|

市場調查報告書

商品編碼

1910540

消防車:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Fire Truck - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

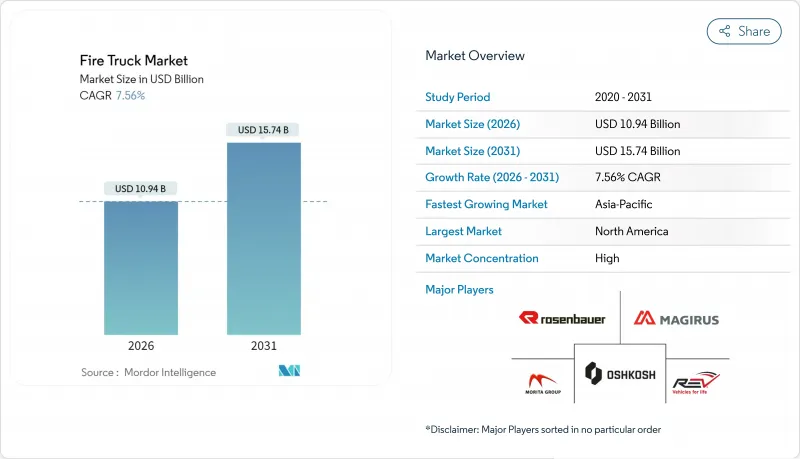

預計消防車市場將從 2025 年的 101.7 億美元成長到 2026 年的 109.4 億美元,到 2031 年將達到 157.4 億美元,2026 年至 2031 年的複合年成長率為 7.56%。

車輛更換週期延長、電氣化程度提高以及氣候變遷導致野火風險加劇,都促使採購預算不斷增加,即便供應鏈瓶頸依然存在。長達18至33個月的交付週期迫使消防部門在等待新車交付期間對其維護計劃進行現代化改造。同時,安全性和性能的提升變得至關重要,消防車市場也持續消化更高的單價。在北美和歐洲,在清潔能源車輛法規以及燃料和維護成本降低的推動下,純電動消防車正從原型車階段走向量產階段。同時,大規模野火的增加推動了對專業野火救援車輛的需求,而隨著美國主要製造商之間的整合,這些車輛正面臨日益嚴格的監管審查。

全球消防車市場趨勢與洞察

更嚴格的全球和區域消防安全法規

新的NFPA 1900標準整合了現有的消防車法規,並強制要求配備後監視錄影機、LED照明和電動車相容性。監管機構透過從規範性的檢查清單轉向性能標準,提高了安全標準,同時也為原始設備製造商(OEM)提供了更大的創新空間。統一的要求也有利於消防車的跨境部署,使擁有全球物流網路的製造商受益。然而,不斷上漲的合規成本正在推動小型製造商之間的整合,進一步加劇了消防車市場的高度集中。

野火發生頻率和嚴重性增加

預計2024年美國面積將達到770萬英畝,超過過去十年的平均水平,儘管火災總數有所下降。規模更大、強度更高的火災促使訂單激增,消防車可以在行進過程中啟動輔助水泵。聯邦和州政府為野火防範提供的津貼正在資助專用設備的購置,並使需求與市政預算週期脫鉤。如今,火災季節幾乎全年無休,迫使消防局保持全年戰備狀態,並提高了消防車的可用性標準。

下一代平台的前期成本很高

像RTX這樣的電動消防車造價近100萬美元,幾乎是同類柴油消防車的兩倍。雖然營運成本的降低改善了整體擁有成本,但初始資金門檻阻礙了志願消防隊和鄉村消防隊的普及。津貼計畫在一定程度上抵消了成本(博爾德市為其第二輛電動消防車獲得了大量外部資金),但在資金充足的大都會圈以外,資金籌措缺口依然存在。儘管電池成本正在下降,但與柴油消防車的價格差距不太可能在2027年後產量大幅提升之前消除。這種兩極化將減緩發展中地區的轉型,並在短期內限制全球消防車市場的成長。

