|

市場調查報告書

商品編碼

1907268

歐洲平板玻璃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Europe Flat Glass - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

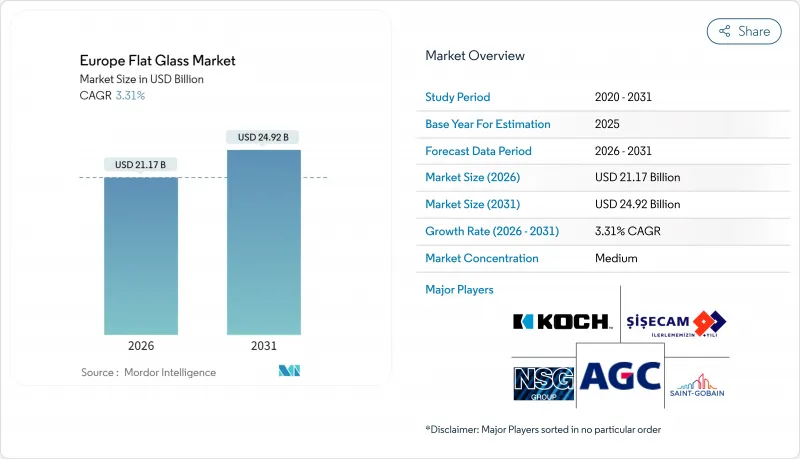

2025年歐洲平板玻璃市場價值為204.9億美元,預計到2031年將達到249.2億美元,而2026年為211.7億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 3.31%。

節能建築法規、輕量化車輛趨勢以及太陽能光電發電容量的不斷成長之間存在著密切的關聯,這正推動著歐洲平板玻璃市場的擴張。全部區域的建築商都在加速安裝低輻射(Low-E)玻璃和真空絕熱板,而汽車製造商則採用全景玻璃來減少碳排放並提升內裝美觀度。同時,歐洲太陽能光電發電的快速普及也帶動了對花紋玻璃和蓋板玻璃的需求,從而形成了一個不同於傳統建築週期的結構性成長平台。隨著歐盟排放交易體系(EU-ETS)第四階段碳價的調整重塑了成本曲線,製造商正在投資建造電爐和氫氣爐,以控制波動較大的堿灰和天然氣成本。在所有終端應用領域,歐洲平板玻璃市場都受益於監管政策的利好,高性能玻璃已成為一項合規要求,而非可選項。

歐洲平板玻璃市場趨勢與洞察

歐洲各地建築和建築幕牆維修增加

基礎建設項目和商業維修正在推動2024年需求下滑後的復甦。西門子已獲得240億歐元的智慧基礎設施訂單,其中大部分與採用三層中空玻璃的節能建築外圍護結構相關。丹麥頂級辦公大樓投資者優先考慮符合ESG(環境、社會和治理)標準的維修,從而推高了對低輻射(Low-E)玻璃的需求。在法國和義大利,老舊住宅存量也正進入維修週期,強制要求U值低於1.0 W/m²K。儘管不斷上漲的建築成本抑制了新建項目,但這一趨勢仍提振了歐洲平板玻璃市場的基準需求。產品線中包含鍍膜玻璃和真空中空玻璃的製造商最能掌握這股監管需求浪潮。

歐盟27個國家汽車輕量化和全景玻璃的應用

汽車製造商正用多面板全景玻璃模組取代鋼製車頂面板,以減輕重量並提高純電動車的續航里程。 Webasto 和 Gosey 的全景車頂銷量均實現了兩位數成長,而 AGC 已將用於抬頭顯示器的擴增實境(AR) 擋風玻璃商業化。加熱、整合天線和隔音貼合加工玻璃具有高附加價值利潤,從而推動了對加工玻璃的需求。隨著空氣動力學法規的日益嚴格,商用車製造商也遵循著類似的發展軌跡。這些趨勢共同推動了每輛車每平方公尺平均消耗量的增加,增強了在汽車生產整體疲軟的情況下,市場對玻璃的韌性。

歐盟排放第四階段的高電力消耗與碳價格

第四階段,免費配額將減少,預計2025年碳成本將超過85歐元/噸二氧化碳。由於平板玻璃熔煉是單位增加價值額排放最高的三大工業部門之一,製造商將透過電費承擔直接和間接的碳成本。與低碳價格地區進口產品的競爭差距日益擴大,導致人們越來越呼籲引入碳邊境調節措施。對富氧燃燒器、太陽能熔塊窯和氫氣測試的投資旨在確保資產的未來適用性,但對於所有營運商而言,數年的投資回收期並不現實。

細分市場分析

在歐洲平板玻璃市場,退火基板預計到2025年將佔總價值的51.88%。日益嚴格的法規正在推動加工玻璃品類的成長。強化玻璃和夾層玻璃符合安全標準,而雙層玻璃則符合低輻射(Low-E)法規。採用軟鍍銀層的塗裝解決方案可增強隔熱性能,並可降低20%的空調負荷。鏡子在家具產業仍保持一定的市場需求,但其價格仍受消費者支出週期的影響。

隨著製造商不斷推進技術創新,加工玻璃的產量已超過商用浮法玻璃。 Secak 的曲面強化玻璃生產線能夠生產 6.5 公尺長的玻璃面板,為機場和博物館等項目提供更大的設計自由度。 Leesec 的機器人分類技術可減少廢棄物,並將厚度偏差控制在 ±0.1 毫米以內,達到三單元組裝所需的精確度。自動化也有助於提高可追溯性,為眾多金融機構所需的 ESG審核提供支援。這些創新增強了歐洲相對於低成本進口產品的競爭優勢。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 歐洲各地建築和建築幕牆維修增加

- 歐盟27個成員國汽車輕量化與全景玻璃應用趨勢

- 太陽能發電裝置容量的快速成長正在推動對太陽能玻璃和花紋玻璃的需求。

- 歐盟「維修浪潮」補貼(針對低輻射玻璃和真空絕熱玻璃)

- 建築一體成型光伏(BIPV)帷幕牆的興起

- 市場限制

- 堿灰、矽砂和天然氣的價格波動

- 歐盟排放第四階段下的高電力消耗量與碳價格

- 大型中空玻璃產品現場安裝技能短缺問題日益凸顯

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 依產品類型

- 退火(包括著色)

- 塗層(低輻射,隔熱)

- 反射玻璃

- 加工產品(強化玻璃、夾層玻璃、雙層玻璃)

- 鏡子

- 按最終用戶行業分類

- 建築/施工

- 車

- 太陽能和光伏發電

- 家具和室內裝飾

- 其他(家用電器、鐵路、船舶)

- 按地區

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 波蘭

- 比荷盧經濟聯盟

- 北歐國家(瑞典、挪威、丹麥、芬蘭)

- 其他歐洲地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率/排名分析

- 公司簡介

- AGC Inc.

- AGP Group

- Ardagh Group SA,

- Bohle AG

- Euroglas

- Interpane Glas Industrie AG

- Koch Industries

- Nippon Sheet Glass Co., Ltd.

- OGIS GmbH

- Press Glass SA

- Saint-Gobain

- SCHOTT

- Sisecam

- Vitro

第7章 市場機會與未來展望

The Europe Flat Glass Market was valued at USD 20.49 billion in 2025 and estimated to grow from USD 21.17 billion in 2026 to reach USD 24.92 billion by 2031, at a CAGR of 3.31% during the forecast period (2026-2031).

The strong correlation between energy-efficient construction regulations, vehicle lightweighting trends, and solar-photovoltaic capacity additions underpins this expansion of the Europe flat glass market. Builders across the region are accelerating the installation of low-emissivity (low-E) and vacuum-insulated units, while automakers are embedding panoramic glazing to cut carbon emissions and improve cabin aesthetics. Simultaneously, Europe's accelerating solar roll-out fuels demand for patterned and cover glass, creating a structural growth pillar distinct from conventional construction cycles. Producers are mitigating volatile soda-ash and natural-gas costs by investing in electric and hydrogen furnaces, even as EU-ETS Phase IV carbon prices reshape cost curves. Across every end-use, the Europe flat glass market benefits from regulatory tailwinds that make high-performance glazing a compliance necessity rather than a discretionary upgrade.

Europe Flat Glass Market Trends and Insights

Increasing Construction and Facade Renovation Across Europe

Infrastructure programs and commercial retrofits are reviving demand after the 2024 downturn. Siemens booked EUR 24 billion of smart-infrastructure orders in 2024, much of it tied to energy-efficient building envelopes that specify triple-insulated glazing. Danish prime office investors prioritize ESG-aligned refurbishments, translating to higher volumes of low-E units. Older housing stock in France and Italy is also entering a mandated upgrade cycle that prescribes U-values below 1.0 W/m2K. This dynamic lifts baseline volumes for the Europe flat glass market, even as high construction costs temper new-build activity. Producers with coated and vacuum-insulated portfolios are best positioned to capture this compliance-driven wave.

Automotive Lightweighting and Panoramic Glazing Adoption in EU-27 Vehicle Platforms

OEMs are replacing steel roof panels with multi-panel panoramic glass modules that cut weight and improve battery-electric range. Webasto and Gauzy report double-digit growth in panoramic roofs, while AGC has commercialized augmented-reality windshields for heads-up displays. Heated, antenna-embedded, and acoustic laminates command premium margins and push processed-glass demand higher. Commercial-vehicle makers follow the same trajectory as aerodynamic regulations tighten. These trends collectively widen average square-meter consumption per vehicle, reinforcing demand resilience when broader auto output softens.

High Electricity Intensity and Carbon Pricing Under EU-ETS Phase IV

Phase IV allocates fewer free allowances, lifting carbon costs above EUR 85/tCO2 in 2025. Flat-glass melting ranks among the top three industrial emitters per USD of value added, so producers pay both direct and indirect carbon charges via power tariffs. The competitive gap versus imports from low-carbon-price regions widens, raising calls for carbon-border adjustments. Investments in oxy-fuel burners, photovoltaic-powered frit kilns, and hydrogen trials aim to future-proof assets but require multi-year paybacks that not all operators can absorb.

Other drivers and restraints analyzed in the detailed report include:

- Surging Solar-PV Capacity Additions Driving Demand for Solar and Pattern Glass

- EU "Renovation Wave" Subsidies for Low-E and Vacuum-Insulated Glazing

- New Skill Gap for On-Site Installation of Oversized Insulated Glazing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Europe flat glass market size attributable to annealed substrates reached 51.88% of the total value in 2025. Regulatory upgrades steer growth into processed categories. Tempered and laminated panes meet safety codes, while insulated units satisfy low-E mandates. Coated solutions incorporating soft-coat silver layers add solar-control functionality that can cut HVAC loads by 20%. Mirrors maintain niche uptake in furniture, yet remain tied to broader consumer spending cycles.

Processed glass volumes outpace commodity float because producers continually push the technology frontier. Sedak's curved-tempering line fabricates 6.5 m panels, unlocking design latitude for airports and museums. LiSEC's robotic sorting shrinks waste and delivers pane thickness variance within +-0.1 mm, a metric critical for triple-unit assemblies. Automation also improves traceability, aiding ESG audits now required by many lenders. These innovations fortify European competitive advantage against lower-cost imports.

The Europe Flat Glass Market Report is Segmented by Product Type (Annealed, Coated, Reflective, Processed, Mirrors), End-User Industry (Building and Construction, Automotive, Solar and Photovoltaic, Furniture and Interior Decor, Others), and Geography (Germany, United Kingdom, France, Italy, Spain, Poland, Benelux, Nordics, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- AGC Inc.

- AGP Group

- Ardagh Group S.A,

- Bohle AG

- Euroglas

- Interpane Glas Industrie AG

- Koch Industries

- Nippon Sheet Glass Co., Ltd.

- OGIS GmbH

- Press Glass SA

- Saint-Gobain

- SCHOTT

- Sisecam

- Vitro

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing construction and facade renovation across Europe

- 4.2.2 Automotive lightweighting and panoramic glazing adoption in EU-27 vehicle platforms

- 4.2.3 Surging solar-PV capacity additions driving demand for solar and pattern glass

- 4.2.4 EU "Renovation Wave" subsidies for low-E and vacuum-insulated glazing

- 4.2.5 Rise of building-integrated-photovoltaic (BIPV) curtain-walls

- 4.3 Market Restraints

- 4.3.1 Volatile soda-ash, silica-sand and natural-gas prices

- 4.3.2 High electricity intensity and carbon-pricing under EU-ETS Phase IV

- 4.3.3 New skill-gap for on-site installation of oversized insulated glazing

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Annealed (incl. Tinted)

- 5.1.2 Coated (low-E, solar-control)

- 5.1.3 Reflective

- 5.1.4 Processed (tempered, laminated, IGU)

- 5.1.5 Mirrors

- 5.2 By End-user Industry

- 5.2.1 Building and Construction

- 5.2.2 Automotive

- 5.2.3 Solar and Photovoltaic

- 5.2.4 Furniture and Interior Decor

- 5.2.5 Others (appliances, rail, marine)

- 5.3 By Geography

- 5.3.1 Germany

- 5.3.2 United Kingdom

- 5.3.3 France

- 5.3.4 Italy

- 5.3.5 Spain

- 5.3.6 Poland

- 5.3.7 Benelux

- 5.3.8 Nordics (Sweden, Norway, Denmark, Finland)

- 5.3.9 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share**/Ranking Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AGC Inc.

- 6.4.2 AGP Group

- 6.4.3 Ardagh Group S.A,

- 6.4.4 Bohle AG

- 6.4.5 Euroglas

- 6.4.6 Interpane Glas Industrie AG

- 6.4.7 Koch Industries

- 6.4.8 Nippon Sheet Glass Co., Ltd.

- 6.4.9 OGIS GmbH

- 6.4.10 Press Glass SA

- 6.4.11 Saint-Gobain

- 6.4.12 SCHOTT

- 6.4.13 Sisecam

- 6.4.14 Vitro

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

2026年全球平板玻璃市場報告

2026年全球平板玻璃市場報告 平板玻璃製造機械市場:依產品類型、機器類型、技術、原料、產能和最終用途分類-全球預測,2026-2032年

平板玻璃製造機械市場:依產品類型、機器類型、技術、原料、產能和最終用途分類-全球預測,2026-2032年 平板玻璃市場規模、佔有率、趨勢和預測:按技術、產品類型、原料、應用、類別、最終用途行業和地區分類,2026-2034年

平板玻璃市場規模、佔有率、趨勢和預測:按技術、產品類型、原料、應用、類別、最終用途行業和地區分類,2026-2034年 平板玻璃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本平板玻璃市場報告(按技術、產品類型、最終用途行業和地區分類,2026-2034年)

平板玻璃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本平板玻璃市場報告(按技術、產品類型、最終用途行業和地區分類,2026-2034年) 平板玻璃市場規模、佔有率和成長分析(按產品類型、技術、終端用戶產業和地區分類)-2026-2033年產業預測

平板玻璃市場規模、佔有率和成長分析(按產品類型、技術、終端用戶產業和地區分類)-2026-2033年產業預測 全球平板玻璃市場分析,市場規模(2025-2034 年)彎玻璃市場按產品類型、厚度、彎角、應用和分銷管道分類-2025-2030 年全球預測

全球平板玻璃市場分析,市場規模(2025-2034 年)彎玻璃市場按產品類型、厚度、彎角、應用和分銷管道分類-2025-2030 年全球預測 平板玻璃加工機械市場-全球產業規模、佔有率、趨勢、機會及預測(按機械類型、最終用戶產業、玻璃類型、自動化程度、地區及競爭情況分類,2020-2030 年預測)

平板玻璃加工機械市場-全球產業規模、佔有率、趨勢、機會及預測(按機械類型、最終用戶產業、玻璃類型、自動化程度、地區及競爭情況分類,2020-2030 年預測) 2030 年全球平板玻璃市場按技術(浮法、捲材、板材)、類型(基本浮法、強化玻璃、鍍膜、夾層、超白)和最終用戶行業(建築和基礎設施、汽車和運輸、太陽能)分類

2030 年全球平板玻璃市場按技術(浮法、捲材、板材)、類型(基本浮法、強化玻璃、鍍膜、夾層、超白)和最終用戶行業(建築和基礎設施、汽車和運輸、太陽能)分類