|

市場調查報告書

商品編碼

1910593

複合地板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Laminate Flooring - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

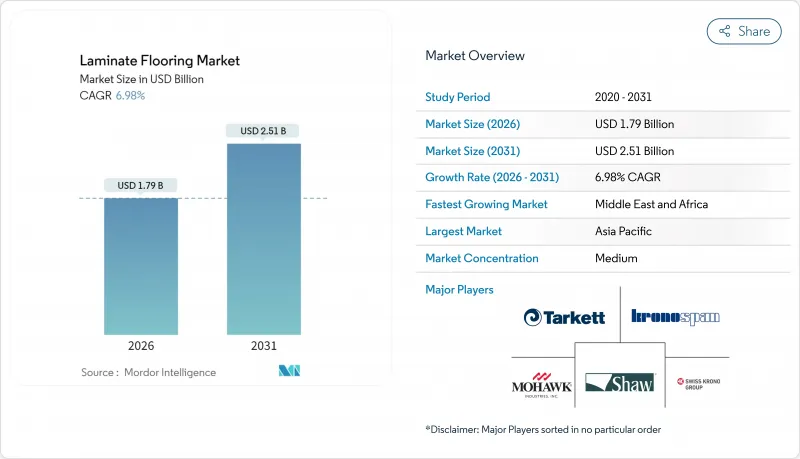

預計到 2025 年,複合地板市場價值將達到 16.7 億美元,到 2026 年將成長至 17.9 億美元,到 2031 年將成長至 25.1 億美元,在預測期(2026-2031 年)內,複合年成長率為 6.98%。

這一成長動能主要得益於疫情後住宅維修需求的增加、亞太地區都市區住宅量的上升,以及更嚴格的甲醛法規促使人們採用更安全的配方。技術創新拓展了應用範圍,例如防水芯材和可減少安裝人工的卡扣式系統,使其在與實木地板和瓷磚的競爭中脫穎而出。隨著豪華乙烯基複合地板材料製造商加大產能投入,市場競爭日益激烈。然而,超耐磨地板仍保持著極具吸引力的成本結構,並且能夠更逼真地模仿天然材質的紋理。雖然高密度纖維板(HDF)和中密度纖維板(MDF)的利潤率對原料價格較為敏感,但主要製造商之間的垂直整合在一定程度上抵消了價格波動的影響。

全球強化複合地板市場趨勢與洞察

自新冠疫情爆發以來,住宅維修活動激增

全球封鎖措施促使消費者將支出轉向住宅維修,推動了地板材料更換需求的激增,即使在經濟重啟後,這一趨勢仍將持續。 Houzz 2024年的調查發現,67%的住宅將進行一項大規模地板材料計劃,其中強化複合地板憑藉其逼真的木紋外觀和低廉的安裝成本,市場佔有率不斷成長。在成熟市場,由於老舊住宅存量需要比新建房屋更頻繁地維修,維修計劃變得越來越普遍,這推動了美國、加拿大、德國和日本等國的需求成長。遠距辦公趨勢維持了對家庭辦公室的需求,進而推動了對耐用地板材料的需求,這種地板比地毯更耐刮擦和咖啡漬。 DIY連鎖店在2024年全年地板材料銷售額強勁成長,家得寶也確認此趨勢將持續到2025年初。製造商正在開發無需專業人員即可在周末完成安裝的簡易卡扣系統,這將進一步增強強化複合地板翻新的需求。

與實木地板相比,價格具競爭力

複合地板的安裝成本比實木地板低約 50%,在木材價格飆升時期,這一差距會進一步擴大。這促使注重預算的買家在價格波動時期考慮更換地板材料。工程複合地板無需重新打磨,降低了終身成本,使其成為租賃房產和首次住宅的成本績效之選。紋理技術的最新進展使得複合地板能夠極其精確地複製手工鋸切的橡木和山核桃木飾面,消除了以往令高階買家望而卻步的美學妥協。建設公司擴大將複合地板應用於樣品屋。這使他們能夠在不犧牲美觀的前提下控制預算,隨著計劃的擴大,這種做法也轉化為買家對升級的需求。零售商在行銷訊息中強調價格差異,提高了消費者對價格優勢的認知。這種經濟吸引力也正在向購買力仍然有限的新興市場蔓延,推動了印度、印尼和巴西等國對複合地板的採用。

