|

市場調查報告書

商品編碼

1910723

碘:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Iodine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

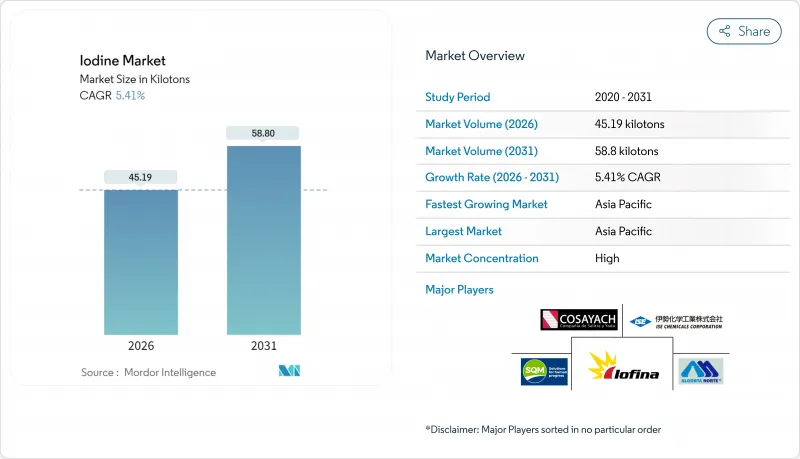

預計到 2026 年,碘市場規模將達到 45.19 千噸,高於 2025 年的 42.87 千噸。預計到 2031 年將達到 58.8 千噸,2026 年至 2031 年的複合年成長率為 5.41%。

碘的需求成長反映了其在X光/CT成像、液晶顯示器和有機發光二極體(LCD/ 有機發光二極體)偏光片、動物保健產品以及特種化學品等領域的不可替代作用,這些領域目前都缺乏經濟有效的替代品。儘管醫療影像仍是碘需求的主要來源,但諸如WET IOsorb等地下鹵水提取技術不斷降低生產成本,削弱了智利鈣質土資源的優勢。亞太地區憑藉著中國電子製造業和印度不斷擴大的診斷能力,推動了碘的消費,但該地區對進口的高度依賴加劇了其對供應中斷的脆弱性。 2022-2023年供不應求後,全球庫存緊張,促使下游用戶簽訂長期合約、穩定現貨價格並推廣回收利用,從而形成了一個更可預測但仍然脆弱的供需平衡。

全球碘市場趨勢及展望

對X光/CT造影劑的需求不斷成長

全球診斷工作量持續成長,光是2023年就進行了超過1,000萬例Medicare造影CT掃描,凸顯了供應衝擊帶來的成本。合約造影生產商正透過擴大在愛爾蘭的產能以及簽署多年原料供應協議來應對這一挑戰,即使價格較高也能確保碘的供應。強調單劑量和多劑量管瓶的永續性舉措,正將成長模式從「按檢查次數」轉向「按量」模式,從而穩定長期需求。同時,醫院也正在實現供應來源多元化,以應對現貨市場價格飆升帶來的衝擊——2011年,碘的價格一度超過每公斤100美元。隨著印度和東南亞各地放射科的現代化,碘市場正獲得更多結構性利多因素,從而抵消成熟經濟體的市場飽和。

碘缺乏症日益嚴重

近期一項調查顯示,儘管印度食鹽加碘普及率已達92.4%,但孕婦和哺乳期婦女仍存在輕度碘缺乏,僅靠食鹽加碘不足以確保充足的碘攝取。中國2025年修訂的膳食參考攝取量進一步證實了因地制宜的營養策略的有效性,這些策略更依賴緩釋肥料和生物強化作物來彌補剩餘的營養缺口。同時,從美國食品藥物管理局(FDA)到香港食物安全中心等監管機構,都在加強標籤法規,以防止因食用單份碘含量超過400微克的海苔零食而導致意外過量攝入碘。這些平行趨勢推動了食品加工用藥用級碘酸鹽需求的穩定成長,同時也促進了緩釋肥料包衣技術的發展,從而創造了非醫療需求。

毒性問題和治療費用

美國職業安全與健康管理局 (OSHA) 將職場碘蒸氣濃度限制在 0.1 ppm,而美國政府工業衛生學家協會 (ACGIH) 建議採用更嚴格的限制,即 0.01 ppm,這要求加工商投資購買洗滌器、隔離室和持續監測設備。同時,美國環保署 (EPA) 對碘基抗菌劑的重新註冊決定也在不斷變化,要求配方商改用更環保的溶劑並提交額外的毒理學文件。儘管醫用同位素用量不大,但仍需要額外的輻射安全通訊協定,這增加了綜合生產商的營運成本。這些監管要求共同提高了新進入者的成本門檻,並可能在監管基礎設施薄弱的地區延誤計劃批准。

細分市場分析

截至2025年,鈣質礦佔全球碘供應量的50.72%,在碘市場佔據主導地位,但由於鹽水計劃的激增,其相對佔有率正在下降。鈣質礦每2,500公斤礦石僅產出1公斤碘,加上智利加強了用水量監測,削弱了其與地下鹽水開採的競爭力。地下鹽水開採的氧化和萃取過程更為簡單。地下鹽水開採正以5.55%的複合年成長率快速擴張,利用現有的油氣基礎設施最大限度地降低資本成本和單位消費量,鞏固了其作為成長最快供應途徑的地位。回收用於電子元件的偏光片在技術上是可行的,儘管目前仍處於起步階段。隨著回收成本的下降,回收碘有望滿足小眾的高純度需求,並緩解首次使用碘的激增。目前,海藻萃取物服務於一個專門的細分市場,為注重「生物來源」認證的保健食品和營養補充劑生產商提供原料,但與主要工業來源相比,其產量仍然小規模。

碘市場報告按來源(地下鹵水、鉀礦、海藻、回收碘)、形態(元素和同位素、無機鹽和錯合、有機化合物)、終端用戶行業(飼料、醫療、消毒劑、光學偏光片等)以及地區(北美、南美、歐洲、亞太、中東和非洲)進行分析。市場預測以千噸為單位。

區域分析

到2025年,亞太地區將佔全球碘市場的34.27%,年複合成長率達6.82%,主要得益於中國電子產業生態系統的發展、對造影造影的強勁需求以及公共衛生強化計畫。中國最新的五年規劃旨在擴大診斷能力,即使國內礦石和鹵水計劃達到瓶頸,原物料需求預計仍將保持穩定。印度的需求則得益於CT掃描的快速成長和標準化的碘鹽計劃,使其成為新興的醫藥級碘酸鹽主要消費國。

北美市場成熟且穩健,以奧克拉荷馬州和猶他州的美國鹽湖開採業務為核心。該地區強大的垂直整合策略有效降低了進口風險。近期對模組化開採設備的投資反映了旨在促進關鍵礦產供應鏈本地化的政策,預計隨著2024年IO#10項目的運作,這一趨勢將進一步加強。

歐洲維持嚴格的食品安全標準和職業接觸限制,這推動了嬰幼兒營養和藥物領域對高純度碘酸鹽的需求。德國、法國和英國支持區域消費,而乳製品行業的殘留基準值則自然地抑制了其成長。隨著對氯己定替代品的評估,為應對抗菌素抗藥性而加強的監管措施可能會進一步增加醫院消毒劑中碘的使用量。

南美洲依賴智利的出口,其供應量遠超過消費量。儘管巴西和阿根廷的國內消費成長受到醫療保健支出和農藥需求增加的推動,但該地區的淨出口仍保持強勁成長。中東和非洲地區的絕對噸位雖然最小,但海灣地區的醫院手術量已實現兩位數成長,並且正在進行碘肥的早期試驗,以解決該地區的營養缺乏問題。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 對X光和CT造影劑的需求不斷成長

- 碘缺乏症日益嚴重

- 擴大液晶顯示器和有機發光二極體偏光片的生產

- 增加牲畜消毒劑的使用

- 直接提取鹽水的成本優勢

- 市場限制

- 毒性問題和處理成本

- 方解石衍生碘的價格波動

- 乳製品中碘殘留的監管限制

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 按來源

- 地下鹽水

- 鈣質礦

- 海藻

- 回收利用

- 按形式

- 元素和同位素

- 無機鹽和錯合

- 有機化合物

- 按最終用途行業分類

- 動物飼料

- 醫療用品(X光造影劑、藥品、帶碘化合物和優碘)

- 消毒劑

- 光學偏光片

- 氟化學品

- 尼龍

- 其他終端用戶產業

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Algorta Norte

- Calibre Chemicals Pvt. Ltd.

- Cosayach

- Deep Water Chemicals

- Eskay Iodine

- Glide Chem Private Limited

- Godo Shigen Co. Ltd

- Infinium Pharmachem Limited

- Iochem Corporation

- Iofina plc

- ISE CHEMICALS CORPORATION

- K&O Energy Group Inc.

- Nippoh Chemicals Co. Ltd

- Parad Corporation Pvt Ltd

- Proto Chemical Industries

- Salvi Chemical Industries Ltd

- Samrat Pharmachem Limited

- SQM

- TOHO EARTHTECH,INC

- Woodward Iodine LLC

第7章 市場機會與未來展望

Iodine market size in 2026 is estimated at 45.19 kilotons, growing from 2025 value of 42.87 kilotons with 2031 projections showing 58.8 kilotons, growing at 5.41% CAGR over 2026-2031.

Volume growth reflects the element's irreplaceable role in X-ray/CT imaging, LCD and OLED polarizers, livestock hygiene products, and specialty chemicals, all of which lack cost-effective substitutes. Medical imaging remains the pivotal demand anchor, while underground brine extraction technologies such as WET IOsorb continue lowering production costs and diluting the dominance of Chilean caliche ore resources. Asia-Pacific leads consumption on the back of Chinese electronics manufacturing and India's expanding diagnostic capacity, even as the region's import dependency magnifies exposure to supply disruptions. Tight global inventories following 2022-2023 shortages have prompted downstream users to sign longer contracts, stabilize spot prices, and encourage recycling initiatives, creating a more predictable yet still fragile supply-demand balance.

Global Iodine Market Trends and Insights

Rising Demand for X-Ray/CT Contrast Media

Global diagnostic workloads keep climbing, and more than 10 million Medicare contrast CT scans in 2023 alone illustrated the cost of any supply shocks. Contract-media producers have responded by expanding Irish-based capacity and by committing to multi-year feedstock contracts that lock in iodine supply even at premium prices. Sustainability initiatives that emphasize individualized dosing and multi-dose vials are shifting growth toward a procedure-volume model rather than per-procedure intensity, which steadies long-run demand. Hospitals are concurrently diversifying suppliers to shield themselves from the spot-market spikes that pushed prices above USD 100 per kg in 2011. As radiology departments modernize across India and Southeast Asia, the iodine market gains an additional structural tailwind that offsets mature-economy saturation.

Growing Iodine-Deficiency Disorders

Universal Salt Iodization lifted India's household coverage to 92.4% in the latest survey, yet mild deficiency persists among pregnant and lactating women, proving that fortification alone cannot guarantee adequate intake. China's 2025 dietary-reference update further validated region-specific nutrition strategies that increasingly rely on controlled-release fertilizers and biofortified crops to close residual gaps. Regulatory agencies from the U.S. FDA to Hong Kong's Centre for Food Safety are concurrently tightening label rules to prevent accidental overconsumption from seaweed snacks whose single-serve iodine content can exceed 400 µg. These parallel trends support measured volume growth for pharmaceutical-grade iodates used in food processing while spurring innovation in slow-release fertilizer coatings that add non-medical demand.

