|

市場調查報告書

商品編碼

1910855

低程式碼開發平台:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Low-code Development Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

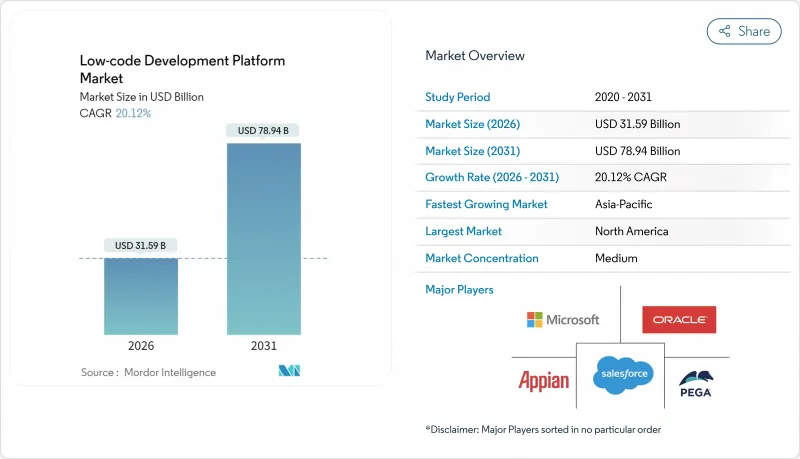

預計到 2026 年,低程式碼開發平台市場規模將達到 315.9 億美元,從 2025 年的 263 億美元成長到 2031 年的 789.4 億美元,2026 年至 2031 年的複合年成長率為 20.12%。

這一成長的驅動力源於對舊有系統現代化改造的迫切需求、開發人員的嚴重短缺以及重視快速應用交付的嚴格監管期限。聯邦機構正在簽署多年期低代碼解決方案一攬子採購協議,歐盟銀行也在爭分奪秒地遵守將於2027年生效的《可組合銀行和資料存取條例》。雲端優先架構、人工智慧驅動的開發協同模式以及不斷擴展的自主雲端框架進一步推動了各行業和地區的採用。隨著平台供應商不斷疊加生成式人工智慧和資料架構功能以縮短建置週期、統一資料並鞏固市場地位,競爭壓力也日益加劇。

全球低程式碼開發平台市場趨勢與洞察

美國聯邦機構透過低程式碼採購強制實現遺留 COBOL 系統現代化

聯邦機構正在逐步淘汰使用了數十年的COBOL平台,並透過多公司總括採購協議轉向低程式碼系統,從而降低23%的合約管理成本。國防合約管理署(DCMA)在其2025年現代化RFI中明確指出,低程式碼是整合合約管理的首選方法。各州政府也正在效仿聯邦政府的做法,擴大符合條件的支出範圍,並將低程式碼平台確立為公共部門快速現代化的標準方法。能夠檢驗是否符合FedRAMP和DoD IL5標準的供應商將優先進入許可權這一日益成長的採購機會,進一步推動低程式碼開發平台市場的發展。

歐盟即時可組合銀行計畫加速低程式碼技術的應用

《金融資料存取條例》要求歐洲銀行在2027年前透過API開放客戶資料。與之配套的《數位營運韌性法案》加強了資訊通訊技術風險監管,並鼓勵金融機構轉向能夠適應不斷變化的監管環境的敏捷架構。低程式碼平台透過自動化產生合規API和證據管理來滿足這兩項需求。歐洲央行監管機構已正式確立了對雲端外包的期望,重視模組化服務部署。因此,傳統銀行正在轉向低程式碼工具,以跟上低程式碼開發平台市場中金融科技挑戰者的快速發布步伐。

鎖定在專有運行時供應商會增加遷移成本

2024 年一項經過同行評審的研究引入了雲端供應商鎖定預測框架,用於量化遷移風險,並強調與專有運行時綁定的應用程式的高成本。許多低程式碼系統將工作流程編譯到封閉式的執行引擎中,限制了其可移植性。資訊長們要求提供原始程式碼匯出和容器化配置選項,這延長了採購週期,並在一定程度上抑制了低程式碼開發平台市場的發展。

