|

市場調查報告書

商品編碼

1907242

奈米感測器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Nanosensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

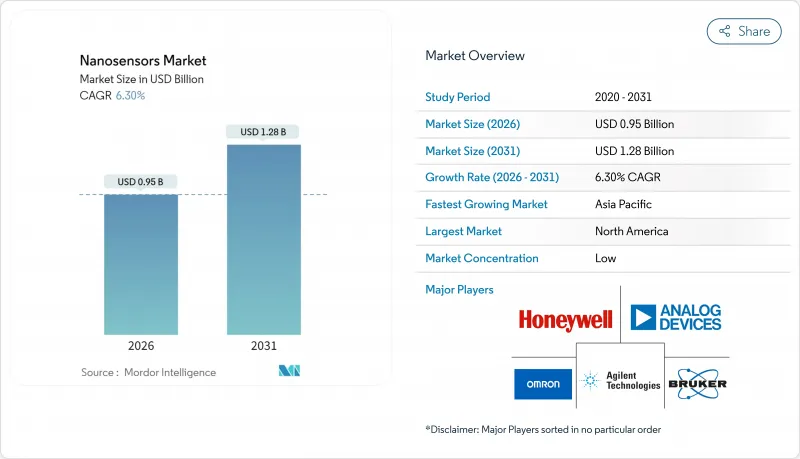

預計到 2025 年,奈米感測器市場價值將達到 8.9 億美元,到 2026 年將成長至 9.5 億美元,到 2031 年將成長至 12.8 億美元,在預測期(2026-2031 年)內複合年成長率為 6.30%。

這一成長主要由三大支柱驅動:電子和醫療保健領域的微型化壓力、量子點製造成本的快速下降以及預測性維護物聯網系統的日益普及。政府的奈米技術計畫、照護現場技術的應用以及國防領域對微量爆炸物檢測的需求,持續擴大奈米感測器的潛在市場。隨著大型半導體公司透過垂直整合來確保單壁奈米碳管的供應,競爭日益激烈,而一些專注於超選擇性生化感測的利基開發商則致力於此。同時,監管機構正在製定奈米毒理學指南,一旦最終定稿,預計將加快產品核可。

全球奈米感測器市場趨勢與洞察

電子設備的微型化及其在穿戴式裝置中的整合

消費品和醫療設備製造商正在將尺寸小於100奈米的感測元件應用於產品中,這些元件能夠在不增加設備體積的情況下追蹤生物標記。蘋果公司最新健康手錶整合了奈米感測器陣列,可連續監測血糖值和血氧飽和度,展現了商業性可行性,預計到2027年將帶來2億美元的潛在額外收入。三星的專利申請暗示了智慧型手機中即時過敏原檢測技術的潛力,而航太零件也在利用奈米感測器測量密閉迴路境中的應力。美國食品藥物管理局(FDA)對穿戴式醫療設備的快速核准流程縮短了產品推出週期,使創新者能夠獲得先發優勢。

政府資助的奈米技術調查計畫

公共支出支撐著長期需求。美國國家奈米技術舉措已為2024年累計18億美元,其中約四分之一用於感測研究。中國的「十四五」規劃和歐盟的「地平線歐洲」計畫也投入了類似的資源用於量子點和奈米碳管設施建設,從而創造了對奈米感測器基板的強勁需求。國防機構已將這項技術視為戰略性技術,即使在景氣衰退時期也保障了其預算,並確保了採購合約的穩定供應。

複雜奈米製造擴充性的瓶頸

50奈米以下的微影製程需要極紫外線曝光設備,每台設備造價高達2億美元,不僅令資本預算捉襟見肘,也限制了全球產能。產量比率低於60%,僅為典型半導體生產線良率的三分之一,導致單位成本高。台積電公開報告稱,缺陷密度挑戰導致生產成本比預期高出三倍。這些限制因素促使企業採用混合架構,削弱了全奈米級解決方案的性能優勢。

細分市場分析

到2025年,化學奈米感測器將佔據奈米感測器市場32.95%的主導佔有率,主要得益於醫療診斷和環境檢測領域需求的成長。物理奈米感測器則因航太對高解析度壓力和應變測量的需求而成為該領域成長最快的產品,年複合成長率(CAGR)達到7.08%。生物奈米感測器利用單分子檢測技術進行藥物監測,並在精準醫療領域佔有一席之地。混合型奈米感測器將化學選擇性與生物特異性相結合,例如雅培公司用於同時篩檢多種生物標記的原型產品。監管機構對分析化學的日益深入理解正在推動化學奈米感測器核准,而機械工程領域的標準化則加速了物理感測器的應用。

