|

市場調查報告書

商品編碼

1910536

照明控制系統:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Lighting Control System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

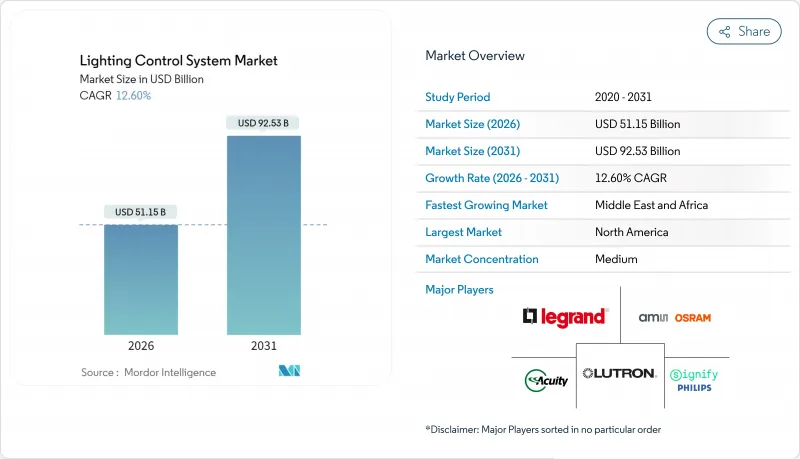

照明控制系統市場預計將從 2025 年的 454.3 億美元成長到 2026 年的 511.5 億美元,預計到 2031 年將達到 925.3 億美元,2026 年至 2031 年的複合年成長率為 12.6%。

這種加速成長反映了強制性的節能要求、智慧城市計畫的激增以及物聯網賦能的建築自動化的廣泛應用,這些技術將照明設備轉化為資料來源。各國政府目前正將自動調光、日光調光和人員佔用偵測功能納入建築規範,從而創造了不可或缺的需求。 LED組件價格的下降縮短了投資回收期,使得即使對於小規模的設施,全面的控制系統也變得經濟可行。無線網狀網路通訊協定的廣泛應用降低了安裝的複雜性,為2020年之前建造的現有設施的維修提供了更多機會。然而,日益嚴重的網路安全威脅和持續的半導體供應瓶頸給供應商和設施業主帶來了短期營運風險。

全球照明控制系統市場趨勢與洞察

節能照明系統的需求日益成長

世界各地的設施都在尋求透過將LED與智慧控制系統結合來降低營運成本和碳排放,與傳統螢光具相比,LED照明能耗最多可降低80%。已驗證的工業計劃表明,安裝後12個月內照明能耗降低了87%,證實即使對於大型工廠,也能快速收回成本。人員佔用偵測、自然光利用和定時功能可實現持續最佳化,而不會影響業務流程,即使在能源成本不斷上漲的環境下,也能促進資本投資核准。業主們欣喜地看到,許多計劃在一個財政年度內即可收回成本,這有助於在其他建設支出受到嚴格審查的情況下維持市場需求。

嚴格的建築能源標準和綠色認證要求

2021年國際節能規範(IECC 2021)強制要求商業建築配備自動調光和日光響應控制系統,使其從可選升級變為強制性要求。加州第24號法規(2022年)提倡對4kW以上的計劃採用需量反應調光,確保幾乎所有大型建築都實施控制系統。 LEED認證體系對先進的照明控制系統給予加分,使監管壓力與資本市場對符合ESG(環境、社會和治理)標準的資產的偏好相一致。由於合規性已成為不可協商的要求,照明控制系統市場獲得了一個能夠抵禦宏觀經濟波動的穩健成長平台。

較高的初始實施和整合成本

一套完整的控制系統維修所需的資金是更換基本LED燈的兩到三倍,這對中小企業構成了障礙。複雜的計劃需要熟練的試運行技術人員,而人才短缺推高了人事費用,尤其是在成熟地區以外的地區。即使是每年節省100,831美元的知名飯店維修也需要大量資金,投資回收期長達1.62年,凸顯了中小企業面臨的資金籌措障礙。由於能源融資的匱乏,新興市場仍是最大的資金籌措缺口地區。

