|

市場調查報告書

商品編碼

1907209

歐洲阻燃劑市場:市場佔有率分析、行業趨勢、統計數據和成長預測(2026-2031 年)Europe Flame Retardant Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

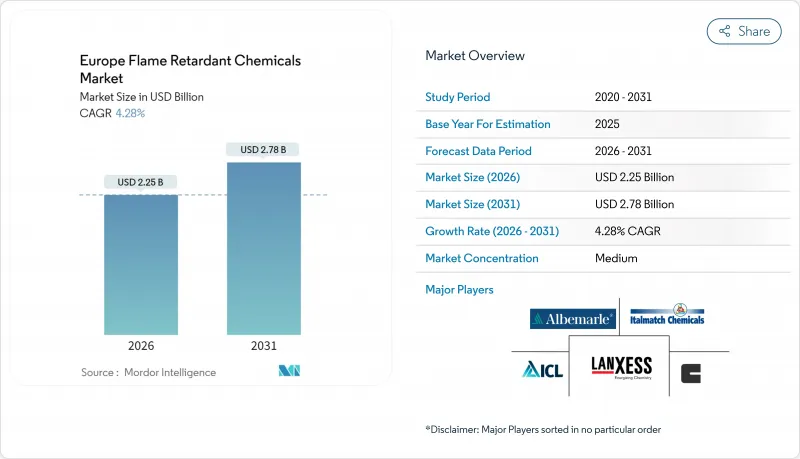

預計到 2026 年,歐洲阻燃化學品市場規模將達到 22.5 億美元。預計該市場規模將從 2025 年的 21.6 億美元成長到 2031 年的 27.8 億美元,2026 年至 2031 年的複合年成長率為 4.28%。

遵守REACH法規、加速替代溴化體係以及持續的基礎設施投資,使該地區成為無鹵添加劑的可靠需求中心。外牆板、隔熱材料和結構鋼的防火安全標準日益嚴格,主導了建築業的消費量。半導體自給自足措施和5G部署的推動,促進了電子產品生產,使其成為第二個成長引擎。同時,中歐和東歐的汽車輕量化和家具製造業正在擴大下游基本客群。隨著生產商競相推出符合歐盟即將推出的永續性目標的無PFAS且符合循環經濟標準的等級產品,市場競爭日益激烈。儘管原物料價格波動仍然是鋁、磷和鎂市場的主要風險因素,但採購多元化策略和不斷成長的庫存緩衝在一定程度上緩解了供應方面的波動。

歐洲阻燃劑市場趨勢及分析

消費性電子電氣製造增加

歐洲電子產品製造商正根據歐盟晶片法規縮短供應鏈並加強回流計畫。電池外殼和5G無線單元的無鹵素法規對阻燃材料的選擇有嚴格的要求。朗盛近期推出的聚醯胺6型阻燃劑在1.5毫米厚度下即可達到UL 94 V-0阻燃等級,幫助汽車製造商在不影響安全性的前提下整合厚電池蓋。 USB-C線纜的配方商目前正採用無鹵素TPE混合物,這些混合物也符合資料中心和充電基礎設施所需的低菸、零鹵素標準。此外,歐盟對優先採購符合歐盟標準的聚合物的半導體製造廠提供的補貼也推動了市場需求的成長。

加強建築業的消防法規

2024 年修訂的 EN 13501-1 標準和各國關於木質覆材的法規規定,低層住宅建築幕牆必須達到 D-s3,d1 等級,而高層建築則維持 B-s3,d1 等級。這促進了膨脹型防火塗料和氫氧化鋁填充材的應用。德國建築技術研究所 (DIBt) 擴大了其認可的不燃板材和塗層鋼系統清單,為製造商提供了清晰的認證途徑。綠色交易下的計劃指定使用磷基膨脹型防火系統,該系統兼具阻燃性和低碳排放的優點。新建住宅和維修必須滿足更高的標準,而法律體制則確保了長期消費成長。

溴化阻燃劑的毒性問題

歐洲化學品管理局 (ECHA) 在 2025 年 4 月的報告中指出,幾種溴代芳香族化合物可能需要獲得授權,這進一步加劇了市場對這些化學物質的抗拒。北歐部長理事會繼續推動 2030 年前全面淘汰這些化學品,進一步降低了市場需求。雖然溴化體系在薄壁電子產品領域表現出色,但替代壓力迫使原始設備製造商 (OEM) 重新設計機殼形狀,並轉向雙協同磷氮系統。合規成本和潛在的過時風險抑制了對新建溴化物生產能力的投資,導致未來銷售損失。

細分市場分析

在歐洲阻燃化學品市場中,無鹵阻燃系統佔88.83%的佔有率。預計到2031年,該市場將以5.52%的複合年成長率成長,這主要得益於磷基、無機和氮基阻燃劑的日益普及,這些阻燃劑簡化了建築和電子行業REACH法規的合規性。氫氧化鋁因其抑煙性能,在牆板和電線電纜行業佔據最大佔有率,而氫氧化鎂的應用範圍正在擴展到高溫領域。磷基添加劑能夠提高薄壁材料的效率,這對於電動車電池機殼至關重要。