細分市場分析

預計到2025年,水泵車將佔消防車市場的36.28%,到2031年將以7.62%的複合年成長率成長。水泵車的演變包括增加壓縮空氣泡沫系統和模組化車身,為消防部門提供多功能能力。早期電氣化也促進了該細分市場的收入成長,Rosenbauer的RTX平台實現了與柴油車型相媲美的泵送性能。在缺乏消防栓網路的地區,罐式消防車仍然至關重要,而雲梯消防車則滿足了日益增多的高層建築的需求。 Bronto Skylift的230英尺(約70公尺)臂展足以覆蓋20層樓高的建築。

現代救援車輛配備了液壓救援工具和電池驅動的切割裝置,縮短了現場準備時間。集消防車、水罐車和救援車功能於一體的綜合車輛需求也在不斷成長,這有助於節省採購預算和消防站用地面積。森林消防響應車輛還配備了可在行駛過程中供水的輔助水泵,這在火勢迅速蔓延的現場至關重要。由於美國聯邦航空管理局 (FAA) 第 139 部分標準對加速和泡沫供應提出了嚴格的要求,機場消防車 (ARFF) 的價格仍然居高不下。預計在預測期內,技術創新將推動消防車市佔率成長至三分之一以上。

到2025年,住宅和商業消防設備將佔消防車市場銷售額的56.90%,成為消防車市場中最大的單一應用領域。人口密集城區強制推行的消防服務訂單。

同時,隨著氣候變遷導致火災季節更加嚴重且持續時間更長,野火消防領域正以7.86%的複合年成長率快速成長。車輛設計正不斷改進,包括提高離地間隙、加固底盤以及配備泵送滾動功能,使消防人員能夠不間斷地撲滅逼近的火勢。與野火緩解計畫相關的聯邦撥款,即使在地方政府收入下降的情況下,也有助於維持採購預算。工業應用領域對耐化學腐蝕密封件和B類危險品運輸的需求日益成長,而機場則繼續根據美國聯邦航空管理局(FAA)的無氟泡沫過渡舉措對機場消防救援車輛(ARFF)提出需求。這些變化表明,多樣化的風險狀況正在影響消防車市場的演變。

區域分析

北美地區將佔2025年總收入的33.95%,並受惠於成熟的緊急服務資金和先進技術測試。該地區將佔據早期電動消防車應用的大部分佔有率,從而鞏固其作為未來全球應用模式標竿的地位。持續的聯邦基礎設施項目為更換車齡超過20年的車輛提供補貼,從而維持了永續的訂單來源。

亞太地區以7.72%的複合年成長率快速發展,中國、印度和東南亞等地的市政消防服務正迅速擴張,以滿足都市化。中國各地城市正撥出專款,投資購置專為高密度高層建築區域設計的消防車和高空作業平台,並擴大消防局網路。印度定期進行競標,優先考慮本地組裝,鼓勵全球整車製造商與本土底盤供應商成立合資企業。市場對電池驅動商用車的需求日益成長,呈現出強勁的複合年成長率,這表明一旦充電基礎設施成熟,零排放消防車市場潛力巨大。

儘管歐洲市場規模依然龐大,但其成長速度正在放緩,這主要受環保法規和車輛更新換代需求的驅動,而非車輛本身的擴張。更嚴格的排放氣體法規和NFPA合規標準正在影響採購標準,推動歐6引擎和混合動力系統的普及。中東和非洲地區的訂單穩定,這與城市擴張和大型企劃密切相關;而南美地區的需求則受到宏觀經濟波動的抑制。這些區域趨勢凸顯了支撐消防車市場的地理多樣性。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 嚴格的全球和地方消防安全法規

- 野火發生頻率和嚴重性增加

- 擴大電動消防車的使用範圍

- 歐洲快速更換老舊市政車隊

- 都市區高層建築的增加推動了對高空作業車輛的需求。

- 物聯網遠端資訊處理整合輔助車隊最佳化

- 市場限制

- 下一代(電動車/混合動力車)平台的初始成本很高

- 半導體和底盤供應鏈中斷

- 熟練的緊急車輛駕駛員短缺

- 新興國家地方政府面臨嚴峻的預算情勢

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按類型

- 泵浦車

- 油船

- 救援車輛

- 高空作業平台/平台車

- 多功能模組化卡車

- 森林消防車

- 機場緊急應變車輛(ARFF)

- 透過使用

- 住宅和商業

- 工業和製造業

- 飛機場

- 軍隊

- 森林火災/森林火災

- 透過推進力

- 內燃機(ICE)

- 混合

- 電池電動車

- 燃料電池電動車

- 最終用戶

- 市政消防部門

- 工業設施消防隊

- 機場管理局

- 國防/軍事

- 合約和私人消防服務

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 亞太其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 埃及

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Rosenbauer International AG

- Oshkosh Corporation(Pierce)

- REV Group

- Morita Holdings Corporation

- Magirus GmbH

- WS Darley & Co.

