|

市場調查報告書

商品編碼

1910480

物理沉澱(PVD)塗層:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Physical Vapor Deposition Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

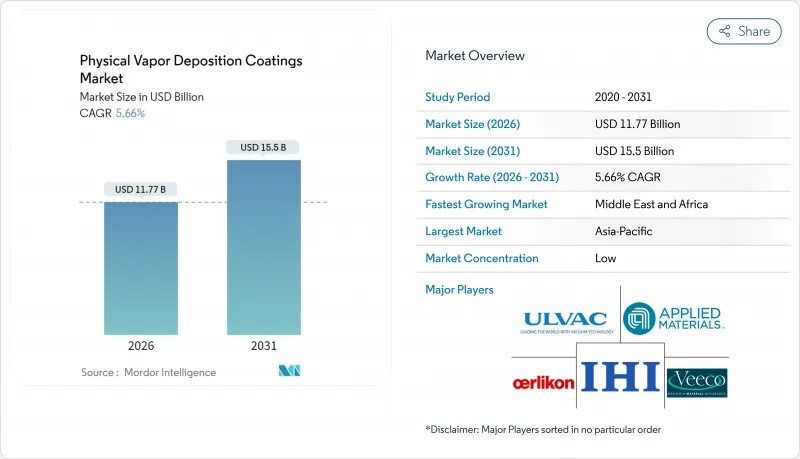

預計到 2026 年,實體沉澱(PVD) 塗層市場規模將達到 117.7 億美元,高於 2025 年的 111.4 億美元。

預計到 2031 年將達到 155 億美元,2026 年至 2031 年的複合年成長率為 5.66%。

這種加速成長反映了7奈米及以下半導體節點需求的激增,以及依賴生物相容性薄膜的微創醫療設備的日益普及。六價鉻電鍍的監管放鬆,加上3D列印零件表面處理的需求,使得物理沉澱(PVD)既成為合規工具,也成為製程賦能技術。該實行技術能夠在金屬、塑膠、玻璃和新興基板上沉積緻密、無缺陷的薄膜,這推動了對新型塗層中心的強勁投資。隨著鈦靶材價格的上漲,以及更多設備製造商競相將高電離濺射源商業化,市場競爭日益激烈。

全球物理沉澱(PVD)塗層市場趨勢及洞察

加速向7奈米以下半導體節點的過渡

向7奈米及以下邏輯和儲存裝置的加速過渡,推動了對亞奈米級精度沉積的隔離層層和種子層的需求激增。應用材料公司提供的設備平台正顯著增加鉬基互連堆疊的採用,以限制極端長寬比的銅擴散。台灣和韓國的大批量部署正在建立超高真空濺射腔、先進鈦和鉭靶材以及原位測量設備的區域供應鏈。隨著製程尺寸的不斷縮小,對公差的要求也越來越高,這促使設備製造商整合高電離濺鍍(HiPIMS)源,從而獲得更高電離度和更緻密的薄膜。包括晶片組和穿透矽通孔的先進封裝技術,進一步推動了對用於3D整合的保形物理沉澱(PVD)製程的投資。

微創醫療設備生產快速成長

隨著對導管植入和整形外科固定裝置的需求加速成長,塗層需求也從簡單的生物相容性發展到抗菌和骨整合能力。磁控濺鍍法製備的550奈米厚鉭薄膜在BMC生物技術測試中實現了39.184牛頓的臨界結合載荷,優於未塗層的鈦結構。美國食品藥物管理局(FDA)的監管核准在製程驗證後帶來了永續的收入,促使美國、德國和愛爾蘭的合約塗層公司增設配備無塵室隔離設施的專用醫療生產線。中國和馬來西亞注重成本的醫療設備原始設備製造商(OEM)擴大將實體沉澱(PVD)製程外包,以滿足全球供應鏈品質審核的要求。

