|

市場調查報告書

商品編碼

1907231

鉿:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Hafnium - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

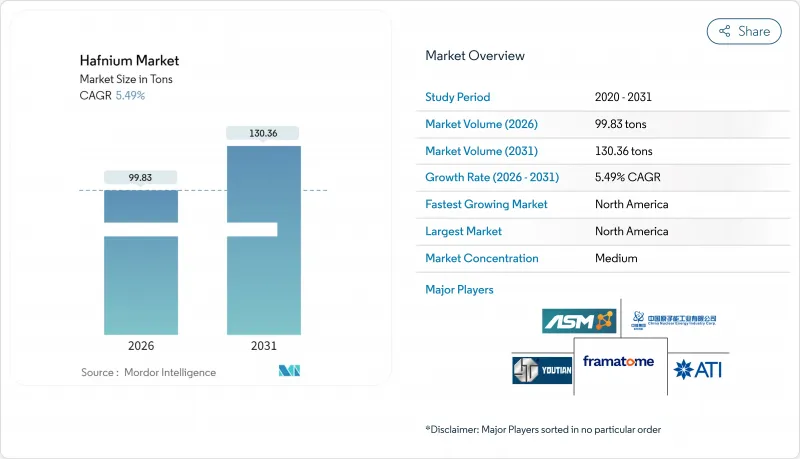

預計到 2026 年,鉿市場規模將達到 99.83 噸,高於 2025 年的 94.63 噸,預計到 2031 年將達到 130.36 噸。

預計從 2026 年到 2031 年,其複合年成長率將達到 5.49%。

這一成長動能是由三個因素共同推動的:尖端晶片中電晶體閘極尺寸的不斷縮小、航太對超高溫材料的需求,以及核能發電廠升級改造對中子吸收控制棒的需求。此外,用鉿取代錸的超合金、向3奈米邏輯節點的轉變,以及核子反應爐運營商的戰略儲備,都在推動需求成長。在供應方面,精煉產品的生產僅限於少數幾家工廠,這加劇了寡頭壟斷,並放大了地緣政治風險和定價權的影響。法國法馬通公司、美國ATI公司、中國煉油商和俄羅斯供應商每年總共僅供應70-75噸初級產品,使得下游用戶極易受到關稅波動和出口限制的影響。

全球鉿市場趨勢與分析

在3奈米以下邏輯節點,對高介電常數(高κ)介質氧化鉿的需求正在激增。

由於傳統材料在氧化層厚度小於1奈米時無法抑制漏電流,半導體製造商正從二氧化矽閘極介質過渡到氧化鉿柵極介質。台積電(TSMC)提交的一項專利申請表明,氧化鉿層與氧化鑭的組合可以擴展平面尺寸,從而推動半導體向2026年設定的2奈米節點目標持續邁進。除了傳統電晶體之外,鐵電氧化鉿鋯薄膜的介電常數可超過900,為低功耗嵌入式記憶體和電容器結構鋪平了道路。這些技術創新是維持莫耳定律的關鍵基礎,並正在推動全球鉿市場的穩定成長。

利用超高溫陶瓷快速擴大可重複使用運載火箭的規模

在可重複使用的運載系統中,火箭彈尖瓦和喉部襯套會在超過2000°C的溫度下經歷反覆的再入循環。碳化鉿的熔點約為3890°C,具有無與倫比的抗氧化性能,倫敦帝國學院的雷射加熱試驗已證實了這一點。摻雜5.7%或以上碳化鉿的碳基複合材料可將燒蝕損失降低近一半,延長火箭零件的使用壽命。隨著民用和國防項目的飛行頻率不斷提高,採購負責人正在將鉿陶瓷應用於火箭鼻錐、控制面和引擎襯套,這進一步刺激了鉿市場的需求。

由於依賴鋯的聯產,導致供應瓶頸

鉿僅在鋯中間體的加工過程中產生,通常以50:1的質量比提取。這使得產能擴張取決於鋯的經濟效益。鋯礦蘊藏量主要集中在南非、澳洲和莫三比克,因此礦砂供應的衝擊會對鉿的供應產生連鎖反應。由於分離工廠僅限於法國、美國、中國和俄羅斯,工廠停產或政策變化會迅速導致全球供需失衡。高資本密集度進一步限制了新進者,並加劇了鉿市場的集中度。

