|

市場調查報告書

商品編碼

1910495

石膏板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Gypsum Board - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

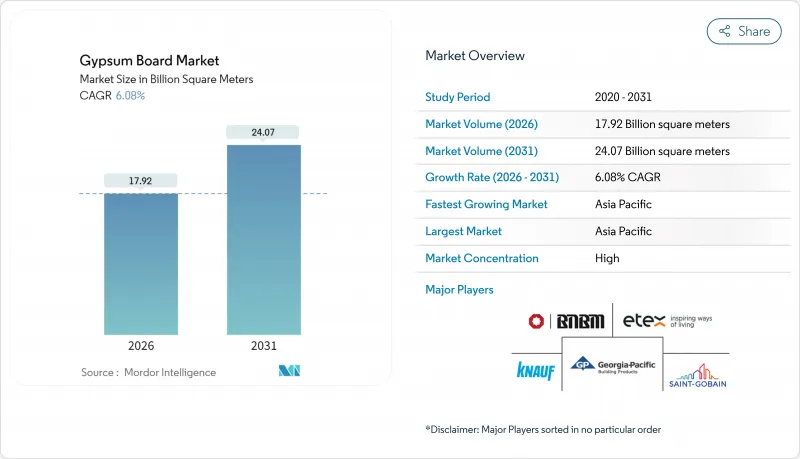

預計到 2026 年,石膏板市場規模將達到 179.2 億平方公尺。

預計從 2025 年的 168.9 億平方公尺成長到 2031 年的 240.7 億平方公尺,2026 年至 2031 年的複合年成長率為 6.08%。

持續的消防安全標準和節能法規支撐著市場需求,而亞太地區的建築熱潮、北美長期存在的住宅短缺以及歐洲日益嚴格的碳排放法規則塑造了競爭格局。德克薩斯州和蒙特婁的蘊藏量擴張計劃表明,製造商如何在成本控制和永續性投資之間取得平衡。同時,輕質預裝飾解決方案的普及有助於承包商緩解勞動力短缺問題,而隨著燃煤電廠的淘汰速度超出預期,再生和合成原料的戰略重要性日益凸顯。纖維水泥板在潮濕地區的擴張使價格保持在合理水平,而大規模的基礎設施更新計劃則持續推動石膏板市場銷售的成長。

全球石膏板市場趨勢與洞察

亞太地區住宅建設激增

快速的都市區化進程正促使開發商轉向高密度住宅,而石膏板系統相比濕抹灰工藝,可縮短室內裝修週期。儘管預計2024年中國水泥總產量將下降10%,但由於開發商專注於加快裝修進度以確保現金流,牆板需求依然強勁。在印度,政府支持的住宅計畫創造了穩定的基礎需求;而在東南亞,石膏因其在學校和交通樞紐等大型計劃中久經考驗的防火性能而被指定使用。全部區域的勞動力短缺也推動了對工廠預製板材的需求,因為這種板材可以減少現場施工。

成熟市場對維修和改造的需求加速成長

預計到2025年,美國房屋維修支出將達到5,090億美元,扭轉先前連續兩年下滑的局面。由於美國40%的住宅建於1970年以前,牆壁材料更換以及日益嚴格的防火和隔熱標準直接推動了石膏板的需求。住宅平均花費4,700美元進行室內維修,其中防黴防潮板材位列購買清單之首。歐盟類似的維修規定也推動了高性能隔熱隔音板材的訂單。這些趨勢即使在經濟放緩時期也能維持石膏板市場的穩定需求。

天然石膏和能源價格波動

2024年,美國石膏礦產量達2,200萬噸,由於開採深度和運輸距離的不同,單位成本有顯著差異。煅燒過程嚴重依賴天然氣,因此燃料價格波動會影響石膏板價格。隨著燃煤發電廠的退役,合成石膏供應減少,工廠被迫依賴更遠地區的礦床,增加了運輸成本和成本風險。雖然節能窯爐和區域倉儲中心在一定程度上緩解了這種影響,但短期內投入成本的波動仍將限制石膏板市場的成長。

細分市場分析

到 2025 年,牆板將保持石膏板市場 59.62% 的佔有率,這主要得益於其在住宅室內裝飾中的普遍接受度,而成本和建築規範的合規性是推動規格製定的主要因素。同時,預計到 2031 年,塗漆面板的複合年成長率將達到 7.39%,比整個石膏板市場的成長率高出 1 個百分點以上。

目前,高階石膏板市場主要由PURPLE XP等品牌主導,這些品牌的石膏板具有更強的防黴、防潮和抗衝擊性能。雖然它們的價格比普通X型石膏板高出20-30%,但由於停工成本高昂,因此常用於廚房、浴室和醫療走廊等場所。製造商正將這些特性與工廠預塗漆相結合,以獲取高利潤。隨著安裝人員對「可直接塗漆」的交付需求日益成長,預塗漆石膏板預計將擴大其在石膏板市場的佔有率。

石膏板市場報告按產品類型(牆板、天花板、預塗板)、原料(天然石膏、合成(脫硫)石膏、再生石膏)、應用領域(住宅、商業、公共、工業)和地區(亞太、北美、歐洲、南美、中東和非洲)進行細分。市場預測以銷售量(單位)為基礎。

區域分析

2025年,亞太地區佔全球出貨量的46.10%,主要得益於中國龐大的房地產市場需求和印度的「全民住宅」計畫。預計到2031年,該地區的複合年成長率將達到7.31%,儘管存在政治和信貸風險的擔憂,但石膏板市場仍將以亞太地區為主要市場。

北美市場代表著由維修需求支撐的穩定局面。歐洲的成長路徑則以監管主導,例如RE2020等舉措,儘管宏觀經濟指標放緩,但仍增強了對碳最佳化設計的需求。這三大區域構成了競爭格局,而南美洲以及中東和非洲地區仍是充滿成長機會的前沿市場,較低的人均滲透率為石膏板市場的未來成長提供了空間。

製造商力求透過環境產品聲明 (EPD) 實現差異化,並經常添加回收成分以滿足競標要求。雖然建築業生產成長速度低於亞太地區,但受 ESG 因素驅動的溢價正在抵消銷售成長放緩的影響,並支撐石膏板市場的收入成長。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 亞太地區住宅建設激增

- 成熟市場對維修和改造的需求加速成長

- 轉向輕質高強度石膏板解決方案

- 政府對防火、隔音和節能建築提供誘因

- 經濟型合成(FGD)石膏的供應狀況

- 市場限制

- 天然石膏和能源價格波動

- 纖維水泥和其他替代板材日益普及

- 由於強制性蘊藏量中和政策,加強了對碳儲備的監測

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 依產品類型

- 牆板

- 帆船板

- 裝飾前板

- 按原料

- 天然石膏

- 合成石膏(FGD)

- 再生石膏

- 透過使用

- 住宅

- 商業的

- 公共利益

- 產業

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 泰國

- 馬來西亞

- 印尼

- 越南

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 土耳其

- 北歐國家

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 奈及利亞

- 埃及

- 卡達

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- BNBM

- Etex Group

- Everest Industries Limited

- Georgia-Pacific Gypsum LLC

- Global Gypsum Board Co LLC(Gypcore)

- Holcim

- Jason New Materials

- Knauf Group

- National Gypsum Services Company

- Osman Group

- PABCO Gypsum

- Saint-Gobain

- Shandong Taihe Dongxin Co.,Ltd

- VANS Gypsum

- Volma

- Winstone Wallboards Limited

- YOSHINO GYPSUM CO.,LTD.

第7章 市場機會與未來展望

Gypsum Board Market size in 2026 is estimated at 17.92 Billion square meters, growing from 2025 value of 16.89 Billion square meters with 2031 projections showing 24.07 Billion square meters, growing at 6.08% CAGR over 2026-2031.

Ongoing fire-safety and energy-efficiency mandates anchor demand, while Asia-Pacific's construction boom, chronic housing shortages in North America, and tightening embodied-carbon rules in Europe shape the competitive field. Capacity expansion projects in Texas and Montreal illustrate how producers balance cost discipline with sustainability investments. Meanwhile, the shift toward lightweight and pre-decorated solutions helps contractors mitigate labor shortages, and recycled or synthetic feedstocks gain strategic importance as coal-powered electricity retires faster than expected. Fiber-cement's encroachment in wet areas keeps pricing rational, yet broad infrastructure renewal programs continue to backstop volume growth across the gypsum board market.

Global Gypsum Board Market Trends and Insights

Surging Residential Construction in APAC

Rapid urban migration pushes developers toward high-density housing, and gypsum board systems help shorten interior fit-out cycles compared with wet plaster. Although China's overall cement output fell 10% in 2024, wallboard volumes remained resilient because developers focused on accelerating finishing work to unlock cash flows. India's government-backed housing schemes add steady baseline demand, while Southeast Asian megaprojects specify gypsum for its proven fire resistance in schools and transit hubs. Labor shortages across the region strengthen the appeal of factory-finished boards that reduce on-site trades.

Accelerating Renovation and Remodeling Wave in Mature Markets

Renovation outlays in the United States climbed to USD 509 billion in 2025, reversing two years of contraction. Forty percent of U.S. dwellings pre-date 1970, so wall replacements align with tighter fire and insulation codes, directly lifting gypsum demand. Homeowners spent an average USD 4,700 on interior upgrades, with mold- and moisture-resistant boards ranking high on shopping lists. Similar retrofit mandates in the EU catalyze orders for high-performance panels that combine thermal and acoustic gains. These dynamics sustain a stable volume base for the gypsum board market during economic slowdowns.

Volatile Natural Gypsum and Energy Prices

Mined gypsum output touched 22 million tons in the United States during 2024, but unit costs varied widely by mine depth and haulage distance. Calcination relies heavily on natural gas, making board pricing sensitive to fuel swings. As decommissioning of coal plants removes synthetic supply, mills draw from deposits located farther afield, inflating freight bills and amplifying cost risk. Energy-efficient kilns and regional warehouse hubs partly soften the blow, yet input volatility still trims the gypsum board market growth trajectory in the near term.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Lightweight and High-Strength Drywall Solutions

- Government Incentives for Fire, Sound, and Energy-Efficient Buildings

- Rising Penetration of Fibre-Cement and Other Panel Alternatives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Wall board retained 59.62% gypsum board market share in 2025, sustained by universal acceptance in residential interiors where cost and code compliance drive specification. Pre-decorated panels, however, are forecast to post 7.39% CAGR to 2031, a speed more than one percentage point above the overall gypsum board market.

Premium segments now favor mold-, moisture- or impact-modified boards such as PURPLE XP, priced at a 20-30% uplift over generic Type X, yet often selected for kitchens, baths, and healthcare corridors where downtime is costly. Manufacturers bundle these attributes with factory coatings to seize higher-margin value capture. As contractors increasingly pursue "paint-ready" delivery, pre-decorated formats are poised to widen their share within the gypsum board market.

The Gypsum Board Report is Segmented by Product Type (Wall Board, Ceiling Board, and Pre-Decorated Board), Raw Material (Natural Gypsum, Synthetic (FGD) Gypsum, and Recycled Gypsum), Application (Residential, Commercial, Institutional, and Industrial), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Units).

Geography Analysis

Asia-Pacific claimed 46.10% of 2025 shipments, thanks to China's massive real-estate backlog and India's Housing for All program. Regional growth at 7.31% CAGR through 2031 ensures the gypsum board market remains volume-weighted to this geography despite political and credit risk clouds.

North America embodies renovation-driven steadiness. Europe's pathway is more regulation-led, as RE2020 and similar frameworks reinforce demand for carbon-optimized designs despite slower macro indicators. Together, the three regions shape the competitive map, while South America, and Middle-East and Africa remain opportunity frontiers where lower per-capita penetration leaves headroom for future gypsum board market growth.

Manufacturers differentiate through environmental product declarations, often bundling recycled content to meet tender prerequisites. Although construction output is flatter than Asia-Pacific, premium ESG-minded pricing offsets slower unit growth, safeguarding revenue expansion inside the gypsum board market.

- BNBM

- Etex Group

- Everest Industries Limited

- Georgia-Pacific Gypsum LLC

- Global Gypsum Board Co LLC (Gypcore)

- Holcim

- Jason New Materials

- Knauf Group

- National Gypsum Services Company

- Osman Group

- PABCO Gypsum

- Saint-Gobain

- Shandong Taihe Dongxin Co.,Ltd

- VANS Gypsum

- Volma

- Winstone Wallboards Limited

- YOSHINO GYPSUM CO.,LTD.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Residential Construction in APAC

- 4.2.2 Accelerating Renovation and Remodeling Wave in Mature Markets

- 4.2.3 Shift Toward Lightweight and High-Strength Drywall Solutions

- 4.2.4 Government Incentives for Fire, Sound, and Energy-Efficient Buildings

- 4.2.5 Cost-Advantaged Synthetic (FGD) Gypsum Availability

- 4.3 Market Restraints

- 4.3.1 Volatile Natural Gypsum and Energy Prices

- 4.3.2 Rising Penetration of Fibre-Cement and Other Panel Alternatives

- 4.3.3 Carbon-Neutral Mandates Raising Embodied-Carbon Scrutiny

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Wall Board

- 5.1.2 Ceiling Board

- 5.1.3 Pre-decorated Board

- 5.2 By Raw Material

- 5.2.1 Natural Gypsum

- 5.2.2 Synthetic (FGD) Gypsum

- 5.2.3 Recycled Gypsum

- 5.3 By Application

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Institutional

- 5.3.4 Industrial

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Thailand

- 5.4.1.6 Malaysia

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Turkey

- 5.4.3.8 Nordics

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Nigeria

- 5.4.5.4 Egypt

- 5.4.5.5 Qatar

- 5.4.5.6 South Africa

- 5.4.5.7 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 BNBM

- 6.4.2 Etex Group

- 6.4.3 Everest Industries Limited

- 6.4.4 Georgia-Pacific Gypsum LLC

- 6.4.5 Global Gypsum Board Co LLC (Gypcore)

- 6.4.6 Holcim

- 6.4.7 Jason New Materials

- 6.4.8 Knauf Group

- 6.4.9 National Gypsum Services Company

- 6.4.10 Osman Group

- 6.4.11 PABCO Gypsum

- 6.4.12 Saint-Gobain

- 6.4.13 Shandong Taihe Dongxin Co.,Ltd

- 6.4.14 VANS Gypsum

- 6.4.15 Volma

- 6.4.16 Winstone Wallboards Limited

- 6.4.17 YOSHINO GYPSUM CO.,LTD.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

石膏板市場:依產品類型、厚度、應用、最終用途及通路分類-2026-2032年全球市場預測石膏板市場:2026-2032年全球市場預測(按產品類型、表面類型、分銷管道、應用、最終用途和用戶類型分類)

石膏板市場:依產品類型、厚度、應用、最終用途及通路分類-2026-2032年全球市場預測石膏板市場:2026-2032年全球市場預測(按產品類型、表面類型、分銷管道、應用、最終用途和用戶類型分類) 2026年全球石膏板懸吊天花板市場報告防水防潮石膏板市場:依產品類型、應用、最終用戶和通路分類-2026-2032年全球預測

2026年全球石膏板懸吊天花板市場報告防水防潮石膏板市場:依產品類型、應用、最終用戶和通路分類-2026-2032年全球預測 石膏板市場規模、佔有率、趨勢和預測:按產品類型、應用和地區分類,2026-2034年

石膏板市場規模、佔有率、趨勢和預測:按產品類型、應用和地區分類,2026-2034年 全球石膏板市場規模、佔有率、趨勢和成長分析報告(2026-2034)日本石膏板市場規模、佔有率、趨勢和預測:按形態、類型、最終用途行業和地區分類,2026-2034年

全球石膏板市場規模、佔有率、趨勢和成長分析報告(2026-2034)日本石膏板市場規模、佔有率、趨勢和預測:按形態、類型、最終用途行業和地區分類,2026-2034年 石膏板市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、形式、最終用戶、地區和競爭格局分類,2021-2031年全球防潮防黴石膏板市場(按產品類型、最終用途、應用、安裝類型和分銷管道分類)預測(2026-2032年)天花板輻射板市場按產品類型、安裝類型、原料、應用、最終用戶產業和分銷管道分類-2026-2032年全球預測

石膏板市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、形式、最終用戶、地區和競爭格局分類,2021-2031年全球防潮防黴石膏板市場(按產品類型、最終用途、應用、安裝類型和分銷管道分類)預測(2026-2032年)天花板輻射板市場按產品類型、安裝類型、原料、應用、最終用戶產業和分銷管道分類-2026-2032年全球預測