同時,先進的表面功能化方法正在模糊類別界限,並推動跨學科應用。物理感測器受益於成熟的微機電系統(MEMS)工藝,降低了單位成本,吸引了汽車原始設備製造商(OEM)的注意。化學裝置在水質監測領域持續獲得應用,因為分子識別在水質監測中至關重要。生物奈米感測器則繼續瞄準重症監護環境,這使其較高的價格也顯得合理。

區域分析

到2025年,北美將佔據奈米感測器市場30.95%的收入佔有率,這主要得益於國防合約、FDA核准的醫療設備以及蓬勃發展的創業融資生態系統。光是美國在2024年就為奈米感測器的研發撥款3.4億美元。加拿大的量子點工廠和墨西哥經濟高效的電子組裝完善了該地區的供應鏈。監管部門的快速核准程序促進了市場准入,但嚴格的環境法規也帶來了高昂的合規成本。

預計到2031年,亞太地區將以7.86%的複合年成長率成長,縮小與北美地區的差距。中國23億美元的感測器計畫、日本的「社會5.0」智慧城市計畫以及韓國的K-Semiconductor Belt計畫都在推動國內製造業的發展。低廉的營運成本吸引了全球製造業外包。新加坡和台灣地區供應高精準組件,而印度則在售後服務和校準領域嶄露頭角。

歐洲汽車和工業領域對奈米感測器的需求仍然強勁,其中德國在汽車排放氣體檢測領域主導。 REACH法規將延長認證週期,但精通合規的供應商將從中受益。法國和英國正在投資研發資金,用於國防相關的奈米感測器計畫。中東和非洲地區正在油田監測領域推廣應用奈米感測器,其耐用性在該領域具有很高的價值。南美洲則相對落後,目前僅限於一些專門的採礦和環境修復試點計畫。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 電子設備小型化和穿戴式設備的整合

- 政府資助的奈米技術調查計畫

- 照護現場的快速擴張

- 工業預測性維護物聯網應用激增

- 國防部門對微量爆炸物和核子生化探測的需求

- 改善量子點成本曲線

- 市場限制

- 複雜奈米製造可擴展性的瓶頸

- 奈米毒理學標準監管方面的延誤

- 高濕度場環境中的訊號漂移

- 集中高純度單壁奈米碳管(SWCNTs)的供應鏈

- 供應鏈分析

- 監管環境

- 技術展望

- 宏觀經濟因素如何影響市場

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 競爭對手之間的競爭

- 替代品的威脅

第5章 市場規模與成長預測

- 按類型

- 生物奈米感測器市場

- 化學奈米感測器市場

- 物理奈米感測器市場

- 透過使用

- 衛生保健

- 家用電子電器

- 航太/國防

- 汽車和工業

- 發電

- 其他終端用戶產業

- 透過技術

- 電化學

- 光學

- 電磁學

- 壓電

- 奈米力學

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東地區

- 非洲

- 南非

- 埃及

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Agilent Technologies Inc.

- Analog Devices Inc.

- OMRON Corporation

- Honeywell International Inc.

- Bruker Corporation

- Texas Instruments Inc.

- Lockheed Martin Corporation

- STMicroelectronics NV

- Robert Bosch GmbH

- Samsung Electronics Co. Ltd.

- Medtronic plc

- Universal Biosensors Inc.

- Hoffmann-La Roche Ltd.

- Nanowear Inc.

- AerBetic LLC

- Applied Nanodetectors Ltd.

- BreathDX Ltd.

- Inanon Bio Inc.

- LamdaGen Corporation

- Vista Therapeutics Inc.

- GBS Inc.

- Applied Nanotech Inc.(PEN Inc.)

- Oxonica Limited

- Beijing ALT Technology Co.

- NanoWorld AG

- Sensonor AS

- Synkera Technologies Inc.

第7章 市場機會與未來展望

The nanosensors market was valued at USD 0.89 billion in 2025 and estimated to grow from USD 0.95 billion in 2026 to reach USD 1.28 billion by 2031, at a CAGR of 6.30% during the forecast period (2026-2031).

This growth rests on three pillars: miniaturization pressures across electronics and healthcare, steep cost declines in quantum dot fabrication, and the widening adoption of predictive maintenance IoT systems. Government nanotechnology programs, point-of-care diagnostic rollouts, and defense demand for trace-explosive detection continue to broaden the addressable nanosensors market. Competitive intensity is rising as semiconductor leaders integrate vertically to secure a single-wall carbon nanotube supply, while niche developers focus on ultra-selective biochemical sensing. Simultaneously, regulators are drafting nano-toxicology guidelines that could accelerate product clearances once finalized.

