|

市場調查報告書

商品編碼

1910455

塗料樹脂:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031)Resins In Paints And Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

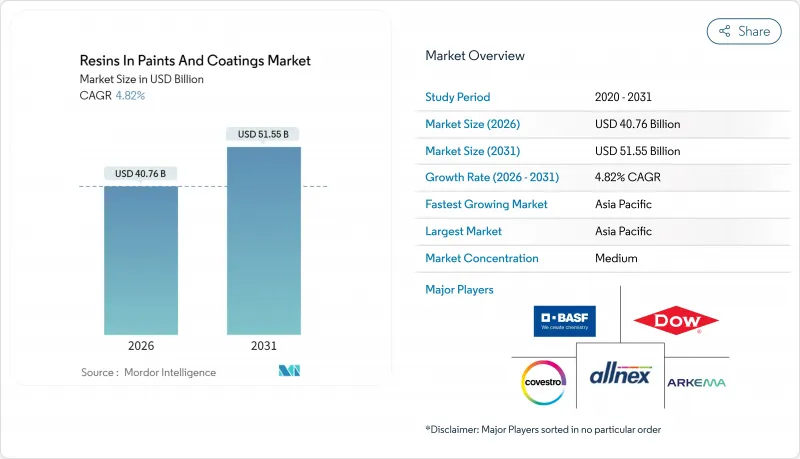

預計到 2026 年,油漆和塗料樹脂市場價值將達到 407.6 億美元,高於 2025 年的 388.9 億美元。

預計到 2031 年,該產業規模將達到 515.5 億美元,2026 年至 2031 年的複合年成長率為 4.82%。

儘管表面上成長率看似溫和,但政策主導的溶劑型化學品減量趨勢正迫使配方商圍繞水性丙烯酸酯、聚氨酯分散體和其他生物循環技術重組產品系列。三大洲的政府已將揮發性有機化合物 (VOC) 的排放上限從 2024 年提前至 2025 年,並加快了轉型進程。亞太地區在基礎設施投資的主導繼續引領價值創造。然而,北美和歐洲正在進行為期多年的維修計劃,旨在推廣優質低 VOC 樹脂。隨著現有企業整合可再生原料、建造區域分散式工廠並採用可縮短產品開發週期的數位化配方平台,競爭日益激烈。

全球油漆及塗料樹脂市場趨勢及洞察

亞太地區的建築業蓬勃發展

公共部門基礎設施項目仍然是建築和防護塗料的最大需求來源。僅印度的國家基礎設施計劃就計劃到2025年累計資本支出達1.4兆美元,這將推動橋樑、港口和鐵路塗料的多年需求,而這些塗料主要依賴環氧樹脂和聚氨酯樹脂。新加坡建設局強制要求所有新建公共住宅計劃從2025年起達到綠建築標誌鉑金級標準,實際上要求工廠預塗面板必須使用水性丙烯酸或聚氨酯塗料。菲律賓已撥款1.1兆披索(約200億美元)用於其2024年的「建設更美好、更繁榮」計劃,該計劃涵蓋機場、道路和能源資產等大量使用工業塗料的設施。在全部區域,國有開發商擴大將低VOC(揮發性有機化合物)規範納入競標文件,從而推動了分散技術的應用。樹脂製造商已宣佈在印尼和越南安裝分散反應器,以縮短前置作業時間並減少運輸排放。這些舉措既能對沖全球公司的產量,又能使區域性化合物生產商實現在地化供應。

加強VOC排放法規

高溶劑樹脂的合規窗口正在迅速縮小。 2025年1月,美國環保署(EPA)將氣霧塗料的揮發性有機化合物(VOC)含量限制在25%(重量比)(先前的限值為45%),這迫使黏合劑的選擇必須即時做出改變。喬治亞隨後也採取了類似措施,在其法規391-3-1-.02(7)(c)中將建築用平塗塗料的VOC含量限制在50克/公升,該法規於2025年7月生效。歐洲進一步收緊了標準,歐盟委員會於2024年10月發布的生態標章標準提案規定,室內塗料的VOC含量上限為30克/公升。只有高固態丙烯酸或混合系統才能達到此標準。中國在其GB 18582-2024標準中也採用了與歐盟相同的閾值,這表明全球最大的建築市場不能再成為VOC法規寬鬆的避風港。隨著配方師們應對日益嚴格的法規,擁有易於規模化的水性產品線(尤其是丙烯酸和聚氨酯分散體)的樹脂供應商正在獲得市場佔有率。

