|

市場調查報告書

商品編碼

1910435

硬體錢包:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Hardware Wallet - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

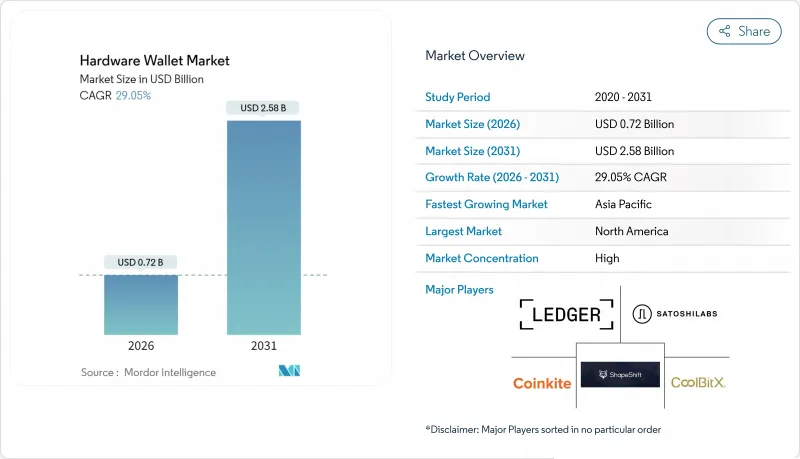

預計到 2025 年,硬體錢包市場價值將達到 5.6 億美元,從 2026 年的 7.2 億美元成長到 2031 年的 25.8 億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 29.05%。

資產管理公司迅速轉向自託管、交易所安全漏洞頻發以及MiCA和OCC等法規結構的明確化,共同為硬體錢包市場的持續成長奠定了基礎。企業客戶正透過以本地金鑰管理設備取代託管帳戶來推動更大的訂單量,迫使傳統上以消費者為中心的供應商提高認證等級並擴展專業服務。此外,關稅衝擊後安全元件生產的本地化以及多鏈DeFi活動的興起也推動了硬體錢包市場的發展,後者需要具備跨多個Layer 1和Layer 2網路進行交易簽署的設備。由於多年創業投資資金使新進業者能夠嘗試外形規格,競爭格局正在發生變化,但擁有雄厚資本的現有企業在認證成本和供應鏈管理方面仍然保持優勢。

全球硬體錢包市場趨勢與洞察

機構採用自我管理解決方案的速度加快

各機構正將數位資產視為金融資產而非投機性資產,決策者也摒棄了單一託管模式,轉而採用符合董事會風險接受度的確定性控制措施。這種轉變解釋了為何硬體錢包市場圍繞著FIPS認證的安全元件、基於REST的簽章協定堆疊和SOC-2報告層展開。 Dfns正是這種轉變的體現,該公司已成功資金籌措1,600萬美元,用於擴展其為富達國際和Zodiac Custody提供支援的「錢包即服務」(WaaS)基礎設施。企業級應用程式推高了平均售價,並延長了更新周期。供應商正轉向訂閱模式,將韌體更新、身份驗證服務和硬體保固捆綁在一起。同時,系統整合商透過將錢包整合到HSM機架和零信任安全區中,延長了設備的使用壽命,從而擴大了硬體錢包市場的潛在規模。

網路安全漏洞揭露事件激增,推動了對離線金鑰的需求。

加密貨幣竊盜案的顯著增加重新喚起了人們對熱錢包攻擊面的關注。 Bybit 和 Femex 的事件促使人們緊急遷移資產,導致消費者設備過載,並揭露了備份檢驗和金鑰分割工作流程的缺陷。廠商們隨即展示了符合通用準則 EAL5+ 標準的晶片、環氧樹脂填充機殼和防篡改全像圖,強調離線恢復能力。行銷宣傳活動利用安全漏洞新聞帶來的認知衝擊,反覆將空氣間隙儲存定位為「金融資產與國家級駭客之間的最後一道防線」。由此帶來的品牌價值進一步鞏固了家族辦公室和交易所交易產品贊助商對硬體錢包的接受度,並將硬體錢包市場擴展到技術愛好者之外。