細分市場分析

到2025年,平台業務將佔總營收的71.35%,成為低程式碼開發平台市場的基礎。企業傾向於採用整合式環境,將視覺化建模、流程協作和整合資料庫結合,從而減少工具的冗餘。 Salesforce以80億美元收購Informatica等整合策略將資料管理和人工智慧整合到單一執行時間環境中,加劇了企業對供應商的依賴。服務線的擴展緊隨平台部署之後:政府機構採用單一供應商將持續推動對整合諮詢、管治框架和人工智慧加速設計的需求。

服務領域雖然規模較小,但正以 23.45% 的複合年成長率快速成長,因為企業尋求合作夥伴來幫助他們遷移 COBOL 工作負載、整合 ESG 分析以及訓練生成式 AI 助理。對諮詢服務日益成長的需求將推高高級支援和託管服務的附加率,從而為行業增加經常性收入。將訓練、資料架構調優和 AI 模型管治與授權打包在一起的供應商,其生命週期價值將在預測期內翻番,市場佔有率也將擴大。

到2025年,Web應用程式仍將佔總支出的54.40%,但行動工作負載正以22.63%的複合年成長率快速成長,這主要得益於現場技術人員和遠端員工對離線優先功能的需求不斷成長。相機、生物識別和擴增實境(AR)的原生插件使行動體驗更加豐富和情境化。面向行動應用場景的低程式碼開發平台市場規模預計將快速成長,尤其是在保險檢驗和公共產業維護領域。

以 API 為中心的設計將擴展 Web 和行動應用程式的規模,符合可組合銀行和開放資料的要求。微軟計劃從 Dynamics 365 的單體式介面轉向任務導向的 AI 代理,這標誌著介面設計正向情境化的微互動轉變。提供響應式設計、一鍵式 PWA 產生和安全離線同步功能的供應商將在追求多通路統一性的組織中贏得市場佔有率。

區域分析

到2025年,北美將佔據30.60%的收入佔有率,這主要得益於聯邦政府的現代化進程和成熟的創投生態系統。美國政府逐步淘汰COBOL語言的舉措以及FedRAMP合規計劃,正為各州政府機構樹立榜樣,促進司法、交通和醫療保健等領域的可複製部署。加拿大正利用低程式碼技術加快金融科技授權和數位身分計劃的核准,推動全部區域的成長動能。創業投資持續支持融合人工智慧的低程式碼Start-Ups,推動產品創新,進而促進低程式碼開發平台市場的發展。

亞太地區以21.13%的複合年成長率領先。日本保險公司正在採用符合審核要求的建構器以遵守國際財務報告準則第17號(IFRS 17),新加坡金融管理局也積極推動金融科技沙盒的快速發展。中國正在為海灣地區的超大規模資料中心提供資金,以建立託管與西方相容運行時環境的主權雲端。印度IT服務巨頭正在將低代碼加速器納入全球轉型契約,以提升出口收入,同時推動國內公共部門採用低程式碼技術。這些共同努力為該地區未來顯著推動低程式碼開發平台市場的成長奠定了基礎。

歐洲正在發揮監管影響力,並塑造全球產品藍圖。歐洲央行(ECB)的雲端標準、開放銀行API的最後期限以及ESG資訊揭露要求,正迫使企業迅速實現合規工作的自動化。北歐各國政府正利用低程式碼入口網站為公民提供服務;德國汽車製造商不顧效能方面的擔憂,仍在開發現場應用程式原型;法國公共產業也在整合ESG報告流程。隨著政策動能不斷增強,歐洲將繼續成為蓬勃發展的低程式碼開發平台市場的基石。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 美國聯邦機構透過低程式碼採購強制實施遺留 COBOL 系統現代化

- 歐盟即時可組合銀行計畫加速低程式碼技術的應用

- 亞太地區保險公司低代碼審核追蹤獲得監管部門核准

- 平台內建的 GenAI Copilot 可將建置週期時間縮短 40%。

- 歐盟ESG報告截止日期推動應用程式部署需求快速成長

- 市場限制

- 與專有運行時供應商的鎖定會增加遷移成本

- 運算密集型工業IoT應用的效能限制

- 資料居住障礙阻礙中東地區雲端優先部署

- 監管或技術環境

- 新興科技趨勢

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 供應商市場定位分析

- 投資分析

第5章 市場規模與成長預測

- 按組件

- 平台

- 服務

- 透過使用

- 基於網路的

- 基於行動裝置的

- 基於桌面/伺服器

- 以 API 為中心和微服務

- 透過部署模式

- 雲

- 本地部署

- 按組織規模

- 小型企業

- 主要企業

- 按行業

- 銀行業

- 金融服務和保險 (BFSI)

- 零售與電子商務

- 政府/國防

- 資訊科技與通訊

- 醫療保健和生命科學

- 製造業

- 能源與公共產業

- 教育

- 媒體與娛樂

- 其他(交通運輸、房地產)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 亞太其他地區

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 奈及利亞

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Microsoft Corporation

- Salesforce Inc.