原物料價格波動

丙烯、苯和乙烯價格波動仍然是重要的不利因素。根據ICIS Chemical Business通報,受三家裂解裝置意外停產的影響,2024年第二季亞洲丙烯合約價格較上季上漲25%。歐洲也面臨類似的壓力,導致乙烯衍生物利潤率跌至負值,迫使規模較小的環氧樹脂生產商關閉部分工廠。對於沒有上游石化業務的樹脂生產商而言,在價格敏感的建築樹脂領域,運作傳導延遲通常為60至90天。一些局部解決方案正在湧現,例如科思創宣布推出一種源自廢棄食用油的生物再生多元醇。該公司計劃在2024年消除與化石原料的價格差異,並降低對石腦油價格波動的依賴。然而,在生物基原料廣泛應用之前,大宗商品價格的相關性仍將繼續限制利潤率。

細分市場分析

由於丙烯酸樹脂與低VOC水性體系的兼容性,預計到2025年,其在塗料市場樹脂佔有率中將佔30.02%。加上5.28%的複合年成長率,隨著監管機構收緊排放上限,丙烯酸樹脂的市場價值轉型將由此展開。環氧樹脂廣泛應用於船舶和風力發電機等高應力應用領域,Hexion在其2024年報告中指出,渦輪機原始設備製造商(OEM)對其訂單強勁。聚氨酯分散體在電動車電池應用領域的需求不斷成長。作為粉末塗料主力軍的聚酯樹脂,由於低溫固化聚酯-環氧樹脂混合塗料的日益普及,其利潤率正面臨壓縮。醇酸樹脂長期以來一直是溶劑型建築塗料的支柱,但由於其乾燥時間長、VOC(揮發性有機化合物)含量高,在主流牆面塗料產品線中的應用正在減少。同時,醇酸樹脂在高檔木器塗料領域仍佔有一席之地。在斯堪地那維亞國家,基於 ISO 14040 的生命週期評估已成為公共採購的強制性要求,市場佔有率正逐漸轉向具有經認證的環境聲明的樹脂。

丙烯酸樹脂優異的分散性能也為模組化住宅的工廠預塗面板生產線奠定了基礎。為了滿足預製現場嚴格的生產週期,快乾型單步驟塗料備受青睞,水性壓克力樹脂自然成為理想之選。環氧樹脂供應商正透過奈米改質系統來縮短烘烤時間,而聚氨酯供應商則在推廣無需強制通風烘箱的濕固化方法。在塗料市場,整體樹脂供應商的創新方向正趨向於使用減少二氧化碳排放的原料。BASF承諾到2026年將可再生丙烯整合到其丙烯酸價值鏈中,便是這一趨勢的有力證明。這項原物料策略符合歐洲公共採購法規,該法規要求對生物基含量達到20%或以上的材料給予溢價。

區域分析

到2025年,亞太地區將佔據全球塗料樹脂市場44.12%的佔有率,並以5.33%的複合年成長率成為成長最快的地區,這主要得益於中國建設業的復甦和印度的大型企劃計畫。在中國,隨著地方政府放寬貸款監管,2024年住宅開工量將回升,貸款發放量也將隨之增加。印度的國家基礎設施計畫將推動橋樑和鐵路防護塗料樹脂的消費,而印尼的IKN努沙登加拉首都地區發展計畫和菲律賓的「建設更美好、更有效率」計畫將提升以地區為基礎需求。日本的抗震維修補貼計畫和韓國的綠色新政政策均要求在公共採購中使用低VOC塗料,並透過當地加工商推廣丙烯酸聚氨酯分散體的使用。

北美地區的成長主要得益於住宅維修支出,預計到2024年將達到4,850億美元,其中節能型外牆覆層和牆板更換將引領這一趨勢。美國環保署(EPA)將於2025年實施的VOC(揮發性有機化合物)法規將加速水性塗料的普及,剪切機表示,低氣味乳膠漆的溢價將有助於提高利潤率。預計到2024年,加拿大的碳價將達到每噸80美元,這將鼓勵建築業主提供包含高反射率屋頂塗料的維修方案,以降低冷氣負荷。