Toxicity Concerns and Handling Costs

OSHA caps workplace iodine vapor at 0.1 ppm, while ACGIH recommends an even tighter 0.01 ppm, obliging processors to invest in scrubbers, isolation booths, and continuous monitoring. At the same time, the EPA's reregistration decision for iodine-based antimicrobials continues to evolve, pushing formulators toward greener solvents and demanding extra toxicological dossiers. Medical isotopes raise additional radiation-safety protocols despite low volume, compounding overhead for integrated producers. Collectively these compliance layers raise the cost floor for new entrants and can slow project sanctioning in regions with limited regulatory infrastructure.

Other drivers and restraints analyzed in the detailed report include:

- Expanding LCD and OLED Polarizer Production

- Increasing Livestock Disinfectant Use

- Regulatory Curbs on Residual Iodine in Dairy

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Caliche ore contributed 50.72% of global supply in 2025, equal to more than half of the iodine market, but its relative share continues slipping as brine projects gain acceptance. The segment's 2,500 kg ore-per-kilogram output ratio, coupled with water-use scrutiny in Chile, is eroding competitiveness versus subterranean brines that offer simpler oxidation-extraction sequences. Underground brine extraction, expanding at a 5.55% CAGR, leverages existing oil-and-gas infrastructure to minimize infrastructure cost while lowering unit energy consumption, reinforcing its position as the fastest-growing supply route. Recycling of electronics-grade polarizer film is still embryonic in tonnage but is technically viable; as recovery costs fall, reclaimed iodine may cover niche, high-purity demand, tempering first-use consumption spikes. Seaweed-based extraction, now a specialized niche, services health-food and nutraceutical producers who prize "biogenic" credentials, yet output volumes remain small relative to the main industrial streams.

The Iodine Report is Segmented by Source (Underground Brine, Caliche Ore, Seaweed, and Recycling), Form (Elementals and Isotopes, Inorganic Salts and Complexes, and Organic Compounds), End-User Industry (Animal Feed, Medical, Biocides, Optical Polarizing Films, and More), and Geography (North America, South America, Europe, Asia-Pacific, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Kilotons).

Geography Analysis

Asia-Pacific held 34.27% of the iodine market in 2025 and is growing at 6.82% CAGR, fueled by China's electronics ecosystem, robust contrast-media demand, and public-health fortification programs. China's latest Five-Year Plan targets expanded diagnostic capacity, implying persistent feedstock pulls even as domestic ore and brine projects plateau. India sustains demand through high CT procedure growth and regulated iodized-salt programs, positioning the country as a major incremental consumer of pharmaceutical-grade iodates.

North America shows mature yet resilient performance underpinned by U.S. brine operations in Oklahoma and Utah, where stable vertical-integration strategies mitigate import risk. Recent investments in modular extraction units underscore a policy push to localize critical-mineral supply chains, a trend reinforced by the IO#10 facility ramp-up in 2024.

Europe maintains stringent food-safety and occupational-exposure rules, driving demand for highly purified iodates in infant nutrition and pharmaceuticals. Germany, France, and the United Kingdom anchor regional consumption, while dairy-sector residue ceilings impose a natural brake on growth. Regulatory momentum toward antimicrobial-resistance mitigation may further elevate iodine use in hospital disinfectants as chlorhexidine alternatives undergo scrutiny.

South America hinges on Chilean exports that dominate supply rather than consumption. Domestic uptake in Brazil and Argentina is climbing alongside healthcare spending and agrochemical demand, yet regional net exports remain firmly positive. The Middle East and Africa, though the smallest territory in absolute tonnage, registers double-digit procedure growth in Gulf hospitals and showcases early iodine-fertilizer trials aimed at correcting local dietary deficiencies.

- Algorta Norte

- Calibre Chemicals Pvt. Ltd.

- Cosayach

- Deep Water Chemicals

- Eskay Iodine

- Glide Chem Private Limited

- Godo Shigen Co. Ltd

- Infinium Pharmachem Limited

- Iochem Corporation

- Iofina plc

- ISE CHEMICALS CORPORATION

- K&O Energy Group Inc.

