|

市場調查報告書

商品編碼

1910639

北美全地形車和多用途車市場:市場佔有率分析、行業趨勢、統計數據和成長預測(2026-2031 年)North America ATV And UTV - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

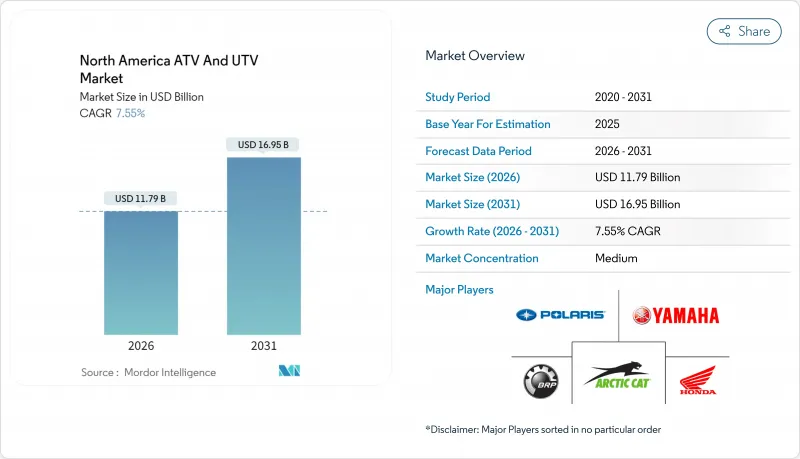

預計到 2026 年,北美 ATV 和 UTV 市場價值將達到 117.9 億美元。

這代表著從 2025 年的 109.6 億美元成長到 2031 年的 169.5 億美元,2026 年至 2031 年的複合年成長率為 7.55%。

強勁的需求源自於休閒步道的擴張、精密農業的興起以及持續的軍事採購。同時,原始設備製造商(OEM)的設計藍圖強調電動動力系統和數位化控制的安全系統。多用途越野車(UTV)的持續成長確保了收入的穩定性,這些平台現在整合了工廠出貨時裝載的遠端資訊處理系統、支援自動駕駛的線束和模組化貨物解決方案,從而降低了農場和公共機構的整體擁有成本。電動並排式越野車在對噪音敏感的旅遊目的地和保護區越來越受歡迎。然而,由於汽油動力系統前期成本低且加油基礎設施完善,它們在價格敏感型細分市場中仍佔據主導地位。隨著德事隆出售北極貓以及北極星在2024年第三季零售下滑,競爭日益激烈。這促使各廠商積極進行車型更新、推出經銷商獎勵計畫並建立在地化的零件供應鏈。

北美全地形車及多用途車市場趨勢及分析

農業機械化的需求不斷成長

安裝在UTV上的基於機器學習的作物監測附件結合了頻譜成像和人工智慧視覺分析技術,能夠即時檢測養分缺乏情況,從而提高15-20%的產量。農民將耐用性視為關鍵的購買標準,促使原始設備製造商(OEM)加固卡車貨廂,使其能夠承受450公斤重的乾草捆。配備亞米級精度GPS的精準導航套件可作為經銷商安裝的選配方案,實現不平坦地形噴灑和土壤採樣的自動化。農業佔全地形車(ATV)工作相關死亡事故的五分之三,因此提高安全性至關重要,這促使翻車檢測系統的引入,該系統可在感測器激活後200毫秒內切斷引擎動力。目前正在愛荷華州測試的一款自主原型車以「跟隨我」模式運行,跟隨聯合運作,從而降低收穫高峰期的人事費用。諸如此類的創新正在將UTV定位為必不可少的農業設備,而非可有可無的配件,並支撐著北美ATV和UTV市場的長期需求。

