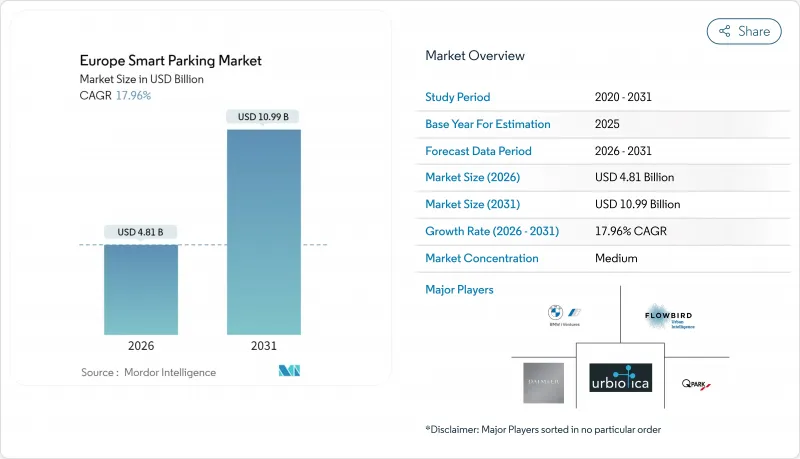

歐洲智慧停車市場預計將從 2025 年的 40.8 億美元成長到 2026 年的 48.1 億美元,預計到 2031 年將達到 109.9 億美元,2026 年至 2031 年的複合年成長率為 17.96%。

即時停車數據強制要求、電動車 (EV) 的快速普及以及企業範圍 3 報告要求,正在加速全部區域對智慧停車系統的投資。市政當局的需求集中在能夠與現有智慧型運輸系統(ITS) 架構整合的擴充性雲端平台,而企業則尋求節省空間的解決方案,以完善永續性儀錶板。平台供應商之間的整合和競爭日益加劇,整合化的出行生態系統模糊了停車、充電和票務服務之間的界線。 GDPR 下的隱私納入設計義務增加了複雜性,但也促使供應商轉向更高價值的託管服務和分析解決方案。

歐洲智慧停車市場趨勢與洞察

電動車普及導致停車位短缺

電動車強制令正迫使城市對現有停車場進行大規模維修和再利用。 《建築能源性能指令》要求到2025年每20個停車位配備一個充電樁,到2027年每10個停車位配備一個充電樁,這促使市政當局實施能夠在充電和常規使用之間動態切換的系統。像APCOA這樣的營運商,透過與丹麥Clever公司的合作,正在將充電硬體整合到現有設施中,並在其站點中添加即時佔用率分析功能。動態分配減少了排隊現象,定價機制平衡了收入和電動車獎勵。隨著充電基礎設施的擴展,協調電網容量限制和停車尖峰時段需求的演算法面臨越來越大的壓力。德國和整個斯堪的納維亞半島的城市正在將這些以分析為驅動的計劃定位為更廣泛的智慧交通系統部署的基礎用例。

行動支付和停車應用程式的興起

在荷蘭的主要城市,數位支付普及率已超過75%。可互通的行動錢包和車載應用程式降低了執法成本,提高了需求預測的準確性,並為擁塞自適應定價鋪平了道路。 BMW的作業系統現已在12個歐洲國家支援停車支付,為用戶提供全新的一鍵式車載支付體驗。儘管面臨資金籌措不確定性的擔憂,英國國家停車平台每月仍記錄了覆蓋10個城市的超過50萬筆交易。該平台的數據被用於機器學習模型,以預測周轉率,使營運商能夠預先定價並減少收入流失。 GDPR強制執行的隱私保護措施正迫使供應商採用令牌化和邊緣處理技術,從而推動了對外包合規專業知識的需求。