- Appian Corporation

- Oracle Corporation

- Mendix(Business of Siemens)

- OutSystems Inc.

- ServiceNow Inc.

- Magic Software Enterprises Ltd.

- Quickbase Inc.

- Zoho Corporation

- Clear Software LLC

- Temenos(formerly Kony Inc.)

- AgilePoint Inc.

- Betty Blocks BV

- Creatio Global

- Kissflow Inc.

- Nintex Global Ltd.

- GeneXus International SA

- LANSA Inc.

- Newgen Software Technologies

- WaveMaker Inc.

第7章 市場機會與未來展望

Low-code Development Platform Market size in 2026 is estimated at USD 31.59 billion, growing from 2025 value of USD 26.30 billion with 2031 projections showing USD 78.94 billion, growing at 20.12% CAGR over 2026-2031.

This growth rests on urgent legacy-system modernization, acute developer shortages, and strict regulatory deadlines that reward rapid application delivery. Federal agencies are issuing multi-year blanket purchase agreements for low-code solutions, while EU banks race to meet 2027 composable-banking and data-access rules. Cloud-first architectures, AI-driven development copilots, and expanding sovereign-cloud frameworks are further lifting adoption across industries and regions. Competitive pressure is intensifying as platform vendors layer generative AI and data-fabric capabilities to shorten build cycles, consolidate data, and defend market position.

Global Low-code Development Platform Market Trends and Insights

Mandated modernization of legacy COBOL systems in U.S. federal agencies via low-code procurement

Federal departments are retiring decades-old COBOL platforms and replacing them with low-code systems through multi-award blanket purchase agreements that lower contract overhead by 23% . The Defense Contract Management Agency highlighted low-code in its 2025 modernization RFI as the preferred path for integrated contract management. States now replicate these federal templates, expanding addressable spend and cementing low-code platforms as the public-sector default for rapid modernization. Vendors able to verify FedRAMP and DoD IL5 compliance gain privileged access to this growing procurement wave, supporting further growth for the low-code development platform market.

Real-time composable banking initiatives in the EU accelerating low-code adoption

The Financial Data Access regulation obliges European banks to expose customer data via APIs by 2027. Complementary Digital Operational Resilience Act rules tighten ICT risk oversight and push institutions toward agile architectures that can adapt to weekly rule updates. Low-code platforms answer both needs by generating compliant APIs and automating control evidence. Supervisors at the European Central Bank have formalized cloud-outsourcing expectations that reward modular service deployment. Traditional banks therefore rely on low-code tooling to match the release velocity of fintech challengers across the low-code development platform market.

Proprietary runtime vendor lock-in elevating migration costs

A 2024 peer-reviewed study introduced a cloud vendor lock-in prediction framework that quantifies switching risk and reveals high cost exposures for applications bound to proprietary runtimes. Many low-code systems compile workflows into closed execution engines that limit portability. CIOs now require source-code export and containerized deployment options, slowing purchase cycles and suppressing a portion of the low-code development platform market.

Other drivers and restraints analyzed in the detailed report include:

- APAC insurers' regulatory approval of low-code audit trails

- GenAI copilots within platforms reducing build-cycle time by 40%

- Performance limitations for compute-intensive industrial IoT apps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The platform segment represented 71.35% revenue in 2025 and anchors the low-code development platform market. Enterprises favor unified environments that combine visual modelling, process orchestration, and integrated databases, thereby reducing tool sprawl. Consolidation plays such as Salesforce's USD 8 billion acquisition of Informatica fold data management and AI into a single runtime to deepen enterprise lock-in. Service-line expansion follows platform rollout: federal agencies that standardize on one vendor generate continuous demand for integration consulting, governance frameworks, and AI-prompt design.

Services, while smaller, are growing at 23.45% CAGR as organizations look for partners to migrate COBOL workloads, embed ESG analytics, and train GenAI copilots. This advisory wave lifts attach rates for premium support and managed services, adding recurring revenue layers to the industry. Over the forecast, vendors that package training, data-fabric tuning, and AI-model governance alongside licences can double lifetime value and widen the market.

