|

市場調查報告書

商品編碼

1910885

四輪車和三輪車:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Quadricycle And Tricycle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

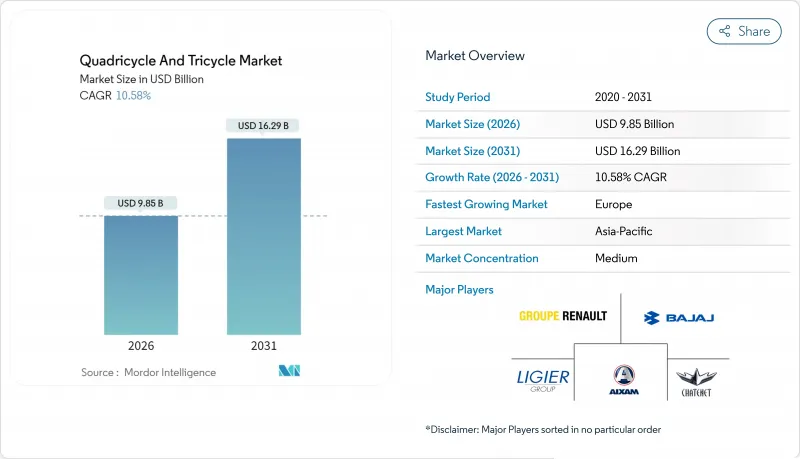

2025年,四輪車和三輪車市場價值為89.1億美元,預計從2026年的98.5億美元成長到2031年的162.9億美元,在預測期(2026-2031年)內,複合年成長率為10.58%。

推動這一成長的因素包括都市區配送密度的增加、降低電動車擁有成本的國家獎勵計劃,以及促進小型低排放交通工具發展的法規結構。儘管目前內燃機產品仍佔據出貨量主導地位,但電池成本的持續下降以及換電網路減少的停機時間,使得電動車型得以在生產線上佔據一席之地。歐洲更嚴格的排放法規以及印度計劃實施的BS7排放標準正在重塑成本格局,而埃及的嘟嘟車替代計劃則充分展現了官方批准四輪微型電動車如何創造新的市場需求。各大汽車製造商正將微型出行定位為新進業者的收入來源,並根據區域政策擴展產品線。這些因素共同推動了四輪和三輪汽車市場(包括貨運和客運領域)的快速成長。

全球四輪及三輪車市場趨勢及洞察

政府對電動三輪車/微型電動車的補貼和激勵措施

獎勵正逐步縮小電動車和汽油動力車之間的價格差距。印度的生產連結獎勵計畫計畫撥出大量資金,用於促進本地零件生產並降低單位成本。泰國的EV 3.5計畫為組裝電動三輪車的企業提供可觀的企業所得稅減免。同時,馬耳他為購買四輪車提供豐厚的財政津貼。中國將小型車輛購置稅豁免期限延長數年,凸顯了其在電動車獎勵的努力。這些措施,加上電池成本的下降,旨在促進電動車的銷售。這些可預測的獎勵鼓勵製造商擴大生產力計畫,以降低資本投資風險並提高工廠使用率。

對最後一公里電子商務配送的需求不斷成長

都市區配送成本約佔總配送成本的五分之四,因此車隊管理人員正在尋找能夠減少停車時間和擁擠費用的車輛。亞馬遜正在歐洲主要城市測試電動三輪貨車,而 Flipkart 則在印度城市中心部署換電三輪車。 Gogoro 和 Sun Mobility 提供的電池即服務 (BaaS) 模式能夠保持較高的車輛運轉率,使駕駛員能夠長時間工作而無需擔心里程問題。這些經濟優勢,加上低排放氣體區法規的日益嚴格,促使路線規劃轉向小型電動車。因此,小包裹配送量的成長直接轉化為底盤訂單,從而為零零件製造商形成良性循環。