不斷變化的反洗錢/了解你的客戶 (AML/KYC) 法規推高了合規成本。

監管機構現在要求硬體供應商在其設備中加入機制,以便對受制裁地址發出警報、實施地址篩檢API,並記錄其設備群中的可疑活動。實施這些韌體會增加韌體開銷,需要定期更新列表,並將資料保護責任轉移到供應商身上。沒有法務團隊的Start-Ups通常會將合規任務外包給雲端評分服務,這會惡化單位經濟效益並加劇營運資金壓力。對加密模組嚴格的跨境出口限制進一步加劇了物流複雜性,導致運往高成長地區的貨物延遲,並減緩了硬體錢包市場的發展。同時,成熟的製造商可以透過利用現有的FATF審核文件,以更低的合規成本維持全球營運。

細分市場分析

截至2025年,USB連接的硬體錢包將維持46.98%的市場佔有率,這得益於空氣間隙架構和極小的攻擊面。同時,NFC設備正以29.62%的複合年成長率成長,這主要得益於消費者將他們在Apple Pay和PayNow等非接觸式支付方式中養成的習慣應用於加密貨幣消費。 Arculus和Sugi等廠商正引領著這一趨勢,他們將安全元件整合到可放入普通錢包的時尚卡片中,從而在銷售點實現「輕觸簽名」並掃描QR碼的便捷支付流程。因此,隨著東南亞超級應用不斷擴大接受穩定幣小額支付的商家數量,基於NFC的硬體錢包市場規模預計將大幅成長。

對於機構用戶而言,實體線纜仍然是減少射頻洩漏並在 SOC-2審核期間保持確定性路徑的首選方案。然而,新一代空氣間隙解決方案以無狀態方式採用 NFC 技術,無需暴露私鑰即可實現外部安全元件認證。一旦 ISO/TC 68 等標準組織發布 NFC 安全儲存的最終指南,法律規範可能會增加。目前,供應商提供三種模式的 SKU——USB、NFC 和藍牙——以涵蓋所有操作環境,防止通路競食,並提高硬體錢包市場的整體潛在佔有率。

早期用戶行為偏好熱錢包,在去中心化交易所的即插即用交換和挖礦獎勵的推動下,到2025年,熱錢包將佔據硬體錢包市場62.78%的佔有率。然而,2024年資產損失的消息促使託管機構加快向冷儲存的轉型。隨著董事會為每種託管模式分配量化風險評分,預計到2031年,冷儲存的複合年成長率將達到29.85%。這一趨勢正在推動硬體錢包市場中空氣間隙保險庫(包括安裝在地下的HSM機架,配備旨在抵禦物理入侵的安全元件刀片)的規模成長。

這種混合設計模糊了界限,允許在M/N法定人數核准下暫時暴露簽名權限的「溫」狀態,然後在清盤完成後恢復到冷狀態。這種可控的啟動方式符合以USDC支付工資並將儲備金離線儲存的資金管理策略。在新興資本市場監管中,MiCA將冷資料儲存視為儲備金檢驗的參考架構,進一步提升了對冷錢包的需求。透過這種轉型實現盈利的供應商獲得了更高的毛利率,並在硬體錢包市場保持了盈利能力,因為每個冷錢包SKU都配備了額外的法拉第籠套管、環氧樹脂密封的PCB以及用於完整顯示智慧合約調用數據的高像素盈利螢幕。

區域分析

預計到2025年,北美將佔據全球39.15%的市場佔有率,這主要得益於美國聯邦存款保險公司(OCC)的政策澄清,促使美國銀行整合硬體安全支付服務。強大的產權保護、深厚的保險實力以及充裕的創業投資投資,為Start-Ups快速迭代安全元件設計創造了有利環境,而機構投資者則透過嚴格的滲透測試檢驗這些產品。隨著資產管理公司以符合SOC-2管理標準的本地冷錢包庫取代綜合託管帳戶,硬體錢包市場也將從中受益。

預計到2031年,亞太地區將以29.66%的複合年成長率成長。新加坡金融管理局(MAS)將助記詞管理不當認定為重大營運風險,以及日本金融廳(FSA)強制要求隔離存儲,都推動了這一成長。國內組件製造商更短的前置作業時間和更低的成本,使得OneKey等品牌能夠以更低的平均售價提供開放原始碼產品,與西方競爭對手相媲美。消費者對超級應用的依賴推動了NFC和藍牙技術的普及,促使行動領先功能在該地區率先應用,隨後擴展到歐洲和北美,進一步增強了亞太地區對硬體錢包市場藍圖的影響力。