感測器和土木工程的初始成本

嵌入式感測器成本高昂,每個感測器在挖掘和鋪設路面之前就要花費 250 到 500 美元,這給有限的市政預算帶來了沉重負擔。捷克共和國帕爾杜比採市安裝了 3421 個感測器,使年度停車收入從 2,300 萬捷克克朗增加到約 4,000 萬捷克克朗,但這筆巨額資本支出也構成了重大障礙。表面安裝式設備雖然可以縮短安裝時間,但需要更多維護。植入式感測器的使用壽命較長,但計劃中會對道路造成損壞 [PARKING.NET]。市政當局通常會將專案分多個財政年度實施,權衡耐用性和預算週期,這減緩了智慧停車在歐洲的推廣速度。

細分市場分析

到2025年,傳統業者將佔據41.02%的收入佔有率,這主要得益於其基於長期特許經營合約和大規模停車場資產組合的優勢。這項基礎支撐著歐洲智慧停車市場的規模,但到2031年,P2P平台將以19.79%的複合年成長率蠶食市場成長。 Easypark與Parkbee的合作,使比利時120個停車場無需增加任何實體資產即可實現基於應用程式的租賃服務。作為回應,營運商將其庫存資訊白牌連接到該平台,並實施動態收費系統以提高每個停車位的盈利。管理公司作為資產所有者和供應商之間的橋樑,提供維護服務和資料分析的服務等級協定(SLA),而這些服務正擴大被市政當局外包。

儘管成長放緩,營運商仍在利用其資產負債表能力為感測器維修和電動車充電樁安裝提供資金,以努力維持其在歐洲智慧停車市場的佔有率。諸如INDIGO收購APCOA比利時公司之類的收購計劃,將其本地基地轉型為跨國平台,從而能夠與汽車製造商直接就SDK整合進行談判。P2P新興企業透過預測定價模式釋放私人和未充分利用的企業停車位,從而實現差異化競爭,但在人口密集的城市地區,整合路邊停車會帶來政治風險,並且需要政府核准。

雲端平台憑藉其一對多的可擴展性,鞏固了軟體在歐洲智慧停車市場的地位,預計到2025年將佔總收入的44.92%。然而,隨著城市將GDPR合規、維護和AI模型調校等工作外包,服務領域的複合年成長率預計將達到20.36%,超過所有其他類別。 JustPark的「洞察-覆蓋-最佳化」套件將報告儀表板與定價演算法相結合,標誌著市場模式正從一次性許可轉向持續的託管服務。

由於市政當局採用混合模式,利用監視錄影機和群眾外包停車數據,從而推遲全面覆蓋感測器,硬體供應商正面臨利潤壓力。 CleverCity 的桅杆式雷達裝置可覆蓋多達 100 個停車位,降低每個停車位的資本支出,使其更容易被中型城市接受。隨著軟體向 SaaS 模式發展,預計到本十年末,歐洲智慧停車市場的服務量將與軟體收入趨於一致。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 電動車普及導致停車位短缺

- 行動支付和停車應用程式的興起

- 歐盟智慧城市資助的旅遊即服務(MaaS)試點項目

- 歐盟資料共用義務(修訂後的ITS指令)

- 企業範圍 3 脫碳目標

- 透過「15分鐘城市」計畫加速路邊改革

- 市場限制

- 初始成本(感測器和土木工程成本)

- 市政採購週期分散

- GDPR 下自動車牌辨識 (ANPR) 分析的局限性

- 減少收費停車位,優先保障電動車在路肩上的行駛。

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 產業生態系分析

- 案例研究—歐洲重點案例

- 投資分析

第5章 市場規模與成長預測

- 按類型

- 停車場營運商

- 停車場管理公司

- 基礎設施提供者(硬體和軟體)

- P2P(P2P)停車平台

- 聚合平台/市場

- 透過解決方案

- 硬體

- 軟體

- 服務

- 透過技術

- 地下安裝/超音波感測器

- 攝影機/電腦視覺和車牌自動辨識(ANPR)

- 物聯網連接平台

- 行動應用和數位支付

- 設有電動車充電設施的停車場

- 最終用戶

- 地方政府和政府機構

- 商業停車場和購物中心

- 交通樞紐(機場、鐵路)

- 企業園區及商務園區

- 住宅和混合用途開發

- 按國家/地區

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 北歐國家

- 其他歐洲地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢與發展

- 市佔率分析

- 公司簡介

- APCOA Parking Holdings GmbH

- EasyPark Group AB(Arrive Mobility)

- Indigo Group SA

- Q-Park NV

- Flowbird SASU(Parkeon SA)

- Parkopedia Ltd.