Global Nanosensors Market Trends and Insights

Miniaturization of Electronics and Wearables Integration

Consumer and medical device makers are embedding sub-100 nm sensing elements that track biomarkers without enlarging device form factors. Apple's latest health watch integrates nanosensor arrays for continuous glucose and oxygen-saturation monitoring, illustrating commercial readiness and spurring a USD 200 million incremental addressable revenue by 2027. Samsung patent filings point to real-time allergen detection in smartphones, while aerospace components adopt nanosensors to measure strain in space-constrained environments. Faster FDA reviews for wearable medical devices shorten launch cycles, allowing innovators to capture early-mover advantages.

Government-Funded Nanotech Research Programs

Public spending anchors long-range demand. The U.S. National Nanotechnology Initiative earmarked USD 1.8 billion in 2024, with nearly one-quarter of the funding allocated to sensing research. China's 14th Five-Year Plan and the EU's Horizon Europe pour matching resources into quantum-dot and carbon-nanotube facilities, creating reliable demand for nanosensor substrates. Defense agencies treat the technology as strategic, insulating budgets even in downturns and ensuring a steady pipeline of procurement contracts.

Complex Nanofabrication Scalability Bottlenecks

Sub-50 nm lithography demands extreme-ultraviolet tools that cost USD 200 million each, pressing capital budgets and capping global output capacity. Yield rates remain below 60%, which is three times lower than the standard for semiconductor lines, thereby inflating unit economics. TSMC's public disclosures reveal defect-density hurdles that triple production costs versus projected metrics. These constraints force blended architectures that dilute the performance edge of fully nanoscale solutions.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Expansion of Point-of-Care Diagnostics

- Surge in Industrial Predictive-Maintenance IoT Deployments

- Regulatory Lag on Nano-Toxicology Standards

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Chemical nanosensors held a dominant 32.95% share of the nanosensors market in 2025, driven by strong uptake in medical diagnostics and environmental testing. Physical variants registered a 7.08% CAGR, the fastest in class, fueled by aerospace demand for high-resolution pressure and strain measurement. Biological nanosensors occupy a niche in precision therapeutics, leveraging single-molecule detection for the monitoring of drugs. Hybrid devices now merge chemical selectivity with biological specificity, as evidenced by Abbott prototypes that simultaneously screen multiple biomarkers. Regulatory familiarity with analytical chemistry provides chemical nanosensors with a smoother path to approval, while mechanical engineering standards expedite the deployment of physical sensors.

In parallel, advanced surface-functionalization methods blur category lines, enabling cross-disciplinary applications. Physical sensors benefit from maturing MEMS processes that cut per-unit costs, drawing interest from automotive OEMs. Chemical devices remain favored in water-quality monitoring where molecular discrimination is crucial. Biological nanosensors continue to target intensive-care environments that justify premium pricing.

The Nanosensors Market Report is Segmented by Type (Biological Nanosensors, Chemical Nanosensors, and More), End-Use Verticals (Healthcare, Consumer Electronics, Aerospace and Defense, and More), Technology (Electrochemical, Optical, Electromagnetic, Piezoelectric, and More), and Geography (North America, South America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 30.95% of the nanosensors market revenue in 2025, driven by defense contracts, FDA-approved medical devices, and a robust venture funding ecosystem. The U.S. Department of Defense alone budgeted USD 340 million for nanosensor research and development in 2024. Canada's quantum-dot plants and Mexico's cost-efficient electronics assembly complement the region's supply chain. Regulatory fast-track programs expedite market entry, but stringent environmental rules impose significant compliance costs.

Asia-Pacific is projected to expand at an 7.86% CAGR through 2031, narrowing the gap with North America. China's USD 2.3 billion sensor initiative, Japan's Society 5.0 smart-city agenda, and South Korea's K-Semiconductor Belt foster domestic fabrication lines. Lower operating costs attract global outsourced manufacturing. Singapore and Taiwan supply high-precision assemblies, while India positions for aftermarket services and calibration.

Europe maintains solid demand from automotive and industrial players, with Germany spearheading vehicle emission sensing and the Netherlands focusing on scientific instrumentation. REACH regulations prolong certification cycles, yet they reward suppliers who are well-versed in compliance. France and the United Kingdom channel research funds into defense-aligned nanosensor programs. The Middle East and Africa exhibit a nascent uptake in oil-field monitoring, where nanosensor durability yields premium margins. South America lags, confined to specialized mining and environmental remediation pilots.

- Agilent Technologies Inc.

- Analog Devices Inc.

- OMRON Corporation

- Honeywell International Inc.

- Bruker Corporation

- Texas Instruments Inc.

- Lockheed Martin Corporation

- STMicroelectronics N.V.

- Robert Bosch GmbH

- Samsung Electronics Co. Ltd.

- Medtronic plc

- Universal Biosensors Inc.

- Hoffmann-La Roche Ltd.

- Nanowear Inc.

- AerBetic LLC

- Applied Nanodetectors Ltd.

- BreathDX Ltd.