歐洲的MiCA框架正在將隱私優先的概念轉化為系統性的硬體應用,推動硬體市場在2031年前實現持續但相對緩慢的成長。法國是Ledger安全元件組裝線的位置,這反映了供應鏈回歸傳統模式以規避關稅和地緣政治風險的趨勢。同時,北歐退休基金正在遊說監管機構,允許在冷錢包中進行有限的加密貨幣配置,並要求儲備證明,從而進一步將安全硬體融入傳統的金融工作流程。這些區域性措施正在提高創新密度,並推動整個硬體錢包市場提升整體安全標準。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 機構採用自我管理解決方案的速度加快

- 網路安全漏洞事件曝光度的提高推動了對離線金鑰的需求。

- 促進隔離加密資產託管的監管(MiCA、OCC)

- 擴展 DeFi 和 NFT 生態系統需要多鏈支持

- 藍牙/NFC外形規格的興起推動了行動支付的發展

- 對中國製造的加密硬體徵收新的進口關稅可能會促進國內生產。

- 市場限制

- 反洗錢/了解你的客戶 (AML/KYC) 法規的不斷演變導致合規成本不斷增加

- 持久性消費者使用者體驗的複雜性

- 安全元件硬體供應鏈短缺

- 標準碎片化阻礙了互通性

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 硬體錢包對比

- 宏觀經濟因素評估

- 案例研究分析

第5章 市場規模與成長預測

- 連結性別

- USB

- NFC

- Bluetooth

- 其他

- 按錢包類型

- 熱錢包

- 冷錢包

- 最終用戶

- 個人/零售

- 對於企業/公司

- 透過分銷管道

- 線上

- 離線

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲地區

- 亞太其他地區

- 中國

- 日本

- 印度

- 澳洲

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Ledger SAS

- SatoshiLabs sro

- ShapeShift AG

- Coinkite Inc.

- CoolBitX Technology Ltd.

- Shift Crypto AG

- Penta Security Systems Inc.

- SecuX Technology Inc.

- ARCHOS SA

- ELLIPAL Ltd.

- BitLox Limited

- SafePal Technology Ltd.

- Keystone(Cobo Technology Ltd.)

- OPOLO SARL

- zSofitto NV(Sugi)

- KeepKey LLC

- IoTrust Co., Ltd.(D'CENT)

- Prokey Technologies Co., Ltd.

- CryoBit LLC

- BC VAULT doo

- Tangem AG

- OneKey Technology Co., Ltd.

第7章 市場機會與未來展望

The hardware wallet market was valued at USD 0.56 billion in 2025 and estimated to grow from USD 0.72 billion in 2026 to reach USD 2.58 billion by 2031, at a CAGR of 29.05% during the forecast period (2026-2031).

A sharp pivot by asset managers toward self-custody, an upsurge in high-profile exchange breaches, and clarity from frameworks such as MiCA and the OCC have together created a durable demand runway for the hardware wallet market. Enterprise clients now drive larger order values as they replace custodial accounts with on-premises key-management appliances, forcing formerly consumer-centric vendors to upgrade certification levels and professional-service offerings. The hardware wallet market also benefits from manufacturers localizing secure-element production after tariff shocks, and from multi-chain DeFi activity that rewards devices able to sign transactions across numerous layer-1 and layer-2 networks. Competitive conditions remain fluid because multi-year venture funding lets new entrants experiment with form factors, yet certification costs and supply-chain control continue to favor incumbents with deeper capital pools.

Global Hardware Wallet Market Trends and Insights

Intensifying Institutional Adoption of Self-Custody Solutions

Organizations now treat digital assets as treasury items rather than speculative holdings, so decision-makers reject omnibus custody in favor of deterministic control that satisfies board-level risk appetites. This change explains why the hardware wallet market increasingly revolves around FIPS-certified secure elements, REST-based signing stacks, and SOC-2 reporting layers. Dfns illustrates the shift by raising USD 16 million to scale wallet-as-a-service infrastructure that supports Fidelity International and Zodia Custody. Enterprise adoption raises average selling prices, lengthens replacement cycles, and nudges vendors toward subscription models bundling firmware updates, attestation services, and hardware warranties. In parallel, systems integrators extend device life by embedding wallets in HSM racks or zero-trust enclaves, widening the addressable hardware wallet market.

