|

市場調查報告書

商品編碼

1907252

高光譜影像:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Hyperspectral Imaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

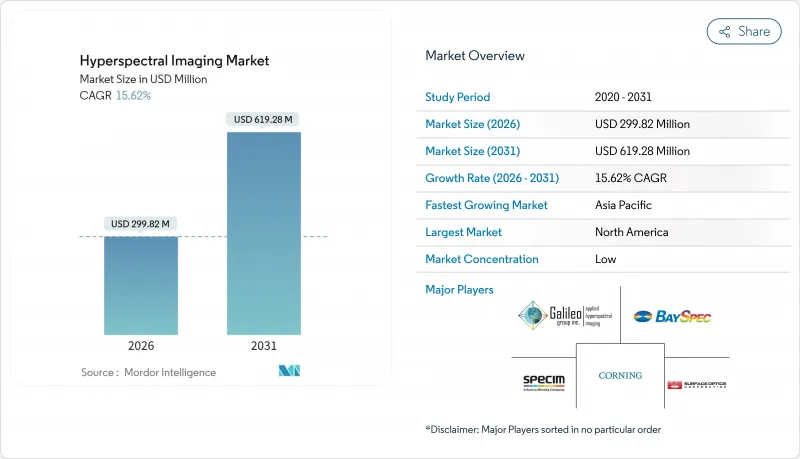

預計到 2026 年,高光譜影像市場規模將達到 2.9982 億美元,高於 2025 年的 2.593 億美元,預計到 2031 年將達到 6.1928 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 15.62%。

可見光近紅外線/短波紅外線感測器價格的下降、美國國防部天衛星群計畫合約以及亞太地區政策支持下精密農業的推廣,都推動了這一領域的擴張。供應商目前正將機器學習加速器整合到檢測器中,以實現現場分析,從而無需笨重的工作站,並將決策週期縮短至毫秒級。同時,小型化簡介相機在尺寸、重量和功耗方面實現了數量級的顯著降低,使其能夠應用於智慧型手機診斷等民用領域。美國政府為高光譜影像(HSI)任務提供的超過13億美元的專案資金,確保了持續的需求,並加速了國防級技術在民用領域的應用。

全球高光譜影像市場趨勢與洞察

整合基於人工智慧的片上分析

邊緣神經網路直接整合在檢測器陣列上,將即時吞吐量提升至超過 1.2 Tb/s。美國的 HyperThreAD 計畫使無人機搭載的攝影機能夠在數秒內識別化學威脅。這些進步降低了延遲和頻寬負載,從而實現了農業分類機、回收機器人和工業生產線的自主品質評估。 Imec 的薄膜濾波器堆疊技術實現了 CMOS 等級製造,在降低單位成本的同時提高了影格速率,加速了其更廣泛的商業應用。因此,人工智慧檢測器有望成為物流、採礦和食品安全等領域下一代自主平台的核心。

VNIR/SWIR感測器成本快速降低

自 2024 年以來,InGaAs 晶圓產量比率加倍,共用後端封裝生產線已實現與智慧型手機相機類似的經濟效益,推動平均售價每年下降近 40%。預計到 2027 年,高光譜成像器將與中階 CMOS 成像器的成本持平,並且在許多生產線上,高光譜遙測相機將從資本分支轉變為耗材。加州大學戴維斯分校的壓縮感知原型機在不影響光譜保真度的前提下,將光學元件的品質降低了 100 倍,進一步強化了這個通縮趨勢。隨著價格的下降,高光譜影像市場在汽車油漆檢測、電子產品故障分析和工業計量等領域正蓬勃發展。

持續的校準漂移

在沒有空調的工廠裡,溫度變化、振動和空氣污染物會導致頻譜校準每月劣化超過2%。基於LED的自校準器可以為高階機載有效載荷實現5%以內的不確定度,但其5萬美元的價格限制了其在高階系統中的應用。用於食品分類和回收工廠的低成本設備仍然需要每週檢驗,這會擾亂工作流程並降低操作人員的信心。隨著用戶對免維護正常運作的需求日益成長,那些整合密封光學元件、板載參考來源和自適應演算法的供應商有機會贏得市場佔有率。

細分市場分析

到2025年,相機部分將佔高光譜影像市場50.40%的佔有率,其中服務供應商的成長速度最快,複合年成長率(CAGR)高達16.05%。承包解決方案將感測器租賃、飛行操作和頻譜打包在一起,使最終用戶無需經歷漫長的學習過程。 Headwall Photonics與GRYFN的合作體現了這種向託管服務的轉變,該服務將無人機搭載的設備與雲端原生控制面板相結合。國防和採礦業的監管審核越來越要求供應商獲得認證,這進一步推動了該領域的成長。系統整合商透過為機器視覺維修客製化光學和照明設備來維持市場需求。例如,美國公司QinetiQ為監視和環境任務建立頻譜庫,並透過多年合約下的軟體更新和資訊服務來獲利。

到2025年,由於推掃式掃描儀在長時間曝光下仍能保持較高的信噪比(SNR),在高光譜影像市場中佔據了61.20%的佔有率。礦業勘測和衛星載重依賴線掃描方法的均勻照明和頻譜保真度。同時,簡介式成像儀的複合年成長率(CAGR)達到了16.35%,它能夠在單幀影像中捕捉完整的資料立方體,從而實現手持操作,並在農業田間調查和醫療內視鏡檢查中實現無模糊運動成像。

Specim公司的FX系列熱成像推掃式攝影機就是一個混合創新的典範,它將中波段覆蓋與機械掃描結合,用於工業爐和火炬的監測。可調濾波器裝置可在特定波段提供足夠的化學物質檢測能力,而擺掃式設計仍效用於需要精確高空平台。

區域分析

北美在高光譜遙測成像市場佔據領先地位,預計2025年將佔據37.50%的市場。這主要得益於強勁的國防預算撥款、美國國立衛生研究院(NIH)的醫學影像津貼以及創投對軍民兩用航太公司的創業投資投入。五年期的聯邦成像合約確保了穩定的收入來源,而矽谷的新興企業正在利用超過2400萬美元的A輪資金籌措來建造低地球軌道衛星星系。與加拿大在北極監測方面的跨境合作也推動了感測器訂單和資料處理服務需求的成長。

亞太地區以16.6%的複合年成長率實現了最快成長,這主要得益於中國的“數位鄉村計劃”和印度的“農業技術補貼計劃”,這兩項計劃都要求即時報告作物健康狀況。以蘇州、新竹和大阪為中心的區域半導體產業叢集正在縮短前置作業時間並降低成本,當地的無人機整合商提供的光譜載荷組合價格低於1萬美元。政府機構也正在對高光譜成像技術進行實地測試,用於河川污染監測和稀土元素資源探勘,從而提高多年專案規劃的透明度。

歐洲在循環經濟法規的指導下保持均衡成長。歐盟2030年城市垃圾回收率達到65%的目標,為光學分類機創造了穩定的需求。同時,歐洲太空總署支持的哥白尼計畫擴建計畫正在為高光譜遙測衛星服務資金籌措。德國正在推動工業自動化,法國專注於葡萄園病害預測,北歐國家則利用高光譜成像技術對木材品質進行評級。區域資料主權規則允許本地雲端服務提供者提供符合規範的分析解決方案,從而增強了國內價值的保留。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 整合基於人工智慧的片上分析

- VNIR/SWIR感測器的成本迅速下降

- 在亞太地區擴大精密農業項目

- 美國/國防高級研究計劃局 (DARPA) 為天基高光譜衛星群計畫提供的資金

- 用於智慧型手機診斷的緊湊型簡介 HSI

- 強制性ESG資訊揭露推動礦產等級檢驗

- 市場限制

- 現場部署單元中持續存在的校準漂移

- 高昂的資本投入和資料儲存成本

- 美國和中國對感測器核心部件的出口管制制度

- 缺乏特定領域的頻譜庫

- 專利分析

- 技術概述 - 應用領域

- 監測

- 遙感探測

- 機器視覺/光學

- 醫學診斷/檢查

- 產業價值鏈分析

- 監管環境

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 對宏觀經濟趨勢的市場評估

第5章 市場規模與成長預測

- 報價

- 相機

- 系統整合商

- 服務供應商

- 透過技術

- 推掃式

- 簡介

- 可調濾波器

- 成像傅立葉變換紅外光譜

- 擺掃式

- 按波長

- 可見光和近紅外線(NIR)

- 短波紅外線 (SWIR)

- 中波紅外線 (MWIR)

- 長波紅外線 (LWIR)

- 按最終用戶行業分類

- 食品和農業

- 衛生保健

- 防禦

- 採礦與計量

- 回收利用

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- ASEAN

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東地區

- 非洲

- 南非

- 埃及

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Galileo Group, Inc.

- BaySpec Inc.

- Specim Spectral Imaging Ltd

- Corning Incorporated

- Surface Optics Corporation

- Headwall Photonics Inc.

- Resonon Inc.

- HyperMed Imaging Inc.

- Norsk Elektro Optikk AS

- Cubert GmbH

- XIMEA GmbH

- HinaLea Imaging(TruTag Technologies Inc.)

- ITRES Research Limited

- Telops Inc.

- Brimrose Corporation of America

- Teledyne DALSA Inc.

- ClydeHSI Ltd.

- ChemImage Corporation

- Diaspective Vision GmbH

- Applied Spectral Imaging Inc.

第7章 市場機會與未來展望

The hyperspectral imaging market size in 2026 is estimated at USD 299.82 million, growing from 2025 value of USD 259.30 million with 2031 projections showing USD 619.28 million, growing at 15.62% CAGR over 2026-2031.

This expansion rests on falling VNIR/SWIR sensor prices, Defense Department contracts for space-borne constellations, and policy-backed precision-agriculture roll-outs across Asia Pacific. Vendors now embed machine-learning accelerators inside detectors, enabling in-field analytics that eliminate bulky workstations and shorten decision cycles to milliseconds. At the same time, miniaturized snapshot cameras shrink size, weight, and power by two orders of magnitude, opening consumer channels such as smartphone diagnostics. Program funding that exceeds USD 1.3 billion for U.S. government HSI missions guarantees recurring demand and accelerates spillover of defense-grade technology into civilian applications.

Global Hyperspectral Imaging Market Trends and Insights

Integration of AI-based on-chip analytics

Edge neural networks now reside directly on detector arrays, pushing real-time throughput beyond 1.2 Tb/s. The U.S. Army's HyperThreAD program demonstrates chemical threat recognition in seconds from UAV-borne cameras. These advances cut latency, reduce bandwidth loads, and enable autonomous quality decisions in agricultural sorters, recycling robots, and industrial process lines. Broader commercial use is accelerating as thin-film filter stacks from Imec allow CMOS-level manufacturing, dropping unit costs while raising frame rates. As a result, AI-enabled detectors are poised to form the core of next-generation autonomous platforms in logistics, mining, and food safety.

Rapid cost erosion of VNIR/SWIR sensors

InGaAs wafer yields have doubled since 2024, and shared back-end packaging lines now mimic smartphone camera economics, pushing average selling prices down nearly 40% per year. Cost parity with mid-range CMOS imagers is expected by 2027, moving hyperspectral cameras from capital expense to consumable tool in many production lines. UC Davis compressive-sensing prototypes cut optics mass by 100X without spectral fidelity loss, reinforcing this deflationary trend. As prices retreat, the hyperspectral imaging market gains traction in automotive paint inspection, electronics failure analysis, and industrial metrology.

Persistent calibration drift

Temperature swings, vibration, and airborne contaminants degrade spectral alignment by more than 2% per month in unconditioned factories. While LED-based self-calibrators keep high-end airborne payloads within 5% uncertainty, their USD 50,000 price tag restricts use to premium systems. Budget units in food sorting and recycling plants still require weekly validation, disrupting workflows and lowering confidence among operators. Vendors that integrate sealed optics, on-board references, and adaptive algorithms are positioned to capture share as users seek maintenance-free uptime.

Other drivers and restraints analyzed in the detailed report include:

- Expanding precision-agriculture programs in APAC

- DoD/DARPA funding for space-borne hyperspectral constellations

- High CAPEX and data-storage costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The cameras segment captured 50.40% of the hyperspectral imaging market share in 2025, while service providers grew the fastest at a 16.05% CAGR. Turnkey models bundle sensor rental, flight operations, and spectral analytics, sparing end-users from steep learning curves. Headwall Photonics' alliance with GRYFN exemplifies this managed-service pivot, pairing UAV payloads with cloud-native dashboards. Regulatory audits in defense and mining increasingly stipulate certified providers, reinforcing the segment's momentum. System integrators sustain demand by customizing optics and illumination for machine-vision retrofits. QinetiQ US, for instance, curates spectral libraries for surveillance and environmental missions, monetizing software updates and data services over multiyear contracts

Pushbroom scanners captured 61.20% of hyperspectral imaging market share in 2025 thanks to high SNR across long dwell times. Mining surveys and satellite payloads rely on the line-scan method's uniform illumination and spectral fidelity. Snapshot imagers, however, posted a 16.35% CAGR, capturing full data cubes in a single frame and enabling handheld, jitter-free operation for field agronomy and medical endoscopy.

Hybrid innovations such as Specim's FX-series thermal pushbroom camera marry mid-wave coverage with mechanical scanning to serve industrial furnaces and flare monitoring. Tunable-filter rigs address chemical sensing where selective bands suffice, while whiskbroom architectures retain relevance on high-altitude platforms demanding pinpoint targeting.

The Hyperspectral Imaging Market Report is Segmented by Offering (Cameras, System Integrator, and Service Provider), Technology (Pushbroom, Snapshot, Tunable Filter, and More), Wavelength (Visible and NIR, SWIR, MWIR, and More), End-User Industry (Food and Agriculture, Healthcare, Defense, Mining and Metrology and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led with 37.50% hyperspectral imaging market size in 2025, driven by strong defense allocations, NIH-funded medical imaging grants, and robust venture capital for dual-use space companies. Federal five-year imagery contracts guarantee steady revenue streams, while Silicon Valley startups tap USD 24 million-plus Series A rounds to build low-Earth-orbit constellations. Cross-border collaboration with Canada on Arctic monitoring generates incremental sensor orders and data-processing services.

Asia Pacific posts the fastest expansion at 16.6% CAGR, propelled by China's Digital Village Initiative and India's agri-tech subsidies, both mandating real-time crop-health reporting. Regional semiconductor clusters around Suzhou, Hsinchu, and Osaka shorten lead times and compress costs, letting local drone integrators bundle spectral payloads below USD 10,000. Governments also field-test HSI for river-pollution tracking and rare-earth exploration, adding multi-year pipeline visibility.

Europe maintains balanced growth anchored in circular-economy regulations. The EU target of 65% municipal-waste recycling by 2030 creates a stable pull for optical sorters, while ESA-backed Copernicus expansion funds hyperspectral satellite services. Germany champions industrial automation, France focuses on vineyard disease prediction, and Nordic countries leverage HSI for timber-quality grading. Regional data-sovereignty rules stimulate local cloud providers to offer compliant analytics stacks, reinforcing domestic value retention.

- Galileo Group, Inc.

- BaySpec Inc.

- Specim Spectral Imaging Ltd

- Corning Incorporated

- Surface Optics Corporation

- Headwall Photonics Inc.

- Resonon Inc.

- HyperMed Imaging Inc.

- Norsk Elektro Optikk AS

- Cubert GmbH

- XIMEA GmbH

- HinaLea Imaging (TruTag Technologies Inc.)

- ITRES Research Limited

- Telops Inc.

- Brimrose Corporation of America

- Teledyne DALSA Inc.

- ClydeHSI Ltd.

- ChemImage Corporation

- Diaspective Vision GmbH

- Applied Spectral Imaging Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Integration of AI-based on-chip analytics

- 4.2.2 Rapid cost erosion of VNIR/SWIR sensors

- 4.2.3 Expanding precision-agriculture programs in APAC

- 4.2.4 DoD/DARPA funding for space-borne HSI constellations

- 4.2.5 Miniaturized snapshot HSI for smartphone diagnostics

- 4.2.6 Mandatory ESG disclosure driving mineral-grade verification

- 4.3 Market Restraints

- 4.3.1 Persistent calibration drift in field-deployable units

- 4.3.2 High CAPEX and data-storage costs

- 4.3.3 US-China export-control regimes on sensor cores

- 4.3.4 Scarcity of domain-specific spectral libraries

- 4.4 Patent Analysis

- 4.5 Technology Snapshot - Applications

- 4.5.1 Surveillance

- 4.5.2 Remote Sensing

- 4.5.3 Machine Vision/Optical

- 4.5.4 Medical Diagnostics/Research

- 4.6 Industry Value Chain Analysis

- 4.7 Regulatory Landscape

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Assessment of Macro-economic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Cameras

- 5.1.2 System Integrator

- 5.1.3 Service Provider

- 5.2 By Technology

- 5.2.1 Pushbroom

- 5.2.2 Snapshot

- 5.2.3 Tunable Filter

- 5.2.4 Imaging FTIR

- 5.2.5 Whiskbroom

- 5.3 By Wavelength

- 5.3.1 Visible and NIR (Near-Infrared)

- 5.3.2 SWIR (Short-Wave Infrared)

- 5.3.3 MWIR (Mid-Wave Infrared)

- 5.3.4 LWIR (Long-Wave Infrared)

- 5.4 By End-user Industry

- 5.4.1 Food and Agriculture

- 5.4.2 Healthcare

- 5.4.3 Defense

- 5.4.4 Mining and Metrology

- 5.4.5 Recycling

- 5.4.6 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 ASEAN

- 5.5.4.6 Rest of Asia Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Galileo Group, Inc.

- 6.4.2 BaySpec Inc.

- 6.4.3 Specim Spectral Imaging Ltd

- 6.4.4 Corning Incorporated

- 6.4.5 Surface Optics Corporation

- 6.4.6 Headwall Photonics Inc.

- 6.4.7 Resonon Inc.

- 6.4.8 HyperMed Imaging Inc.

- 6.4.9 Norsk Elektro Optikk AS

- 6.4.10 Cubert GmbH

- 6.4.11 XIMEA GmbH

- 6.4.12 HinaLea Imaging (TruTag Technologies Inc.)

- 6.4.13 ITRES Research Limited

- 6.4.14 Telops Inc.

- 6.4.15 Brimrose Corporation of America

- 6.4.16 Teledyne DALSA Inc.

- 6.4.17 ClydeHSI Ltd.

- 6.4.18 ChemImage Corporation

- 6.4.19 Diaspective Vision GmbH

- 6.4.20 Applied Spectral Imaging Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

醫療領域近紅外線成像市場:依產品、技術、模式、應用、最終用戶和分銷管道分類-2026年至2032年全球市場預測

醫療領域近紅外線成像市場:依產品、技術、模式、應用、最終用戶和分銷管道分類-2026年至2032年全球市場預測 2026年全球頻譜成像市場報告高光譜影像系統市場:依產品類型、技術、頻譜範圍及應用分類-2026-2032年全球市場預測農業高光譜影像市場:按平台、感測器、應用和最終用戶分類-2026-2032年全球市場預測2026年全球高光譜影像系統市場報告

2026年全球頻譜成像市場報告高光譜影像系統市場:依產品類型、技術、頻譜範圍及應用分類-2026-2032年全球市場預測農業高光譜影像市場:按平台、感測器、應用和最終用戶分類-2026-2032年全球市場預測2026年全球高光譜影像系統市場報告 高光譜影像市場規模、佔有率、成長及全球產業分析:按類型和應用分類,區域洞察及2026-2034年預測

高光譜影像市場規模、佔有率、成長及全球產業分析:按類型和應用分類,區域洞察及2026-2034年預測 高光譜成像系統市場:依產品、技術和應用劃分 - 全球預測至 2036 年2026年全球超音波乳化設備市場報告2026-2034年全球醫用高光譜影像系統市場規模、佔有率、趨勢及成長分析報告

高光譜成像系統市場:依產品、技術和應用劃分 - 全球預測至 2036 年2026年全球超音波乳化設備市場報告2026-2034年全球醫用高光譜影像系統市場規模、佔有率、趨勢及成長分析報告 高光譜影像系統市場-全球產業規模、佔有率、趨勢、機會、預測:按產品、技術、應用、地區和競爭格局分類,2021-2031年

高光譜影像系統市場-全球產業規模、佔有率、趨勢、機會、預測:按產品、技術、應用、地區和競爭格局分類,2021-2031年