超高真空系統需要高額資本投入

一台12吋叢集式設備的價格可高達500萬美元,這還不包括無塵室建設和設施公用費用。這些資金障礙阻礙了巴西、印尼和撒哈拉以南非洲地區的新進業者,訂單集中在擁有資產折舊免稅額優勢的現有企業手中。 5-7年的投資回收期以及隨著節點尺寸縮小而導致的製程過時風險,都使資金籌措變得複雜。印度和越南的政府獎勵計畫可以部分抵銷資本支出,但銀行協議仍要求主要客戶提供訂單量擔保。

細分市場分析

高功率脈衝磁控濺鍍(HiPIMS)技術電離率超過70%,能夠為切削刀具製備高附著力、高密度的塗層,預計年複合成長率(CAGR)將達到6.92%,成為成長最快的技術。濺鍍技術仍是基礎技術,預計到2025年將維持42.35%的市場佔有率,擴充性涵蓋從微電子到建築玻璃等多個領域。熱沉澱和電子束沉澱在光學塗層領域佔據一定的市場佔有率,而電弧沉澱儘管存在大顆粒沉積的問題,但仍繼續用於耐磨裝飾塗層。隨著汽車原始設備製造商(OEM)將氮化物配方標準化以延長沖壓製作流程中的刀具壽命,HiPIMS物理沉澱(PVD)塗層市場規模預計將穩定成長。

設備製造商正在採用多陰極配置,實現靶材的即時更換,將配方切換時間縮短30%。離子布植和離子鍍在醫療植入領域日益受到認可,該領域融合了表面改質和塗層沉積技術。製程類型的多樣化與應用主導藍圖相契合,例如半導體製造廠尋求超潔淨環境,工具製造商尋求高能量離子轟擊,家具製造商尋求低溫裝飾性鍍鉻。

塑膠基板雖然目前市佔率較小,但正以6.05%的複合年成長率成長,這主要得益於低溫循環製程和等離子體預處理技術的應用,這些技術可以避免聚合物變形。金屬仍佔據PVD(物理沉澱)塗層市場的主導地位,市佔率高達60.78%,這反映了金屬在模具和引擎零件領域根深蒂固的需求。濺鍍氮化鋯正在取代電解鉻,用於豪華車的聚碳酸酯和ABS裝飾件,從而在美觀性和可回收性之間取得平衡。

用於建築低輻射(Low-E)面板的玻璃金屬化過程保持穩定。康寧Eagle XG等特種玻璃在光電應用領域的需求日益成長。受國防費用的推動,直升機和無人機的複合材料基板正成為一個新興的市場區隔。基板多樣化的需求促使塗層必須檢驗其在不同熱膨脹係數下的附著力,從而推動了對原位等離子體活化和底塗層策略的投資。

區域分析

亞太地區預計到2025年將維持47.40%的市場佔有率,這主要得益於台灣、韓國和中國當地的半導體投資。當地的設備補貼和晶圓製造獎勵正在推動資金流入下一代高功率脈衝磁控濺鍍(HiPIMS)和離子化物理氣相沉積(PVD)生產線。日本和泰國的汽車製造中心正在實施裝飾性鍍鉻替代技術,以滿足REACH法規的出口要求。在印度,Ionbond位於孟買的新生產線已運作,有助於縮短國內切削刀具製造商的前置作業時間。

北美地區維持穩定成長,主要得益於航太和醫療設備產業的叢集。美國渦輪引擎原始設備製造商(OEM)正在採用多層耐熱阻隔塗層,這種塗層能夠承受超過1500攝氏度的燃燒溫度。同時,加州的鉻禁令加速了低溫裝飾塗層在管道配件領域的應用。加拿大和墨西哥也為汽車零件(包括汽車工具和需要耐腐蝕性的油砂開採設備)的成長做出了貢獻。

歐洲正因禁止使用有害電鍍液的法規而取得進展。德國是精密工具領域的主導,瑞士專注於手錶零件的塗層,北歐國家則擁有燃料電池堆層技術的先驅地位。 Iondbond位於瑞典的大型中心將於2024年11月開業,屆時將使斯堪地那維亞地區的產能翻番,並有助於降低出口到北美的原始設備製造商(OEM)的物流成本。以沙烏地阿拉伯、阿拉伯聯合大公國和南非為首的新興地區正以5.82%的複合年成長率(CAGR)保持最快成長,這主要得益於不斷擴大的基礎設施對塗層鑽頭、閥門和裝飾性金屬外觀五金件的需求。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 半導體節點向7nm以下過渡的趨勢日益明顯。