創新活動圍繞著活性磷寡聚物,這些低聚物可聚合形成聚氨酯和環氧樹脂網路,從而防止回收過程中遷移。來自特種化學品領域的新參與企業正在利用金屬膦酸鹽添加劑的協同效應來降低用量,同時保持材料的機械性能。將內部磷生產商垂直整合到高純度衍生物的生產中,提高了成本競爭力,並緩解了價格波動。取得再生原料仍然是一個瓶頸,但德國的初步試驗成功地將回收的聚碳酸酯與25%的包覆磷酸酯混合,在不影響性能的前提下達到了UL-94 V-0標準。

歐洲阻燃化學品市場報告按產品類型(非鹵代阻燃劑和鹵代阻燃劑)、終端用戶行業(電氣電子、建築施工、交通運輸、紡織家具)以及地區(德國、英國、義大利、法國、西班牙、歐洲其他地區)進行細分。市場預測以美元以金額為準。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 消費性電子電氣製造增加

- 加強建築業的消防安全法規

- 中歐及東歐家具及室內裝飾品生產的成長

- 過渡到與循環經濟相容的阻燃添加劑

- 5G電纜和資料中心安裝量激增

- 市場限制

- 人們對溴化阻燃劑的毒性表示擔憂

- 原料價格波動(鋁、磷、鎂礦石)

- 歐盟限制聚合物使用的微塑膠法規尚未訂定

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 依產品類型

- 非鹵素

- 無機物

- 氫氧化鋁

- 氫氧化鎂

- 硼化合物

- 磷

- 氮基

- 其他

- 無機物

- 鹵化

- 溴化合物

- 氯基化合物

- 非鹵素

- 按最終用戶行業分類

- 電氣和電子設備

- 建築/施工

- 運輸

- 紡織品和家具

- 按地區

- 德國

- 英國

- 義大利

- 法國

- 西班牙

- 其他歐洲地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Adeka Corporation

- Albemarle Corporation

- BASF

- Clariant

- DIC Corporation

- Dow

- Eti Maden

- ICL

- Italmatch Chemicals SpA

- JM Huber Corp.(Huber Engineered Materials)

- LANXESS

- MPI Chemie BV

- Nabaltec AG

- RTP Company

- THOR Group

- TOR Minerals

第7章 市場機會與未來展望

The Europe Flame Retardant Chemicals Market size in 2026 is estimated at USD 2.25 billion, growing from 2025 value of USD 2.16 billion with 2031 projections showing USD 2.78 billion, growing at 4.28% CAGR over 2026-2031.

Regulatory alignment with REACH, accelerated replacement of brominated systems, and sustained infrastructure investment make the region a dependable demand center for non-halogenated additives. Construction leads the volume offtake owing to tightened fire-safety rules for cladding, insulation, and structural steel. Electronics production, revitalized by semiconductor sovereignty initiatives and 5G rollouts, adds a second growth engine, while automotive lightweighting and furniture manufacturing in Central and Eastern Europe expand the downstream customer base. Competitive intensity is rising as producers race to launch PFAS-free, circular-economy-ready grades that satisfy upcoming EU sustainability targets. Raw-material price swings in aluminum, phosphorus, and magnesium markets remain the chief risk, yet supply-side volatility is partly cushioned by diversified sourcing strategies and higher inventory buffers.

Europe Flame Retardant Chemicals Market Trends and Insights

Rising Consumer Electrical and Electronics Manufacturing

European electronics producers have intensified reshoring programs that shorten supply lines and align with the EU Chips Act. Flame-retardant selection is governed by halogen-free mandates for battery housings and 5G radio units. Recent polyamide 6 grades introduced by LANXESS achieve UL 94 V-0 at 1.5 mm, helping automakers integrate thicker battery covers without sacrificing safety. Formulators targeting USB-C cables now deploy halogen-free TPE blends that also meet low-smoke zero-halogen criteria, a requirement for data centers and charging infrastructure. Demand strength is reinforced by EU subsidies for local semiconductor fabs that prioritize in-region procurement of compliant polymers.

Stricter Fire-Safety Regulations in Construction

The 2024 update of EN 13501-1 and national rules for wood cladding imposed class D-s3,d1 for low-rise residential facades and maintained B-s3,d1 for taller buildings, spurring uptake of intumescent coatings and aluminum hydroxide fillers. Germany's DIBt expanded its list of non-combustible boards and coated steel systems, giving manufacturers clear pathways for approval. Projects funded under the EU Green Deal specify phosphorus-based intumescent systems that provide both flame retardancy and embodied-carbon reductions. The legal framework locks in long-term consumption growth as new dwellings and retrofits must meet higher standards.

