|

市場調查報告書

商品編碼

1910614

量子感測器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Quantum Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

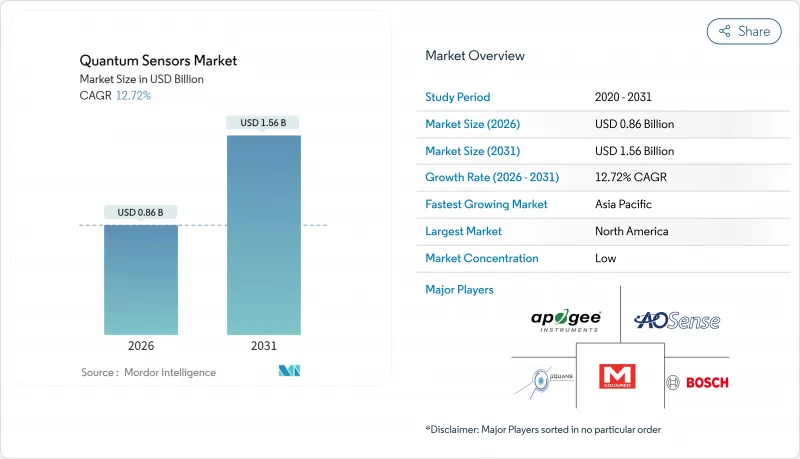

預計到 2026 年,量子感測器市場價值將達到 8.6 億美元,高於 2025 年的 7.6 億美元,預計到 2031 年將達到 15.6 億美元。

預計2026年至2031年年複合成長率(CAGR)為12.72%。

這項快速發展得益於政府和私人部門的共同投資,旨在克服傳統感測技術在授時、導航和原位測量任務方面的限制。美國打擊GPS欺騙的計畫、中國和歐洲的旗艦計劃以及波音公司的量子慣性系統飛行測試都表明,市場對具備戰略級性能的可靠設備有著迫切的需求。超過250億美元的國家量子預算加劇了國內供應鏈的競爭。同時,晶圓級製造技術的進步正在降低單位成本,並開闢新的商業性途徑。航太機構、通訊業者、自動駕駛汽車開發商和雲端資料中心所有者正在探索從奈秒同步到地下資源測繪等系統級優勢。儘管仍存在一些挑戰,例如冷原子元件的退相干、出口管制條例和鹼金屬蒸氣池瓶頸等,但誤差補償演算法和CMOS相容製程的進步正在不斷降低部署風險。

全球量子感測器市場趨勢及展望

增加對量子定位、導航和授時(PNT)技術的國防投入

美國自2024年起簽訂的總額達27億美元的合約表明,即使在GPS訊號受到干擾或欺騙的情況下,量子定位、導航和授時系統仍能保持精度,這體現了戰略上對此類系統的迫切需求。北約國防創新加速器也表達了類似的優先事項,英國在2024年累計1.85億英鎊用於量子授時和導航技術的研究與開發。澳洲也承諾追加1.27億澳元用於類似工作,顯示全球已達成共識,認為量子定位、導航和授時是自主武器、彈性通訊和遠徵後勤保障的關鍵基礎技術。因此,各國國防部目前正在並行採購手錶、量子加速計和量子磁力計,從而形成長尾需求,以穩定早期供應鏈。供應商的藍圖也日益強調抗輻射封裝、抗衝擊性和現場校準工具的重要性,以滿足嚴格的軍用標準。

國家量子舉措和預算

中國耗資150億美元的國家量子資訊科學實驗室、美國重啟的120億美元國家量子舉措以及歐盟70億歐元的量子旗艦計劃,都是致力於將量子感測器製度化為一項自主技術的舉措。日本耗資1兆日圓的「登月計畫」明確設定了2030年實現商業化里程碑的目標,旨在將學術突破與企業生產線連結起來。這些多年預算撥款為大學、國防主要企業和Start-Ups提供可預測的資金,促進合作先導計畫和交叉授權協議的達成。同時,這些撥款也觸發了出口管制法規,鼓勵國內採購蒸氣池組件、雷射和真空子組件。由此產生的政策組合雖然增加了短期合規成本,但確保了開發平臺的持續暢通,從而為量子感測器市場提供充足的供應。