細分市場分析

由於碳化鉿具有無與倫比的熔點,且在火箭噴管嵌件和高超音速飛行器前緣等領域有著成熟的應用,預計到2025年,碳化鉿的消費量的48.20%。依材料類型分類,碳化鉿的市佔率幾乎佔鉿市場總量的一半。雖然氮化物衍生物有望實現更低的燒蝕損失,但市場對純碳化鉿的需求仍然強勁。因此,全球鉿市場的噸位穩定性取決於碳化鉿的供應量。

隨著晶圓廠向3nm製程過渡並逐步推進2nm生產,氧化鉿預計將在2031年前以6.05%的複合年成長率實現最快成長。閘極堆疊技術的應用、鐵電記憶體原型開發以及電容器技術的創新,正推動氧化鉿的需求遠超歷史基準值。該領域的成長軌跡表明,在預測期內,氧化鉿的市場佔有率將持續擴大,尤其是在晶片收入預計在未來十年內達到1兆美元的情況下。製造商目前要求雜質閾值達到兆分之一的水平,這進一步推動了對能夠供應電子級氧化鉿的供應商的需求。

鉿市場報告按類型(氧化鉿、碳化鉿及其他)、應用(超合金、光學塗層、核能、等離子切割及其他)和地區(亞太地區、北美地區、歐洲地區、世界其他地區)進行細分。市場預測以噸為單位。

區域分析

北美仍將維持全球最大區域需求佔有率,預計2025年將佔38.55%。儘管國內產量有限,但預計到2031年仍將以5.66%的複合年成長率成長。雖然ATI位於奧勒岡州和猶他州的工廠生產特殊合金,但2017年至2020年期間,美國買家的進口來源仍是德國(42%)、法國(29%)和中國(24%)。波音公司的民航機項目、國防渦輪機大修項目以及英特爾的先進晶圓廠正在推動鉿市場消費成長。

歐洲憑藉法國的傑瑞煉油廠擁有戰略優勢,該煉油廠約佔歐洲煉油廠產能的43%,年產量約30噸。空中巴士、賽峰和羅爾斯·羅伊斯等公司依賴歐洲國內供應,而德國作為美國主要出口國的歷史地位也凸顯了該地區在加工技術方面的專長。法國近期徵收的出口關稅減少了跨大西洋貿易,但由於飛機訂單和核子反應爐維護週期延長,歐盟內部的需求仍然穩定。

在亞太地區,隨著日本和韓國擴大核能發電能和半導體生產線,需求成長正在加速。中國既是生產國又是新興消費國,其雙重身分導致供應摩擦,因為國內半導體工廠和火箭製造商對氧化鉿和碳化鉿的消費量不斷成長。台灣在採用3奈米邏輯電路的主導以及越南稀土元素的開發,凸顯了該地區日益增強的自給自足能力。整體而言,從快堆控制棒到可重複使用火箭的耐熱瓦,鉿在亞太地區的應用範圍十分廣泛,這支撐了該地區鉿市場的強勁前景。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 用於亞3奈米邏輯節點的高κ介電材料氧化鉿的需求激增

- 利用鉿基超高溫陶瓷快速擴大可重複使用運載火箭的規模

- 核能營運商在燃料多樣化背景下的戰略儲備

- 成本壓力日益增大,航太高溫合金中錸的替代問題日益凸顯。

- 市場限制

- 由於依賴鋯的聯產,導致供應瓶頸

- 由於中國煉油產能過剩,油價飆升

- 分離和提取困難

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 定價分析

第5章 市場規模與成長預測

- 按類型

- 氧化鉿

- 碳化鉿

- 其他類型(包括金屬鉿)

- 透過使用

- 超合金

- 光學鍍膜

- 核能

- 等離子切割

- 其他用途

- 按地區

- 生產分析

- 法國

- 美國

- 中國

- 世界其他地區

- 消費分析

- 亞太地區

- 中國

- 印度

- 日本

- 亞太其他地區

- 北美洲

- 美國

- 北美其他地區

- 歐洲

- 法國

- 德國

- 俄羅斯

- 其他歐洲地區

- 世界其他地區

- 亞太地區

- 生產分析

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- ACI Alloys

- American Elements

- ATI

- Australian Strategic Materials Ltd

- Baoji ChuangXin Metal Materials Co. Ltd(CXMET)

- China Nuclear JingHuan Zirconium Industry Co., Ltd

- CMP JSC

- Framatome(EDF)

- Nanjing Youtian Metal Technology Co.,Ltd

- Phelly Materials Inc.