Surge in Cyber-Breach Publicity Pushing Demand for Offline Keys

Crypto theft reached signficantly, reigniting awareness of hot-wallet attack surfaces. Incidents at Bybit and Phemex triggered emergency asset migrations that overloaded consumer-grade devices, exposing feature gaps in backup verification and key-sharding workflows. Vendors responded by showcasing Common Criteria EAL5+ chips, epoxy-filled enclosures, and tamper-evident holograms that underline offline resilience. Marketing campaigns play on the cognitive impact of breach headlines, repeatedly framing air-gapped storage as the last line of defense between treasury assets and state-linked exploit groups. The resulting brand equity further entrenches device use among family offices and exchange-traded-product sponsors, expanding the hardware wallet market beyond technology enthusiasts.

Evolving AML/KYC Mandates Raising Compliance Costs

Regulators now ask hardware suppliers to embed mechanisms that flag sanctioned addresses, impose address-screening APIs, and log suspicious activity across device fleets. Implementing these functions adds firmware overhead, demands regular list updates, and exposes vendors to data-protection liability. Start-ups lacking legal teams often outsource compliance to cloud scorers, inflating unit economics and stretching working capital. Stringent cross-border export classifications for cryptographic modules further complicate logistics, delaying shipment into high-growth corridors and slowing the hardware wallet market momentum. Meanwhile, established manufacturers lean on pre-existing FATF audit files to maintain global reach at a lower marginal compliance outlay.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Push for Segregated Crypto Custody (MiCA, OCC)

- Expanding DeFi and NFT Ecosystems Requiring Multi-Chain Support

- Persistent Consumer UX Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

USB connectivity retained a 46.98% slice of the hardware wallet market in 2025, underpinned by its air-gapped lineage and minimal attack surface. NFC devices, however, are racing ahead at a 29.62% CAGR as consumers align crypto spending with contactless habits honed on Apple Pay and PayNow. Vendors like Arculus and Sugi shape the discussion by enclosing secure elements in sleek cards that slip into normal wallets, and by enabling tap-to-sign workflows that appeal to shoppers scanning QR codes at point-of-sale. The hardware wallet market size attributable to NFC is therefore expected to surge as super-apps in Southeast Asia enroll merchants that now accept stablecoin micropayments.

Institutional desks still prefer physical cables to reduce radio-frequency leakage and to preserve deterministic paths during SOC-2 audits. Even so, next-generation air-gap solutions adapt NFC in a stateless manner that permits external secure-element attestation without exposing private keys. Regulatory oversight may tilt further once standards bodies like ISO/TC 68 publish final guidelines on NFC-enabled custody. For now, vendors hedge bets by offering tri-modal SKUs, USB, NFC, and Bluetooth, to cover every operational context, thereby preventing channel cannibalization and growing their total addressable share of the hardware wallet market.

Hot wallets dominated early user behavior, grabbing 62.78% hardware wallet market share in 2025 thanks to plug-and-play swaps and decentralized-exchange farming incentives. Yet the asset-wipe headlines of 2024 have pushed fiduciaries toward cold environments that record a 29.85% CAGR through 2031 as boards assign quantitative risk scores to each custody model. That trend lifts the hardware wallet market size devoted to air-gapped vaults, including bunker-installed HSM racks equipped with secure-element blades designed to withstand physical intrusion.

Hybrid designs blur boundaries by allowing "warm" states that temporarily expose signing rights under M-of-N quorum approval, then revert to cold once sweeps finish. This controlled activation fits treasury playbooks that disburse payroll in USDC yet store reserves offline. In emerging capital-market mandates, MiCA interprets cold storage as the reference architecture for reserve verification, further amplifying unit demand. Vendors monetizing the shift receive elevated gross margins because every cold-wallet SKU ships with additional Faraday-cage sleeves, epoxy-sealed PCBs, and high-pixel-density screens required to display full-length smart-contract call data, sustaining profitability inside the hardware wallet market.

The Hardware Wallet Market Report is Segmented by Connectivity (USB, NFC, Bluetooth, and More), Wallet Type (Hot Wallet and Cold Wallet), End User (Individual/Retail and Institutional/Enterprise), Distribution Channel (Online and Offline), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 39.15% of 2025 value as OCC clarification prompted U.S. banks to integrate hardware-secured settlement services. High property-rights enforcement, deep insurance capacity, and significant venture capital pools create an ecosystem where start-ups iterate quickly on secure-element designs while institutional buyers validate those products through rigorous penetration tests. The hardware wallet market benefits when asset-managers replace omnibus custody accounts with on-premises cold-wallet cages that anchor SOC-2 controls.

