|

市場調查報告書

商品編碼

1907258

異氰酸酯:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Isocyanates - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

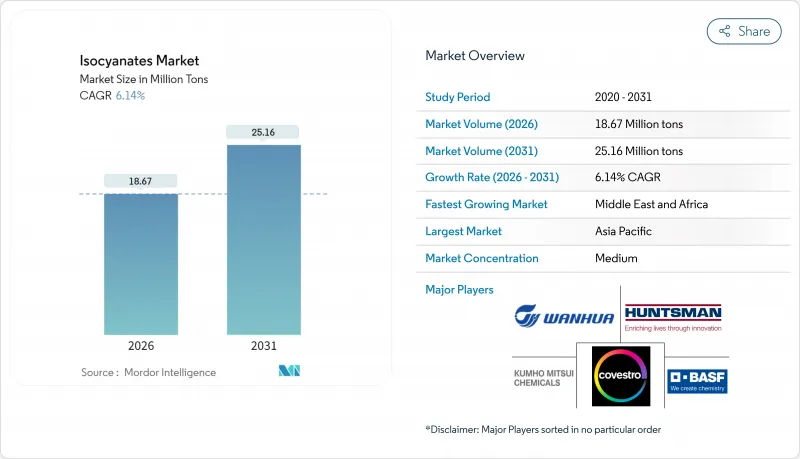

預計到 2026 年,異氰酸酯市場規模將達到 1,867 萬噸,高於 2025 年的 1,759 萬噸。預計到 2031 年將達到 2,516 萬噸,2026 年至 2031 年的複合年成長率為 6.14%。

這一成長軌跡反映了高性能聚氨酯系統的日益普及、供應端的整合以及有利於垂直整合生產商的日益嚴格的環境法規。隨著保溫標準的提高,對硬質泡棉的需求依然強勁,同時輕型汽車也推動了建築應用以外特種泡沫的需求。一體化的原料策略、貿易政策的轉變以及向高脂肪族化學品的轉型,進一步塑造了異氰酸酯市場的競爭格局。

全球異氰酸酯市場趨勢與洞察

建築隔熱材料領域對硬質聚氨酯泡棉的需求激增

2024 年國際建築規範修訂版要求對含有可燃隔熱材料的外牆組裝進行 NFPA 285 防火測試,這使得成熟的異氰酸酯基系統成為設計師的低風險選擇。聚異氰酸酯板材的導熱係數極低,僅為 0.018 W/m*K,與空間受限的維修中使用的礦棉相比,可實現更薄的牆體組裝。各州能源規範擴大引用 ASHRAE 90.1 標準,要求建築商在現有建築圍護結構中達到使用硬質聚氨酯所能實現的高隔熱性能(R 值)。隨著現有建築進行維修以達到淨零排放目標,這推動了異氰酸酯市場的發展。此外,全球綠色建築認證專案更傾向於選擇具有成熟生命週期資料的材料,這使得 MDI 基泡棉材料具有額外的相容性優勢。

亞太地區的快速工業化與都市化

東南亞國家正將製造地拓展至中國以外,從而創造了MDI和TDI的新區域需求。在越南、泰國和印尼設有生產基地的製造商既能滿足不斷成長的本地消費需求,又能降低地緣政治因素帶來的供應鏈風險。東曹在越南的年產13萬噸MDI工廠便是這種多元化策略的典範。東協大規模城市住宅和交通計劃推動了對隔熱材料、密封劑和複合板的需求,而這些產品都依賴異氰酸酯化學。收入水準的提高以及耐用品(尤其是床墊和家用電器)消費的成長,也推動了對柔軟性泡棉材料的穩定需求。儘管其他地區的出口成長放緩,但這些結構性變化使得異氰酸酯市場得以保持多年的成長勢頭。

苯和硝基苯原料價格波動

由於苯是MDI和TDI的主要芳烴前驅物,原油價格與石腦油價格的掛鉤上漲會直接影響異氰酸酯的生產成本。亞洲現貨苯價格波動劇烈,迫使生產商啟用月度價格調整條款,並降低了買家對價格的預期。無法追溯取得芳烴原料的非一體化轉化企業利潤率壓縮最為迅速,促使企業進行垂直整合並簽署長期承購協議。庫存策略已演變為對沖至少三個月的需求以降低波動性,但這會佔用營運資金並增加持有成本。因此,當原料價格不確定時,合成商會延後訂單,抑制近期消費成長。

