|

市場調查報告書

商品編碼

1910911

光纖布拉格光柵(FBG)感測器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Fiber Bragg Grating Sensor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

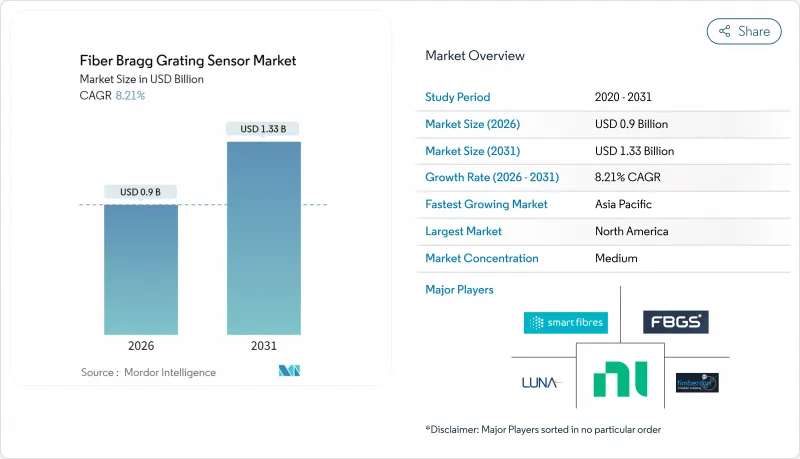

預計光纖布拉格光柵(FBG)感測器市場將從2025年的8.3億美元成長到2026年的9億美元,到2031年將達到13.3億美元,2026年至2031年的複合年成長率為8.21%。

結構健康監測、氫氣管道、智慧採礦和5G回程傳輸基礎設施的快速普及支撐著這一穩定成長的趨勢。競爭優勢主要體現在波長密集型感測器網路、多參數測量能力以及基於人工智慧(AI)的訊號處理。不斷成長的基礎設施投資、以安全為中心的法規以及傳統電感測器的運行局限性,共同推動了光學感測技術的發展。然而,溫度和應變之間的交叉敏感性以及較高的初始安裝成本,仍然限制了其在價格敏感型部署環境中的短期應用。

全球光纖布拉格光柵(FBG)感測器市場趨勢及洞察

對即時結構健康監測的需求日益成長

如今,老舊橋樑、隧道和高層建築都透過高密度光纖布拉格光柵(FBG)進行持續監測,在結構失效前發現疲勞裂縫和荷載重分佈模式。 2024年弗朗西斯·斯科特·基大橋的崩壞加速了美國聯邦政府強制要求在繁忙路段進行持續監測的進程。沿著整根梁體進行分散式感測可以產生完整的應變曲線,取代了分散的電感測器,後者往往無法捕捉到早期異常。歐洲類似的法規將公共資金支援的基礎設施升級與光學感測技術的部署掛鉤,這使得光纖布拉格光柵(FBG)感測器市場在土木工程領域擁有長期穩定的需求。

引入氫氣管道網路

歐洲氫能骨幹網路計畫要求洩漏偵測系統必須不受氫脆影響,並將光纖布拉格光柵(FBG)列為安全標準。雙模聲學和應變檢測技術使操作人員能夠同時檢測微小洩漏和機械變形,這是電氣系統在腐蝕性氫環境中無法實現的。德國H2-Netz為新建輸電線路制定的規範已成為可複製的模板,北美和亞太地區的計劃也開始效仿,從而擴大了光纖布拉格光柵(FBG)感測器在能源運輸基礎設施領域的市場佔有率。

溫度和應變之間的相互敏感性

將機械應變與熱效應分離仍然需要高成本的雙光柵結構和計算補償,導致航太和能源應用中的測量不確定度達到5-10%。尋求±1%精度的客戶被迫採用冗餘感測器配置,不僅推高了計劃預算,也限制了其在高溫度波動環境中的應用。預計在先進的補償設計具備價格競爭力之前,這項技術挑戰將暫時抑制光纖布拉格光柵(FBG)感測器市場的成長。