細分市場分析

到2025年,硬體將佔總收入的56.80%,因為驅動程式、感測器和閘道器是任何智慧升級的基礎。服務業務將以12.83%的複合年成長率快速成長,因為大規模部署需要設計諮詢、現場試運行和定期最佳化。基於人工智慧的分析需要持續調整,預計將進一步擴大照明控制系統服務市場規模。諸如能源管理計劃(EMC)藍牙Mesh計劃(在43個地區部署了3685個控制器)等全球部署案例,展現了服務的複雜性和持續收入潛力。

專業服務能夠確保長期合約的簽訂,將一次性資本計劃轉化為可預測的現金流。韌體更新、故障分析和能源報告等服務擴大被納入企業外包的託管服務合約中。因此,硬體供應商正在將生命週期合約打包,推動照明控制系統市場從單純的零件銷售模式轉向解決方案生態系統。這種策略轉變提高了缺乏設計和支援資源的企業的進入門檻。

到2025年,有線通訊協定將保持63.40%的市場佔有率,這主要得益於其抗電磁干擾能力和穩定的延遲,而這些特性對於關鍵任務型工廠至關重要。醫院和資料中心等網路停機時間不可接受的場所,將繼續對採用有線DALI-2安裝的照明控制系統保持強勁的需求。工程師重視專用佈線的確定性性能和固有的物理安全性。

無線部署正以14.85%的複合年成長率迅速縮小差距。藍牙Mesh提供自癒功能和基於智慧型手機的性能驗證,顯著降低了人事費用。整合到Matter生態系統後,住宅和商業設備可以在通用的管理平台下協同工作,從而加速規範制定者的採用。計畫於2026年推出的Thread 1.4升級將增加邊界路由器的柔軟性,使設施管理團隊無需重新佈線即可擴展網路。在停機時間至關重要的環境中,例如歷史建築和開放式零售場所,減少中斷是一項極具吸引力的優勢。

照明控制系統市場按產品類型(硬體、軟體、服務)、通訊協定(有線、無線)、安裝類型(新建、維修)、應用領域(室外、室內)和地區進行細分。市場預測以美元計價。

區域分析

預計到2025年,北美地區的市佔率將達到34.10%,這主要得益於嚴格的節能標準和智慧城市建設的領先。照明控制系統市場正受益於聯邦政府的節能計畫和稅收優惠政策,這些政策加速了投資回報。公共產業對感測器組件的補貼進一步提升了商業房地產維修的經濟效益。加拿大各省正在效仿美國的標準,而墨西哥的工業走廊則將照明控制系統整合到加工廠的擴建項目中,以最大限度地降低營運成本。

歐洲保持強勁勢頭,並制定了2030年實現脫碳的宏偉目標。德國、法國和英國已將智慧照明納入公共部門採購規則。歐盟分類揭露要求業主證明其能源強度降低,從而引導資金流向配備豐富感測器的升級改造專案。 DALI-2 和新興的 ETSI EN 303 645 安全框架的標準化工作正在降低多供應商部署的風險,並促進單一市場內的普及應用。

預計中東和非洲地區將實現最快成長,到2031年複合年成長率將達到12.74%。沙烏地阿拉伯和阿拉伯聯合大公國正在建造的特大城市從一開始就將智慧照明系統納入總體規劃。儘管石油收入波動,但政府對智慧基礎設施的預算將確保計劃儲備充足。在撒哈拉以南非洲,電網不穩定促使人們採用電壓下降時自動調暗負載的感測器,從而保護資產並延長燈具的使用壽命。開發銀行的融資支援將有助於消除初期成本障礙,確保銷售持續成長。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 節能照明系統的需求日益成長

- 嚴格的建築能源標準和綠色認證要求

- LED價格快速下降導致投資報酬率提高。

- 利用自適應路燈進行智慧城市規劃

- ESG掛鉤融資加速智慧維修

- 為Li-Fi部署做好準備,將開啟新的收入來源。

- 市場限制

- 較高的初始實施和整合成本

- 多廠商環境下的互通性挑戰

- 網路安全與資料隱私風險

- 合格試運行專業人員短缺

- 供應鏈分析

- 監管環境

- 技術展望(物聯網邊緣控制、人工智慧、Li-Fi)