HDF/MDF原物料價格波動

纖維板約佔層壓板生產成本的65%,因此,木屑和樹脂原料價格的波動會在供應衝擊期間立即擠壓利潤空間。德國基準預測,2024年高密度纖維板(HDF)價格將上漲15-20%,這將迫使製造商多次提價,並加劇與經銷商的緊張關係。沒有自有板材廠的小型加工商面臨的壓力更大,在某些情況下,他們不得不終止無利可圖的合約。能源價格波動加劇了風險,因為纖維板生產需要大量熱量,成本與天然氣和電力價格密切相關。符合加州空氣資源委員會(CARB)第二階段和歐盟甲醛含量法規增加了樹脂的複雜性和成本,而這些成本並非總是能轉嫁給下游企業。製造商透過簽訂多年纖維合約和建立自有樹脂生產設施來規避風險,但這些策略需要資金,而許多區域性企業恰好缺乏資金。

細分市場分析

2025年,高密度纖維板(HDF)地板憑藉其優異的密度和抗日常人流磨損性能,佔據了強化複合地板市場63.61%的佔有率。同時,中密度纖維板(MDF)地板憑藉其輕盈易裝的優勢,正以7.11%的複合年成長率成長。受同步暫存器技術進步的推動,MDF強化複合地板市場預計將從2026年的6.5億美元成長到2031年的9.2億美元,該技術能夠實現高度逼真的紋理效果。供應商將HDF產品定位在高階市場,並將MDF產品線定位在價值管道,從而在不蠶食競爭對手的情況下實現產品線細分。防潮添加劑的創新正在縮小傳統性能差距,促使設計師考慮將MDF用於承受中等荷載的商業建築。板材製造商正在使用再生木纖維以達到碳排放目標,同時其機械性能也符合EN 13329耐磨等級標準。隨著亞洲工廠加大中密度纖維板(MDF)的產量,預計產業競爭將加劇,單位成本將下降,全球價格壓力將上升。

不同地區的需求趨勢各異。北美地區繼續青睞高密度芯材,因為它能抵抗季節性濕度波動;而歐洲則更注重中密度纖維板(MDF)的永續性。行銷宣傳活動強調低密度板材與襯墊結合使用可顯著提升隔音效果,吸引了尋求噪音控制的多用戶住宅開發商。對中國產高密度纖維板徵收關稅迫使進口商轉向越南和巴西等國採購,最終由於MDF供應穩定而促進了其普及。 Kronospan和Swiss Krono等品牌提案混合結構產品,其密度在板材內部呈現梯度變化,並兼具高密度纖維板的表面耐久性和中密度纖維板的成本績效。未來的創新將探索使用生物基樹脂,以在不影響性能的前提下進一步減少排放。最終,買家會根據價格、穩定性和感知品質的平衡來選擇基材類型。

區域分析

亞太地區預計在2025年佔全球收入的37.95%,主要得益於中國和印度的大規模住宅。該地區預計到2031年將維持6.55%的複合年成長率。中國正在進行的城市改造,地級市對老舊住宅進行翻新,對複合地板等經濟實惠的內部裝潢建材提出了更高的要求。印度的「PMAY-Urban」計畫為低收入住宅津貼,並指定使用複合地板,以平衡預算和滿足消費者對木質美觀的期望。東南亞市場(包括越南和菲律賓)中產階級消費的成長,推動了地板產品零售,並提升了品牌知名度。該地區不同的法規要求產品符合排放標準,促使全球製造商在當地設立檢測實驗室。

中東和非洲是成長最快的地區,年複合成長率達6.82%,這主要得益於沙烏地阿拉伯、埃及和波灣合作理事會(GCC)國家大型企劃的激增,儘管目前成長較為溫和。開發商優先考慮速度和成本可控性,而複合地板恰好能滿足這兩點需求,其外觀也與現代建築風格相得益彰。由於進口依賴度仍然很高,經銷商正在儲備更多種類的產品,以降低運輸不穩定帶來的前置作業時間風險。匯率波動會影響到岸成本,進而推動區域生產。克朗斯潘在中東地區進行的板材工廠可行性研究也印證了這項轉變。消費者教育也在進行中,零售商舉辦安裝研討會,幫助承包商熟悉適合當地勞動力的卡扣式鎖扣技術。北美市場維持了5.05%的穩定年複合成長率,這主要得益於住宅維修的持續需求以及混合辦公模式帶來的辦公室重建的潛在需求。美國對中國製造的板材徵收關稅,刺激了國內生產的成長,莫霍克公司在北卡羅來納州投資 8,700 萬美元的擴建項目正是製造業回歸這一趨勢的象徵。

在歐洲,儘管法國和德國的建築業低迷,但對地板的需求仍在成長。濃厚的DIY文化和節能維修獎勵推動了地板材料升級。歐盟的循環經濟指令提高了人們對經認證的可回收產品的興趣,鼓勵工廠採用生物基黏合劑並實施回收計畫。對中國膠合板徵收的反傾銷稅間接保護了區域強化地板工廠,減輕了其他木質板材的價格競爭。東歐國家,特別是波蘭和羅馬尼亞,憑藉具有競爭力的人事費用和便利的物流位置,正在崛起為出口中心。儘管南美洲受經濟波動影響成長緩慢,年複合成長率僅3.95%,但巴西的「我的家,我的生活」(Minha Casa Minha Vida)社會住宅計畫正在創造對經濟實惠的超耐磨地板的基礎性需求。貨幣貶值導致進口成本上升,促使Duratex等公司進行在地化生產。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 新冠疫情後,住宅維修活動激增

- 與實木地板的成本競爭力及比較

- 亞太地區的快速都市化和住宅需求

- 防水層壓板的技術進步

- DIY地板套裝電商市場的興起

- 歐盟公共工程循環經濟認證

- 市場限制

- HDF/MDF原物料價格波動

- 豪華乙烯基瓷磚(LVT)越來越受歡迎

- 加強甲醛排放法規

- 樹脂添加劑供應鏈中斷

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 產業間競爭

第5章 市場規模與成長預測

- 依產品類型

- 高密度纖維板複合地板

- 中密度纖維板複合地板

- 透過使用

- 住宅

- 商業的

- 透過建設業

- 新房產

- 維修/更換

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 秘魯

- 智利

- 其他南美洲

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 比荷盧經濟聯盟(比利時、荷蘭、盧森堡)

- 北歐國家(丹麥、芬蘭、冰島、挪威、瑞典)

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 東南亞(新加坡、馬來西亞、泰國、印尼、越南、菲律賓)

- 亞太其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Mohawk Industries

- Tarkett SA

- Shaw Industries Group Inc.

- Kronospan Holdings Ltd.

- Swiss Krono Group

- Armstrong Flooring, Inc.

- Mannington Mills, Inc.

- BerryAlloc NV

- Egger Group

- Classen Group

- Kaindl Flooring GmbH

- Faus Group

- Pergo(Unilin)

- Alsafloor

- Beaulieu International Group

- Nature Home Holding Co.

- Der International

- Formica Group

- Quick-Step Flooring

- Milliken & Company

第7章 市場機會與未來展望

The Laminate Flooring Market was valued at USD 1.67 billion in 2025 and estimated to grow from USD 1.79 billion in 2026 to reach USD 2.51 billion by 2031, at a CAGR of 6.98% during the forecast period (2026-2031).

Momentum stems from post-pandemic home renovation, accelerating urban housing starts in Asia-Pacific, and stricter formaldehyde regulations that spur safer formulations. Technology is widening end-use possibilities through water-resistant cores and click-lock systems that cut installation labor, a key advantage over hardwood and ceramic tile alternatives. Competition is intensifying as luxury vinyl players invest in capacity, yet laminate retains a compelling cost profile while replicating natural textures more convincingly than before. Margins remain sensitive to HDF and MDF input prices, but vertical integration among leading mills partially offsets volatility.

Global Laminate Flooring Market Trends and Insights

Surge in Residential Renovation Activities Post-COVID

Global lockdowns reoriented consumer spending toward home upgrades, causing a sharp rise in flooring replacements that persists even as economies reopen. Houzz's 2024 survey showed 67% of homeowners undertook major flooring projects, and laminate won share by combining low install cost with realistic wood visuals. Renovation projects dominate mature markets because aging housing stock requires refreshes more frequently than new builds, boosting volumes in the United States, Canada, Germany, and Japan. Remote work trends keep the spotlight on home offices, directing demand toward durable surfaces that resist chair scuffs and coffee spills better than carpet. DIY chains reported elevated flooring sales throughout 2024, and Home Depot confirmed continuing strength into early 2025. Manufacturers responded with simplified click-systems that allow weekend installation without professional crews, reinforcing laminate's renovation appeal.