- Urbiotica SL

- Cleverciti Systems GmbH

- JustPark Parking Ltd.

- Parclick SL

- ParkBee BV

- RingGo Ltd.

- Telpark(Empark Aparcamientos y Servicios SA)

- Parklio doo

- ParkHub Inc.

- FlashParking, Inc.

- ParkAir Systems AB

- Daimler Mobility

- Parklio doo

- Park+Mobility BV

- Bosch Service Solutions SE(Parking-as-a-Service)

- BMW i Ventures(ParkNow heritage assets)

第7章 市場機會與未來展望

The Europe smart parking market is expected to grow from USD 4.08 billion in 2025 to USD 4.81 billion in 2026 and is forecast to reach USD 10.99 billion by 2031 at 17.96% CAGR over 2026-2031.

Mandates on real-time parking data, rapid EV adoption, and corporate Scope 3 reporting requirements combine to accelerate investment in intelligent parking systems across the region. Municipal demand concentrates on scalable cloud platforms that dovetail with existing ITS architecture, while corporates look for space-saving solutions that feed sustainability dashboards. Consolidation among platform vendors is tightening competitive intensity, and integrated mobility ecosystems are starting to blur the lines between parking, charging, and ticketing services. Privacy-by-design obligations under GDPR add complexity, but they also push suppliers toward higher-value managed services and analytics.

Europe Smart Parking Market Trends and Insights

EV-Driven Parking Space Stress

Electric vehicle mandates force cities to retrofit or repurpose large sections of parking stock. The Energy Performance of Buildings Directive requires one charger per 20 spaces by 2025 and one per 10 by 2027, pushing municipalities to adopt systems that dynamically switch bays between charging and conventional use. Operators such as APCOA, through its partnership with Clever in Denmark, are embedding charging hardware into existing facilities and layering the sites with real-time occupancy analytics. Dynamic allocation eases queuing, while tariff engines balance revenue with EV incentives. As charging infrastructure spreads, pressure grows on algorithms to reconcile grid capacity limits with peak-hour parking demand. German and Nordic cities treat these analytics-centric projects as cornerstone use cases for broader ITS deployments.

Rise of Mobile Payments and Parking Apps

Digital payment penetration has crossed 75% in major Dutch municipalities. Interoperable mobile wallets and in-vehicle apps slash enforcement costs, sharpen demand forecasts, and open the door to congestion-responsive pricing. BMW's operating system now settles parking fees in 12 European countries, resetting user expectations for one-click, car-native transactions. The United Kingdom's National Parking Platform records more than 500,000 monthly transactions across 10 councils even as funding uncertainties loom. Platform data feeds machine-learning models that predict turnover, letting operators pre-price inventory and reduce revenue leakage. Privacy safeguards mandated by GDPR have pushed vendors to implement tokenization and edge processing, increasing demand for outsourced compliance expertise.

Up-Front Sensor and Civil-Works Costs

Embedded sensors range from USD 250 to USD 500 per unit before trenching and resurfacing, placing a heavy load on tight municipal budgets. Pardubice in the Czech Republic laid 3,421 sensors, boosting annual parking revenue from CZK 23 million to almost CZK 40 million yet demonstrating the steep capex hurdle. Surface-mounted devices cut installation time but demand more maintenance; flush-mounted options last longer but disrupt streets during deployment [PARKING.NET]. Cities weigh durability against budget cycles, often phasing projects over several fiscal years, slowing the Europe smart parking market rollout.