Toxicity Concerns Over Brominated FRs

ECHA signaled potential authorization requirements for several aromatic brominated compounds in its April 2025 report, intensifying market aversion toward this chemistry. The Nordic Council of Ministers continues to lobby for a complete phase-out by 2030, further dampening demand. While brominated systems excel in thin-wall electronics, substitution pressures compel OEMs to redesign housing geometries or shift to dual-synergy phosphorus-nitrogen systems. Compliance costs and potential obsolescence reduce investment appetite for new brominated capacity, lowering future sales.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Furniture and Upholstery Production in CEE

- Shift to Circular-Economy Compliant FR Additives

- Pending EU Microplastics Legislation Limiting Polymer Uses

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Europe flame retardant chemicals market size for non-halogenated systems is equal to 88.83% share. Growth continues at 5.52% CAGR through 2031 as construction and electronics buyers adopt phosphorus, inorganic, and nitrogen chemistries that simplify REACH compliance. Aluminum hydroxide remains volume leader in wallboard and wire-cable owing to its smoke-suppressant action, while magnesium hydroxide penetrates higher-temperature applications. Phosphorus-based additives deliver thin-wall efficiency critical for electric vehicle battery enclosures.

Innovation activity clusters around reactive phosphorus oligomers that polymerize into polyurethane or epoxide networks, preventing migration during recycling. Market entrants from specialty chemicals leverage metal phosphinate-based synergies to lower loading levels, preserving material mechanics. Cost competitiveness improves as captive phosphorus producers forward-integrate into high-purity derivatives, smoothing price spikes. Access to recycled feedstock grades remains a bottleneck; however, pilot trials in Germany demonstrate successful incorporation of reclaimed polycarbonate blended with locked-in phosphorus esters at 25% levels without sacrificing UL-94 V-0 ratings.

The Europe Flame Retardant Chemicals Report is Segmented by Product Type (Non-Halogenated and Halogenated), End-User Industry (Electrical and Electronics, Buildings and Construction, Transportation, and Textiles and Furniture), and Geography (Germany, United Kingdom, Italy, France, Spain, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Adeka Corporation

- Albemarle Corporation

- BASF

- Clariant

- DIC Corporation

- Dow

- Eti Maden

- ICL

- Italmatch Chemicals SpA

- J.M. Huber Corp. (Huber Engineered Materials)

- LANXESS

- MPI Chemie BV

- Nabaltec AG

- RTP Company

- THOR Group

- TOR Minerals

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising consumer electrical and electronics manufacturing

- 4.2.2 Stricter fire-safety regulations in construction

- 4.2.3 Growth in furniture and upholstery production in CEE

- 4.2.4 Shift to circular-economy compliant FR additives

- 4.2.5 Surge in 5G cable and data-center installations

- 4.3 Market Restraints

- 4.3.1 Toxicity concerns over brominated FRs

- 4.3.2 Raw-material price volatility (Al, P, Mg ores)

- 4.3.3 Pending EU micro-plastics legislation limiting polymer uses

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Non-Halogenated

- 5.1.1.1 Inorganic

- 5.1.1.1.1 Aluminum Hydroxide

- 5.1.1.1.2 Magnesium Hydroxide

- 5.1.1.1.3 Boron Compounds

- 5.1.1.2 Phosphorus-based

- 5.1.1.3 Nitrogen-based

- 5.1.1.4 Others

- 5.1.1.1 Inorganic

- 5.1.2 Halogenated

- 5.1.2.1 Brominated Compounds

- 5.1.2.2 Chlorinated Compounds

- 5.1.1 Non-Halogenated

- 5.2 By End-user Industry

- 5.2.1 Electrical and Electronics

- 5.2.2 Buildings and Construction

- 5.2.3 Transportation

- 5.2.4 Textiles and Furniture

- 5.3 By Geography

- 5.3.1 Germany

- 5.3.2 United Kingdom

- 5.3.3 Italy

- 5.3.4 France

- 5.3.5 Spain

- 5.3.6 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Adeka Corporation

- 6.4.2 Albemarle Corporation

- 6.4.3 BASF

- 6.4.4 Clariant

- 6.4.5 DIC Corporation

- 6.4.6 Dow

- 6.4.7 Eti Maden

- 6.4.8 ICL

- 6.4.9 Italmatch Chemicals SpA

- 6.4.10 J.M. Huber Corp. (Huber Engineered Materials)

- 6.4.11 LANXESS

- 6.4.12 MPI Chemie BV

- 6.4.13 Nabaltec AG

- 6.4.14 RTP Company

- 6.4.15 THOR Group

- 6.4.16 TOR Minerals

7 Market Opportunities and Future Outlook

- 7.1 White-space and unmet-need assessment

阻燃化學品市場規模、佔有率和成長分析(按產品類型、最終用戶產業、應用和地區分類)—產業預測(2026-2033 年)

阻燃化學品市場規模、佔有率和成長分析(按產品類型、最終用戶產業、應用和地區分類)—產業預測(2026-2033 年) 阻燃化學品:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)

阻燃化學品:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年) 阻燃化學品:技術與全球市場

阻燃化學品:技術與全球市場