Cost Competitiveness Versus Hardwood Flooring

Laminate's installed cost runs roughly 50% below hardwood, a spread that widens when lumber prices spike, prompting thrifty buyers to switch materials during volatile periods. Engineered overlays eliminate the need for refinishing, lowering lifetime expense and positioning laminate as a value-engineered solution for rental properties and first-time homeowners. Recent texturing advances replicate hand-scraped oak or hickory finishes convincingly, reducing the aesthetic compromise that once deterred premium buyers. Builders increasingly use laminate in model homes to control budgets without sacrificing curb appeal, and this practice cascades to buyer upgrades once a project scales. Retailers highlight the value gap in marketing messages, amplifying consumer awareness of price advantages. The economic appeal extends to emerging markets where purchasing power remains constrained, fuelling adoption in India, Indonesia, and Brazil.

Volatility in HDF/MDF Raw-Material Prices

Fibreboard accounts for roughly 65% of laminate production cost, so swings in woodchip and resin inputs quickly erode margins during supply shocks. German indices showed 15-20% HDF inflation during 2024, compelling mills to execute multiple price hikes that strained distributor relationships. Smaller converters lacking captive panel mills faced greater pressure, occasionally exiting unprofitable contracts. Energy price fluctuations magnify the risk because fiberboard production is heat-intensive, tying costs to natural gas and electricity tariffs. Compliance with CARB Phase 2 and EU limits on formaldehyde content adds resin complexity and cost that cannot always be passed downstream. Manufacturers hedge through multi-year fiber contracts and in-house resin facilities, but such strategies require capital that many regional players lack.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Urbanization & Housing Demand in Asia-Pacific

- Technological Advances in Water-Resistant Laminates

- Growing Popularity of Luxury Vinyl Tiles (LVT)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

HDF-based planks commanded 63.61% of laminate flooring market share in 2025 due to superior density that resists indentation during daily traffic. MDF alternatives, however, are increasing at a 7.11% CAGR, capitalizing on lighter weight that eases handling for DIY installers. The laminate flooring market size for MDF substrates is projected to expand from USD 0.65 billion in 2026 to USD 0.92 billion by 2031 as improved emboss-in-register technology delivers highly realistic textures. Suppliers position HDF products at premium price points while MDF lines target value channels, enabling portfolio segmentation without cannibalization. Innovations in moisture-resistant additives blur the historical performance gap, encouraging specifiers to accept MDF in moderate-duty commercial jobs. Panel producers integrate recycled wood fibers to meet carbon goals, yet mechanical properties still meet EN 13329 wear ratings. Sector rivalry is expected to intensify as Asian mills scale MDF output, lowering unit cost and amplifying price competition globally.

Demand dynamics vary regionally, with North America continuing to favor high-density cores for resilience against seasonal humidity swings, while Europe leans toward MDF's sustainability narrative. Marketing campaigns highlight acoustic improvements possible through lower-density boards paired with underlay, a feature attracting multifamily developers seeking noise mitigation. Trade tariffs on Chinese HDF push importers to diversify sourcing from Vietnam and Brazil, inadvertently boosting MDF acceptance where availability proves steadier. Brands such as Kronospan and Swiss Krono showcase hybrid constructions that gradient density across the plank, merging HDF surface durability with MDF affordability. Future innovation may explore bio-based resins to further cut emissions without sacrificing performance. Buyers will ultimately balance price, stability, and perceived quality when selecting substrate types.

The Laminate Flooring Market Report is Segmented by Product Type (High-Density Fiberboard, Medium-Density Fiberboard), Application (Residential, Commercial), Construction (New Construction, Renovation/Replacement), and Geography (North America, South America, Europe, Asia-Pacific, Middle East & Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commanded 37.95% of global revenue in 2025 on the back of large-scale residential construction in China and India, and the region is projected to post a 6.55% CAGR through 2031. Chinese urban renewal continues, with county-level cities redeveloping obsolete housing blocks that require cost-effective interiors like laminate. India's PMAY-Urban scheme subsidizes low-income flats that specify laminate to balance the budget with consumer expectations for wood aesthetics. Southeast Asian markets, including Vietnam and the Philippines, witness rising middle-class consumption, driving organized retail of flooring products and increasing brand awareness. Regulatory diversity across the region necessitates tailored emission compliance, prompting global manufacturers to set up localized testing labs.

Middle East & Africa, though smaller today, is the fastest-growing territory at 6.82% CAGR as megaprojects proliferate in Saudi Arabia, Egypt, and the Gulf Cooperation Council. Developers prioritize speed and cost certainty; laminate delivers both attributes alongside visuals suited to modern architectural themes. Import dependency remains high, so distributors stock broader SKU assortments to limit lead-time risk amid shipping volatility. Currency swings can destabilize landed cost, encouraging regional production; Kronospan's feasibility study for a Middle East panel plant illustrates this pivot. Consumer education is underway as retailers host installation workshops to familiarize contractors with click-lock techniques suitable for local labor pools. North America grows at a steady 5.05% CAGR, propelled by persistent home improvement and a backlog of office conversions sparked by hybrid work arrangements. U.S. tariffs on Chinese panels raise domestic production volumes, and Mohawk's USD 87 million expansion in North Carolina exemplifies reshoring trends.

European demand advances despite construction downturns in France and Germany, as robust DIY cultures and energy-retrofit incentives fuel flooring upgrades. EU circular-economy directives elevate interest in products with verified recyclability, encouraging mills to adopt bio-based binders and take-back programs. Anti-dumping duties on Chinese plywood indirectly shield regional laminate mills by reducing price competition from alternative wood panels. Eastern European countries, notably Poland and Romania, emerge as export hubs due to competitive labor costs and central logistics. South America trails with 3.95% CAGR amid economic volatility, yet Brazil's Minha Casa Minha Vida social-housing initiative adds baseline volume for cost-efficient laminate. Currency depreciation elevates import costs, stimulating local production by firms such as Duratex.

- Mohawk Industries

- Tarkett S.A.

- Shaw Industries Group Inc.

- Kronospan Holdings Ltd.

- Swiss Krono Group

- Armstrong Flooring, Inc.

- Mannington Mills, Inc.

- BerryAlloc NV

- Egger Group

- Classen Group

- Kaindl Flooring GmbH

- Faus Group

- Pergo (Unilin)

- Alsafloor

- Beaulieu International Group

- Nature Home Holding Co.

- Der International

- Formica Group

- Quick-Step Flooring

- Milliken & Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in residential renovation activities post-COVID

- 4.2.2 Cost competitiveness versus hardwood flooring

- 4.2.3 Rapid urbanization & housing demand in APAC

- 4.2.4 Technological advances in water-resistant laminates

- 4.2.5 Rise of DIY e-commerce flooring kits

- 4.2.6 EU circular-economy certifications for public projects

- 4.3 Market Restraints

- 4.3.1 Volatility in HDF/MDF raw-material prices

- 4.3.2 Growing popularity of luxury vinyl tiles (LVT)

- 4.3.3 Stricter formaldehyde-emission regulations

- 4.3.4 Resin-additive supply-chain disruptions

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 High-Density Fiberboard Laminated Flooring

- 5.1.2 Medium-Density Fiberboard Laminated Flooring

- 5.2 By Application

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.3 By Construction

- 5.3.1 New Construction

- 5.3.2 Renovation / Replacement

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Peru

- 5.4.2.4 Chile

- 5.4.2.5 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Spain

- 5.4.3.5 Italy

- 5.4.3.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.4.3.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.4.3.8 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 South Korea

- 5.4.4.5 Australia

- 5.4.4.6 South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines)

- 5.4.4.7 Rest of Asia-Pacific

- 5.4.5 Middle East & Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle East & Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Mohawk Industries

- 6.4.2 Tarkett S.A.

- 6.4.3 Shaw Industries Group Inc.

- 6.4.4 Kronospan Holdings Ltd.

- 6.4.5 Swiss Krono Group

- 6.4.6 Armstrong Flooring, Inc.

- 6.4.7 Mannington Mills, Inc.

- 6.4.8 BerryAlloc NV

- 6.4.9 Egger Group

- 6.4.10 Classen Group

- 6.4.11 Kaindl Flooring GmbH

- 6.4.12 Faus Group

- 6.4.13 Pergo (Unilin)

- 6.4.14 Alsafloor

- 6.4.15 Beaulieu International Group

- 6.4.16 Nature Home Holding Co.

- 6.4.17 Der International

- 6.4.18 Formica Group

- 6.4.19 Quick-Step Flooring

- 6.4.20 Milliken & Company

7 Market Opportunities & Future Outlook

- 7.1 Bio-based zero-VOC laminate formulations

- 7.2 Rental-oriented modular click-lock panels