- KME(Kovatch Mobile Equipment)

- Sutphen Corporation

- Gimaex GmbH

- Albert Ziegler GmbH

- Bronto Skylift Oy

- NAFFCO

- Emergency One UK Ltd

- Weihai Guangtai

- Iturri Group

- Zhongtian Heavy Industry

- Sides SA

- BAI Brescia Antincendi International

- Fouts Bros Fire Equipment

- Alexis Fire Equipment

第7章 市場機會與未來展望

The Fire Truck Market is expected to grow from USD 10.17 billion in 2025 to USD 10.94 billion in 2026 and is forecast to reach USD 15.74 billion by 2031 at 7.56% CAGR over 2026-2031.

Fleet replacement cycles, electrification momentum, and climate-driven wildfire risk are combining to lift procurement budgets despite lingering supply-chain bottlenecks. Extended order lead times of 18-33 months are prompting departments to modernize maintenance programs while they wait for new deliveries. Yet, the fire truck market continues to absorb higher unit prices as safety and performance features become non-negotiable. Battery-electric models are moving from pilot to production status in North America and Europe, supported by clean-fleet mandates and measurable savings in fuel and maintenance outlays. Meanwhile, an increase in large-scale wildfire incidents stimulates demand for specialized wildland configurations, and consolidated OEM power is drawing heightened regulatory scrutiny in the United States.

Global Fire Truck Market Trends and Insights

Stringent global & regional fire-safety regulations

The new NFPA 1900 standard unifies previous apparatus rules and introduces mandatory rear-view cameras, LED lighting and electric-vehicle guidance. By shifting from prescriptive checklists toward performance-based criteria, regulators give OEMs room to innovate while still elevating baseline safety. Harmonized requirements also support cross-border apparatus deployment, a benefit for manufacturers with global logistics footprints. Compliance costs, however, are accelerating consolidation among smaller builders, reinforcing the high-concentration profile of the fire truck market.

Rising frequency & severity of wildfires

U.S. wildfire acreage hit 7.7 million acres in 2024, outpacing the 10-year average despite fewer total incidents. Larger, more intense events drive orders for Type 1 Wildland-Urban Interface engines with auxiliary pumps that operate while the vehicle is moving. Federal and state grants aimed at wildfire readiness funnel capital into specialized equipment, keeping demand insulated from municipal budget cycles. The extended season now covers nearly the full calendar year, requiring departments to maintain year-round readiness and boosting the baseline for apparatus utilization.

High upfront cost of next-gen platforms

An electric pumper such as the RTX lists close to a million dollar, roughly double a comparable diesel engine. While operational savings improve total cost of ownership, the initial capital hurdle delays adoption for volunteer and rural departments. Grant programs partially offset costs-Boulder secured a decent amount in external funding for its second electric unit-but financing gaps persist outside well-funded metros. Battery costs are falling yet are unlikely to reach parity with diesel until production runs scale meaningfully after 2027. This two-tier dynamic slows the transition in developing regions, restraining global fire truck market growth in the near term.

Other drivers and restraints analyzed in the detailed report include:

- Growing adoption of electric fire trucks

- Rapid replacement of ageing municipal fleets in Europe

- Semiconductor & chassis supply-chain disruptions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The pumper segment held 36.28% of the fire truck market in 2025 and is set to advance at a 7.62% CAGR to 2031. Pumper evolution adds compressed-air foam systems and modular bodywork, giving departments multi-purpose capability. Segment revenue also benefits from early electrification, with Rosenbauer's RTX platform offering identical pump-rating performance to diesel models. Tankers remain indispensable where hydrant networks are sparse, and ladder platforms satisfy growing urban skylines, including Bronto Skylift's 230-foot reach that covers 20-story buildings.

Modern rescue units embed hydraulic extrication tools and battery-powered cutting devices, reducing scene set-up time. Demand is also rising for combination apparatus that blend pumper, tanker and rescue functions to save procurement budgets and station footprints. Wildland trucks add auxiliary pumps that deliver water while the vehicle is moving, a feature vital during fast-moving fires. ARFF vehicles command premium pricing due to FAA Part 139 standards that mandate stringent acceleration and foam-delivery benchmarks. With incremental innovation, the pumper's share of the fire truck market is likely to remain above one-third through the forecast horizon.

Residential & commercial protection accounted for 56.90% of 2025 revenues, making it the largest single application inside the fire truck market. Fire service mandates for dense urban cores keep order flow steady, and new building codes continue to shift equipment needs toward higher pump capacity and integrated decontamination systems.

Wildland & forestry, however, is expanding at 7.86% CAGR as climate patterns intensify severity and length of fire seasons. Vehicle designs incorporate greater ground clearance, reinforced underbodies and pump-and-roll capacity so crews can attack advancing flames without stopping. Federal grants tied to wildfire mitigation programs sustain procurement budgets even during municipal revenue downturns. Industrial applications demand chemical-proof seals and fire suppression agents compatible with class B hazards, while airports continue ordering ARFF units compliant with fluorine-free foam requirements set by the FAA's ongoing F3 transition initiative. Taken together, these shifts demonstrate how diverse risk profiles shape the evolving fire truck market.

The Fire Truck Market Report is Segmented by Type (Pumpers, Tankers, Rescue Trucks, and More), Application (Residential and Commercial, Airports, Military, and More), Propulsion (Internal Combustion Engine (ICE), Hybrid, and More), End-User (Municipal Fire Departments and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 33.95% of 2025 revenue, benefiting from mature emergency-services funding and advanced technology trials. The region hosts the bulk of early electric deployments, reinforcing its role as a bellwether for future global adoption patterns. Ongoing federal infrastructure programs provide supplemental funding to replace apparatus older than 20 years, keeping the order pipeline resilient.

Asia-Pacific, recording a 7.72% CAGR, is rapidly scaling municipal fire services to match urbanization in China, India and Southeast Asia. China's tier-2 and tier-3 cities allocate capital to expand station networks and invest in pumpers and aerials designed for dense, high-rise districts. India issues regular tenders that prioritize local assembly, encouraging joint ventures between global OEMs and domestic chassis suppliers. Emerging interest in battery-electric commercial vehicles at a robust CAGR hints at a budding market for zero-emission apparatus once charging infrastructure matures.

Europe remains a large yet slower-growing arena focused on green compliance and replacement rather than fleet expansion. Tightening emissions rules and NFPA-aligned standards influence procurement criteria, stimulating uptake of Euro-VI engines and hybrid drives. The Middle East & Africa register steady orders linked to expanding urban footprints and industrial megaprojects, while South America's demand is tempered by macroeconomic volatility. Collectively, these regional trajectories underscore the geographic diversity underpinning the fire truck market.

- Rosenbauer International AG

- Oshkosh Corporation (Pierce)

- REV Group

- Morita Holdings Corporation

- Magirus GmbH

- W.S. Darley & Co.

- KME (Kovatch Mobile Equipment)

- Sutphen Corporation

- Gimaex GmbH

- Albert Ziegler GmbH

- Bronto Skylift Oy

- NAFFCO

- Emergency One UK Ltd

- Weihai Guangtai

- Iturri Group

- Zhongtian Heavy Industry

- Sides S.A.