- Inanon Bio Inc.

- LamdaGen Corporation

- Vista Therapeutics Inc.

- GBS Inc.

- Applied Nanotech Inc. (PEN Inc.)

- Oxonica Limited

- Beijing ALT Technology Co.

- NanoWorld AG

- Sensonor AS

- Synkera Technologies Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Miniaturisation of electronics and wearables integration

- 4.2.2 Government-funded nanotech research programmes

- 4.2.3 Rapid expansion of point-of-care diagnostics

- 4.2.4 Surge in industrial predictive-maintenance IoT deployments

- 4.2.5 Defence demand for trace-explosive and CBRN detection

- 4.2.6 Quantum-dot cost curve improvements

- 4.3 Market Restraints

- 4.3.1 Complex nanofabrication scalabilty bottlenecks

- 4.3.2 Regulatory lag on nano-toxicology standards

- 4.3.3 Signal drift in high-humidity field environments

- 4.3.4 Supply-chain concentration of high-purity SWCNTs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Intensity of Competitive Rivalry

- 4.8.5 Threat of Substitute Products

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Biological Nanosensors

- 5.1.2 Chemical Nanosensors

- 5.1.3 Physical Nanosensors

- 5.2 By End-use Verticals

- 5.2.1 Healthcare

- 5.2.2 Consumer Electronics

- 5.2.3 Aerospace and Defence

- 5.2.4 Automotive and Industrial

- 5.2.5 Power Generation

- 5.2.6 Other End-user Verticals

- 5.3 By Technology

- 5.3.1 Electrochemical

- 5.3.2 Optical

- 5.3.3 Electromagnetic

- 5.3.4 Piezoelectric

- 5.3.5 Nanomechanical

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 South-East Asia

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Egypt

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Agilent Technologies Inc.

- 6.4.2 Analog Devices Inc.

- 6.4.3 OMRON Corporation

- 6.4.4 Honeywell International Inc.

- 6.4.5 Bruker Corporation

- 6.4.6 Texas Instruments Inc.

- 6.4.7 Lockheed Martin Corporation

- 6.4.8 STMicroelectronics N.V.

- 6.4.9 Robert Bosch GmbH

- 6.4.10 Samsung Electronics Co. Ltd.

- 6.4.11 Medtronic plc

- 6.4.12 Universal Biosensors Inc.

- 6.4.13 Hoffmann-La Roche Ltd.

- 6.4.14 Nanowear Inc.

- 6.4.15 AerBetic LLC

- 6.4.16 Applied Nanodetectors Ltd.

- 6.4.17 BreathDX Ltd.

- 6.4.18 Inanon Bio Inc.

- 6.4.19 LamdaGen Corporation

- 6.4.20 Vista Therapeutics Inc.

- 6.4.21 GBS Inc.

- 6.4.22 Applied Nanotech Inc. (PEN Inc.)

- 6.4.23 Oxonica Limited

- 6.4.24 Beijing ALT Technology Co.

- 6.4.25 NanoWorld AG

- 6.4.26 Sensonor AS

- 6.4.27 Synkera Technologies Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

奈米感測器市場規模、佔有率、趨勢和預測:按類型、技術、應用和地區分類,2026-2034年

奈米感測器市場規模、佔有率、趨勢和預測:按類型、技術、應用和地區分類,2026-2034年 奈米感測器市場:2026-2032年全球市場預測(依感測器類型、技術、材料、應用、終端用戶產業和部署模式分類)

奈米感測器市場:2026-2032年全球市場預測(依感測器類型、技術、材料、應用、終端用戶產業和部署模式分類) 2032 年奈米感測器市場預測:按類型、材料、技術、應用和地區進行的全球分析

2032 年奈米感測器市場預測:按類型、材料、技術、應用和地區進行的全球分析 奈米位置感測器市場報告:至2031年的趨勢、預測與競爭分析

奈米位置感測器市場報告:至2031年的趨勢、預測與競爭分析 中東和非洲的奈米感測器 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030)亞太地區奈米感測器:市場佔有率分析、產業趨勢和成長預測(2025-2030)北美化學感測器:市場佔有率分析、產業趨勢、統計、成長預測(2025-2030)北美奈米感測器:市場佔有率分析、行業趨勢和成長預測(2025-2030)歐洲奈米感測器:市場佔有率分析、產業趨勢、成長預測(2025-2030)

中東和非洲的奈米感測器 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030)亞太地區奈米感測器:市場佔有率分析、產業趨勢和成長預測(2025-2030)北美化學感測器:市場佔有率分析、產業趨勢、統計、成長預測(2025-2030)北美奈米感測器:市場佔有率分析、行業趨勢和成長預測(2025-2030)歐洲奈米感測器:市場佔有率分析、產業趨勢、成長預測(2025-2030)