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 對影響市場的宏觀經濟因素進行評估

第5章 市場規模與成長預測

- 報價

- 硬體

- LED驅動器

- 感應器

- 開關和調光器

- 繼電器單元

- 閘道器和控制面板

- 軟體

- 服務

- 硬體

- 透過通訊協定

- 有線

- 無線的

- 按安裝類型

- 新建工程

- 維修

- 透過使用

- 室內的

- 銷售辦事處

- 工業和倉儲

- 住宅

- 飯店及休閒

- 其他

- 戶外

- 道路和街道

- 建築和建築幕牆

- 體育場館

- 其他

- 室內的

- 地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲地區

- 埃及

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 市佔率分析

- 策略趨勢

- 公司簡介

- Signify(Philips Lighting)

- Acuity Brands

- Legrand

- Lutron Electronics

- ams OSRAM

- Schneider Electric

- Eaton(Cooper Lighting)

- Hubbell Lighting

- Honeywell

- Cisco Systems

- Siemens(Enlighted)

- Delta Electronics

- Panasonic

- Zumtobel Group

- Helvar

- Synapse Wireless

- WAGO

- Cree Lighting

- Leviton Manufacturing

- Digital Lumens

- ABB

第7章 市場機會與未來展望

The lighting control system market is expected to grow from USD 45.43 billion in 2025 to USD 51.15 billion in 2026 and is forecast to reach USD 92.53 billion by 2031 at 12.6% CAGR over 2026-2031.

Accelerated growth reflects mandated energy-efficiency requirements, the spread of smart city programs, and wider use of IoT-enabled building automation that turns luminaires into data sources. Governments now anchor automatic shut-off, daylight-responsive dimming, and occupancy sensing in building standards, which creates non-discretionary demand. Price erosion in LED components has shortened payback periods, making comprehensive controls economically viable even for smaller facilities. Wireless mesh protocols have reduced installation complexity, opening retrofit opportunities in stock built before 2020. At the same time, escalating cybersecurity threats and lingering semiconductor supply bottlenecks present near-term operational risks for suppliers and facility owners.

Global Lighting Control System Market Trends and Insights

Growing Demand for Energy-Efficient Lighting Systems

Facilities worldwide pursue lower operating costs and carbon footprints by pairing LEDs with intelligent controls that trim lighting energy as much as 80% compared with legacy fluorescent installations. Documented industrial projects have reached 87% lighting-energy savings in the first twelve months, underscoring quick payback even in large plants. Occupancy sensing, daylight harvesting, and scheduling allow continuous optimisation without impacting workflow, which makes capital approval easier when utility prices keep rising. Building owners value that many projects now return cash within a single fiscal year, creating momentum that sustains demand when other construction outlays are under scrutiny.

Stringent Building-Energy Codes and Green Certification Mandates

The International Energy Conservation Code 2021 requires automatic shut-off and daylight-responsive controls in commercial spaces, converting optional upgrades into mandatory scope. California Title 24 (2022) pushes demand-responsive dimming on projects above 4 kW, guaranteeing control deployment in virtually every large build. LEED rating systems award points for advanced lighting controls, aligning regulatory pressure with capital markets that now prioritise ESG-ready assets. Because compliance is non-negotiable, the lighting control system market gains a defensive growth pillar that softens macro-economic swings.

High Upfront Installation and Integration Cost

Comprehensive control retrofits still command two- to three-times the capital of basic LED lamp swaps, which discourages smaller businesses. Complex projects rely on skilled commissioning engineers whose limited availability inflates labour fees, especially outside mature regions.Even high-profile hotel retrofits that now yield USD 100,831 annual savings required sizeable capital and a 1.62-year payback, highlighting the cash hurdle that smaller enterprises face. Financing gaps remain widest in emerging markets where energy loans are scarce.

Other drivers and restraints analyzed in the detailed report include:

- Rapid LED Price Erosion Expanding ROI

- Smart-City Programs Using Adaptive Street Lighting

- Interoperability Issues Across Multi-Vendor Ecosystems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware captured 56.80% revenue in 2025 as drivers, sensors, and gateways form the backbone of any intelligent upgrade. Services are poised for the fastest 12.83% CAGR because every significant deployment requires design consultation, site commissioning, and periodic optimisation. The lighting control system market size for services is projected to gain momentum as AI-based analytics demand continuous tuning. Global roll-outs such as Energy Management Collaborative's Bluetooth Mesh project, which involved 3,685 controllers in 43 areas, illustrate service-heavy complexity and recurring revenue potential.