- BAI Brescia Antincendi International

- Fouts Bros Fire Equipment

- Alexis Fire Equipment

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent global & regional fire-safety regulations

- 4.2.2 Rising frequency & severity of wildfires

- 4.2.3 Growing adoption of electric fire trucks

- 4.2.4 Rapid replacement of ageing municipal fleets in Europe

- 4.2.5 Urban high-rise construction boosting aerial truck demand

- 4.2.6 Integration of IoT-telematics for fleet optimisation

- 4.3 Market Restraints

- 4.3.1 High upfront cost of next-gen (EV / hybrid) platforms

- 4.3.2 Semiconductor & chassis supply-chain disruptions

- 4.3.3 Shortage of skilled emergency-vehicle operators

- 4.3.4 Tight municipal budgets in developing economies

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Type

- 5.1.1 Pumpers

- 5.1.2 Tankers

- 5.1.3 Rescue Trucks

- 5.1.4 Aerial / Platform Trucks

- 5.1.5 Multi-tasking Modular Trucks

- 5.1.6 Wildland Fire Trucks

- 5.1.7 Airport Crash Tender (ARFF)

- 5.2 By Application

- 5.2.1 Residential & Commercial

- 5.2.2 Industrial & Manufacturing

- 5.2.3 Airports

- 5.2.4 Military

- 5.2.5 Wildland & Forestry

- 5.3 By Propulsion

- 5.3.1 Internal Combustion Engine (ICE)

- 5.3.2 Hybrid

- 5.3.3 Battery Electric

- 5.3.4 Fuel-Cell Electric

- 5.4 By End-User

- 5.4.1 Municipal Fire Departments

- 5.4.2 Industrial Facility Brigades

- 5.4.3 Airport Authorities

- 5.4.4 Defense & Military

- 5.4.5 Contract & Private Fire Services

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Egypt

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Rosenbauer International AG

- 6.4.2 Oshkosh Corporation (Pierce)

- 6.4.3 REV Group

- 6.4.4 Morita Holdings Corporation

- 6.4.5 Magirus GmbH

- 6.4.6 W.S. Darley & Co.

- 6.4.7 KME (Kovatch Mobile Equipment)

- 6.4.8 Sutphen Corporation

- 6.4.9 Gimaex GmbH

- 6.4.10 Albert Ziegler GmbH

- 6.4.11 Bronto Skylift Oy

- 6.4.12 NAFFCO

- 6.4.13 Emergency One UK Ltd

- 6.4.14 Weihai Guangtai

- 6.4.15 Iturri Group

- 6.4.16 Zhongtian Heavy Industry

- 6.4.17 Sides S.A.

- 6.4.18 BAI Brescia Antincendi International

- 6.4.19 Fouts Bros Fire Equipment

- 6.4.20 Alexis Fire Equipment

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

消防車市場:2026-2032年全球市場預測(依產品類型、動力系統、應用和銷售管道分類)

消防車市場:2026-2032年全球市場預測(依產品類型、動力系統、應用和銷售管道分類) 2026年全球消防車市場報告消防車輛市場:依車輛類型、推進系統、驅動系統和應用分類-2026-2032年全球市場預測

2026年全球消防車市場報告消防車輛市場:依車輛類型、推進系統、驅動系統和應用分類-2026-2032年全球市場預測 電動緊急應變車輛市場:策略性洞察與預測(2026-2031年)空中消防車輛市場:按類型、動力類型、安裝類型、最終用戶、應用和銷售管道,全球預測,2026-2032年緊急應變指揮車輛市場(依車輛類型、動力系統、傳動系統和應用分類)-全球預測,2026-2032年全球消防車市場規模、佔有率、趨勢和成長分析報告(2026-2034年)2026年全球消防車行動數據終端(MDT)顯示器市場報告全球緊急排水車輛市場按技術、動力來源、車輛尺寸、銷售管道、應用及最終用戶分類,2026-2032年預測

電動緊急應變車輛市場:策略性洞察與預測(2026-2031年)空中消防車輛市場:按類型、動力類型、安裝類型、最終用戶、應用和銷售管道,全球預測,2026-2032年緊急應變指揮車輛市場(依車輛類型、動力系統、傳動系統和應用分類)-全球預測,2026-2032年全球消防車市場規模、佔有率、趨勢和成長分析報告(2026-2034年)2026年全球消防車行動數據終端(MDT)顯示器市場報告全球緊急排水車輛市場按技術、動力來源、車輛尺寸、銷售管道、應用及最終用戶分類,2026-2032年預測 消防車市場機會、成長要素、產業趨勢分析及2026年至2035年預測

消防車市場機會、成長要素、產業趨勢分析及2026年至2035年預測