擴大休閒賽車運動

由各州旅遊機構資助的全地形車(ATV)越野道總長度持續成長,賓州的區域越野道連接線目前已將1200英里的多用途路線與區域住宿目的地連接起來。租賃業者報告稱,年收入超過8.5萬美元,因為導遊業者將設備租賃、越野道許可證和安全裝備打包成週末套餐。在威斯康辛州,允許在指定的縣級道路上行駛全地形車和多用途越野車的立法變更促進了當地旅遊業的發展,並增加了當地住宿設施的收入。設備製造商正在聯合舉辦一些節日活動,例如猶他州的2025年派尤特越野車節,以展示新車型並透過遠端資訊處理技術收集即時性能數據。因此,北美全地形車和多用途越野車市場正在滿足全球對全地形車的巨大需求,並支撐著售後市場零件和服裝銷售的持續成長。

高昂的購置和維修成本

高階UTV的價格現已超過3萬美元,一輛配置齊全的2025年北極星Ranger XP Kinetic售價高達37,499美元。對於商業車隊所有者而言,不斷上漲的保險成本和零件庫存佔用了大量營運資金,因為傳動系統、懸吊和電池模組都是品牌特定的。雖然預計電動車型將在五年內降低五分之一以上的營運成本,但經銷商有限的服務能力可能意味著高壓零件故障時會造成長時間的停機。融資的複雜性給管理季節性現金流的小規模農場帶來了挑戰。貸款機構通常要求20%的首付以及車輛以外的抵押品。價格壓力減緩了車輛的更換週期,抑制了短期銷售成長,儘管北美ATV和UTV市場的長期基本面依然強勁。

細分市場分析

到2025年,多用途越野車(UTV)將佔據北美全地形車(ATV)和UTV市場71.18%的佔有率,複合年成長率(CAGR)為7.66%。多用途應用(包括建築、緊急應變和山地旅遊)的高需求推動了這一市場主導地位。這項優勢增強了貨箱襯墊、駕駛室封閉裝置和液壓升降套件供應商的規模經濟效益。預計到2031年,北美多用途UTV配置的市場佔有率將快速成長,這主要得益於經銷商安裝的遠端資訊處理技術,該技術將規範市政車隊的監控。運動型UTV車型,例如Yamaha的Wolverine RMAX4 1000,幫助製造商在保持高利潤率的同時,展示了可應用於工作車型的懸吊技術。

全地形車 (ATV) 在一些細分市場中仍然保持著重要地位,這些市場尤其注重單人駕駛的操控性、輕量化車身和窄輪距,特別是那些要求車輛寬度小於 50 英寸的越野路段。原始設備製造商 (OEM) 的藍圖圖顯示,到 2025 年將推出六款新型 ATV,這些車型將整合線傳油門、盲點雷達和原廠絞車,以抵禦快速發展的 UTV 對市場佔有率的衝擊。 ATV 翻滾標準和 UTV 乘員保護通訊協定的監管協調可能會模糊傳統的車型分類界限。預計未來的車型將共用底盤部件和電力電子設備。由此產生的模組化平台架構有望縮短開發週期,在保持創新步伐的同時,緩解北美 ATV 和 UTV 市場不斷上漲的零件成本。

截至2025年,汽油引擎將佔據北美全地形車(ATV)和多用途車(UTV)市場62.67%的佔有率。然而,受更嚴格的排放氣體法規和消費者對更安靜駕駛體驗的偏好推動,電動動力系統將以7.62%的複合年成長率成長。本田在北卡羅來納州的擴張計劃旨在確保電池組和整車組裝能力,這標誌著電動動力系統正逐漸被主流市場所接受。假設電池價格持續下降,預計到2031年,北美ATV和UTV市場的電動車型規模將大幅成長。同時,柴油動力仍將局限於重型農場和林業應用領域,在這些領域,高扭矩牽引力超過了能量密度的限制。

像HuntVe的Switchback這樣的混合動力增程概念車代表了一種過渡架構。 72V鋰電池組可提供25英哩的靜音續航里程,之後708cc汽油引擎才會啟動。加州政策制定者已經強制實施了相當於第五階段排放標準的非道路排放標準,加速了公共車輛的電氣化。然而,電動車要在大眾市場廣泛應用,還必須等到在越野路段和農場附近建立起完善的240V二級充電基礎設施。目前,中西部各州的公用事業公司和經銷商正在透過一項聯合計劃來滿足這一需求。在這些電網升級改造完成之前,汽油動力車輛仍將繼續主導北美全地形車和多用途車的銷售市場。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 農業機械化的需求不斷成長

- 休閒和賽車運動活動增加

- 自然保護和狩獵領域對安靜的電動並排式車輛的需求

- 懸吊和安全技術的進步

- 步道旅遊獎勵計劃

- 鄉村地區的寬頻車輛連接

- 市場限制

- 高昂的購置和維修成本

- 鋰供應鏈波動

- 加強對排放氣體和噪音的監管

- 土地所有者責任訴訟

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按車輛類型

- 全地形車(ATV)

- 運動型全地形車

- 多用途/工作用全地形車

- 多用途越野車(UTV/並排式越野車)

- 運動型多用途越野車

- 多用途UTV

- 全地形車(ATV)

- 按推進方式和燃料類型

- 汽油

- 柴油引擎

- 電動車

- 混合

- 按最終用途行業分類

- 休閒與體育

- 農業/林業

- 工業與建築

- 軍事和政府機構

- 搜救和緊急服務

- 按座位數和容量

- 單人座

- 2-3座

- 4-6座

- 按驅動類型

- 兩輪驅動

- 四輪驅動

- 全輪驅動

- 按國家/地區

- 美國

- 加拿大

- 北美其他地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Polaris Inc.

- BRP Inc.(Can-Am)

- American Honda Motor Co.

- Yamaha Motor Co.

- Kawasaki Heavy Industries

- Textron Inc.(Arctic Cat & Tracker Off-Road)

- Suzuki Motor Corp.

- CF Moto Powersports

- Kubota Corp.

- Deere & Company(Gator)

- Mahindra Automotive NA(ROXOR)

- Segway Powersports

- Hisun Motors Corp.

- DRR USA Inc.

- Intimidator/BAD BOY Off-Road

- ODES Powersports

- Club Car LLC

- Toro Co.

- Kioti(Daedong-USA)

第7章 市場機會與未來展望

The North America ATV and UTV market size in 2026 is estimated at USD 11.79 billion, growing from 2025 value of USD 10.96 billion with 2031 projections showing USD 16.95 billion, growing at 7.55% CAGR over 2026-2031.

Robust demand is rooted in recreational trail expansion, precision-farming uptake, and ongoing military procurement, while OEM design roadmaps emphasize electrified drivetrains and digitally controlled safety systems. Persistent growth of utility terrain vehicles (UTVs) safeguards revenue stability as these platforms now integrate factory-installed telematics, autonomous-ready wire-harnesses, and modular cargo solutions that lower the total cost of ownership for farms and public agencies. Electric side-by-sides gain traction in noise-sensitive tourism zones and conservation areas. Yet, gasoline powertrains remain dominant among price-sensitive segments because of their lower upfront cost and established refueling infrastructure. Competitive intensity has heightened after Textron divested Arctic Cat and Polaris confronted retail decline in Q3 2024, prompting aggressive model refreshes, dealer incentive programs, and localization of component supply chains.

North America ATV And UTV Market Trends and Insights

Growing Agricultural Mechanization Needs

Machine-learning-based crop-scouting attachments mounted on UTVs deliver 15-20% yield gains by combining multispectral imaging and AI vision analytics that flag nutrient deficiencies in real time. Farmers cite durability as their prime purchase criterion, pushing OEMs to reinforce cargo beds to withstand 450 kg hay bale loads. Precision guidance kits with sub-meter GPS accuracy now ship as dealer-installed options, automating spraying and soil sampling on irregular fields. Safety enhancements remain critical because agriculture accounts for three-fifth of work-related ATV fatalities, prompting roll-over detection systems that cut engine power within 200 ms of sensor activation. Autonomous prototypes undergoing pilot trials in Iowa operate follow-me modes behind combines, reducing hired-hand costs during peak harvest. Such innovations position UTVs as integral field assets rather than discretionary purchases, supporting long-run demand for the North America ATV and UTV market.

Rising Recreational & Motorsports Activities

ATV trail mileage funded by state tourism boards keeps expanding, exemplified by Pennsylvania's Regional Trail Connector that now links 1,200 miles of mixed-use routes to local lodging hubs. Rental fleets report annual profits topping USD 85,000 as guided tour operators bundle equipment hire, trail permits, and safety gear in weekend packages. Wisconsin's statutory update allowing ATVs and UTVs on designated county roads bolsters ride-in/ride-out tourism, lifting rural hospitality revenue. Equipment OEMs co-sponsor festivals such as Utah's 2025 Paiute Trail Jamboree to showcase new models and collect real-time performance data through telematics. As a result, the North America ATV and UTV market captures significant global ATV demand, underpinning sustained aftermarket parts and apparel sales.

High Purchase & Maintenance Costs

Premium UTV stickers now eclipse USD 30,000 with the 2025 Polaris RANGER XP Kinetic topping USD 37,499 in fully optioned trim. For commercial fleet owners, high insurance costs and parts inventory tie up working capital because driveline, suspension, and battery modules remain brand-specific. Electric models promise more than one-fifth lower running costs over five years, yet limited dealership service capability prolongs downtime when high-voltage components fail. Financing complexities emerge for small farms that manage seasonal cash flows; lenders often require 20% down payments and collateral beyond the vehicle. Price pressure delays replacement cycles, muting short-term unit sales despite robust long-term fundamentals for the North America ATV and UTV market.

Other drivers and restraints analyzed in the detailed report include:

- Silent Electric SxS Demand in Conservation & Hunting

- Technological Advances in Suspension & Safety

- Lithium Supply-Chain Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Utility terrain vehicles commanded 71.18% of the North America ATV and UTV market share in 2025 and growing at a 7.66% CAGR, underscoring their multi-purpose appeal across construction, emergency response, and back-country tourism. This dominance-reinforcing scale advantages for cargo-bed liners, cab enclosures, and hydraulic lift kits suppliers. The North America ATV and UTV market size allocated to multi-purpose UTV configurations is set to grow exponentially by 2031, supported by dealer-installed telematics that standardize fleet monitoring for municipalities. Sport-oriented UTV models such as Yamaha's Wolverine RMAX4 1000 help manufacturers defend high-margin niches while showcasing suspension technology transferable to work-focused trims.

All-terrain vehicles maintain niche relevance where single-rider agility, lower curb weight, and narrower track widths matter, particularly on trail systems mandating sub-50-inch vehicles. OEM roadmaps reveal six new ATV variants for 2025, integrating ride-by-wire throttles, blind-spot radar, and factory-installed winches to protect share against rapidly advancing UTVs. Regulatory alignment of ATV rollover standards with UTV occupant-protection protocols could blur historic category boundaries, with future models sharing chassis components and power electronics. Consequently, platform modularity is poised to reduce development cycles, sustaining innovation cadence while tempering bill-of-materials inflation across the North America ATV and UTV market.

Gasoline engines held 62.67% of the North America ATV and UTV market share in 2025. Yet, electrified drivetrains are advancing at a 7.62% CAGR, reflecting tightening emission caps and user preference for low-noise operation. Honda's expansion in North Carolina earmarks battery packs and final vehicle assembly capacity, signaling mainstream adoption. The North America ATV and UTV market size attributable to electric units is projected to grow drastically by 2031, assuming pack prices decline. Meanwhile, diesel remains confined to heavy-duty ranch and forestry applications where high-torque hauling supersedes energy-density constraints.

Hybrid range-extended concepts such as HuntVe's Switchback illustrate transitional architectures: a 72-V lithium pack supplies 40 km silent range before a 708 cc gasoline engine engages. Policymakers in California already mandate stage-V-equivalent off-road emission limits, hastening fleet electrification among public agencies. Yet mass-market electric penetration awaits infrastructure build-out of 240-V Level-2 chargers across trailheads and farmsteads, a requirement now tackled by cooperative utility-dealer programs in Midwestern states. Until such grid upgrades materialize, gasoline will sustain its majority hold on unit volumes within the North America ATV and UTV market.

The North America ATV & UTV Market Report is Segmented by Vehicle Type (All-Terrain Vehicles and Utility Terrain Vehicles), Propulsion/Fuel Type (Gasoline, Diesel, and More), End-Use Industry (Hybrid, and More), Seating/Capacity (Single-Seat, 2-3 Seat, and 4-6 Seat), Drive Type (2-Wheel Drive and More), and Geography (United States and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

List of Companies Covered in this Report:

- Polaris Inc.

- BRP Inc. (Can-Am)

- American Honda Motor Co.

- Yamaha Motor Co.

- Kawasaki Heavy Industries

- Textron Inc. (Arctic Cat & Tracker Off-Road)

- Suzuki Motor Corp.

- CF Moto Powersports

- Kubota Corp.

- Deere & Company (Gator)

- Mahindra Automotive NA (ROXOR)

- Segway Powersports

- Hisun Motors Corp.

- DRR USA Inc.

- Intimidator/BAD BOY Off-Road

- ODES Powersports

- Club Car LLC

- Toro Co.

- Kioti (Daedong-USA)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing agricultural mechanisation needs

- 4.2.2 Rising recreational & motorsports activities

- 4.2.3 Silent electric SxS demand in conservation & hunting

- 4.2.4 Technological advances in suspension & safety

- 4.2.5 Trail-tourism incentive programs

- 4.2.6 Rural broadband-enabled fleet connectivity

- 4.3 Market Restraints

- 4.3.1 High purchase & maintenance costs

- 4.3.2 Lithium supply-chain volatility

- 4.3.3 Emission & noise regulation tightening

- 4.3.4 Land-owner liability litigation

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Vehicle Type

- 5.1.1 All-Terrain Vehicles (ATVs)

- 5.1.1.1 Sport ATVs

- 5.1.1.2 Utility/Work ATVs

- 5.1.2 Utility Terrain Vehicles (UTVs/Side-by-Sides)

- 5.1.2.1 Sport UTVs

- 5.1.2.2 Multi-purpose UTVs

- 5.1.1 All-Terrain Vehicles (ATVs)

- 5.2 By Propulsion/Fuel Type

- 5.2.1 Gasoline

- 5.2.2 Diesel

- 5.2.3 Electric

- 5.3 By End-use Industry

- 5.3.1 Hybrid

- 5.3.2 Recreation & Sports

- 5.3.3 Agriculture & Forestry

- 5.3.4 Industrial & Construction

- 5.3.5 Military & Government

- 5.3.6 Search, Rescue & Emergency Services

- 5.4 By Seating/Capacity

- 5.4.1 Single-seat

- 5.4.2 2 - 3 seat

- 5.4.3 4 - 6 seat

- 5.5 By Drive Type

- 5.5.1 2-Wheel Drive

- 5.5.2 4-Wheel Drive

- 5.5.3 All-Wheel Drive

- 5.6 By Country

- 5.6.1 United States

- 5.6.2 Canada

- 5.6.3 Rest of North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Polaris Inc.

- 6.4.2 BRP Inc. (Can-Am)

- 6.4.3 American Honda Motor Co.

- 6.4.4 Yamaha Motor Co.

- 6.4.5 Kawasaki Heavy Industries

- 6.4.6 Textron Inc. (Arctic Cat & Tracker Off-Road)

- 6.4.7 Suzuki Motor Corp.

- 6.4.8 CF Moto Powersports

- 6.4.9 Kubota Corp.

- 6.4.10 Deere & Company (Gator)

- 6.4.11 Mahindra Automotive NA (ROXOR)

- 6.4.12 Segway Powersports

- 6.4.13 Hisun Motors Corp.

- 6.4.14 DRR USA Inc.

- 6.4.15 Intimidator/BAD BOY Off-Road

- 6.4.16 ODES Powersports

- 6.4.17 Club Car LLC

- 6.4.18 Toro Co.

- 6.4.19 Kioti (Daedong-USA)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

全地形車(ATV)市場:按類型、驅動方式、動力來源、引擎排氣量、乘客容量、變速箱類型、銷售管道和應用分類-2026-2032年全球市場預測

全地形車(ATV)市場:按類型、驅動方式、動力來源、引擎排氣量、乘客容量、變速箱類型、銷售管道和應用分類-2026-2032年全球市場預測 全球全地形車(ATV)市場:按類型、驅動方式、燃料類型、電池容量、引擎排氣量、乘客容量、車輪數量、應用和地區分類-預測至2035年

全球全地形車(ATV)市場:按類型、驅動方式、燃料類型、電池容量、引擎排氣量、乘客容量、車輪數量、應用和地區分類-預測至2035年 全地形車(ATV)市場機會、成長要素、產業趨勢分析及2026-2035年預測全地形防洪車輛市場按推進系統、車輛類型、應用、終端用戶產業和分銷管道分類,全球預測(2026-2032年)全球全地形車和多用途車市場(按車輪配置、推進方式、車輛類型、引擎排氣量、應用、配銷通路和最終用戶分類)預測,2026-2032年數位驅動系統市場(按馬達類型、齒輪類型、分銷管道、終端用戶產業和車輛類型分類)-全球預測(2026-2032年)

全地形車(ATV)市場機會、成長要素、產業趨勢分析及2026-2035年預測全地形防洪車輛市場按推進系統、車輛類型、應用、終端用戶產業和分銷管道分類,全球預測(2026-2032年)全球全地形車和多用途車市場(按車輪配置、推進方式、車輛類型、引擎排氣量、應用、配銷通路和最終用戶分類)預測,2026-2032年數位驅動系統市場(按馬達類型、齒輪類型、分銷管道、終端用戶產業和車輛類型分類)-全球預測(2026-2032年) 全地形車市場-全球產業規模、佔有率、趨勢、機會及預測,依產品類型、引擎排氣量、應用、地區及競爭格局分類,2021-2031年預測

全地形車市場-全球產業規模、佔有率、趨勢、機會及預測,依產品類型、引擎排氣量、應用、地區及競爭格局分類,2021-2031年預測 多用途地形車(UTV)市場規模、佔有率和成長分析(按引擎排氣量、引擎類型、乘客容量、推進方式、應用和地區分類)-2026-2033年產業預測

多用途地形車(UTV)市場規模、佔有率和成長分析(按引擎排氣量、引擎類型、乘客容量、推進方式、應用和地區分類)-2026-2033年產業預測 全地形車(ATV)市場規模、佔有率和成長分析(按產品類型、引擎排氣量、應用、動力方式和地區分類)-2026-2033年產業預測電動全地形車市場按推進類型、電池類型、電池容量、應用、最終用戶和銷售管道分類-2025-2030 年全球預測

全地形車(ATV)市場規模、佔有率和成長分析(按產品類型、引擎排氣量、應用、動力方式和地區分類)-2026-2033年產業預測電動全地形車市場按推進類型、電池類型、電池容量、應用、最終用戶和銷售管道分類-2025-2030 年全球預測