受「維修」和「工業排放指令」(該指令優先考慮低溶劑和粉末塗料)的推動,歐洲塗料市場正經歷著個位數的溫和成長。北歐各市政當局在競標中越來越要求提供產品特定的環境聲明,這使得擁有全面審核且產品線多元化的供應商更具優勢。南美洲、中東和非洲在耐腐蝕樹脂市場規模中所佔佔有率相對較小,但預計巴西、沙烏地阿拉伯和阿拉伯聯合大公國等國的石油天然氣、採礦和體育場建設等產業將帶動局部成長。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 亞太地區的建築業蓬勃發展

- 收緊(VOC)排放法規

- 汽車生產從2024年開始復甦

- 經合組織國家的住宅維修熱潮

- 用於原位3D列印修復的樹脂

- 市場限制

- 原物料價格波動

- 改用純粉末系統

- 微塑膠淘汰法規

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 按類型

- 環氧樹脂

- 丙烯酸纖維

- 聚氨酯

- 聚酯纖維

- 聚丙烯

- 醇酸樹脂

- 其他類型

- 按最終用戶行業分類

- 產業

- 建築學

- 車

- 包裝

- 其他最終用戶

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 埃及

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率/排名分析

- 公司簡介

- Allnex GmbH

- Arkema

- BASF SE

- Covestro AG

- Dow

- Evonik Industries AG

- Hexion

- Huntsman International LLC

- Kangnam Chemical

- KANSAI HELIOS

- Mitsubishi Shoji Chemical Corporation

- Mitsui Chemicals Inc.

- Olin Corporation.

- Reichhold LLC 2

- Solvay

- Synthomer plc

- Uniform Synthetics

- Vil Resins

- Wanhua

第7章 市場機會與未來展望

Resins In Paints And Coatings market size in 2026 is estimated at USD 40.76 billion, growing from 2025 value of USD 38.89 billion with 2031 projections showing USD 51.55 billion, growing at 4.82% CAGR over 2026-2031.

Although the headline growth rate appears measured, policy-driven shifts away from solvent-borne chemistries are forcing formulators to retool their portfolios around waterborne acrylic, polyurethane dispersion, and other biocircular technologies. Governments on three continents tightened volatile-organic-compound (VOC) ceilings in 2024-2025, accelerating the transition timeline. The Asia-Pacific region continues to dominate value creation, thanks to infrastructure spending. However, North America and Europe are staging multi-year renovation programs that favor premium, low-VOC resins. Competitive intensity is rising as incumbents integrate renewable feedstocks, build regional dispersion plants, and deploy digital formulation platforms to compress product-development cycles.

Global Resins In Paints And Coatings Market Trends and Insights

Construction Boom Across the Asia-Pacific

Public-sector infrastructure pipelines remain the single largest demand engine for architectural and protective coatings. India's National Infrastructure Pipeline alone targets USD 1.4 trillion in cumulative capital outlays through 2025, generating a multi-year pull-through for epoxy- and polyurethane-rich bridge, port, and rail coatings. Singapore's Building and Construction Authority now requires Green Mark Platinum performance on all new public housing projects from 2025, effectively mandating water-based acrylic or polyurethane chemistries for factory-applied panels. The Philippines allocated PHP 1.1 trillion (approximately USD 20 billion) to its Build Better More program in 2024, which includes industrial coating-intensive airports, roads, and energy assets. Across the region, state-owned developers are bundling low-VOC specifications into tender documents, accelerating the adoption of dispersion technology. Resin suppliers have responded by announcing the establishment of dispersion reactors in Indonesia and Vietnam, aiming to shorten lead times and reduce freight emissions. These moves provide global incumbents with a volume hedge while enabling regional formulators to localize their supply.

Tightening VOC-Emission Regulations

The compliance window for high-solvent resins is narrowing rapidly. In January 2025 the U.S. Environmental Protection Agency capped aerosol-coating VOC content at 25% by weight-down from prior category ceilings of 45%-forcing an immediate shift in binder selection. Georgia followed with Rule 391-3-1-.02(7)(c), effective July 2025, limiting flat architectural finishes to 50 grams per liter. Europe raised the bar again when the European Commission published draft Ecolabel criteria in October 2024 that impose a 30 grams-per-liter ceiling for interior paints, achievable only with high-solids acrylic or hybrid systems. China mirrored the EU thresholds in its GB 18582-2024 standard, signaling that the world's largest construction market can no longer serve as a VOC-light haven. Resin suppliers with ready-to-scale waterborne portfolios-especially acrylic- and polyurethane-based dispersions-are winning share as formulators scramble to meet the cliff.

Feedstock Price Volatility

Price swings for propylene, benzene, and ethylene remain a significant headwind. ICIS Chemical Business reported that Asian contract propylene prices increased by 25% quarter-on-quarter in Q2 2024, following three unplanned cracker outages. Similar squeezes in Europe turned ethylene-derivative margins negative, compelling smaller epoxy producers to idle plants. Resin makers without upstream petrochemical integration face 60- to 90-day pass-through lags in the price-sensitive architectural channel. Partial insulation is emerging; Covestro has disclosed bio-circular polyols derived from waste vegetable oils that reached price parity with fossil feedstock by 2024, thereby trimming exposure to naphtha volatility. Still, the commodity link will limit margins until bio-feedstock adoption scales.

Other drivers and restraints analyzed in the detailed report include:

- Automotive Output Revival Post-2024

- Refurbishment Wave in OECD Housing

- Shift Toward Powder-Only Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Acrylic resins commanded 30.02% of the 2025 resins in paints and coatings market share, supported by their superior fit in low-VOC waterborne systems. Coupled with a 5.28% CAGR, they anchor value migration as regulators tighten emission ceilings. Epoxy resins are used in high-stress applications, such as those in the marine and wind-turbine industries; Hexion noted robust orders from turbine OEMs in its 2024 report. Polyurethane dispersions benefit from EV battery use cases. Polyester, a workhorse for powder coatings, faces margin compression as buyers mix polyester-epoxy hybrids that cure at lower temperatures. Alkyds, long the backbone of solvent-borne architectural paints, retain a niche in premium wood finishes but fade in mainstream wall-coating lines due to their slower dry time and higher VOC. ISO 14040 life-cycle assessments are now mandatory in Scandinavian public tenders, funneling share toward resins with verified environmental declarations.

Acrylic's dispersion superiority also underpins factory-applied panel lines for modular housing. Prefabrication sites prefer quick-dry, single-pass coatings to meet tight takt times, making waterborne acrylic a natural choice. Epoxy suppliers are responding with nano-modified systems that cut bake curves, while polyurethane vendors push humidity-cure versions that eliminate forced-air ovens. Across the resins in paints and coatings market, supplier innovation is converging on CO2-reduced feedstocks, evidenced by BASF's pledge to integrate renewable propylene into its acrylic value chain by 2026. This feedstock strategy aligns with European public-procurement rules granting price premiums to materials with >=20% bio-content.

The Resins in Paints and Coatings Market Report is Segmented by Type (Epoxy, Acrylic, Polyurethane, Polyester, Polypropylene, Alkyd, Other Types), End-User Industry (Industrial, Architectural, Automotive, Packaging, Other End-Users), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific accounted for a 44.12% share of the resins in paints and coatings market in 2025 and is growing fastest at a 5.33% CAGR, propelled by China's construction recovery and India's megaproject pipelines. China's residential completions rebounded in 2024 as municipal authorities eased credit, translating into higher drawdowns. India's National Infrastructure Pipeline drives protective-coating resin consumption for bridges and railways, while the IKN Nusantara capital-city buildout in Indonesia and the Philippines' Build Better More program lift regional baseline volumes. Japan's seismic-retrofit subsidy and South Korea's Green New Deal mandate low-VOC coatings in public procurement, driving the use of acrylic and polyurethane dispersions through local converting channels.

North America's momentum rests on remodeling spending that hit USD 485 billion in 2024, with energy-efficient exteriors and siding replacements at the top of the wallet. The EPA's 2025 VOC rule accelerates waterborne adoption, and Sherwin-Williams has flagged premium pricing on low-odor emulsions as margin-accretive. Canada's carbon price reached CAD 80 per metric ton in 2024 and is nudging building owners toward retrofit packages that include high-albedo roof coatings to cut cooling loads.

Europe advances at a mid-single-digit pace led by the Renovation Wave and the Industrial Emission Directive, both of which prioritize low-solvent or powder chemistries. Nordic municipalities now require product-specific environmental product declarations in tenders, advantaging suppliers with fully audited dispersion lines. South America and the Middle East and Africa collectively account for a smaller share of coating resins market size but offer pocket-growth linked to oil-and-gas, mining, and stadium construction in Brazil, Saudi Arabia, and the United Arab Emirates.

- Allnex GmbH

- Arkema

- BASF SE

- Covestro AG

- Dow

- Evonik Industries AG

- Hexion

- Huntsman International LLC

- Kangnam Chemical

- KANSAI HELIOS

- Mitsubishi Shoji Chemical Corporation

- Mitsui Chemicals Inc.