Other drivers and restraints analyzed in the detailed report include:

- EU Smart-City Funding for MaaS Pilots

- Corporate Scope-3 Decarbonization Targets

- Fragmented Municipal Procurement Cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Traditional operators controlled 41.02% of 2025 revenue, a lead built on long-term concessions and large garage portfolios. This base underpinned the Europe smart parking market size for the segment, though peer-to-peer platforms are eating into growth with a 19.79% CAGR through 2031. EasyPark's link-up with ParkBee opened 120 Belgian garages to app-based rentals without adding physical assets. Operators counter by white-labeling their inventory to platforms and layering dynamic tariffs that raise yield per bay. Management companies sit between asset owners and tech vendors, bundling maintenance and data-analytics SLAs that municipalities increasingly outsource.

Despite slower growth, operators leverage balance-sheet capacity to fund sensor retrofits and EV charger installations, sustaining their hold over the Europe smart parking market share. Acquisition pipelines, exemplified by INDIGO's purchase of APCOA Belgium, convert regional strongholds into multicountry platforms able to negotiate SDK integrations directly with automotive OEMs. Peer-to-peer challengers differentiate through predictive pricing models that unlock driveways and underused corporate lots, but they rely on municipal approval for curbside blending, which can be politically fraught in dense city cores.

Cloud platforms accounted for 44.92% revenue in 2025 thanks to one-to-many scalability, cementing software's rank within the Europe smart parking market. However, services are forecast to outpace all other categories at a 20.36% CAGR as cities outsource GDPR compliance, maintenance, and AI model tuning. JustPark's Insights-Reach-Optimize suite blends reporting dashboards with tariff algorithms, demonstrating the pivot from one-off licenses toward recurring managed services.

Hardware providers confront margin pressure because municipalities can defer full-sensor coverage by adopting hybrid schemes that mix overhead cameras and crowd-sourced occupancy data. Cleverciti's mast-mounted radar units cover up to 100 spaces and cut per-space capex, easing sales into mid-tier cities. As software shifts to SaaS, the Europe smart parking market size for services is expected to converge with software revenue by the decade's end.

The Europe Smart Parking Market Report is Segmented by Type (Parking Operators, Parking Management Companies, Infrastructure Providers, and More), Solution (Hardware, Software, and Services), Technology (In-Ground Sensors, Camera/ANPR, Iot Platforms, Mobile Apps, and EV-Charging Integration), End-User (Municipalities, Commercial Car-Parks, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- APCOA Parking Holdings GmbH

- EasyPark Group AB (Arrive Mobility)

- Indigo Group S.A.

- Q-Park NV

- Flowbird SASU (Parkeon SA)

- Parkopedia Ltd.

- Urbiotica SL

- Cleverciti Systems GmbH

- JustPark Parking Ltd.

- Parclick S.L.

- ParkBee B.V.

- RingGo Ltd.

- Telpark (Empark Aparcamientos y Servicios S.A.)

- Parklio d.o.o.

- ParkHub Inc.

- FlashParking, Inc.

- ParkAir Systems AB

- Daimler Mobility

- Parklio d.o.o.

- Park+ Mobility B.V.

- Bosch Service Solutions SE (Parking-as-a-Service)

- BMW i Ventures (ParkNow heritage assets)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EV-driven parking space stress

- 4.2.2 Rise of mobile payments and parking apps

- 4.2.3 EU Smart-City funding for MaaS pilots

- 4.2.4 EU data-sharing mandates (ITS-Directive rev.)

- 4.2.5 Corporate scope-3 decarbonisation targets

- 4.2.6 15-Minute-City zoning accelerating curb reforms

- 4.3 Market Restraints

- 4.3.1 Up-front sensor and civil-works costs

- 4.3.2 Fragmented municipal procurement cycles

- 4.3.3 GDPR-driven restrictions on ANPR analytics

- 4.3.4 EV-first kerb allocation shrinking paid bays

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Industry Ecosystem Analysis

- 4.8 Case Studies - Flagship European Deployments

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Parking Operators

- 5.1.2 Parking Management Companies

- 5.1.3 Infrastructure Providers (HW and SW)

- 5.1.4 Peer-to-Peer (P2P) Parking Platforms

- 5.1.5 Aggregators / Marketplaces

- 5.2 By Solution

- 5.2.1 Hardware

- 5.2.2 Software

- 5.2.3 Services

- 5.3 By Technology

- 5.3.1 In-ground / Ultrasonic Sensors

- 5.3.2 Camera / Computer-Vision and ANPR

- 5.3.3 IoT Connectivity Platforms

- 5.3.4 Mobile Apps and Digital Payments

- 5.3.5 EV-Charging Integrated Parking

- 5.4 By End-User

- 5.4.1 Municipalities and Government

- 5.4.2 Commercial Car-Parks and Malls

- 5.4.3 Transport Hubs (Airports, Rail)

- 5.4.4 Corporate Campuses and Business Parks

- 5.4.5 Residential and Mixed-Use Developments

- 5.5 By Country

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 France

- 5.5.4 Spain

- 5.5.5 Italy

- 5.5.6 Netherlands

- 5.5.7 Nordics

- 5.5.8 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Developments

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 APCOA Parking Holdings GmbH

- 6.4.2 EasyPark Group AB (Arrive Mobility)

- 6.4.3 Indigo Group S.A.

- 6.4.4 Q-Park NV

- 6.4.5 Flowbird SASU (Parkeon SA)

- 6.4.6 Parkopedia Ltd.

- 6.4.7 Urbiotica SL

- 6.4.8 Cleverciti Systems GmbH

- 6.4.9 JustPark Parking Ltd.

- 6.4.10 Parclick S.L.

- 6.4.11 ParkBee B.V.

- 6.4.12 RingGo Ltd.

- 6.4.13 Telpark (Empark Aparcamientos y Servicios S.A.)

- 6.4.14 Parklio d.o.o.

- 6.4.15 ParkHub Inc.

- 6.4.16 FlashParking, Inc.

- 6.4.17 ParkAir Systems AB

- 6.4.18 Daimler Mobility

- 6.4.19 Parklio d.o.o.

- 6.4.20 Park+ Mobility B.V.

- 6.4.21 Bosch Service Solutions SE (Parking-as-a-Service)

- 6.4.22 BMW i Ventures (ParkNow heritage assets)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Opportunity Hotspots (2025-2030)

- 7.3 Strategic Roadmap for Stakeholders

智慧停車市場:按組件、停車類型、部署方式、應用程式和最終用戶分類-2026-2032年全球市場預測

智慧停車市場:按組件、停車類型、部署方式、應用程式和最終用戶分類-2026-2032年全球市場預測 智慧停車系統市場預測至2034年—按組件、類型、技術、最終用戶和地區分類的全球分析停車即服務市場:按組件、部署類型和最終用戶分類 - 2026-2032 年全球市場預測

智慧停車系統市場預測至2034年—按組件、類型、技術、最終用戶和地區分類的全球分析停車即服務市場:按組件、部署類型和最終用戶分類 - 2026-2032 年全球市場預測 2026年全球數位雙胞胎智慧停車系統市場報告2026年全球智慧停車系統市場報告

2026年全球數位雙胞胎智慧停車系統市場報告2026年全球智慧停車系統市場報告 智慧停車市場規模、佔有率、趨勢和預測:按系統、技術、組件、解決方案、產業、停車地點和地區分類,2026-2034 年

智慧停車市場規模、佔有率、趨勢和預測:按系統、技術、組件、解決方案、產業、停車地點和地區分類,2026-2034 年 智慧停車系統市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、部署、最終用戶和解決方案分類

智慧停車系統市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、部署、最終用戶和解決方案分類 全球智慧停車系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球智慧停車系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 混合智慧停車平台市場 - 全球產業規模、佔有率、趨勢、機會、預測:停車、應用、解決方案、區域及競爭格局,2021-2031年智慧停車管理系統服務市場按組件、技術、應用和最終用戶分類 - 全球預測 2026-2032 年

混合智慧停車平台市場 - 全球產業規模、佔有率、趨勢、機會、預測:停車、應用、解決方案、區域及競爭格局,2021-2031年智慧停車管理系統服務市場按組件、技術、應用和最終用戶分類 - 全球預測 2026-2032 年