第7章 市場機會與未來展望

Hafnium market size in 2026 is estimated at 99.83 tons, growing from 2025 value of 94.63 tons with 2031 projections showing 130.36 tons, growing at 5.49% CAGR over 2026-2031.

This growth momentum flows from three converging forces: shrinking transistor gate dimensions in leading-edge chips, aerospace demand for ultra-high-temperature materials, and nuclear fleet upgrades that require neutron-absorbing control rods. Superalloys that replace rhenium with hafnium, the march toward 3-nm logic nodes, and strategic stockpiling by reactor operators collectively widen demand. On the supply side, refined output is confined to a handful of facilities, reinforcing an oligopolistic structure that compounds geopolitical risk and pricing power. France's Framatome, the United States' ATI, Chinese refiners, and Russian suppliers together deliver only 70-75 tons of primary product annually, leaving downstream users exposed to tariff shifts and export controls.

Global Hafnium Market Trends and Insights

Surging Demand for High-κ Dielectric Hafnium Oxides in 3-nm and Below Logic Nodes

Chipmakers are shifting from silicon dioxide to hafnium oxide gate dielectrics because the older material cannot suppress leakage when oxide thickness drops below 1 nm. Patents filed by Taiwan Semiconductor Manufacturing Company illustrate how hafnium oxide layers paired with lanthanum oxide extend planar scaling and enable continued progress toward 2-nm nodes slated for 2026. Beyond conventional transistors, ferroelectric hafnium-zirconium oxide films deliver dielectric permittivity above 900, opening doors for low-power embedded memory and capacitor architectures. These breakthroughs anchor an essential pathway for sustaining Moore's Law, driving steady growth for the hafnium market worldwide.

Rapid Scale-up of Reusable Launch Vehicles Using Ultra-High-Temperature Ceramics

Reusable launch systems subject leading-edge tiles and rocket throat inserts to repeated re-entry cycles exceeding 2,000 °C. Hafnium carbide, with a melting point near 3,890 °C, offers unmatched oxidation resistance, as validated through laser-heating studies at Imperial College London. Carbon-carbon composites doped with more than 5.7% hafnium carbide cut ablation losses nearly in half, extending component life in launch vehicles. As commercial and defense programs accelerate sortie rates, procurement managers are embedding hafnium ceramics into nose cones, control surfaces, and engine liners, pulling incremental tons into the hafnium market.

Supply Bottlenecks from Zirconium Co-production Dependency

Hafnium emerges only when zirconium intermediates are processed, typically at a 50:1 mass ratio, making capacity additions hostage to zirconium economics. Since zirconium ore reserves reside mainly in South Africa, Australia, and Mozambique, supply shocks in mineral sands cascade into hafnium availability. With separation plants limited to France, the United States, China, and Russia, any outage or policy shift quickly tightens global balances. Capital intensity further restricts new entrants, perpetuating concentration in the hafnium market.

Other drivers and restraints analyzed in the detailed report include:

- Strategic Stockpiling by Nuclear-Fleet Operators Amid Fuel Diversification

- Aerospace Superalloy Substitution for Rhenium Under Cost Inflation Pressure

- Volatile Price Spikes Driven by China-Centric Refining Capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The carbide category captured 48.20% of 2025 volumes, thanks to its unmatched melting point and proven use in rocket throat inserts and hypersonic leading edges. This dominance accounts for nearly half of the hafnium market size allocated to material types. Although nitrided derivatives promise even lower ablation losses, foundational demand remains anchored in pure hafnium carbide. The global hafnium market, therefore, leans on carbide stability for baseline tonnage.

Hafnium oxide is charting the fastest 6.05% CAGR to 2031 as fab lines transition to 3-nm and move toward 2-nm production. Gate-stack adoption, ferroelectric memory prototypes, and capacitor innovations lift oxide volumes well above historical baselines. The segment's trajectory hints at a growing slice of hafnium market share across the forecast horizon, especially as chip revenue aims toward USD 1 trillion by decade-end. Fabricators now specify parts-per-trillion impurity thresholds, putting a premium on suppliers able to deliver electronics-grade oxide.