細分市場分析

到2025年,應變感測器將為光纖布拉格光柵(FBG)感測器市場貢獻3.1億美元(佔總收入的37.78%),證實了其在橋樑、飛機機翼和水泥建築物等眾多應用領域的廣泛應用。聲波感測器雖然絕對值較小,但隨著分散式聲學感測技術在周界安防和洩漏檢測領域的日益普及,其複合年成長率將達到9.12%。應變感測器仍將是大型基礎設施計劃的基礎,而聲學系統將作為一種互補技術實現高速成長。

多參數混合技術將應變光柵和溫度光柵整合在單一光纖上,從而減少了補償誤差和通道數量。油田服務供應商正擴大採用多感測器技術來降低完井的複雜性,這使得光纖布拉格光柵(FBG)感測器的市場拓展到電子壓力計無法勝任的井下環境中。

在電信級元件供應和成熟測量硬體的支援下,關鍵的C波段市場預計到2025年將達到約3.7億美元的市場規模。網路規模計劃正在耗盡可用的C波段頻道,推動著向L波段的遷移。 LL波段預計將以9.32%的複合年成長率實現最快成長,隨著大型企劃需要在單根光纖上實現數百個感測點, L波段光纖布拉格光柵(FBG)感測器市場規模預計將顯著擴大。

先進的詢問器現在可以同時掃描C波段和L波段,從而實現兼顧組件成本和通道密度的混合架構。研究聯盟正在測試用於特定生物醫學和水下應用的寬頻O波段陣列,但與主流波長相比,其商業化程度仍然有限。

區域分析

北美地區的主導主要來自重大橋樑事故後強制執行的結構監測要求。聯邦撥款支持老舊鋼拱橋的安裝,美國的潛艇船體完整性計劃則推動了軍方的需求。加拿大極端的氣溫波動使得光感測器成為易受冰凍負荷影響的偏遠輸電線路的理想選擇。墨西哥汽車工廠部署的光纖陣列減少了計劃外停機時間,為當地市場開闢了一個新的工業領域。

亞太地區的蓬勃發展在中國高速鐵路的建設中體現得淋漓盡致。中國在多個省份鋪設高速鐵路,每座高架橋上都安裝了數千個格柵,用於偵測旋轉滑移和接頭位移。日本嚴格的抗震標準推動了新幹線車站的即時監測,而韓國則將感測器整合到5G主幹線路中,以精確定位數公尺範圍內的光纖斷點。印度的智慧城市計畫正在資助一個試點項目,該項目利用路肩上的分散式聲波感測技術來建構交通監控網路,從而擴大了潛在需求。

在歐洲,人們正在製定標準化法規,以協調氫能、風能和鐵路計劃,例如在IEC 61757等框架下進行。德國的氫氣管道標準現已將聲學洩漏檢測作為預設選項,而英國皇家地產局則強制要求對固定式和浮體式風電資產進行光學監測。南歐正將重建資金投入到地震帶的高速鐵路建設中,並強制要求在隧道襯砌上使用光學陣列進行應變測量,這為該地區的光纖布拉格光柵(FBG)感測器市場帶來了利好。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 對即時結構健康監測的需求日益成長

- 氫氣管網部署現狀

- 加大智慧採礦作業的投資

- 擴展 5G 光纖回程傳輸基礎設施

- 在高壓直流(HVDC)電纜中的應用日益廣泛

- 國防部門重視基於狀態的飛機維修。

- 市場限制

- 對溫度和應變的交叉敏感性

- 與電子儀表相比,初始安裝成本較高

- 超快事件中的動態範圍限制

- 熟練光纖技術人員短缺

- 產業價值鏈分析

- 監管環境

- 技術展望

- 宏觀經濟因素的影響

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按類型

- 溫度感測器

- 應變感測器

- 壓力感測器

- 聲波感測器

- 其他類型

- 光柵波長範圍

- C波段(1530-1565奈米)

- L波段(1565-1625奈米)

- O波段(1260-1360奈米)