缺乏快速充電/切換基礎設施

在大多數新興市場,充電站密度低於國際能源總署(IEA)建議的每10輛車配備一個充電樁的標準。在充電樁供應不穩定的地區,私人投資者持觀望態度;公共負責人也面臨預算限制,尤其是在農村地區。在電網不穩定的地區,營運商難以保證商用車輛的運轉率。儘管一些政府為充電樁提供補貼,但安裝速度仍落後於需求,導致電動車銷量放緩。由於能源供應不穩定,車隊管理者可能會繼續購買內燃機車型,這可能會延緩全面電氣化的進程。

細分市場分析

到2025年,三輪車將在四輪車和三輪車市場中佔據87.05%的絕對市場佔有率,這主要得益於印度、泰國和印尼成熟的製造地。三輪車市場預計將穩定成長,但成長速度低於四輪車市場。儘管四輪三輪車的絕對銷量較小,但預計到2031年,其複合年成長率將達到10.62%,這主要得益於歐洲和北非地區推行的有利於安全性和防風雨性能的封閉式座艙政策。 Bajaj Auto正在擴大Qute的生產規模,以滿足埃及的車輛更新換代需求;而Piaggio則在改進其基於Porter平台的微型電動車平台,以適應歐洲人口密集的都市區市場。因此,區域市場的發展模式受到多種複雜因素的影響,包括成本考量、氣候條件以及對車輛類型進行不同分類的法規。

三輪車平台不斷發展以保持競爭力,並融合了電池更換相容性和遠端資訊處理技術。四輪車設計則採用車頂太陽能輔助和輕質複合材料來減輕電池重量。這使得原始設備製造商 (OEM) 能夠建立針對不同使用者需求的開發平臺,而不是在所有地區推廣單一平台。競爭優勢依賴模組化架構,該架構允許零件共用,同時又能符合區域法規,從而實現柔軟性和適應性。整合高級駕駛員警告系統和基本互聯功能也有助於四輪車型在以「零事故」安全目標為導向的城市獲得監管部門的核准。隨著資金來源與零排放目標相契合,四輪車和三輪車市場正在走向多元化,兩種車型的發展趨勢是共存而非完全融合。

到2025年,商業營運將佔四輪和三輪車市場規模的73.10%,隨著小包裹遞送網路覆蓋範圍的擴大,這一佔有率預計還將繼續成長。在可預測的路線密度和低排放區免徵通行費的推動下,預計到2031年,商業營運將以10.7%的複合年成長率成長。在南亞地區,共享出行仍然主導著共乘和非正規計程車服務,但由於新地鐵線和快速公車系統的開通,其成長速度正在放緩。大規模電子商務平台提供的批量保障支援專用組裝的建設,使供應商能夠獲得多年合約。

車隊所有者正努力透過安裝封閉式駕駛室和空調系統來提高駕駛員留存率,這既能提升舒適度,又能保持較低的每公里成本。城市規劃者正在住宅附近設立微型物流樞紐,以縮短運輸距離,並凸顯緊湊型貨艙的適用性。軟體負責人目前正在整合專門針對三輪車的路線規劃功能,從而在尖峰時段減少燃油或電池消耗。在法規允許的情況下,搭乘用車輛正被改裝為旅遊接駁車和校園交通工具。在預測期內,四輪三輪車和三輪車市場將從普通客運轉型為盈利豐厚且資產周轉率合理的專業貨運生態系統。

區域分析

到2025年,亞太地區將佔四輪三輪車市場41.05%的佔有率,這主要得益於印度龐大的三輪車製造基地和中國在磷酸鐵鋰電池領域的規模優勢。印度的大規模生產關聯補貼(PLI)計畫正在重塑供應鏈,吸引電池製造商和零件供應商。同時,中國擴大了低功率車輛的購置稅豁免範圍,確保了微型電動車的成本競爭力。泰國的電動車計畫正將該國打造成為區域出口中心,並將其供應鏈與印尼和菲律賓無縫連接。這種策略合作有利於四輪三輪車市場,因為跨境經濟活動縮短了前置作業時間,最佳化了庫存週轉。