Professional services secure long-term contracts that convert one-time capital projects into predictable cash flows. Firmware updates, fault analytics, and energy reporting increasingly fall under managed-service agreements that enterprises outsource. As a result, hardware vendors bundle lifecycle contracts, pushing the lighting control system market toward solution ecosystems rather than component sales. This strategic shift raises entry barriers for firms that lack design and support resources.

Wired protocols preserved 63.40% share in 2025, valued for EMI immunity and stable latency that mission-critical factories demand. The lighting control system market size tied to wired DALI-2 installations remains considerable among hospitals and data centres where network downtime is unacceptable. Engineers favour deterministic performance and inherent physical security of dedicated cabling.

Wireless deployments are closing the gap at a 14.85% CAGR. Bluetooth Mesh offers self-healing paths and smartphone-based commissioning that slash labour costs. Integration into the Matter ecosystem aligns residential and commercial devices under common management shells, which accelerates specifier acceptance. Thread 1.4 upgrades planned by 2026 will add border-router flexibility, allowing facility teams to scale networks without rewiring. Reduced disruption is compelling for heritage sites and live retail stores where shutdown time is limited.

Lighting Control System Market is Segmented by Offering (Hardware, Software, Services), Communication Protocol (Wired, Wireless), Installation Type (New Construction, Retrofit), Application (Outdoor, Indoor) and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 34.10% revenue in 2025 due to strict energy codes and early smart-city adoption. The lighting control system market benefits from federal efficiency programmes and tax incentives that improve investment payback. Utility rebate schemes covering sensor packages further sweeten economics for commercial retrofits. Canadian provinces mirror United States standards, while Mexico's industrial corridors integrate lighting controls into maquiladora expansions to minimise operational spend.

Europe maintains momentum with firm decarbonisation targets set for 2030. Germany, France, and the United Kingdom embed intelligent lighting in public-sector procurement rules. EU taxonomy disclosures oblige property owners to prove energy intensity reductions, which steers capital toward sensor-rich upgrades. Standardisation efforts through DALI-2 and the emerging ETSI EN 303 645 security framework make multi-vendor deployments less risky, reinforcing uptake across the single market.

The Middle East and Africa post the fastest 12.74% CAGR through 2031. Mega-cities under construction in Saudi Arabia and the UAE incorporate control-ready luminaires into master plans from the start. Government budgets earmarked for smart infrastructure keep project pipelines robust even when oil revenues fluctuate. In sub-Saharan Africa, grid instability motivates adoption of sensors that dim loads during voltage dips, protecting equipment and extending luminaire life. Financing backed by development banks helps bridge initial cost hurdles, ensuring sustained volume growth.

- Signify (Philips Lighting)

- Acuity Brands

- Legrand

- Lutron Electronics

- ams OSRAM

- Schneider Electric

- Eaton (Cooper Lighting)

- Hubbell Lighting

- Honeywell

- Cisco Systems

- Siemens (Enlighted)

- Delta Electronics

- Panasonic

- Zumtobel Group

- Helvar

- Synapse Wireless

- WAGO

- Cree Lighting

- Leviton Manufacturing

- Digital Lumens

- ABB

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for energy-efficient lighting systems

- 4.2.2 Stringent building-energy codes and green certification mandates

- 4.2.3 Rapid LED price erosion expanding ROI

- 4.2.4 Smart-city programs using adaptive street lighting

- 4.2.5 ESG-linked finance accelerating smart retrofits

- 4.2.6 Li-Fi readiness unlocking new revenue streams

- 4.3 Market Restraints

- 4.3.1 High upfront installation and integration cost

- 4.3.2 Interoperability issues across multi-vendor ecosystems

- 4.3.3 Cyber-security and data-privacy risks

- 4.3.4 Shortage of qualified commissioning professionals

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook (IoT-edge controls, AI, Li-Fi)