- 其他光柵波長範圍

- 按最終用戶行業分類

- 電訊

- 航太與國防

- 建築和基礎設施

- 能源與電力

- 石油和天然氣

- 礦業

- 其他終端用戶產業

- 透過使用

- 結構健康監測

- 溫度監測

- 振動和聲學監測

- 壓力監測

- 負載容量和重量監測

- 其他用途

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東地區

- 非洲

- 南非

- 埃及

- 其他非洲地區

- 中東

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- FBGS International NV

- Smart Fibres Ltd

- Micron Optics Inc-Luna Innovations

- Timbercon Inc

- National Instruments Corporation

- Hottinger Bruel and Kjaer HBM Inc

- Broptics Technology Inc

- ITF Technologies Inc

- Advanced Optics Solutions GmbH

- Technica Optical Components LLC

- Opsens Inc

- TeraXion Inc

- FISO Technologies Inc

- Optromix Inc

- Shenzhen Fibersail Technology Co Ltd

- Neoptix Inc

- Lightwave Logic Inc

- Smart Sensing Solutions GmbH

- Blue Road Research

- Cinogy Technologies GmbH

第7章 市場機會與未來展望

The Fiber Bragg Grating Sensor market is expected to grow from USD 0.83 billion in 2025 to USD 0.9 billion in 2026 and is forecast to reach USD 1.33 billion by 2031 at 8.21% CAGR over 2026-2031.

The surging adoption of structural health monitoring, hydrogen pipelines, smart mining, and 5G backhaul infrastructure underpins this steady trajectory. Competitive differentiation centers on wavelength-dense sensor networks, multi-parameter measurement capabilities, and artificial intelligence-based signal processing. Rising infrastructure investments, safety-centric regulations, and the operational limits of traditional electrical gauges jointly favor optical sensing. Nevertheless, cross-sensitivity between temperature and strain, as well as higher upfront installation costs, continue to moderate near-term adoption in price-sensitive deployments.

Global Fiber Bragg Grating Sensor Market Trends and Insights

Growing Demand for Real-Time Structural Health Monitoring

Aging bridges, tunnels, and high-rise buildings are now monitored continuously with dense arrays of fiber Bragg gratings that reveal fatigue cracks and patterns of load redistribution before structural failure. The 2024 Francis Scott Key Bridge collapse accelerated federal mandates for continuous monitoring on high-traffic corridors in the United States. Distributed sensing along entire girders creates a complete strain profile, replacing scattered electrical gauges that overlook early-stage anomalies. Similar regulations in Europe tie public-funded infrastructure upgrades to the adoption of optical sensing, positioning the Fiber Bragg Grating Sensor market for long-term demand in civil assets.

Adoption in Hydrogen Pipeline Networks

Europe's Hydrogen Backbone initiative requires leak detection systems immune to hydrogen embrittlement, elevating fiber Bragg gratings as a safety standard. Dual-mode acoustic and strain detection enables operators to spot micro-leaks and mechanical deformation simultaneously, a capability that electrical systems cannot deliver in the corrosive hydrogen environment. Germany's H2-Netz specifications for new transmission lines create a replicable template that North American and Asia-Pacific projects are beginning to follow, widening the Fiber Bragg Grating Sensor market footprint in energy transport infrastructure.

Cross-Sensitivity to Temperature and Strain

Separating mechanical strain from thermal effects still necessitates costly dual-grating configurations or computational compensation that introduce 5-10% measurement uncertainty in aerospace and energy applications. Customers seeking +-1% accuracy often resort to redundant sensor schemes, which raises project budgets and hinders adoption in environments with wide thermal swings. This technical hurdle temporarily tempers the expansion of the Fiber Bragg Grating Sensor market until advanced compensation designs become price-competitive.

Other drivers and restraints analyzed in the detailed report include:

- Rising Investments in Smart Mining Operations

- Expansion of 5G Fiber Backhaul Infrastructure

- High Upfront Installation Cost versus Electrical Gauges

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Strain sensors contributed USD 0.31 billion to the Fiber Bragg Grating Sensor market in 2025, retaining a 37.78% revenue share, which underscores their ubiquity across bridges, aircraft wings, and concrete structures. Acoustic variants, while smaller in absolute terms, show a 9.12% CAGR as distributed acoustic sensing gains traction in perimeter security and leak detection. Strain devices will continue to anchor flagship infrastructure projects, but acoustic systems provide a high-growth complement.

Multi-parameter hybrids that co-locate strain and temperature gratings on a single fiber are shrinking compensation errors and lowering channel counts. Oilfield service providers are increasingly favoring combined sensors to reduce wellbore completion complexity, thereby broadening the reach of the Fiber Bragg Grating Sensor market across downhole conditions where electronic gauges fail.

The dominant C-Band segment generated nearly USD 0.37 billion in 2025, driven by telecom-grade component availability and proven interrogation hardware. Network-scale projects exhaust available C-Band channels, driving migration to the L-Band, which is posting the fastest 9.32% CAGR. The Fiber Bragg Grating Sensor market size for L-Band devices is forecast to expand significantly as mega-projects demand hundreds of sensing points on a single fiber.

Advanced interrogators now sweep across C- and L-Bands simultaneously, enabling mixed architectures that balance component cost with channel density. Research consortia are testing broader O-Band arrays for niche biomedical and underwater applications, although commercialization remains modest compared to mainstream wavelengths.

The Fiber Bragg Grating Sensor Market Report is Segmented by Type (Temperature Sensor, Strain Sensor, and More), Grating Wavelength Range (C-Band, L-Band, and More), End-User Industry (Telecommunication, Aerospace and Defense, and More), Application (Structural Health Monitoring, Temperature Monitoring, Vibration and Acoustic Monitoring, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

\North American revenue leadership stems from mandated structural monitoring after catastrophic bridge failures. Federal grants subsidize installation on aging steel arches, and the U.S. Navy's submarine hull integrity program extends military demand. Canada's extreme temperature swings make optical sensors a logical choice for remote transmission lines prone to ice loading. Mexico adopts fiber arrays in automotive factories to reduce unplanned downtime, adding a nascent industrial layer to the regional Fiber Bragg Grating Sensor market.

Asia-Pacific's dynamism is evident in China's multi-province high-speed rail rollout, with each viaduct equipped with thousands of gratings to detect rotational slip and joint displacement. Japan's stringent seismic codes drive real-time monitoring on new Shinkansen stations, while Korea integrates sensors into 5G trunk lines to localize fiber cuts within meters. India's smart-city program funds pilot traffic-monitoring grids using distributed acoustic sensing on roadway shoulders, thereby expanding the addressable demand.

Europe benefits from standardized regulations that align hydrogen, wind, and rail projects under frameworks like IEC 61757. Germany's H2-Ready pipeline criteria specify acoustic leak detection by default, and the United Kingdom's Crown Estate requires optical monitoring on fixed and floating wind assets. Southern Europe channels recovery funds into high-speed rail that crosses seismic zones, mandating optical arrays for tunnel liner strain measurement, buttressing the regional Fiber Bragg Grating Sensor market outlook.

- FBGS International NV

- Smart Fibres Ltd

- Micron Optics Inc - Luna Innovations

- Timbercon Inc

- National Instruments Corporation

- Hottinger Bruel and Kjaer HBM Inc

- Broptics Technology Inc

- ITF Technologies Inc

- Advanced Optics Solutions GmbH

- Technica Optical Components LLC

- Opsens Inc

- TeraXion Inc

- FISO Technologies Inc

- Optromix Inc

- Shenzhen Fibersail Technology Co Ltd

- Neoptix Inc

- Lightwave Logic Inc

- Smart Sensing Solutions GmbH

- Blue Road Research

- Cinogy Technologies GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Real-Time Structural Health Monitoring

- 4.2.2 Adoption in Hydrogen Pipeline Networks

- 4.2.3 Rising Investments in Smart Mining Operations

- 4.2.4 Expansion of 5G Fiber Backhaul Infrastructure

- 4.2.5 Increasing Use in High-Voltage Direct Current (HVDC) Cables

- 4.2.6 Defense Focus on Condition-Based Aircraft Maintenance

- 4.3 Market Restraints

- 4.3.1 Cross-Sensitivity to Temperature and Strain

- 4.3.2 High Upfront Installation Cost versus Electrical Gauges

- 4.3.3 Limited Dynamic Range in Ultra-Fast Events

- 4.3.4 Scarcity of Skilled Fiber-Optic Technicians

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Temperature Sensor

- 5.1.2 Strain Sensor

- 5.1.3 Pressure Sensor

- 5.1.4 Acoustic Sensor

- 5.1.5 Other Types

- 5.2 By Grating Wavelength Range

- 5.2.1 C-Band (1530-1565 nm)

- 5.2.2 L-Band (1565-1625 nm)