Web apps still controlled 54.40% spending in 2025, yet mobile workloads are rising at 22.63% CAGR as field technicians and remote employees demand offline-first capabilities. Native plug-ins for camera, biometrics, and augmented reality make mobile experiences richer and more contextual. The low-code development platform market size for mobile use cases is projected to grow rapidly, especially in insurance inspections and utility maintenance.

API-centric designs extend both web and mobile apps, aligning with composable-banking and open-data directives. Microsoft's planned shift from monolithic Dynamics 365 screens to task-oriented AI agents underlines how interfaces will dissolve into contextual micro-interactions. Vendors that ship responsive design, one-click PWA generation, and secure offline sync will capture incremental market share among organizations pursuing multi-channel parity.

Low Code Development Platform Market Report is Segmented by Component (Platform and More), Application Type (Web-Based, Mobile-Based, and More), Deployment Type (On-Premises, Cloud), Organization Size (Small and Medium Enterprises, Large Enterprises), Industry Vertical (BFSI, Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 30.60% revenue in 2025, driven by federal modernization and a mature venture ecosystem. The U.S. government's push to sunset COBOL and enforce FedRAMP compliance sets a template for state agencies, seeding repeatable rollouts across justice, transport, and health. Canada leverages low-code to expedite fintech licensing and digital-identity projects, broadening regional momentum. Venture capital continues to back AI-infused low-code startups, fuelling product innovation that sustains the low-code development platform market.

Asia-Pacific posts the fastest 21.13% CAGR. Japan's insurers adopted audit-ready builders for IFRS 17, while Singapore's Monetary Authority encourages rapid fintech sandboxing. China finances hyperscale data centers in Gulf states, offering sovereign clouds that host Western-compatible runtimes. India's IT-services leaders embed low-code accelerators within global transformation deals, amplifying export revenue while catalyzing local public-sector uptake. These initiatives collectively underpin the region's outsized contribution to future low-code development platform market growth.

Europe wields regulatory influence that shapes global product roadmaps. ECB cloud standards, open-banking API deadlines, and ESG disclosure mandates force enterprises to automate compliance fast. Nordic governments deliver citizen services via low-code Portals, Germany's auto OEMs prototype shop-floor apps despite performance caveats, and French utilities integrate ESG reporting pipelines. With policy momentum compounding, Europe remains a cornerstone of the expanding low-code development platform market.

- Microsoft Corporation

- Salesforce Inc.

- Appian Corporation

- Oracle Corporation

- Mendix (Business of Siemens)

- OutSystems Inc.

- ServiceNow Inc.

- Magic Software Enterprises Ltd.

- Quickbase Inc.

- Zoho Corporation

- Clear Software LLC

- Temenos (formerly Kony Inc.)

- AgilePoint Inc.

- Betty Blocks B.V.

- Creatio Global

- Kissflow Inc.

- Nintex Global Ltd.

- GeneXus International SA

- LANSA Inc.

- Newgen Software Technologies

- WaveMaker Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandated Modernization of Legacy COBOL Systems in U.S. Federal Agencies via Low-Code Procurement

- 4.2.2 Real-Time Composable Banking Initiatives in EU Accelerating Low-Code Adoption

- 4.2.3 APAC Insurers Regulatory Approval of Low-Code Audit Trails

- 4.2.4 GenAI Copilots Within Platforms Reducing Build-Cycle Time by 40%

- 4.2.5 EU ESG Reporting Deadlines Driving Rapid App Deployment Demand

- 4.3 Market Restraints

- 4.3.1 Proprietary Runtime Vendor Lock-In Elevating Migration Costs

- 4.3.2 Performance Limitations for Compute-Intensive Industrial IoT Apps

- 4.3.3 Data-Residency Barriers Hampering Cloud-First Deployments in Middle East

- 4.4 Regulatory or Technological Outlook

- 4.4.1 Emerging Technology Trends

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Vendor Market Positioning Analysis

- 4.7 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Platform

- 5.1.2 Services

- 5.2 By Application Type

- 5.2.1 Web-Based

- 5.2.2 Mobile-Based

- 5.2.3 Desktop / Server-Based

- 5.2.4 API-Centric & Micro-Services

- 5.3 By Deployment Mode

- 5.3.1 Cloud

- 5.3.2 On-Premise

- 5.4 By Organization Size

- 5.4.1 Small and Medium Enterprises

- 5.4.2 Large Enterprises

- 5.5 By Industry Vertical

- 5.5.1 Banking

- 5.5.2 Financial Services and Insurance (BFSI)

- 5.5.3 Retail and E-commerce

- 5.5.4 Government and Defense

- 5.5.5 Information Technology and Telecom

- 5.5.6 Healthcare and Life Sciences

- 5.5.7 Manufacturing

- 5.5.8 Energy and Utilities

- 5.5.9 Education

- 5.5.10 Media and Entertainment

- 5.5.11 Others (Transportation, Real Estate)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Nordics

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 South Africa

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 United Arab Emirates

- 5.6.5.4 Nigeria

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 Salesforce Inc.

- 6.4.3 Appian Corporation

- 6.4.4 Oracle Corporation

- 6.4.5 Mendix (Business of Siemens)

- 6.4.6 OutSystems Inc.

- 6.4.7 ServiceNow Inc.

- 6.4.8 Magic Software Enterprises Ltd.

- 6.4.9 Quickbase Inc.

- 6.4.10 Zoho Corporation

- 6.4.11 Clear Software LLC

- 6.4.12 Temenos (formerly Kony Inc.)

- 6.4.13 AgilePoint Inc.

- 6.4.14 Betty Blocks B.V.

- 6.4.15 Creatio Global

- 6.4.16 Kissflow Inc.

- 6.4.17 Nintex Global Ltd.

- 6.4.18 GeneXus International SA

- 6.4.19 LANSA Inc.

- 6.4.20 Newgen Software Technologies

- 6.4.21 WaveMaker Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

低程式碼應用開發平台市場:2026-2032年全球市場預測(按組件、開發方法、定價模式、用例、最終用戶產業、部署模式和組織規模分類)

低程式碼應用開發平台市場:2026-2032年全球市場預測(按組件、開發方法、定價模式、用例、最終用戶產業、部署模式和組織規模分類) 低程式碼應用開發平台市場規模、佔有率和成長分析:按組件、部署模式、應用、企業規模、最終用戶產業和地區分類-2026-2033年產業預測

低程式碼應用開發平台市場規模、佔有率和成長分析:按組件、部署模式、應用、企業規模、最終用戶產業和地區分類-2026-2033年產業預測 無程式碼人工智慧平台市場規模、佔有率和成長分析:按組件、部署類型、應用、產業和地區分類-2026-2033年產業預測

無程式碼人工智慧平台市場規模、佔有率和成長分析:按組件、部署類型、應用、產業和地區分類-2026-2033年產業預測 低程式碼人工智慧開發平台市場預測至2034年:按組件、部署類型、企業規模、技術、應用、最終用戶和地區分類的全球分析

低程式碼人工智慧開發平台市場預測至2034年:按組件、部署類型、企業規模、技術、應用、最終用戶和地區分類的全球分析 2026-2030年全球低程式碼人工智慧平台市場低程式碼人工智慧平台市場預測至2034年—按組件、部署類型、企業規模、技術、應用、最終用戶和地區分類的全球分析低程式碼人工智慧開發平台市場預測至2034年—按組件、技術、平台類型、部署模式、應用、最終用戶和地區分類的全球分析低程式碼開發平台市場:按組件、部署類型、組織規模、應用和產業分類-2026年至2032年全球市場預測無程式碼人工智慧平台市場:2026年至2032年全球市場預測,依產業、應用、使用者類型、定價模式、平台組件、部署模式和組織規模分類

2026-2030年全球低程式碼人工智慧平台市場低程式碼人工智慧平台市場預測至2034年—按組件、部署類型、企業規模、技術、應用、最終用戶和地區分類的全球分析低程式碼人工智慧開發平台市場預測至2034年—按組件、技術、平台類型、部署模式、應用、最終用戶和地區分類的全球分析低程式碼開發平台市場:按組件、部署類型、組織規模、應用和產業分類-2026年至2032年全球市場預測無程式碼人工智慧平台市場:2026年至2032年全球市場預測,依產業、應用、使用者類型、定價模式、平台組件、部署模式和組織規模分類 低程式碼開發平台市場:依部署類型、公司規模、應用程式類型、產業和地區分類。

低程式碼開發平台市場:依部署類型、公司規模、應用程式類型、產業和地區分類。