- 微創醫療設備生產快速成長

- 六價鉻電鍍監管過渡

- 需要進行保形PVD表面處理的3D列印零件

- 塑膠和複合材料的低溫裝飾性PVD

- 市場限制

- 超高真空系統需要高額資本投入

- 與 CVD/ALD 在高長寬比結構中的競爭

- 熟練的真空製程工程師短缺

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 透過流程

- 濺鍍沉積

- 熱沉澱/電子束沉澱

- 電弧沉澱法

- 離子布植和離子電鍍

- HiPIMS

- 按平台

- 金屬

- 塑膠

- 玻璃

- 依材料類型

- 金屬

- 陶瓷和氧化物

- 其他材料類型

- 最終用戶

- 工具

- 成分

- 航太/國防

- 車

- 電子和半導體(包括光學產品)

- 發電

- 其他組件(太陽能產品、醫療設備等)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 埃及

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率/排名分析

- 公司簡介

- Advanced Energy

- AJA International, Inc.

- Angstrom Engineering Inc.

- Applied Materials, Inc.

- Buhler Leybold Optics,

- Crystallume PVD

- Denton Vacuum

- HEF

- IHI Corporation

- Impact Coatings AB

- KDF Electronic & Vacuum Services Inc.

- KOLZER SRL

- Mitsubishi Materials Corporation

- Mustang Vacuum Systems

- OC Oerlikon Management AG

- PLATIT AG

- Richter Precision Inc.

- Satisloh AG

- Silfex Inc.

- Singulus Technologies AG

- ULVAC

- Veeco Instruments Inc.

- voestalpine eifeler Group

第7章 市場機會與未來展望

Physical Vapor Deposition Coatings market size in 2026 is estimated at USD 11.77 billion, growing from 2025 value of USD 11.14 billion with 2031 projections showing USD 15.5 billion, growing at 5.66% CAGR over 2026-2031.

This acceleration reflects demand spikes from sub-7 nm semiconductor nodes and the wider use of minimally invasive medical devices that rely on biocompatible thin films. Regulatory momentum away from hexavalent chromium electroplating, combined with the need to finish 3D-printed parts, positions physical vapor deposition as both a compliance route and a process enabler. The technology's ability to deliver dense, defect-free layers on metals, plastics, glass, and emerging substrates underpins robust capital spending on new coating centers. Competitive intensity rises as titanium target prices increase and equipment manufacturers rush to commercialize high-ionization sputter sources.

Global Physical Vapor Deposition Coatings Market Trends and Insights

Rising Semiconductor Node Transition Below 7 nm

The current ramp toward sub-7 nm logic and memory devices multiplies demand for barrier and seed layers deposited with sub-nanometer precision. Equipment platforms supplied by Applied Materials reported strong uptake for molybdenum-based interconnect stacks that mitigate copper diffusion at extreme aspect ratios. Volume adoption in Taiwan and South Korea anchors regional supply chains for ultra-high-vacuum sputter chambers, advanced titanium and tantalum targets, and in-situ metrology. Each shrink node tightens tolerance bands, pushing tool makers to integrate HiPIMS sources that deliver higher ionization and denser films. Advanced packaging formats, including chiplets and through-silicon vias, further lift spending on conformal physical vapor deposition steps for 3D integration.

Booming Minimally-Invasive Medical Device Production

The accelerating demand for catheter-based implants and orthopedic fixation hardware elevates coating requirements from simple biocompatibility to antimicrobial and osteointegrative functions. Magnetron-sputtered tantalum films of 550 nm thickness achieved critical adhesion loads of 39.184 N, outperforming uncoated titanium constructs in BMC Biotechnology trials. Regulatory approvals under the US FDA (Food and Drug Administration) create durable revenue once process validation is complete, stimulating contract coaters in the United States, Germany, and Ireland to add dedicated medical lines with clean-room isolation. Cost-sensitive device OEMs (original equipment manufacturers) in China and Malaysia are increasingly outsourcing PVD (physical vapor deposition) steps to meet global supply-chain quality audits.