- 5.2.3 O-Band (1260-1360 nm)

- 5.2.4 Other Grating Wavelength Ranges

- 5.3 By End-User Industry

- 5.3.1 Telecommunication

- 5.3.2 Aerospace and Defense

- 5.3.3 Construction and Infrastructure

- 5.3.4 Energy and Power

- 5.3.5 Oil and Gas

- 5.3.6 Mining

- 5.3.7 Other End-User Industries

- 5.4 By Application

- 5.4.1 Structural Health Monitoring

- 5.4.2 Temperature Monitoring

- 5.4.3 Vibration and Acoustic Monitoring

- 5.4.4 Pressure Monitoring

- 5.4.5 Load and Weight Monitoring

- 5.4.6 Other Applications

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Egypt

- 5.5.4.2.3 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 FBGS International NV

- 6.4.2 Smart Fibres Ltd

- 6.4.3 Micron Optics Inc - Luna Innovations

- 6.4.4 Timbercon Inc

- 6.4.5 National Instruments Corporation

- 6.4.6 Hottinger Bruel and Kjaer HBM Inc

- 6.4.7 Broptics Technology Inc

- 6.4.8 ITF Technologies Inc

- 6.4.9 Advanced Optics Solutions GmbH

- 6.4.10 Technica Optical Components LLC

- 6.4.11 Opsens Inc

- 6.4.12 TeraXion Inc

- 6.4.13 FISO Technologies Inc

- 6.4.14 Optromix Inc

- 6.4.15 Shenzhen Fibersail Technology Co Ltd

- 6.4.16 Neoptix Inc

- 6.4.17 Lightwave Logic Inc

- 6.4.18 Smart Sensing Solutions GmbH

- 6.4.19 Blue Road Research

- 6.4.20 Cinogy Technologies GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

光纖布拉格光柵市場:按類型、波長範圍、檢測範圍和最終用戶分類-2026-2032年全球市場預測

光纖布拉格光柵市場:按類型、波長範圍、檢測範圍和最終用戶分類-2026-2032年全球市場預測 光纖感測器市場分析及至2035年預測:類型、產品、技術、組件、應用、最終用戶、功能、安裝配置、模式

光纖感測器市場分析及至2035年預測:類型、產品、技術、組件、應用、最終用戶、功能、安裝配置、模式 2026年全球光纖陣列單元市場研究報告光子晶體光纖感測器市場分析及預測(至2035年):按類型、產品類型、技術、組件、應用、材料類型、最終用戶、功能、安裝類型和解決方案分類光纖布拉格光柵市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、材料類型、最終用戶、功能分類

2026年全球光纖陣列單元市場研究報告光子晶體光纖感測器市場分析及預測(至2035年):按類型、產品類型、技術、組件、應用、材料類型、最終用戶、功能、安裝類型和解決方案分類光纖布拉格光柵市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、材料類型、最終用戶、功能分類 光纖感測器市場 - 全球產業規模、佔有率、趨勢、機會、預測(按類型、最終用戶、組件、地區和競爭格局分類),2021-2031年光纖感測器市場按類型、感測器類型、測量方法、傳輸類型、應用和最終用戶分類,全球預測(2026-2032年)

光纖感測器市場 - 全球產業規模、佔有率、趨勢、機會、預測(按類型、最終用戶、組件、地區和競爭格局分類),2021-2031年光纖感測器市場按類型、感測器類型、測量方法、傳輸類型、應用和最終用戶分類,全球預測(2026-2032年) 光纖感測器市場規模及預測(2021-2031 年)、全球及地區佔有率、趨勢及成長機會分析報告涵蓋範圍:依感測類型、最終用戶、應用及地理分類

光纖感測器市場規模及預測(2021-2031 年)、全球及地區佔有率、趨勢及成長機會分析報告涵蓋範圍:依感測類型、最終用戶、應用及地理分類 光纖感測器市場:全球2025-2029

光纖感測器市場:全球2025-2029 石油和天然氣分佈式光纖感測器市場規模、佔有率、趨勢分析報告:按類型、地區和細分市場預測,2025-2030 年

石油和天然氣分佈式光纖感測器市場規模、佔有率、趨勢分析報告:按類型、地區和細分市場預測,2025-2030 年