- Nippoh Chemicals Co. Ltd

- Parad Corporation Pvt Ltd

- Proto Chemical Industries

- Salvi Chemical Industries Ltd

- Samrat Pharmachem Limited

- SQM

- TOHO EARTHTECH,INC

- Woodward Iodine LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for X-Ray/CT Contrast Media

- 4.2.2 Growing Iodine?Deficiency Disorders

- 4.2.3 Expanding LCD and OLED Polarizer Production

- 4.2.4 Increasing Livestock Disinfectant Use

- 4.2.5 Direct Brine Extraction Cost Advantage

- 4.3 Market Restraints

- 4.3.1 Toxicity Concerns and Handling Costs

- 4.3.2 Price Volatility of Caliche-Derived Iodine

- 4.3.3 Regulatory Curbs on Residual Iodine In Dairy

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Source

- 5.1.1 Underground Brine

- 5.1.2 Caliche Ore

- 5.1.3 Seaweed

- 5.1.4 Recycling

- 5.2 By Form

- 5.2.1 Elementals and Isotopes

- 5.2.2 Inorganic Salts and Complexes

- 5.2.3 Organic Compounds

- 5.3 By End-use Industry

- 5.3.1 Animal Feed

- 5.3.2 Medical (X-ray contrast media, pharmaceuticals, iodophors and povidone-iodine)

- 5.3.3 Biocides

- 5.3.4 Optical Polarizing Films

- 5.3.5 Fluorochemicals

- 5.3.6 Nylon

- 5.3.7 Other End-user Industries

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)**/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Algorta Norte

- 6.4.2 Calibre Chemicals Pvt. Ltd.

- 6.4.3 Cosayach

- 6.4.4 Deep Water Chemicals

- 6.4.5 Eskay Iodine

- 6.4.6 Glide Chem Private Limited

- 6.4.7 Godo Shigen Co. Ltd

- 6.4.8 Infinium Pharmachem Limited

- 6.4.9 Iochem Corporation

- 6.4.10 Iofina plc

- 6.4.11 ISE CHEMICALS CORPORATION

- 6.4.12 K&O Energy Group Inc.

- 6.4.13 Nippoh Chemicals Co. Ltd

- 6.4.14 Parad Corporation Pvt Ltd

- 6.4.15 Proto Chemical Industries

- 6.4.16 Salvi Chemical Industries Ltd

- 6.4.17 Samrat Pharmachem Limited

- 6.4.18 SQM

- 6.4.19 TOHO EARTHTECH,INC

- 6.4.20 Woodward Iodine LLC

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

碘市場-2026-2032年全球市場預測

碘市場-2026-2032年全球市場預測 2026年全球碘缺乏症治療市場報告

2026年全球碘缺乏症治療市場報告 碘市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年

碘市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年 碘市場:依原料、應用及地區分類碘-131同位素市場:依產品類型、應用、最終用途及通路分類-2026-2032年全球預測

碘市場:依原料、應用及地區分類碘-131同位素市場:依產品類型、應用、最終用途及通路分類-2026-2032年全球預測 碘市場報告:按原料、形態、應用和地區分類(2026-2034 年)

碘市場報告:按原料、形態、應用和地區分類(2026-2034 年) 碘市場-全球產業規模、佔有率、趨勢、機會及預測(依來源、形態、應用、區域及競爭格局分類,2021-2031年)

碘市場-全球產業規模、佔有率、趨勢、機會及預測(依來源、形態、應用、區域及競爭格局分類,2021-2031年) 全球碘市場:產業分析、規模、佔有率、成長、趨勢和預測(2025-2032)2025年全球碘市場報告

全球碘市場:產業分析、規模、佔有率、成長、趨勢和預測(2025-2032)2025年全球碘市場報告 2025-2029年全球碘市場

2025-2029年全球碘市場