細分市場分析

到2025年,MDI將佔據異氰酸酯市場58.75%的佔有率,這主要得益於其在硬質發泡體和複合材料配方中的多功能性,滿足了高需求建築和工業應用的需求。同時,脂肪族異氰酸酯的複合年成長率(CAGR)為6.72%,超過了整體異氰酸酯市場的成長速度。具有紫外線穩定性的HDI和IPDI正在滲透到汽車透明塗層和風力發電機葉片樹脂系統中,這些產品因其長期耐久性而價格較高。 TDI在床上用品和家具行業的需求仍然強勁,但隨著該領域日趨成熟,以及來自黏彈性MDI體系的競爭壓力加劇,其成長速度正在放緩。特種嵌段和預聚物變體透過針對較低的產量、電子封裝、船舶塗料和航太複合材料等領域,提供了更高的利潤空間。

隨著汽車和可再生能源行業的原始設備製造商 (OEM) 對耐久性的要求不斷提高,而芳香族化學品難以達到這些標準,脂肪族異氰酸酯的市場規模預計將穩步擴大。為因應北美和歐洲可能出現的本地採購限制,生產商正在投資建造更多的 HDI 單體生產線,以縮短下游聚異氰酸酯生產的供應鏈。同時,MDI 供應商也在提高產量,以消除瓶頸並維持成本優勢,這凸顯了一種雙軌投資策略,即在商品規模和高附加價值特種產品之間取得平衡。

本異氰酸酯市場報告按類型(MDI、TDI、脂肪族、其他)、應用(硬質泡沫、軟質泡沫、油漆和塗料、黏合劑和密封劑等)、終端用戶行業(建築和施工、汽車、醫療、家具、其他終端用戶等)以及地區(亞太地區、北美、歐洲等)進行分析。市場預測以噸為單位。

區域分析

到2025年,亞太地區將佔據異氰酸酯市場46.85%的佔有率。這一主導地位主要得益於中國以苯為主導的MDI生產體係以及東南亞新興的製造地,這些基地能夠為區域加工商提供更快的交貨速度。在中國,隨著排放法規的排放嚴格,中小型工廠的整合使得生產集中在規模更大的企業手中,這些企業既能利用規模經濟,又能實現環保目標。越南和印尼的下游叢集也在擴大硬質發泡體和鞋類產品的生產,從而強化了自我維持的需求循環,使其不易受出口波動的影響。

北美憑藉其以頁岩氣為主的原料供應以及接近性汽車和建築行業的地理優勢,佔據關鍵地位,而這兩個行業正是聚氨酯消費的主要支撐。BASF在路易斯安那州蓋斯馬的持續擴建計畫將使該地區的MDI名義產能於2026年達到約60萬噸/年,從而確保不斷成長的電動車產能所需的充足供應。貿易政策的不確定性,例如美國國際貿易委員會(USITC)將於2025年對中國MDI展開反傾銷調查,促使企業採用雙重採購模式,並支持國內工廠的運轉率。儘管歐洲技術先進,但遵守REACH法規的成本正迫使中小加工商從海外採購原料,儘管對保溫維修的需求持續存在,但這在一定程度上減緩了該地區的成長前景。

預計中東和非洲將成為該地區成長最快的市場,到2031年複合年成長率將達到6.25%,主要得益於各國政府對大型基礎建設計劃和石化自給自足計劃的資金投入。國營企業正利用低成本的丙烷脫氫和苯萃取技術,為MDI和TDI整合裝置提供原料。智慧城市和醫療綜合體的建設,尤其是在波灣合作理事會(GCC)國家,正在推動對高性能隔熱材料和密封劑的需求,進一步擴大該地區異氰酸酯市場規模的成長。在阿曼和沙烏地阿拉伯擁有資產的生產商還可以逆向整合到基礎芳烴領域,從而在全球苯價格波動的情況下提高利潤率。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 建築隔熱材料用硬質聚氨酯泡棉的需求激增

- 亞太地區的快速工業化與都市化

- 輕量化汽車趨勢推動聚氨酯複合材料的應用

- 低溫運輸和電子商務包裝的成長

- 利用異氰酸酯複合材料製造風力發電機葉片

- 市場限制

- 苯和硝基苯原料價格波動;