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assesment of Macroeconomic Factors on the market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Hardware

- 5.1.1.1 LED Drivers

- 5.1.1.2 Sensors

- 5.1.1.3 Switches and Dimmers

- 5.1.1.4 Relay Units

- 5.1.1.5 Gateways and Control Panels

- 5.1.2 Software

- 5.1.3 Services

- 5.1.1 Hardware

- 5.2 By Communication Protocol

- 5.2.1 Wired

- 5.2.2 Wireless

- 5.3 By Installation Type

- 5.3.1 New Construction

- 5.3.2 Retrofit

- 5.4 By Application

- 5.4.1 Indoor

- 5.4.1.1 Commercial Offices

- 5.4.1.2 Industrial and Warehousing

- 5.4.1.3 Residential

- 5.4.1.4 Hospitality and Leisure

- 5.4.1.5 Others

- 5.4.2 Outdoor

- 5.4.2.1 Roadway and Street

- 5.4.2.2 Architectural and Facade

- 5.4.2.3 Sports and Stadium

- 5.4.2.4 Others

- 5.4.1 Indoor

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Southeast Asia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.5.2.5 Egypt

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Strategic Moves

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Signify (Philips Lighting)

- 6.4.2 Acuity Brands

- 6.4.3 Legrand

- 6.4.4 Lutron Electronics

- 6.4.5 ams OSRAM

- 6.4.6 Schneider Electric

- 6.4.7 Eaton (Cooper Lighting)

- 6.4.8 Hubbell Lighting

- 6.4.9 Honeywell

- 6.4.10 Cisco Systems

- 6.4.11 Siemens (Enlighted)

- 6.4.12 Delta Electronics

- 6.4.13 Panasonic

- 6.4.14 Zumtobel Group

- 6.4.15 Helvar

- 6.4.16 Synapse Wireless

- 6.4.17 WAGO

- 6.4.18 Cree Lighting

- 6.4.19 Leviton Manufacturing

- 6.4.20 Digital Lumens

- 6.4.21 ABB

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

LED照明組件市場預測至2034年:全球產品類型、組件類型、安裝類型、分銷管道、技術、應用、最終用戶和地區分析

LED照明組件市場預測至2034年:全球產品類型、組件類型、安裝類型、分銷管道、技術、應用、最終用戶和地區分析 全球照明燈具及照明控制市場規模、佔有率、趨勢及成長分析報告(2026-2034)

全球照明燈具及照明控制市場規模、佔有率、趨勢及成長分析報告(2026-2034) 2026年全球工廠照明市場報告2026年全球照明控制系統市場報告

2026年全球工廠照明市場報告2026年全球照明控制系統市場報告 劇院主機市場按主機類型、控制技術、安裝類型、應用、最終用戶和配銷通路分類 - 全球預測 2026-2032

劇院主機市場按主機類型、控制技術、安裝類型、應用、最終用戶和配銷通路分類 - 全球預測 2026-2032 照明控制系統市場規模、佔有率及成長分析(按組件、類型、應用、最終用戶和地區分類)-2026-2033年產業預測

照明控制系統市場規模、佔有率及成長分析(按組件、類型、應用、最終用戶和地區分類)-2026-2033年產業預測 調光器市場規模、佔有率和成長分析(按類型、控制通訊協定、應用和地區分類)—2026-2033年產業預測照明控制系統市場預測至2032年:按組件、通訊協定、安裝類型、最終用戶和地區分類的全球分析照明控制市場按產品、技術、控制模式、光源相容性、安裝類型、最終用途和分銷管道分類 - 全球預測 2025-2030

調光器市場規模、佔有率和成長分析(按類型、控制通訊協定、應用和地區分類)—2026-2033年產業預測照明控制系統市場預測至2032年:按組件、通訊協定、安裝類型、最終用戶和地區分類的全球分析照明控制市場按產品、技術、控制模式、光源相容性、安裝類型、最終用途和分銷管道分類 - 全球預測 2025-2030 全球調光器市場:產業分析、規模、佔有率、成長、趨勢、預測(2024-2031)

全球調光器市場:產業分析、規模、佔有率、成長、趨勢、預測(2024-2031)