The Hafnium Report is Segmented by Type (Hafnium Oxide, Hafnium Carbide, and Other Types), Application (Super Alloy, Optical Coating, Nuclear, Plasma Cutting, and Other Applications), and Geography (Asia-Pacific, North America, Europe, and Rest of the World). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

North America controlled 38.55% of global demand in 2025, the largest share by region, and is on course for a 5.66% CAGR through 2031 despite limited indigenous production. ATI's Oregon and Utah operations produce specialty alloys, yet U.S. buyers still sourced 42% of imports from Germany, 29% from France, and 24% from China during 2017-20. Boeing's civil airframe programs, defense turbine overhaul schedules, and Intel's advanced fabs anchor consumption growth in the hafnium market.

Europe wields strategic leverage through France's Jarrie refinery, which holds roughly 43% of refined capacity and turns out nearly 30 tons per year. Airbus, Safran, and Rolls-Royce rely on this domestic supply, while Germany's historical role as the leading exporter to the United States highlights the region's processing specialization. Recent French export fees have tightened trans-Atlantic trade, but intra-EU demand remains steady amid aircraft backlog and rising reactor maintenance cycles.

Asia-Pacific's uptake accelerates as Japan and South Korea boost nuclear output and semiconductor lines. China's dual status as both producer and rising consumer introduces supply friction, since domestic fabs and launch-vehicle builders increasingly capture oxide and carbide volumes. Taiwan's leadership in 3-nm logic adoption and Vietnam's rare-earth development underscore the region's growing self-sufficiency aspirations. Overall, regional diversity in end uses, from control rods in fast reactors to thermal tiles on reusable rockets, keeps the hafnium market outlook constructive across Asia-Pacific.

- ACI Alloys

- American Elements

- ATI

- Australian Strategic Materials Ltd

- Baoji ChuangXin Metal Materials Co. Ltd (CXMET)

- China Nuclear JingHuan Zirconium Industry Co., Ltd

- CMP JSC

- Framatome (EDF)

- Nanjing Youtian Metal Technology Co.,Ltd

- Phelly Materials Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand for high-κ dielectric hafnium oxides in 3-nm and below logic nodes

- 4.2.2 Rapid scale-up of reusable launch vehicles using hafnium-based ultra-high-temperature ceramics

- 4.2.3 Strategic stock-piling by nuclear-fleet operators amid fuel diversification

- 4.2.4 Aerospace super-alloy substitution for rhenium under cost-inflation pressure

- 4.3 Market Restraints

- 4.3.1 Supply bottlenecks from zirconium co-production dependency

- 4.3.2 Volatile price spikes driven by China-centric refining capacity

- 4.3.3 Difficulties in Seperation and Extraction

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

- 4.6 Price Analysis

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Hafnium Oxide

- 5.1.2 Hafnium Carbide

- 5.1.3 Other Types (including Hafnium Metal)

- 5.2 By Application

- 5.2.1 Super Alloy

- 5.2.2 Optical Coating

- 5.2.3 Nuclear

- 5.2.4 Plasma Cutting

- 5.2.5 Other Applications

- 5.3 By Geography

- 5.3.1 Production Analysis

- 5.3.1.1 France

- 5.3.1.2 United States

- 5.3.1.3 China

- 5.3.1.4 Rest of the World

- 5.3.2 Consumption Analysis

- 5.3.2.1 Asia-Pacific

- 5.3.2.1.1 China

- 5.3.2.1.2 India

- 5.3.2.1.3 Japan

- 5.3.2.1.4 Rest of Asia-Pacific

- 5.3.2.2 North America

- 5.3.2.2.1 United States

- 5.3.2.2.2 Rest of North America

- 5.3.2.3 Europe

- 5.3.2.3.1 France

- 5.3.2.3.2 Germany

- 5.3.2.3.3 Russia

- 5.3.2.3.4 Rest of Europe

- 5.3.2.4 Rest of the World

- 5.3.2.1 Asia-Pacific

- 5.3.1 Production Analysis

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ACI Alloys

- 6.4.2 American Elements

- 6.4.3 ATI

- 6.4.4 Australian Strategic Materials Ltd

- 6.4.5 Baoji ChuangXin Metal Materials Co. Ltd (CXMET)

- 6.4.6 China Nuclear JingHuan Zirconium Industry Co., Ltd

- 6.4.7 CMP JSC

- 6.4.8 Framatome (EDF)

- 6.4.9 Nanjing Youtian Metal Technology Co.,Ltd

- 6.4.10 Phelly Materials Inc.

7 Market Opportunities and Future Outlook

- 7.1 Reusable spacecraft heat-shield tiles

- 7.2 Hafnium oxide nanoparticles as radiosensitizers

- 7.3 White-space and Unmet-need Assessment