- 歐盟REACH法規訓練與分類障礙

- 中國環境法規導致停產,造成供應受限

- 價值鏈分析

- 監管環境

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 價格趨勢

第5章 市場規模與成長預測

- 按類型

- MDI

- TDI

- 脂肪族(例如 HDI、IPDI)

- 其他類型

- 透過使用

- 硬發泡塑膠

- 軟性泡沫

- 油漆和塗料

- 黏合劑和密封劑

- 彈性體

- 活頁夾

- 其他用途

- 按最終用戶行業分類

- 建築/施工

- 車

- 衛生保健

- 家具

- 其他終端使用者(航太、電子、船舶)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 泰國

- 印尼

- 越南

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 土耳其

- 埃及

- 奈及利亞

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率/排名分析

- 公司簡介

- Anderson Development Company

- Asahi Kasei Chemicals

- BASF SE

- BorsodChem

- Chemtura Corp.

- China National Bluestar(Group)Co. Ltd.

- Covestro AG

- Dow Inc.

- Evonik Industries

- Huntsman Corporation LLC

- Kemipex

- Korea Fine Chemical Co. Ltd.

- Kumho

- MITSUI CHEMICALS AMERICA INC.

- Perstorp

- Tosoh Corporation

- Vencorex

- Wanhua Chemical Group Co. Ltd.

第7章 市場機會與未來展望

Isocyanates market size in 2026 is estimated at 18.67 million tons, growing from 2025 value of 17.59 million tons with 2031 projections showing 25.16 million tons, growing at 6.14% CAGR over 2026-2031.

This trajectory reflects escalating adoption of high-performance polyurethane systems, supply-side consolidation, and tightening environmental regulations that reward vertically integrated producers. Rigid foam maintains momentum as efficiency standards raise thermal-insulation baselines, while automotive lightweighting broadens specialized demand beyond strictly construction uses. Integrated feedstock strategies, trade-policy shifts, and a pivot toward premium aliphatic chemistries further shape competitive positioning within the isocyanates market.

Global Isocyanates Market Trends and Insights

Surging Demand for Rigid PU Foam in Building Insulation

Revisions to the 2024 International Building Code mandate NFPA 285 fire testing for exterior wall assemblies that contain combustible insulation, making proven isocyanate-based systems the low-risk route for specifiers. Polyisocyanurate boards offer thermal conductivity as low as 0.018 W/m*K, allowing for thinner wall assemblies compared to mineral wool in retrofit settings where space is limited. State energy codes now cite ASHRAE 90.1 more frequently, pushing builders to higher R-values that rigid polyurethane can achieve within existing envelopes. The isocyanates market, therefore, benefits from retro-demand as older structures upgrade to meet net-zero targets. Global green-building certifications also favor materials with established life-cycle data, giving MDI-based foams a further compliance edge.

Rapid Industrialization and Urbanization in APAC

Southeast Asian economies are scaling manufacturing bases beyond China, creating new intra-regional demand pools for MDI and TDI. Producers with units in Vietnam, Thailand, and Indonesia can meet the rising local consumption while mitigating geopolitical-driven supply-chain risks. Tosoh's 130,000-tpy MDI plant in Vietnam exemplifies this diversification strategy. Large-scale urban housing and transportation projects across ASEAN are driving demand for insulation, sealants, and composite panels, all of which rely on isocyanate chemistries. As income levels rise, consumption of durable goods-especially mattresses and appliances-drives steady demand for flexible foam. These structural shifts keep the isocyanates market on a multi-year growth path, irrespective of export softness elsewhere.

Volatile Benzene and Nitro-Benzene Feedstock Pricing

Benzene is the primary aromatic precursor for both MDI and TDI, so any spike in crude-linked naphtha values cascades directly into isocyanate manufacturing costs. Spot benzene in Asia swung, forcing producers to issue monthly price-adjustment clauses that eroded buyer visibility. Margins compress fastest for non-integrated converters that lack backward links to aromatics, encouraging vertical integration or long-term offtake contracts. Inventory strategies are evolving toward hedged positions that cover at least three months of demand to cushion volatility; however, this ties up working capital and raises carrying costs. The net result is a dampening effect on short-term consumption growth as formulators delay orders when the feedstock price direction is unclear.

Other drivers and restraints analyzed in the detailed report include:

- Lightweight Vehicle Trend Driving PU Composites Adoption

- Cold-Chain and E-Commerce Packaging Growth

- EU REACH Training and Classification Hurdles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

MDI held a 58.75% market share of the isocyanates market in 2025, backed by its versatility in rigid foam and composite formulations that serve high-volume construction and industrial applications. At the same time, aliphatic isocyanates are tracking a 6.72% CAGR that outpaces the overall isocyanates market, with UV-stable HDI and IPDI penetrating automotive clearcoat and wind-blade resin systems where long-term durability commands premium prices. TDI demand remains resilient in bedding and furniture, but growth is slower as the segment reaches maturity and competitive pressure from viscoelastic MDI systems intensifies. Specialty blocked and pre-polymer variants, while low volume, offer elevated margins by targeting electronics encapsulation, marine coatings, and aerospace composites.

The isocyanates market size for aliphatic grades is set to climb steadily as OEM specifications in both automotive and renewable-energy sectors pivot to durability metrics that aromatic chemistries struggle to meet. Producers are investing in additional HDI monomer loops to shorten supply chains for downstream polyisocyanate production, anticipating regional content rules in North America and Europe. Meanwhile, MDI suppliers are adding capacity to address bottlenecks to retain cost leadership, highlighting a dual-track investment landscape that balances commodity scale with specialty value capture.

The Isocyanates Market Report is Segmented by Type (MDI, TDI, Aliphatic, and Other Types), Application (Rigid Foam, Flexible Foam, Paints and Coatings, Adhesives and Sealants, and More), End-User Industry (Building and Construction, Automotive, Healthcare, Furniture, and Other End-Users), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific accounted for 46.85% of the isocyanates market share in 2025, a lead secured by China's benzene-advantaged MDI complexes and Southeast Asia's emerging manufacturing corridors that shorten delivery times to regional converters. The consolidation of smaller Chinese plants under stricter emissions regulations is driving volume toward large operators that can leverage economies of scale while meeting environmental targets. Vietnamese and Indonesian downstream clusters are also scaling rigid-foam and footwear production, reinforcing a self-sustaining demand loop that cushions the region from export swings.

North America holds a significant position, benefiting from shale-advantaged feedstock and proximity to the automotive and construction sectors, which anchor polyurethane consumption. BASF's ongoing expansion at Geismar, Louisiana, will lift regional MDI nameplate capacity to roughly 600,000 t/y in 2026, ensuring supply sufficiency as electric-vehicle output scales. Trade-policy uncertainty, exemplified by the 2025 USITC antidumping probe into Chinese MDI, encourages dual sourcing and supports domestic plant utilization. Europe, while technologically advanced, contends with REACH training costs that nudge smaller converters toward offshore sourcing, modestly softening local growth prospects despite continued retro-insulation activity.

The Middle-East and Africa are projected to experience the fastest regional expansion at a 6.25% CAGR to 2031, as governments fund mega-infrastructure projects and petrochemical self-sufficiency programs. State-backed players leverage low-cost propane dehydrogenation and benzene extraction to feed integrated MDI and TDI units. The construction of smart cities and healthcare complexes-particularly in the Gulf Cooperation Council-drives demand for high-performance insulation and sealants, further amplifying the regional isocyanates market size trajectory. Producers with assets in Oman and Saudi Arabia can also back-integrate into basic aromatics, enhancing margin capture under volatile global benzene pricing.

- Anderson Development Company

- Asahi Kasei Chemicals

- BASF SE

- BorsodChem

- Chemtura Corp.

- China National Bluestar (Group) Co. Ltd.

- Covestro AG

- Dow Inc.

- Evonik Industries

- Huntsman Corporation LLC

- Kemipex

- Korea Fine Chemical Co. Ltd.

- Kumho

- MITSUI CHEMICALS AMERICA INC.