儘管目前出貨量小規模,但預計到2031年,歐洲的複合年成長率將達到10.65%。這一成長主要得益於地方政府的立法,例如堵塞收費和減少停車位。倫敦的超低排放區豁免了符合條件的輕型四輪車輛,而巴黎則透過減少路邊停車位來鼓勵居民選擇小型汽車。馬耳他針對輕型四輪車輛的獎勵措施,加上168/2013號法規下的標準化規定,簡化了型式認證流程。借助這一清晰的框架,製造商正計劃在歐盟範圍內推出新產品,將研發成本分攤到多個市場,並加強其在該地區輕型四輪和三輪車輛市場的地位。

北美正謹慎地加快步伐,充分利用各州層級的法規,例如加州的先進清潔車輛規則。在中東和非洲,埃及正式批准四輪計程車運營,推動了市場成長,並為印度供應商開闢了出口管道。南美洲面臨宏觀經濟問題和基礎設施不足等挑戰。然而,巴西聖保羅市零排放區的設立以及阿根廷微型電動車試點計畫的啟動,一旦信貸環境穩定,將帶來成長潛力。不同地區的監管時間表各不相同,預示著未來十年主導將發生動態變化,從而確保供應鏈的靈活性。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 政府對電動三輪車(E-3W)/微型電動車的補貼與獎勵措施

- 電子商務對最後一公里配送的需求不斷成長

- 排放氣體法規加速了從內燃機汽車向電動車的過渡。

- 都市區擁塞和停車限制有利於四輪Scooter

- 商用三輪車電池更換經營模式

- 埃及嘟嘟車換四輪車計劃

- 市場限制

- 缺乏快速充電/電池更換基礎設施

- 鋰離子電池初始成本高

- 消費者轉向性能更佳的電動二輪車

- 等待歐盟制定L6E/L7E車輛碰撞安全標準

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 產業間競爭

第5章 市場規模及成長預測(價值(美元)及銷售量(單位))

- 按車輛類型

- 四輪車

- 三輪車

- 透過使用

- 對於個人

- 商業的

- 依動力傳動系統類型

- 內燃機

- 電動車

- 透過設計/配置

- 搭乘用車

- 貨物

- 地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 土耳其

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Bajaj Auto Ltd.

- Piaggio & C. SpA

- Mahindra & Mahindra Ltd.(Last Mile Mobility)

- YC Electric Vehicle Private Limited

- Groupe Renault

- TVS Motor Company Ltd.

- Atul Auto Ltd.

- Kinetic Green Energy & Power Solutions Ltd.

- Terra Motors Corp.

- Ligier Group

- AIXAM MEGA SAS

- Speego Vehicles Co. Pvt. Ltd.

- Saera Electric Auto Pvt. Ltd.

- E-Tuk Factory BV

- Polaris Inc.(Ranger LSV)

- Toyota Motor Corp.(C+Pod)

- BYD Co. Ltd.(mini-EV platforms)

第7章 市場機會與未來展望

The Quadricycle and Tricycle Market was valued at USD 8.91 billion in 2025 and estimated to grow from USD 9.85 billion in 2026 to reach USD 16.29 billion by 2031, at a CAGR of 10.58% during the forecast period (2026-2031).

This growth is driven by increasing urban delivery density, national incentive programs that reduce the cost of electric-vehicle ownership, and regulatory frameworks that incentivize compact, low-emission transportation. Internal-combustion products currently dominate shipments, yet electric models are securing factory line time because battery costs continue to fall and swap networks reduce downtime. Tight emission limits in Europe and planned India BS7 rules reshape cost calculations, while Egypt's tuk-tuk replacement scheme illustrates how formal recognition of four-wheel micro-EVs unlocks fresh demand. Major automakers now treat micro-mobility as an entry-level profit pool, prompting portfolio extensions that mirror regional policy cues. Together, these forces propel the quadricycle and tricycle market onto a steep adoption curve across both freight and passenger niches.