High Cap-ex of Ultra-High-Vacuum Systems

A single 12-inch cluster tool can cost USD 5 million, excluding clean-room build-out and facility utilities. Such capital thresholds deter new entrants in Brazil, Indonesia, and sub-Saharan Africa, consolidating orders among established players that possess depreciation-advantaged assets. Financing is complicated by five- to seven-year payback horizons and the risk of process obsolescence as node geometry evolves. Government incentive programs in India and Vietnam partially offset cap-ex, yet bank covenants still require volume guarantees from blue-chip customers.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Shift Away from Hex-Chrome Electroplating

- 3D-Printing Parts Requiring Conformal PVD Finishes

- Competition from CVD / ALD for High-Aspect Features

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

HiPIMS recorded the highest 6.92% forecast CAGR, driven by ionization levels exceeding 70%, which yield dense coatings with superior adhesion for cutting tools. Sputter Deposition remains the bedrock, with a 42.35% market share in 2025, favored for its scalability from microelectronics to architectural glass. Thermal and e-beam evaporation occupy niche markets in optical coating, while Arc Vapor Deposition continues to be used in wear-resistant decorative trims, despite challenges from macro-particles. The physical vapor deposition coatings market size for HiPIMS is projected to climb steadily as automotive OEMs standardize on nitride recipes that extend tool life in press shops.

Equipment builders incorporate multi-cathode configurations that allow for on-the-fly target changes, reducing recipe switch-over by 30%. Ion Implantation and Ion Plating gain visibility in medical implants where surface modification and coating deposition converge. Process-type diversification aligns with an application-driven roadmap: semiconductor fabs demand ultra-clean environments, tool manufacturers prize high-energy ion bombardment, and furniture producers seek low-temperature decorative chrome.

Plastic substrates, though smaller today, are advancing at a 6.05% CAGR as low-temperature cycles and plasma pre-treatments avoid polymer deformation. The physical vapor deposition coatings market share for Metals stays dominant at 60.78%, reflecting entrenched tooling and engine component volumes. Polycarbonate and ABS trim pieces in premium cars utilize sputtered zirconium nitride to replace electroplated chrome, striking a balance between aesthetics and recyclability.

Metallization of glass for architectural low-E panels sustains steady volumes; specialty glass, such as Corning Eagle XG, sees an uptick in photonics applications. Composite substrates in helicopters and drones represent an emergent niche propelled by defense spending. Substrate diversification pressures coerce coatings to validate adhesion under disparate coefficients of thermal expansion, prompting investments in in-situ plasma activation and base-coat strategies.

The Physical Vapor Deposition Coatings Market Report is Segmented by Process Type (Sputter Deposition, E-Beam Evaporation, Hipims, and More), Substrate (Metals, Glass, and More), Material Type (Metals/Alloys, Ceramics and Oxides, and More), End User (Tools and Components), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

The Asia-Pacific region retained a 47.40% share in 2025, driven by semiconductor investments in Taiwan, South Korea, and mainland China. Local equipment subsidies and wafer-fab incentive packages channel capital into next-generation HiPIMS and ionized PVD lines. Automotive hubs in Japan and Thailand add decorative chrome alternatives to meet REACH-style export requirements. India benefits from Ionbond's new Mumbai line, which shortens lead times for domestic cutting-tool manufacturers.

North America records stable growth, driven by clusters in the aerospace and medical device sectors. US turbine-engine OEMs adopt multilayer thermal-barrier coatings that lift firing temperatures past 1,500 °C, while California's chrome ban accelerates the adoption of low-temperature decorative films on plumbing hardware. Canada and Mexico contribute to the automotive industry through components such as automotive tooling and oil-sand extraction, which demand erosion resistance.

Europe advances through regulatory tailwinds that outlaw toxic plating baths. Germany leads in precision tools, Switzerland specializes in watch component coatings, and the Nordics pioneer fuel cell stack layers. Ionbond's Swedish mega-center, opened November 2024, doubles Scandinavian capacity and reduces logistics costs for OEMs exporting to North America. Emerging regions led by Saudi Arabia, the United Arab Emirates and South Africa record the swiftest 5.82% CAGR, reflecting infrastructure expansions that rely on coated drill bits, valves and decorative metal-effect fittings.

- Advanced Energy

- AJA International, Inc.

- Angstrom Engineering Inc.

- Applied Materials, Inc.

- Buhler Leybold Optics,

- Crystallume PVD

- Denton Vacuum

- HEF

- IHI Corporation

- Impact Coatings AB

- KDF Electronic & Vacuum Services Inc.

- KOLZER SRL

- Mitsubishi Materials Corporation

- Mustang Vacuum Systems

- OC Oerlikon Management AG

- PLATIT AG

- Richter Precision Inc.

- Satisloh AG

- Silfex Inc.

- Singulus Technologies AG

- ULVAC

- Veeco Instruments Inc.

- voestalpine eifeler Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising semiconductor node transition below 7 nm

- 4.2.2 Booming minimally-invasive medical device production

- 4.2.3 Regulatory shift away from hex-chrome electroplating

- 4.2.4 3D-printing parts requiring conformal PVD finishes

- 4.2.5 Low-temperature decorative PVD on plastics and composites

- 4.3 Market Restraints

- 4.3.1 High cap-ex of ultra-high-vacuum systems

- 4.3.2 Competition from CVD / ALD for high-aspect features

- 4.3.3 Shortage of skilled vacuum-process engineers

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Process Type

- 5.1.1 Sputter Deposition

- 5.1.2 Thermal / e-Beam Evaporation

- 5.1.3 Arc Vapor Deposition

- 5.1.4 Ion Implantation and Ion Plating

- 5.1.5 HiPIMS

- 5.2 By Substrate

- 5.2.1 Metals

- 5.2.2 Plastics

- 5.2.3 Glass

- 5.3 By Material Type

- 5.3.1 Metals(Includes Alloys)

- 5.3.2 Ceramics and Oxides

- 5.3.3 Other Material Types

- 5.4 By End User

- 5.4.1 Tools

- 5.4.2 Components

- 5.4.2.1 Aerospace and Defense

- 5.4.2.2 Automotive

- 5.4.2.3 Electronics and Semiconductors (incl. Optics)

- 5.4.2.4 Power Generation

- 5.4.2.5 Other Components (Solar Products, Medical Equipment, and Others)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Nordic Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Qatar

- 5.5.5.4 Egypt

- 5.5.5.5 South Africa

- 5.5.5.6 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share**/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Advanced Energy

- 6.4.2 AJA International, Inc.

- 6.4.3 Angstrom Engineering Inc.

- 6.4.4 Applied Materials, Inc.

- 6.4.5 Buhler Leybold Optics,

- 6.4.6 Crystallume PVD

- 6.4.7 Denton Vacuum

- 6.4.8 HEF

- 6.4.9 IHI Corporation

- 6.4.10 Impact Coatings AB

- 6.4.11 KDF Electronic & Vacuum Services Inc.

- 6.4.12 KOLZER SRL

- 6.4.13 Mitsubishi Materials Corporation

- 6.4.14 Mustang Vacuum Systems

- 6.4.15 OC Oerlikon Management AG

- 6.4.16 PLATIT AG

- 6.4.17 Richter Precision Inc.

- 6.4.18 Satisloh AG

- 6.4.19 Silfex Inc.

- 6.4.20 Singulus Technologies AG

- 6.4.21 ULVAC

- 6.4.22 Veeco Instruments Inc.

- 6.4.23 voestalpine eifeler Group

7 Market Opportunities & Future Outlook

- 7.1 White-space and unmet-need assessment