安裝和維修成本高昂

冷原子乾涉儀需要超高真空腔、雷射頻率鎖定和磁屏蔽,這些加起來導致每個站點的資本支出高達200萬美元——比傳統加速計高出幾個數量級。氮氣填充鑽石元件可能需要低溫運行,這需要額外的氦氣處理系統和伺服控制子系統。精通原子物理和光學的工程師供不應求,他們的人事費用推高了營運成本。行動和機載用戶還面臨著在嚴格的尺寸、重量和功耗(SWaP)限制下進行隔振、增壓和溫度控管的額外負擔,這限制了其應用範圍,使其僅限於量子性能具有明確商業價值的高階應用。

細分市場分析

到2025年,手錶仍將佔據量子感測器市場31.45%的最大佔有率,因為電信營運商和資料中心營運商需要同步其網路,從而對納秒級精度提出要求。量子重力儀和梯度儀是成長最快的產品類別,預計到2031年將以15.92%的複合年成長率成長,因為地球觀測衛星和油氣探勘計劃需要高解析度的質量密度圖。量子磁力計應用於神經學、礦產探勘和電子戰任務,而量子加速計和陀螺儀則支援在GPS不可用環境下進行慣性導航。 PAR量子感測器和各種細分領域的設備完善了日益多元化的產品線。供應商正在將多種感測器類型整合到混合有效載荷中,從而能夠從單一模組獲取時間、慣性和磁性資料流,以支援自主系統的融合演算法。這種融合有望實現規模經濟和擴大基本客群,從而支撐量子感測器市場的持續收入成長。

第二波創新浪潮聚焦於晶圓級製造技術,可將蒸氣單元和光子波導管直接嵌入CMOS背板。早期原型已實現組件成本降低40%,並提升了熱穩定性。掌握這些製程的供應商將能夠提供晶粒級子系統用於大規模生產,從而加速其在工業自動化、精密農業和智慧電網監控等領域的應用。Start-Ups、國防主要企業和半導體代工廠之間的交叉授權表明,標準化外形規格的轉變即將到來,這將與傳統MEMS感測器的商業化進程相呼應。

由於數十年的實驗室檢驗和日益成熟的雷射冷卻技術,冷原子乾涉儀在2025年佔據了量子感測器市場44.35%的佔有率。它們在重力和慣性測量方面無與倫比的靈敏度,仍然是大地測量和國防項目的核心。氮空位鑽石感測器具有室溫工作和生物相容性,為心磁圖、腦磁圖和奈米材料研究鋪平了道路,並創下了16.63%的年複合成長率,成為成長最快的領域。里德堡原子電場感測器具有100 MHz的瞬時頻寬,能夠應用於先前量子技術無法觸及的雷達和頻譜分析領域。光機器零件和光子裝置實現了與現有光學儀器的晶片級整合,而超導干涉儀系統則實現了亞飛特斯拉級的靈敏度,可用於低溫物理研究。

雖然機制的多樣化擴大了目標市場,但也給零件供應鏈帶來了壓力。鑽石生長室、銫/銣蒸氣池和高相干雷射二極體都需要專用的生產設備。生態系統參與者正透過組成聯盟來應對這一挑戰,共用智慧財產權並共同投資建設聯合設施,以期獲得規模經濟效益,從而滿足量子感測器市場多學科領域需求的激增。

量子感測器市場按產品類型(手錶、量子磁力計等)、感測機制(冷原子乾涉法、氮空位鑽石等)、部署平台(地面、機載、天基等)、最終用戶(國防安全、航太衛星等)和地區進行細分。市場預測以美元價值為單位。

區域分析

預計到2025年,北美將佔全球收入的36.40%,這得益於DARPA、NASA和美國國家科學基金會(NSF)資助的研究叢集,以及國防部源源不斷的契約,這些契約降低了供應商在加固型設計方面的投資風險。諸如ITAR之類的出口管制框架在保護本地智慧財產權的同時,也施加了許可方面的負擔,並將初始生產集中在美國本土的晶圓廠。圍繞加拿大滑鐵盧形成的量子研究走廊正在引入互補的光子整合技術,並擴展區域生態系統。

亞太地區預計將以15.95%的複合年成長率成為成長最快的地區,這主要得益於中國150億美元的量子計畫以及日本雄心勃勃的舉措旨在連接學術聯盟與電子和材料領域的工業巨頭。澳洲正在資助一個商業化中心,以連接Start-Ups與採礦和國防領域的終端用戶;而韓國正在製定藍圖,為能夠製造沉澱單元和鑽石缺陷的半導體代工廠提供稅收優惠。這波投資浪潮使該地區成為量子感測器市場供需兩端的關鍵參與者,並鞏固了其在量子感測器市場的地位。

在70億歐元的「量子技術旗艦計畫」的推動下,歐洲保持著穩健而適度的成長態勢。德國、法國和荷蘭分別專注於半導體製造設備、雷射系統和原子晶片封裝,從而建構了跨境供應鏈。歐洲太空總署(ESA)的一項太空感測器合約正在將大學和主要企業的航太公司聚集在一起,共同將冷原子有效載荷整合到先進的小型衛星載具。關於兩用物項出口管制和資料主權問題的法規的明確,使得歐洲供應商能夠瞄準民營市場的細分領域,例如精密農業和智慧電網監控,而無需受到同樣程度的《國際武器貿易條例》(ITAR)的限制。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 增加對量子定位、導航和授時(PNT)技術的國防投入

- 國家量子舉措和預算

- 高精度自主導航的需求

- 量子手錶在通訊和資料中心領域的商業部署

- 星載氣候監測重力儀

- 晶圓級製造技術推動成本降低

- 市場限制

- 高昂的實施和維修成本

- 冷原子系統中的環境敏感性/退相干

- 鹼性蒸氣電池供應鏈中的瓶頸(未被察覺)

- 對量子技術的出口管制限制(未引起太多關注)

- 產業價值鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 依產品類型

- 手錶

- 量子磁力計

- 量子加速計/陀螺儀

- 量子重力儀/梯度儀

- PAR量子感測器

- 其他產品類型

- 透過感測機制

- 冷原子乾涉測量

- 氮空位(NV)鑽石

- 里德堡原子電場感測器

- 光機/光電感測器

- 超導性量子乾涉裝置

- 透過部署平台

- 地面

- 機載

- 天基

- 海洋/地下

- 最終用戶

- 國防與安全

- 太空/衛星

- 石油、天然氣和採礦

- 醫療保健和生命科學

- 交通運輸和汽車

- 電信和資料中心

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 智利

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 俄羅斯

- 其他歐洲

- 亞太地區

- 中國

- 日本

- 韓國

- 澳洲

- 印度

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- AOSense Inc.

- Robert Bosch GmbH

- Muquans SAS(iXblue)

- M Squared Lasers Ltd.

- Microchip Technology Inc.

- Apogee Instruments Inc.

- Campbell Scientific Inc.

- LI-COR Biosciences Inc.

- Skye Instruments Ltd.

- Q-CTRL Pty Ltd

- Infleqtion Inc.

- SBQuantum Inc.

- iXblue SAS

- Teledyne e2v Semiconductors

- Honeywell Quantum Solutions(Quantinuum)

- Surrey Satellite Technology Ltd.

- SiTime Corp.

- Micro-G LaCoste LLC

- Atomionics Pte Ltd.

- SBQ Instruments AB

第7章 市場機會與未來展望

The quantum sensors market size in 2026 is estimated at USD 0.86 billion, growing from 2025 value of USD 0.76 billion with 2031 projections showing USD 1.56 billion, growing at 12.72% CAGR over 2026-2031.

This rapid expansion stems from synchronized government and commercial investments aimed at overcoming the limits of classical sensing in timing, navigation, and field-measurement tasks. Pentagon programs that counter GPS spoofing, Chinese and European flagship projects, and Boeing's flight tests of quantum inertial systems validate near-term demand for ruggedized devices capable of strategic-grade performance. National quantum budgets topping USD 25 billion intensify the race to secure domestic supply chains, while wafer-scale fabrication lowers unit costs and opens fresh commercial pathways. Space agencies, telecom operators, autonomous vehicle developers, and cloud data-center owners now explore system-level benefits ranging from nanosecond synchronization to subsurface resource mapping. Headwinds persist-decoherence in cold-atom devices, export-control regimes, and alkali-vapor cell bottlenecks-but advances in error-compensation algorithms and CMOS-compatible processes continue to reduce deployment risk.

Global Quantum Sensors Market Trends and Insights

Growing Defense Funding for Quantum PNT

Pentagon contracts worth USD 2.7 billion issued since 2024 illustrate the strategic need for quantum positioning, navigation and timing systems that remain accurate when GPS signals are jammed or spoofed. NATO's Defence Innovation Accelerator echoes this priority, and the United Kingdom earmarked GBP 185 million for quantum timing and navigation R&D in 2024. Australia added AUD 127 million to similar efforts, underscoring a global consensus that quantum PNT is a critical enabler of autonomous weapons, resilient communications and expeditionary logistics. As a result, defense ministries now procure atomic clocks, quantum accelerometers and magnetometers in parallel, creating long-tail demand that stabilizes early-stage supply chains. Vendor roadmaps increasingly emphasize radiation-hardened packaging, shock tolerance and field-calibration tools to satisfy stringent military standards.

National Quantum Initiatives & Budgets

China's USD 15 billion National Laboratory for Quantum Information Sciences, the renewed USD 12 billion US National Quantum Initiative and the EU's EUR 7 billion Quantum Flagship collectively institutionalize quantum sensors as sovereignty technologies. Japan's trillion-yen moonshot program specifically targets commercialization milestones by 2030, linking academic breakthroughs to corporate manufacturing lines. Such multi-year appropriations deliver predictable funding for universities, defense primes and start-ups, stimulating joint pilot projects and cross-licensing agreements. They also trigger protective export-control regimes that encourage local sourcing of vapor-cell components, lasers and vacuum sub-assemblies. The resulting policy mix raises near-term compliance costs yet guarantees sustained R&D pipelines feeding the quantum sensors market.

High Deployment & Maintenance Costs

Cold-atom interferometers require ultra-high vacuum chambers, laser-frequency locks and magnetic shielding that together raise capital outlay to as much as USD 2 million per site-orders of magnitude above classical accelerometers. Nitrogen-vacancy diamond devices must sometimes operate at cryogenic temperatures, introducing helium handling and servo-control subsystems. Skilled technicians versed in atomic physics and optics are scarce, and their salaries amplify OPEX. Mobile and airborne users face additional burdens of vibration isolation, pressurization and thermal management within tight SWaP envelopes, limiting uptake to premium applications where quantum performance delivers clear ROI.

Other drivers and restraints analyzed in the detailed report include:

- Demand for High-Precision Autonomous Navigation

- Commercial Rollout of Quantum Clocks in Telecom/Datacenters

- Spaceborne Climate-Monitoring Gravimeters

- Environmental Sensitivity of Cold-Atom Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Atomic clocks maintained the largest 31.45% share of the quantum sensors market in 2025 as telecom carriers and data-center operators synchronized networks requiring nanosecond accuracy. Quantum gravimeters and gradiometers are the fastest-growing product cohort, expanding at a 15.92% CAGR through 2031 as Earth-observation satellites and oil-and-gas exploration projects seek higher-resolution mass-density maps. Quantum magnetometers service neurology, mineral prospecting and electronic-warfare tasks, whereas quantum accelerometers and gyroscopes underpin inertial navigation when GPS is denied. PAR quantum sensors and miscellaneous niche devices round out an increasingly diversified catalogue. Vendors now integrate multiple sensor types into hybrid payloads, enabling single modules to output timing, inertial and magnetic data streams for autonomous-system fusion algorithms. This convergence promises economy of scale and a broader customer base, supporting sustained revenue lift for the quantum sensors market.

A second wave of innovation centers on wafer-scale fabrication that embeds vapor cells and photonic waveguides directly on CMOS backplanes. Early prototypes achieve 40% component cost reduction and improved thermal stability. Suppliers that master these processes can ship die-level subsystems for high-volume assembly, accelerating diffusion into industrial automation, precision agriculture and smart-grid monitoring. Cross-licensing among start-ups, defense primes and semiconductor foundries signals imminent shifts toward standardized form factors that mirror classical MEMS sensor commoditization.

Cold-atom interferometry led with 44.35% quantum sensors market share in 2025, benefiting from decades of lab validation and steadily maturing laser cooling techniques. Its unmatched sensitivity in gravimetry and inertial measurement remains central to geodesy and defense programs. Nitrogen-vacancy diamond sensors post the swiftest 16.63% CAGR thanks to room-temperature operation and biocompatibility that open paths in magnetocardiography, magnetoencephalography and nanoscale materials research. Rydberg-atom electric-field sensors, with 100 MHz instantaneous bandwidth, target radar and spectrum-analysis tasks formerly outside quantum reach. Optomechanical and photonic devices promise chip-level integration with existing optical equipment, while superconducting interference systems deliver sub-femtotesla sensitivity for cryogenic physics.

Diversification of mechanisms broadens addressable markets yet places pressure on component supply chains. Diamond growth chambers, cesium/rubidium vapor cells and high-coherence laser diodes each require specialized manufacturing setups. Ecosystem players respond by forming consortia that pool IP and co-invest in shared facilities, anticipating the economies of scale necessary to satisfy multi-sector demand spikes in the quantum sensors market.

Quantum Sensors Market Segmented by Product Type (Atomic Clocks, Quantum Magnetometers and More), Sensing Mechanism (Cold-Atom Interferometry, Nitrogen-Vacancy Diamond and More), Deployment Platform (Ground-Based, Airborne, Spaceborne, and More), End-User (Defense & Security, Space & Satellite and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 36.40% of global revenue in 2025, anchored by DARPA, NASA and National Science Foundation-funded research clusters plus a steady flow of Pentagon contracts that de-risk supplier investment in ruggedized designs. Export-control frameworks such as ITAR impose licensing overhead but also protect local intellectual property, concentrating early production in US-based fabs. Canada's quantum research corridor around Waterloo adds complementary photonic-integration expertise, expanding the regional ecosystem.

Asia-Pacific is on track for the fastest 15.95% CAGR, driven by China's USD 15 billion quantum program and Japan's moonshot initiative that pairs academic consortia with industrial titans in electronics and materials. Australia funds commercialization centers that match start-ups with end users in mining and defense, while South Korea's roadmap allocates tax incentives for semiconductor foundries capable of vapor-cell and diamond-defect manufacture. This investment wave positions the region as both a demand and supply powerhouse, elevating its weight in the quantum sensors market.

Europe maintains a cohesive, moderate-growth trajectory under the EUR 7 billion Quantum Technologies Flagship. Germany, France and the Netherlands specialize respectively in semiconductor tooling, laser systems and atomic-chip packaging, forming a transnational supply chain. ESA's space-sensor contracts pull universities and aerospace primes into joint ventures that combine cold-atom payloads with advanced small-sat buses. Regulatory clarity on dual-use export and data-sovereignty issues helps European vendors target civil-market niches such as precision agriculture and smart-grid monitoring without facing the same degree of ITAR restraints.

- AOSense Inc.

- Robert Bosch GmbH

- Muquans SAS (iXblue)

- M Squared Lasers Ltd.

- Microchip Technology Inc.

- Apogee Instruments Inc.

- Campbell Scientific Inc.

- LI-COR Biosciences Inc.

- Skye Instruments Ltd.

- Q-CTRL Pty Ltd

- Infleqtion Inc.

- SBQuantum Inc.

- iXblue SAS

- Teledyne e2v Semiconductors

- Honeywell Quantum Solutions (Quantinuum)

- Surrey Satellite Technology Ltd.

- SiTime Corp.

- Micro-G LaCoste LLC

- Atomionics Pte Ltd.

- SBQ Instruments AB

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing defense funding for quantum PNT

- 4.2.2 National quantum initiatives and budgets

- 4.2.3 Demand for high-precision autonomous navigation

- 4.2.4 Commercial rollout of quantum clocks in telecom/datacenters

- 4.2.5 Spaceborne climate-monitoring gravimeters

- 4.2.6 Wafer-scale fabrication drives cost decline

- 4.3 Market Restraints

- 4.3.1 High deployment and maintenance costs

- 4.3.2 Environmental sensitivity/decoherence of cold-atom systems

- 4.3.3 Alkali-vapor cell supply-chain bottlenecks (under-radar)

- 4.3.4 Export-control restrictions on quantum tech (under-radar)

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Atomic Clocks

- 5.1.2 Quantum Magnetometers

- 5.1.3 Quantum Accelerometers and Gyroscopes

- 5.1.4 Quantum Gravimeters and Gradiometers

- 5.1.5 PAR Quantum Sensors

- 5.1.6 Other Product Types

- 5.2 By Sensing Mechanism

- 5.2.1 Cold-Atom Interferometry

- 5.2.2 Nitrogen-Vacancy (NV) Diamond

- 5.2.3 Rydberg-Atom Electric-Field Sensors

- 5.2.4 Optomechanical / Photonic Sensors

- 5.2.5 Superconducting Quantum Interference Sensors

- 5.3 By Deployment Platform

- 5.3.1 Ground-based

- 5.3.2 Airborne

- 5.3.3 Spaceborne

- 5.3.4 Marine / Sub-surface

- 5.4 By End-user

- 5.4.1 Defense and Security

- 5.4.2 Space and Satellite

- 5.4.3 Oil, Gas and Mining

- 5.4.4 Healthcare and Life Sciences

- 5.4.5 Transportation and Automotive

- 5.4.6 Telecom and Datacenters

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Chile

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 Australia

- 5.5.4.5 India

- 5.5.4.6 Rest of Asia Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AOSense Inc.

- 6.4.2 Robert Bosch GmbH

- 6.4.3 Muquans SAS (iXblue)

- 6.4.4 M Squared Lasers Ltd.

- 6.4.5 Microchip Technology Inc.

- 6.4.6 Apogee Instruments Inc.

- 6.4.7 Campbell Scientific Inc.

- 6.4.8 LI-COR Biosciences Inc.

- 6.4.9 Skye Instruments Ltd.

- 6.4.10 Q-CTRL Pty Ltd

- 6.4.11 Infleqtion Inc.

- 6.4.12 SBQuantum Inc.

- 6.4.13 iXblue SAS

- 6.4.14 Teledyne e2v Semiconductors

- 6.4.15 Honeywell Quantum Solutions (Quantinuum)

- 6.4.16 Surrey Satellite Technology Ltd.

- 6.4.17 SiTime Corp.

- 6.4.18 Micro-G LaCoste LLC

- 6.4.19 Atomionics Pte Ltd.

- 6.4.20 SBQ Instruments AB

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

2026年全球量子感測與測量市場報告

2026年全球量子感測與測量市場報告 量子感測器市場:按產品類型、產業、公司規模和地區分類:產業趨勢與全球市場預測(至2035年)

量子感測器市場:按產品類型、產業、公司規模和地區分類:產業趨勢與全球市場預測(至2035年) 量子感測器市場預測至2034年—全球產品類型、檢測機制、組件、部署平台、技術平台、應用、最終用戶和區域分析

量子感測器市場預測至2034年—全球產品類型、檢測機制、組件、部署平台、技術平台、應用、最終用戶和區域分析 量子感測器市場:按產品、應用和地區分類,2026-2034年

量子感測器市場:按產品、應用和地區分類,2026-2034年 量子感測器市場:2026-2032年全球市場預測(按感測器類型、組件類型、量子感測方法、終端用戶產業、應用和分銷管道分類)

量子感測器市場:2026-2032年全球市場預測(按感測器類型、組件類型、量子感測方法、終端用戶產業、應用和分銷管道分類) 量子感測器:量子糾纏在通訊及其他領域的應用

量子感測器:量子糾纏在通訊及其他領域的應用 量子感測器市場:按產品、產業和地區分類2026年全球量子感測器市場報告

量子感測器市場:按產品、產業和地區分類2026年全球量子感測器市場報告 量子感測器市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、材料類型、裝置、最終用戶、功能及部署方式分類

量子感測器市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、材料類型、裝置、最終用戶、功能及部署方式分類 量子感測器市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2026-2034)

量子感測器市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2026-2034)