Global Quadricycle And Tricycle Market Trends and Insights

Government Subsidies & Incentives For E-3W / Micro-EVs

Incentive packages are increasingly bridging the price gap between electric and gasoline vehicles. India's Production Linked Incentive scheme is allocating significant funding to boost local component production and reduce unit costs. Under Thailand's EV 3.5 policy, firms assembling electric tricycles are eligible for substantial corporate tax relief. Meanwhile, Malta is incentivizing quadricycle purchases with notable financial grants. In a move underscoring its commitment, China has extended purchase-tax exemptions for smaller vehicles for several more years. These initiatives, coinciding with falling battery costs, aim to boost electric car sales. With these predictable incentives, manufacturers are ramping up capacity planning, seeing it as a way to mitigate risks in capital spending and enhance plant utilization.

Rising E-Commerce Last-Mile Delivery Demand

Urban fulfillment costs account for almost three-fifths of shipping expenses, so fleet managers seek vehicles that reduce parking time and congestion fees. Amazon pilots electric cargo tricycles in several European capitals, while Flipkart equips Indian city hubs with swap-enabled three-wheelers. Battery-as-a-service models from Gogoro and Sun Mobility maintain high asset uptime, enabling operators to run longer shifts without range anxiety. Combined with stricter low-emission zones, these economics tilt route planning toward compact, electric vehicles. Volume growth in parcel shipments, therefore, transmits directly to chassis orders, sustaining a virtuous cycle for component makers.

Sparse Fast-Charging / Swap Infrastructure

Station density remains below the International Energy Agency guideline of one charger per ten vehicles across most emerging markets. Private investors hesitate where utilization rates are uncertain, and public planners face budget constraints, especially in rural areas. In regions with unreliable electricity grids, operators struggle to guarantee uptime for commercial fleets. Some governments subsidize chargers, but the rollout speed still lags behind demand, slowing electric vehicle sales. Without predictable access to energy, fleet managers may continue to purchase internal-combustion models, thereby delaying the tipping point for full electrification.

Other drivers and restraints analyzed in the detailed report include:

- Emission Regulations Accelerating ICE-To-EV Shift

- Urban Congestion & Parking Limits Favouring Quadricycles

- High Li-Ion Battery Upfront Cost

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tricycles accounted for a commanding 87.05% of the quadricycle and tricycle market share in 2025, sustained by entrenched manufacturing clusters in India, Thailand, and Indonesia. The quadricycle and tricycle market size for tricycles is projected to expand steadily, yet at a slower pace than four-wheel formats. Quadricycles, though smaller in absolute volume, are projected to register a 10.62% CAGR through 2031 as European and North African policies reward enclosed cabins for safety and weather protection. Bajaj Auto scales Qute production for Egypt's replacement program, while Piaggio refines its Porter-based micro-EV platform for dense European cores. Regional adoption patterns, therefore, reflect a complex mix of cost priorities, climate conditions, and rulebooks that classify vehicle classes differently.

Tricycle platforms continue to evolve, integrating battery-swap compatibility and telematics to maintain their relevance. Quadricycle engineering now incorporates roof-mounted solar assistance and lightweight composites to offset the mass of the battery. OEMs thus tailor R&D pipelines to distinct user requirements rather than forcing a single platform across geographies. Competitive positioning relies on modular architectures that share components while allowing for local variations in compliance, thereby enabling flexibility and adaptability. The integration of advanced driver alerts and basic connectivity features also helps four-wheel models gain regulatory approval in cities targeting Zero-Accident safety outcomes. As funding pools align with zero-emission targets, the quadricycle and tricycle markets diversify, with both formats coexisting rather than fully converging.

Commercial operations controlled 73.10% of the quadricycle and tricycle market size in 2025, a share expected to increase as parcel networks expand their coverage. Commercial operations are forecast to post a 10.7% CAGR through 2031, driven by predictable route density and fee exemptions in low-emission zones. Passenger formats still dominate ride-hailing and informal taxi services across South Asia; however, the introduction of new metro lines and bus rapid transit corridors is tempering incremental growth. Large e-commerce platforms offer volume guarantees that support dedicated assembly lines, allowing suppliers to secure multi-year contracts.

Fleet owners address driver retention by installing enclosed cabins and climate control systems, which enhance comfort while keeping the cost per kilometer low. Urban planners designate micro-logistics hubs near residential areas, shortening trip lengths and underscoring the suitability of compact cargo beds. Software providers are now integrating route planning specifically for three-wheel vehicles, which reduces fuel or battery consumption during peak congestion. Passenger units pivot toward tourism shuttles and campus transport where regulation permits. Over the forecast window, the quadricycle and tricycle market therefore shifts from general people movement toward specialized freight ecosystems whose earnings justify faster asset turnover.

The Quadricycle and Tricycle Market Report is Segmented by Vehicle Type (Quadricycle and Tricycle), Application Type (Personal and Commercial), Powertrain Type (Internal Combustion Engine and Electric), Design & Configuration (Passenger and Cargo), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia-Pacific commanded 41.05% of the quadricycle and tricycle market share in 2025, anchored by India's expansive three-wheeler manufacturing base and China's scale advantages in lithium-iron-phosphate chemistry. India's significant PLI initiative is reshaping supply chains, attracting both cell manufacturers and component vendors. Meanwhile, China has extended purchase-tax waivers for vehicles with lower power output, ensuring cost parity for micro-EVs. Thailand's EV program is positioning the nation as a regional export hub, seamlessly connecting its supply bases with those of Indonesia and the Philippines. This strategic alignment benefits the quadricycle and tricycle market, as cross-border economies reduce lead times and streamline inventory cycles.

Europe, while smaller in current shipments, is projected to log a 10.65% CAGR through 2031 as city halls codify congestion fees and parking reductions. This growth is driven by city halls implementing congestion fees and parking reductions. London's Ultra Low Emission Zone offers exemptions for compliant quadricycles, while Paris is reducing curbside stalls, encouraging residents to opt for compact vehicles. Malta's incentive for quadricycles, combined with the standardized rules of Regulation 168/2013, streamlines the homologation process. Capitalizing on this clarity, manufacturers are orchestrating pan-EU launches, distributing R&D costs across multiple markets, and bolstering the region's stake in the quadricycle and tricycle market.

North America is treading cautiously yet picking up pace, harnessing state-level mandates, such as California's Advanced Clean Fleets Rule. In the Middle East and Africa, growth is driven by Egypt's official recognition of quadricycle taxis, which paves the way for export routes for Indian suppliers. South America faces challenges from macroeconomic issues and inconsistent infrastructure. Yet, with Brazil's Sao Paulo introducing a zero-emission zone and Argentina piloting micro-EVs, there's potential for growth once credit conditions stabilize. The varying regulatory timelines across regions suggest a dynamic shift in leadership roles over the decade, ensuring nimble supply chains.

- Bajaj Auto Ltd.

- Piaggio & C. SpA

- Mahindra & Mahindra Ltd. (Last Mile Mobility)

- YC Electric Vehicle Private Limited

- Groupe Renault

- TVS Motor Company Ltd.

- Atul Auto Ltd.

- Kinetic Green Energy & Power Solutions Ltd.

- Terra Motors Corp.

- Ligier Group

- AIXAM MEGA SAS

- Speego Vehicles Co. Pvt. Ltd.

- Saera Electric Auto Pvt. Ltd.

- E-Tuk Factory BV

- Polaris Inc. (Ranger LSV)

- Toyota Motor Corp. (C+Pod)

- BYD Co. Ltd. (mini-EV platforms)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government Subsidies & Incentives For E-3W / Micro-Evs

- 4.2.2 Rising E-Commerce Last-Mile Delivery Demand

- 4.2.3 Emission Regulations Accelerating ICE-To-EV Shift

- 4.2.4 Urban Congestion & Parking Limits Favouring Quadricycles

- 4.2.5 Battery-Swap Business Models For Commercial Tricycles

- 4.2.6 Egypt Tuk-Tuk-To-Quadricycle Replacement Programme

- 4.3 Market Restraints

- 4.3.1 Sparse Fast-Charging / Swap Infrastructure

- 4.3.2 High Li-Ion Battery Upfront Cost

- 4.3.3 Consumer Shift To Improved Electric Two-Wheelers

- 4.3.4 Pending EU Crash-Safety Rules For L6E/L7E

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Vehicle Type

- 5.1.1 Quadricycle

- 5.1.2 Tricycle (Three-Wheeler)

- 5.2 By Application Type

- 5.2.1 Personal

- 5.2.2 Commercial

- 5.3 By Powertrain Type

- 5.3.1 Internal Combustion Engine

- 5.3.2 Electric

- 5.4 By Design & Configuration

- 5.4.1 Passenger

- 5.4.2 Cargo

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Turkey

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Bajaj Auto Ltd.

- 6.4.2 Piaggio & C. SpA

- 6.4.3 Mahindra & Mahindra Ltd. (Last Mile Mobility)

- 6.4.4 YC Electric Vehicle Private Limited

- 6.4.5 Groupe Renault

- 6.4.6 TVS Motor Company Ltd.

- 6.4.7 Atul Auto Ltd.

- 6.4.8 Kinetic Green Energy & Power Solutions Ltd.

- 6.4.9 Terra Motors Corp.

- 6.4.10 Ligier Group

- 6.4.11 AIXAM MEGA SAS

- 6.4.12 Speego Vehicles Co. Pvt. Ltd.

- 6.4.13 Saera Electric Auto Pvt. Ltd.

- 6.4.14 E-Tuk Factory BV

- 6.4.15 Polaris Inc. (Ranger LSV)

- 6.4.16 Toyota Motor Corp. (C+Pod)

- 6.4.17 BYD Co. Ltd. (mini-EV platforms)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

四輪和三輪車輛市場-2026-2032年全球市場預測

四輪和三輪車輛市場-2026-2032年全球市場預測 四元回收市場分析及至2035年預測:類型、產品、技術、組件、應用、最終用戶、功能、安裝類型、解決方案、模式

四元回收市場分析及至2035年預測:類型、產品、技術、組件、應用、最終用戶、功能、安裝類型、解決方案、模式 四輪車和三輪車市場:按車輛類型、動力傳動系統類型、設計佈局配置、應用、分銷管道和地區分類-產業預測,2026-2033年

四輪車和三輪車市場:按車輛類型、動力傳動系統類型、設計佈局配置、應用、分銷管道和地區分類-產業預測,2026-2033年 四輪和三輪車輛市場報告:按車輛類型、動力來源、應用和地區分類(2026-2034 年)

四輪和三輪車輛市場報告:按車輛類型、動力來源、應用和地區分類(2026-2034 年) 2026年全球四輪摩托車和三輪摩托車市場報告

2026年全球四輪摩托車和三輪摩托車市場報告 全球電動四輪車市場規模、佔有率、趨勢和成長分析報告(2026-2034年)四輪摩托車全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球電動四輪車市場規模、佔有率、趨勢和成長分析報告(2026-2034年)四輪摩托車全球市場規模、佔有率、趨勢和成長分析報告(2026-2034) 四輪和三輪車輛市場-全球產業規模、佔有率、趨勢、機會和預測:按應用、動力來源、車輛類型、地區和競爭格局分類,2021-2031年按動力類型、車輛分類、應用、最終用戶和分銷管道分類的四輪驅動機動車市場—2026-2032年全球預測

四輪和三輪車輛市場-全球產業規模、佔有率、趨勢、機會和預測:按應用、動力來源、車輛類型、地區和競爭格局分類,2021-2031年按動力類型、車輛分類、應用、最終用戶和分銷管道分類的四輪驅動機動車市場—2026-2032年全球預測 四輪車市場規模、佔有率和成長分析(按動力來源、應用、車輛尺寸、應用和地區分類)—產業預測(2026-2033 年)

四輪車市場規模、佔有率和成長分析(按動力來源、應用、車輛尺寸、應用和地區分類)—產業預測(2026-2033 年)