- Perstorp

- Tosoh Corporation

- Vencorex

- Wanhua Chemical Group Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand for rigid PU foam in building insulation

- 4.2.2 Rapid industrialization and urbanization in APAC

- 4.2.3 Lightweight vehicle trend driving PU composites adoption

- 4.2.4 Cold-chain and e-commerce packaging growth

- 4.2.5 Wind-turbine blade production using isocyanate composites

- 4.3 Market Restraints

- 4.3.1 Volatile benzene and nitro-benzene feedstock pricing

- 4.3.2 EU REACH training and classification hurdles

- 4.3.3 Supply tightness from China environmental shutdowns

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Degree of Competition

- 4.7 Price Trend

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 MDI

- 5.1.2 TDI

- 5.1.3 Aliphatic (e.g., HDI, IPDI)

- 5.1.4 Other Types

- 5.2 By Application

- 5.2.1 Rigid Foam

- 5.2.2 Flexible Foam

- 5.2.3 Paints and Coatings

- 5.2.4 Adhesives and Sealants

- 5.2.5 Elastomers

- 5.2.6 Binders

- 5.2.7 Other Applications

- 5.3 By End-user Industry

- 5.3.1 Building and Construction

- 5.3.2 Automotive

- 5.3.3 Healthcare

- 5.3.4 Furniture

- 5.3.5 Other End-users (Aerospace, Electronics, Marine)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Nordic Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Qatar

- 5.4.5.4 Turkey

- 5.4.5.5 Egypt

- 5.4.5.6 Nigeria

- 5.4.5.7 South Africa

- 5.4.5.8 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Anderson Development Company

- 6.4.2 Asahi Kasei Chemicals

- 6.4.3 BASF SE

- 6.4.4 BorsodChem

- 6.4.5 Chemtura Corp.

- 6.4.6 China National Bluestar (Group) Co. Ltd.

- 6.4.7 Covestro AG

- 6.4.8 Dow Inc.

- 6.4.9 Evonik Industries

- 6.4.10 Huntsman Corporation LLC

- 6.4.11 Kemipex

- 6.4.12 Korea Fine Chemical Co. Ltd.

- 6.4.13 Kumho

- 6.4.14 MITSUI CHEMICALS AMERICA INC.

- 6.4.15 Perstorp

- 6.4.16 Tosoh Corporation

- 6.4.17 Vencorex

- 6.4.18 Wanhua Chemical Group Co. Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

異氰酸酯市場:2026-2032年全球市場預測(按類型、製造技術、分銷管道、應用和最終用戶分類)苯基甲烷二異氰酸酯市場:依產品類型、形態、應用和分銷管道分類-2026-2032年全球市場預測

異氰酸酯市場:2026-2032年全球市場預測(按類型、製造技術、分銷管道、應用和最終用戶分類)苯基甲烷二異氰酸酯市場:依產品類型、形態、應用和分銷管道分類-2026-2032年全球市場預測 全球異氰酸酯市場(至2030年):按類型(MDI、TDI、脂肪族)、應用(發泡體、黏合劑和密封劑、塗料)、終端用戶產業(汽車、建築施工、家具和床上用品、消費品、工業塗料)和地區分類

全球異氰酸酯市場(至2030年):按類型(MDI、TDI、脂肪族)、應用(發泡體、黏合劑和密封劑、塗料)、終端用戶產業(汽車、建築施工、家具和床上用品、消費品、工業塗料)和地區分類 異氰酸酯全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)

異氰酸酯全球市場規模、佔有率、趨勢和成長分析報告(2026-2034) 異氰酸酯市場規模、佔有率和成長分析(按類型、應用、終端用戶產業和地區分類)-2026-2033年產業預測

異氰酸酯市場規模、佔有率和成長分析(按類型、應用、終端用戶產業和地區分類)-2026-2033年產業預測 2026-2030年全球二異氰酸酯和多異氰酸酯市場脂肪族聚異氰酸酯市場按類型、產品形式、應用和最終用途產業分類,全球預測(2026-2032年)苯基異氰酸酯市場按產品類型、形態、應用、終端用戶產業和分銷管道分類-2026-2032年全球預測

2026-2030年全球二異氰酸酯和多異氰酸酯市場脂肪族聚異氰酸酯市場按類型、產品形式、應用和最終用途產業分類,全球預測(2026-2032年)苯基異氰酸酯市場按產品類型、形態、應用、終端用戶產業和分銷管道分類-2026-2032年全球預測 美國異氰酸酯市場規模、佔有率和趨勢分析報告:按來源、類型、傳統最終用途、生物基最終用途和細分市場預測(2025-2033 年)

美國異氰酸酯市場規模、佔有率和趨勢分析報告:按來源、類型、傳統最終用途、生物基最終用途和細分市場預測(2025-2033 年) 脂肪族異氰酸酯:全球市場佔有率和排名、總收入和需求預測(2025-2031年)

脂肪族異氰酸酯:全球市場佔有率和排名、總收入和需求預測(2025-2031年)