- Olin Corporation.

- Reichhold LLC 2

- Solvay

- Synthomer plc

- Uniform Synthetics

- Vil Resins

- Wanhua

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Construction boom across Asia-Pacific

- 4.2.2 Tightening (VOC)-emission regulations

- 4.2.3 Automotive output revival post-2024

- 4.2.4 Refurbishment wave in OECD housing

- 4.2.5 On-site 3-D printing repair resins

- 4.3 Market Restraints

- 4.3.1 Feed-stock price volatility

- 4.3.2 Shift toward powder-only systems

- 4.3.3 Micro-plastic phase-out rules

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Epoxy

- 5.1.2 Acrylic

- 5.1.3 Polyurethane

- 5.1.4 Polyester

- 5.1.5 Polypropylene

- 5.1.6 Alkyd

- 5.1.7 Other Types

- 5.2 By End-user Industry

- 5.2.1 Industrial

- 5.2.2 Architectural

- 5.2.3 Automotive

- 5.2.4 Packaging

- 5.2.5 Other End-users

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Egypt

- 5.3.5.5 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Allnex GmbH

- 6.4.2 Arkema

- 6.4.3 BASF SE

- 6.4.4 Covestro AG

- 6.4.5 Dow

- 6.4.6 Evonik Industries AG

- 6.4.7 Hexion

- 6.4.8 Huntsman International LLC

- 6.4.9 Kangnam Chemical

- 6.4.10 KANSAI HELIOS

- 6.4.11 Mitsubishi Shoji Chemical Corporation

- 6.4.12 Mitsui Chemicals Inc.

- 6.4.13 Olin Corporation.

- 6.4.14 Reichhold LLC 2

- 6.4.15 Solvay

- 6.4.16 Synthomer plc

- 6.4.17 Uniform Synthetics

- 6.4.18 Vil Resins

- 6.4.19 Wanhua

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

浸漬清漆市場規模、佔有率和成長分析:按樹脂類型、固化方法、塗裝流程、終端用戶產業和地區分類-2026-2033年產業預測

浸漬清漆市場規模、佔有率和成長分析:按樹脂類型、固化方法、塗裝流程、終端用戶產業和地區分類-2026-2033年產業預測 耐腐蝕樹脂市場分析及預測(至2035年):類型、產品類型、應用、技術、成分、形態、材料類型、最終用戶、功能

耐腐蝕樹脂市場分析及預測(至2035年):類型、產品類型、應用、技術、成分、形態、材料類型、最終用戶、功能 全球耐腐蝕樹脂市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球耐腐蝕樹脂市場規模、佔有率、趨勢和成長分析報告(2026-2034) 耐腐蝕樹脂市場-全球產業規模、佔有率、趨勢、機會與預測:按類型、技術、應用、競爭對手、地區分類,2021-2031年

耐腐蝕樹脂市場-全球產業規模、佔有率、趨勢、機會與預測:按類型、技術、應用、競爭對手、地區分類,2021-2031年 全球耐腐蝕樹脂市場,2026-2030年

全球耐腐蝕樹脂市場,2026-2030年 浸漬絕緣清漆市場(依樹脂類型、形態、應用、固化製程、最終用途產業、包裝與黏度等級分類)-2026-2032年全球預測

浸漬絕緣清漆市場(依樹脂類型、形態、應用、固化製程、最終用途產業、包裝與黏度等級分類)-2026-2032年全球預測 耐腐蝕樹脂市場規模、佔有率及成長分析(依技術、樹脂類型、應用及地區分類)-2026-2033年產業預測耐腐蝕樹脂市場按樹脂類型和最終用途行業分類 - 全球預測 2025-2032

耐腐蝕樹脂市場規模、佔有率及成長分析(依技術、樹脂類型、應用及地區分類)-2026-2033年產業預測耐腐蝕樹脂市場按樹脂類型和最終用途行業分類 - 全球預測 2025-2032 2032年耐腐蝕樹脂市場預測:按樹脂類型、基材類型、分銷管道、配方技術、應用、最終用戶和地區進行的全球分析

2032年耐腐蝕樹脂市場預測:按樹脂類型、基材類型、分銷管道、配方技術、應用、最終用戶和地區進行的全球分析 塗料樹脂市場報告(按類型、技術、應用和地區)2025-2033

塗料樹脂市場報告(按類型、技術、應用和地區)2025-2033