Asia Pacific is on track for a 29.66% CAGR through 2031, accelerated by Singapore's MAS guidelines that label seed-phrase mis-management a critical operational risk and by Japan's FSA mandate for segregated custody. Domestic component manufacturers shorten lead times and lower costs, letting brands such as OneKey ship open-source units competitive with Western peers at lower ASPs. Consumers' dependence on super-apps cultivates NFC and Bluetooth deployment, so the region often previews mobile-first features that later migrate to Europe and North America, magnifying APAC's influence on the hardware wallet market roadmap.

Europe's MiCA framework translates privacy-first culture into systematic hardware adoption, driving consistent though comparatively moderate growth through 2031. France hosts Ledger's secure-element assembly lines, illustrating supply-chain reshoring designed to hedge tariff and geopolitical exposure. Simultaneously, Nordic pension funds lobby regulators to allow limited crypto allocations-conditional upon cold-wallet proof of reserves, which further embeds secure hardware in traditional finance workflows. Accordingly, regional dynamics enhance innovation density and push collective security standards higher across the hardware wallet market.

- Ledger SAS

- SatoshiLabs s.r.o.

- ShapeShift AG

- Coinkite Inc.

- CoolBitX Technology Ltd.

- Shift Crypto AG

- Penta Security Systems Inc.

- SecuX Technology Inc.

- ARCHOS S.A.

- ELLIPAL Ltd.

- BitLox Limited

- SafePal Technology Ltd.

- Keystone (Cobo Technology Ltd.)

- OPOLO SARL

- zSofitto NV (Sugi)

- KeepKey LLC

- IoTrust Co., Ltd. (D'CENT)

- Prokey Technologies Co., Ltd.

- CryoBit LLC

- BC VAULT d.o.o.

- Tangem AG

- OneKey Technology Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Intensifying institutional adoption of self-custody solutions

- 4.2.2 Surge in cyber-breach publicity pushing demand for offline keys

- 4.2.3 Regulatory push for segregated crypto custody (MiCA, OCC)

- 4.2.4 Expanding DeFi and NFT ecosystems requiring multi-chain support

- 4.2.5 Emergence of Bluetooth/NFC form-factors enabling mobile payments

- 4.2.6 New import tariffs on Chinese crypto hardware boosting on-shore production

- 4.3 Market Restraints

- 4.3.1 Evolving AML/KYC mandates raising compliance costs

- 4.3.2 Persistent consumer UX complexity

- 4.3.3 Hardware supply-chain shortages for secure elements

- 4.3.4 Fragmented standards hindering interoperability

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Hardware Wallet Product Comparison

- 4.8 Assessment of Macroeconomic Factors

- 4.9 Case Study Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Connectivity

- 5.1.1 USB

- 5.1.2 NFC

- 5.1.3 Bluetooth

- 5.1.4 Others

- 5.2 By Wallet Type

- 5.2.1 Hot Wallet

- 5.2.2 Cold Wallet

- 5.3 By End User

- 5.3.1 Individual / Retail

- 5.3.2 Institutional / Enterprise

- 5.4 By Distribution Channel

- 5.4.1 Online

- 5.4.2 Offline

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Rest of Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 Australia

- 5.5.4.5 Rest of Asia Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Ledger SAS

- 6.4.2 SatoshiLabs s.r.o.

- 6.4.3 ShapeShift AG

- 6.4.4 Coinkite Inc.

- 6.4.5 CoolBitX Technology Ltd.

- 6.4.6 Shift Crypto AG

- 6.4.7 Penta Security Systems Inc.

- 6.4.8 SecuX Technology Inc.

- 6.4.9 ARCHOS S.A.

- 6.4.10 ELLIPAL Ltd.

- 6.4.11 BitLox Limited

- 6.4.12 SafePal Technology Ltd.

- 6.4.13 Keystone (Cobo Technology Ltd.)

- 6.4.14 OPOLO SARL

- 6.4.15 zSofitto NV (Sugi)

- 6.4.16 KeepKey LLC

- 6.4.17 IoTrust Co., Ltd. (D'CENT)

- 6.4.18 Prokey Technologies Co., Ltd.

- 6.4.19 CryoBit LLC

- 6.4.20 BC VAULT d.o.o.

- 6.4.21 Tangem AG

- 6.4.22 OneKey Technology Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment